ASX 200 Live Today - Wednesday, 22nd April

The S&P/ASX 200 is set to fall after doubts around US-Iran de-escalation weighed on overnight markets. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Wednesday, April 22. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 sharply lower as healthcare stocks bleed, banks tumble

[2:27 pm] That's a wrap! A very ugly session for the ASX 200, currently down 1.03% and trading at intraday lows. The selling is very company-specific, though the catalysts have led to sector wide contagion, dragging the broader healthcare and financials sector lower. While the local index is tanking, S&P 500 and Nasdaq futures are currently up 0.52% and 0.67% respectively.

Cochlear was absolutely obliterate today, marking its worst session on record. What's interesting is that the earnings downgrade has arguably weighed on other healthcare stocks, with CSL, Mesoblast and Ebos all down 4-5%.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

COH | Cochlear | -39.62% | $101.40 | -60.95% |

4DX | 4DMedical | -8.24% | $4.90 | 1650.00% |

CSL | CSL | -5.17% | $129.92 | -45.53% |

MSB | Mesoblast | -4.57% | $2.20 | 37.19% |

EBO | Ebos Group | -4.05% | $17.51 | -49.11% |

RMD | Resmed | -2.31% | $30.81 | -6.64% |

PME | Pro Medicus | -1.73% | $139.77 | -31.27% |

RHC | Ramsay Health Care | -0.93% | $40.97 | 24.14% |

FPH | Fisher & Paykel | -0.82% | $30.90 | 0.02% |

SIG | Sigma Healthcare | -0.70% | $2.82 | -4.73% |

ANN | Ansell | -0.62% | $27.38 | -5.23% |

TLX | Telix Pharmaceuticals | -0.14% | $14.46 | -42.91% |

SHL | Sonic Healthcare | -0.02% | $20.14 | -19.59% |

Data as at 2:20 pm AEST

Banks are also under pressure after Bank of Queensland's 1H26 result flagged softer-than-expected earnings and net interest margins of 1.67% (vs. Macquarie ests of 1.73%). The 6 bp miss might not seem like much – but reporting a NIM decline when analysts expected growth is a big deal (especially at a time where most market participants would argue banks deserve to trade on lower multiples).

This joins the recent string of soft bank results, including Westpac noting higher loan losses (14-Apr) and NAB flagging $706 million in credit impairments (20-Apr).

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

BOQ | Bank Of Queensland | -8.80% | $6.63 | -7.14% |

JDO | Judo Capital | -6.62% | $1.38 | -18.71% |

BEN | Bendigo & Adelaide Bank | -4.11% | $10.62 | 0.71% |

MQG | Macquarie Group | -3.59% | $232.61 | 29.80% |

CBA | Commonwealth Bank | -2.30% | $175.45 | 9.79% |

ANZ | ANZ Group | -2.04% | $36.52 | 31.51% |

WBC | Westpac | -1.71% | $39.56 | 28.07% |

NAB | National Australia Bank | -1.31% | $40.67 | 20.33% |

Data as at 2:25 pm AEST

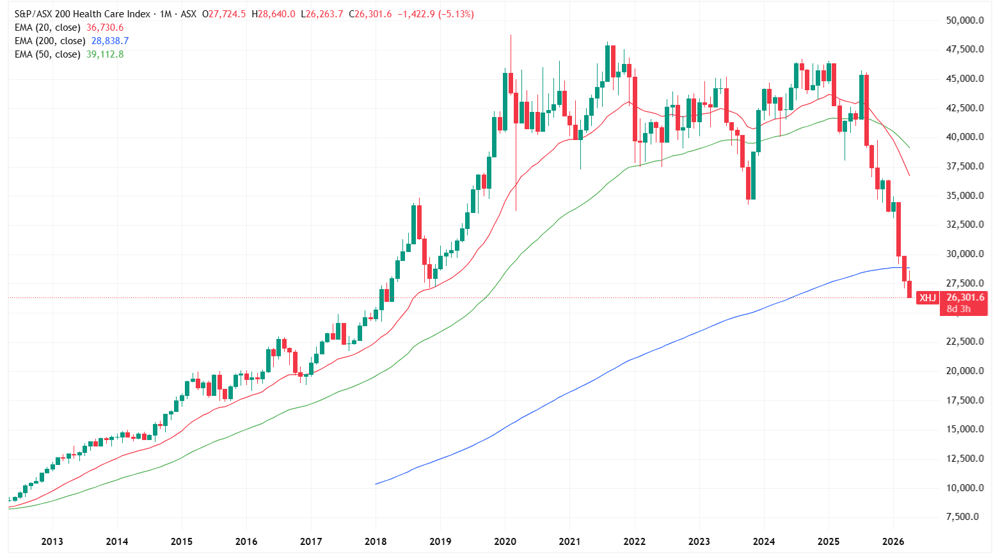

The market's most important sector continues to disappoint, and that's a problem. Weak financial earnings/read throughs are being compounded by a healthcare sector in freefall, now down 22% year-to-date and overtaking tech as the year's worst performer. While Iran remains front and centre, investors must now contend with a softening earnings backdrop for banks and a healthcare sector that looks increasingly broken.

GDG, Cochlear and Virgin under selling pressure

[1:40 pm] The below table observes the S&P/ASX 200 stocks experiencing the largest declines from the open price.

Generation Development Group smashed after a non-price sensitive quarterly update, which noted March quarter FUM up 30% year-on-year to $34.8 billion (but up just 0.8% quarter-on-quarter, so perhaps a slowdown-related selloff). Virgin under pressure amid the bounce in oil prices overnight, Ebos and CSL lower intraday (likely a COH sympathy move), regionals also under pressure from Bendigo Bank's 1H26 miss.

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

GDG | Generation Development Group | -16.14% | $3.69 |

COH | Cochlear | -12.05% | $100.16 |

VGN | Virgin Australia | -6.92% | $2.42 |

4DX | 4DMedical | -6.68% | $4.89 |

NXT | NextDC | -4.73% | $14.22 |

SMR | Stanmore Resources | -4.48% | $2.13 |

EBO | Ebos Group | -4.33% | $17.46 |

CSL | CSL | -4.30% | $130.27 |

BOQ | Bank Of Queensland | -4.05% | $6.63 |

BEN | Bendigo & Adelaide Bank | -3.85% | $10.61 |

Healthcare stocks at the point of no return?

[1:30 pm] Who would've thought that two of the market's healthcare darlings (CSL and Cochlear) would wind up in massive earnings downgrade cycles? The two heavyweights have driven the S&P/ASX 200 Healthcare Index to the lowest since April 2018. The index is now down 22% year-to-date and down 42% since August 2025.

S&P/ASX 200 Healthcare Index monthly chart (Source: TradingView)

Analysts' take on Atlas Arteria

[12:42 pm] Atlas' March quarter update revealed softer-than-expected traffic and revenue outcomes, with group results below consensus, with traffic was essentially flat while revenue increased only marginally, with weakness at APRR and Chicago Skyway partially offset by strong Dulles Greenway performance.

UBS retained Neutral, lowered target from $5.15 to $4.50. Valuation seen as broadly fair given softer operational outcomes, with distributions viewed as unsustainable without material cash flow improvement and large-scale growth investment critical to the bull case.

RBC Capital Markets retained Sector Perform, lowered target from $5.00 to $4.75. Dividend sustainability is constrained by the approaching debt maturity, with traffic weakness seen as broader than fuel cost factors alone and the portfolio in urgent need of new growth opportunities.

Macquarie retained Outperform, lowered target from $5.43 to $5.02. Dulles viewed as a structurally improving asset with strong pricing power, though fuel elasticity effects are likely materialising at APRR, Skyway weakness appears structural, and currency poses a growing threat to distribution sustainability.

Cuscal Chair lifts stake with on-market purchase

[12:41 pm] Elizabeth Proust bought 30,000 shares, lifting her beneficial holding to 180,000 shares (a 20% increase in ownership).

Company page: Cuscal (CCL)

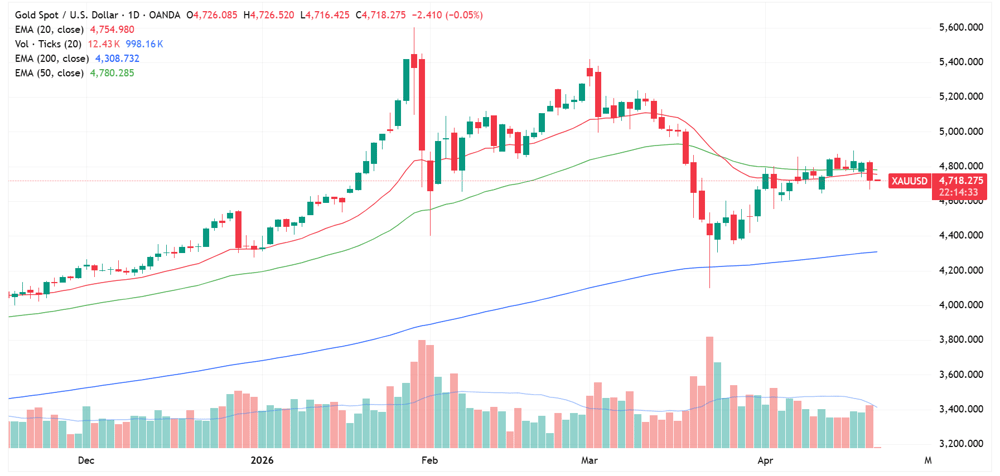

Gold stocks broadly lower

[12:22 pm] A fairly weak session for gold miners, with the S&P/ASX All Ords Gold Index down 2.3%. This follows a 2.1% decline in gold prices overnight to US$4,719/oz.

Ticker | Company | % Chg | Price |

|---|---|---|---|

ALK | Alkane Resources | -4.42% | $1.62 |

WGX | Westgold Resources | -4.28% | $6.16 |

EVN | Evolution Mining | -3.79% | $13.09 |

PNR | Pantoro Gold | -3.46% | $3.77 |

RRL | Regis Resources | -3.32% | $7.43 |

NST | Northern Star Resources | -3.21% | $22.90 |

SBM | St. Barbara | -2.84% | $0.69 |

GMD | Genesis Minerals | -2.69% | $6.50 |

EMR | Emerald Resources | -2.62% | $6.32 |

RMS | Ramelius Resources | -2.38% | $3.91 |

RSG | Resolute Mining | -1.94% | $1.42 |

AMI | Aurelia Metals | -1.85% | $0.27 |

NEM | Newmont | -1.77% | $155.80 |

PRU | Perseus Mining | -1.68% | $5.55 |

CMM | Capricorn Metals | -1.35% | $11.73 |

BGL | Bellevue Gold | -0.86% | $1.72 |

CYL | Catalyst Metals | -0.30% | $6.54 |

MEK | Meeka Metals | 0.00% | $0.15 |

BMR | Ballymore Resources | 0.00% | $0.14 |

BC8 | Black Cat Syndicate | 0.16% | $1.29 |

OBM | Ora Banda Mining | 1.27% | $1.60 |

VAU | Vault Minerals | 1.37% | $4.81 |

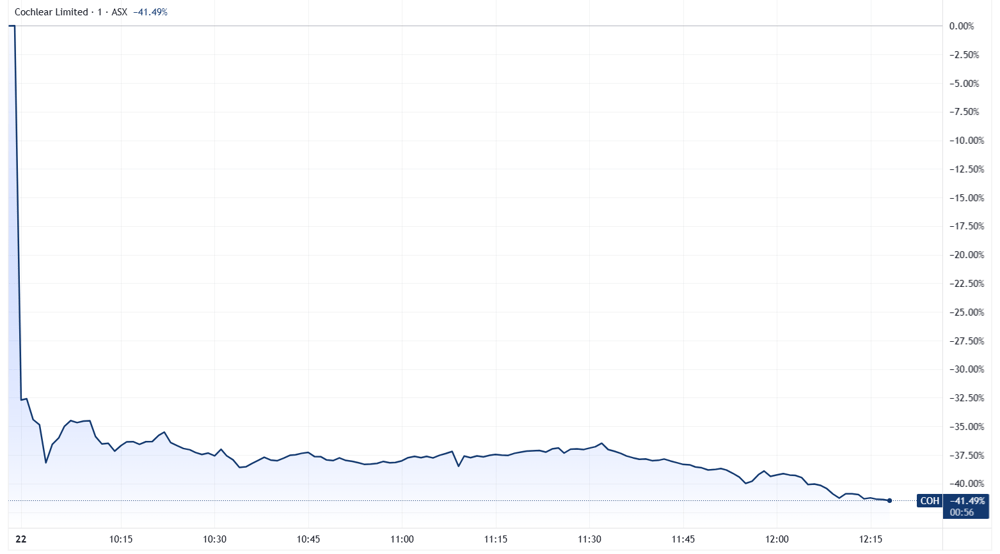

No bounce in sight for Cochlear

[12:20 pm] There's no relief rally for Cochlear, with the stock now down 41% to $98.49, despite opening 32% lower.

Cochlear daily price chart (Source: TradingView)

Analysts' take on Lynas

[11:25 am] Lynas Rare Earths' Q3 result on Tuesday missed market expectations on production and sales due to deliberate process improvements at Kalgoorlie and ramp constraints at Mt Weld. The stock finished 2.1% lower on the day.

UBS retained Buy, lowered target from $23.90 to $23.65. Flagged Kalgoorlie process improvements and an unfavourable mix skewed to lower-margin lanthanum/cerium as the drivers of the production and pricing shortfall, while pointing to downstream magnet capacity as a material earnings opportunity.

JPMorgan retained Overweight, target unchanged at $22.00. Noted realised pricing was helped by a one-month customer contract lag, with current ~8kt annualised run rate sitting well below nameplate, and called out diesel cost reduction from the renewable power station as removing a key historical risk.

Analysts' take on Hub24

[11:25 am] Hub24's Q3 net inflows update on Tuesday was broadly in line with consensus despite a one-off institutional client outflow and adverse market movements, with underlying flows healthy and adviser growth accelerating to a two-year high. The stock still tumbled 8.3% on the day.

Macquarie downgraded to Neutral from Outperform, raised target from $92.75 to $94.50. Flagged record March quarter net inflows (ex-migrations) and top-decile market share expansion, but viewed the superior earnings outlook as insufficient to justify the premium valuation versus peers.

Morgans retained Accumulate, lowered target from $112.40 to $96.50. Highlighted accelerating adviser growth and positive month-to-date market momentum supporting FUA guidance, with the target cut driven by a higher risk-free rate.

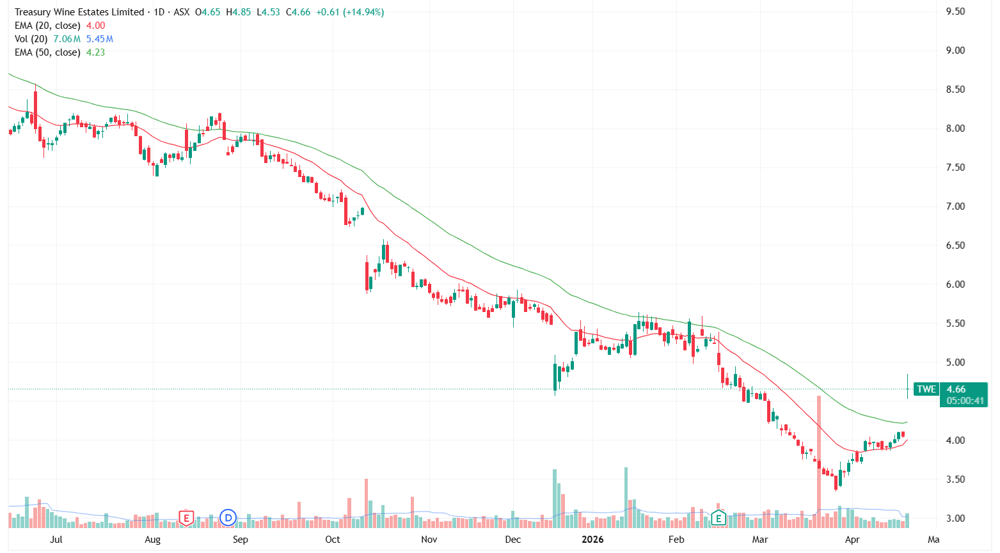

Treasury Wine rallies on Q3 depletion momentum

[11:00 am] Treasury Wine is trading 14.8% higher to a ~6 week high after a Q3 trading update noted positive depletion momentum across its key global markets. While the FY26 guidance was reaffirmed, this was seen as a net positive, given stabilising US market depletions and a solid balance sheet.

The key numbers we noted earlier:

Penfolds depletions in China up 40% year-on-year on a seasonally adjusted basis through Chinese New Year, with momentum continuing to end of 3Q26.

Treasury Americas US market depletions up 9.1% year-on-year in 3Q26, a marked improvement on 1H26 (down 2.6%). California returned to growth following the 1H26 distributor transition

ANZ depletions up 11% and Asia ex-China up 14% on a seasonally adjusted basis

FY26 outlook reiterated, with 2H26 EBITS expected to be higher than 1H26. Middle East conflict not expected to have a material cost impact

New regional operating model effective 1 October 2026, structured across four regions, targets $100m pa of operating cost savings over two to three years, with initial benefits in FY27

TWE has been in a brutal downtrend since October 2024, where the stock price has been effectively moving from the top left of your screen to the bottom right. It dipped as much as ~73% between Oct-24 and Mar-26. Today's rally marks the first meaningful move above the 50-day moving average since late 2024.

Treasury Wine Estates daily price chart (Source: TradingView)

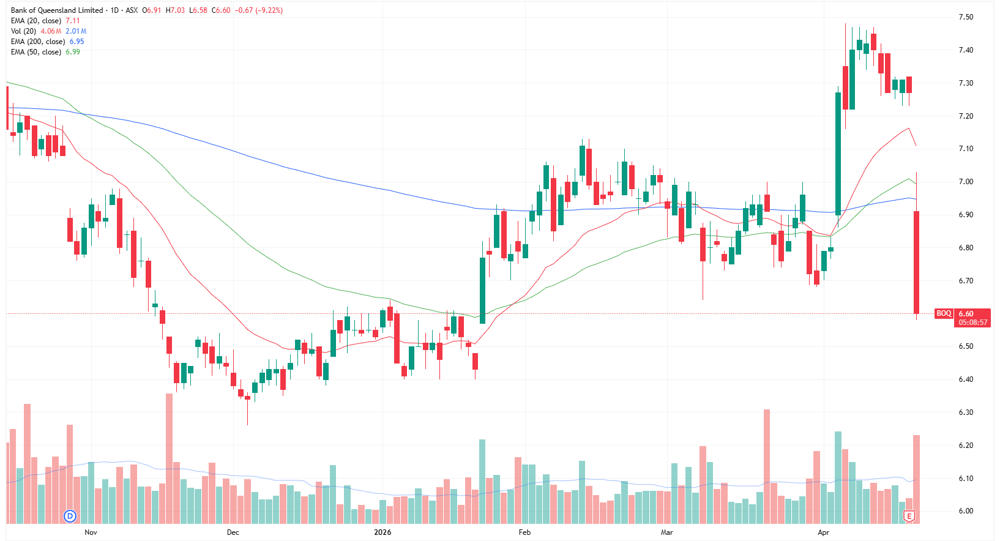

Bank of Queensland tumbles on margin miss

[10:53 am] A very heavy day for Bank of Queensland shares, currently down 9% to the lowest since 22 January.

As we noted this morning, earnings was slightly softer-than-expected, but the main driver of today's share price weakness was likely the NIM miss.

Cash NPAT down 4% to $176m vs $181.7m ests (3% miss)

Net interest income up 4% to $755m vs $766m ests (1% miss)

NIM down 3 bps on 2H25 to 1.67%, reflecting a highly competitive environment and non-repeat of prior half cash rate benefits, partly offset by improved asset mix and funding spreads

NIM of 1.67% represents a wide miss vs. Macquarie ests of 1.73% (Apr-26)

Interim fully-franked DPS up 11% to 20c vs 19.6c ests (2% beat),

Bank of Queensland daily price chart (Source: TradingView)

Cochlear still down 37%

[10:47 am] No bounce in sight for Cochlear, after that abysmal trading update. The stock opened 32% lower ($113.88%) and currently down 38% to $104.15.

This marks the stock's worst one-day decline on record.

Date | Close | % Chg |

|---|---|---|

22/04/2026 | $104.15 | -38.0% |

16/12/2003 | $21.65 | -23.8% |

12/09/2011 | $57.50 | -20.3% |

16/03/2020 | $174.51 | -19.2% |

13/02/2026 | $199.22 | -18.9% |

3/06/2013 | $52.88 | -18.1% |

28/10/1997 | $3.80 | -15.9% |

12/03/2004 | $18.90 | -15.9% |

14/09/2011 | $51.30 | -14.6% |

14/02/2025 | $262.73 | -13.7% |

Top ASX 200 gainers

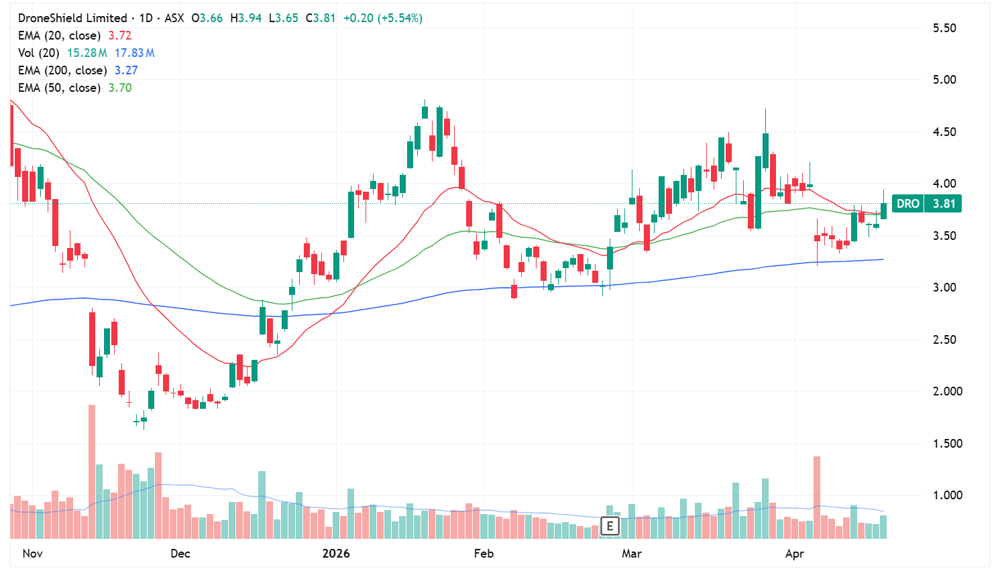

[10:25 am] Shares in Treasury Wine, Ampol and Droneshield higher off the back of positive trading updates, while utilities name like Mercury NZ and Genesis also ticking higher.

Ticker | Company | % Chg | Price |

|---|---|---|---|

TWE | Treasury Wine Estates | 15.80% | $4.69 |

ALD | Ampol | 4.05% | $32.89 |

EOS | Electro Optic Systems | 3.04% | $10.83 |

MCY | Mercury Nz | 2.46% | $5.41 |

GNE | Genesis Energy | 2.44% | $1.89 |

DRO | Droneshield | 2.36% | $3.90 |

SGM | Sims | 1.41% | $20.88 |

VEA | Viva Energy Group | 1.29% | $2.35 |

WTC | Wisetech Global | 1.23% | $46.15 |

A2M | A2 Milk Company | 1.09% | $7.43 |

Top ASX 200 losers

[10:25 am] Cochlear absolutely obliterated, Bank of Queensland also trending lower off the back of weaker-than-expected 1H26 net interest margins. Gold and copper names also down on a pullback in commodity prices overnight.

Ticker | Company | % Chg | Price |

|---|---|---|---|

COH | Cochlear | -36.48% | $106.68 |

GDG | Generation Development Group | -16.74% | $3.83 |

BOQ | Bank Of Queensland | -7.02% | $6.76 |

CSC | Capstone Copper Corp | -4.78% | $12.15 |

4DX | 4DMedical | -4.31% | $5.11 |

EVN | Evolution Mining | -3.46% | $13.13 |

WGX | Westgold Resources | -3.34% | $6.22 |

RSG | Resolute Mining | -3.32% | $1.40 |

ALK | Alkane Resources | -3.13% | $1.64 |

360 | Life360 | -3.05% | $21.61 |

Cochlear crashes 34%

[10:02 am] Cochlear has tumbled 34.5% to $109.80, now trading at the lowest since May 2016. The stock is currently down 58% year-to-date.

A few other numbers to note about the trading update:

FY26 underlying NPAT guidance cut to $290-330m (midpoint $310m) vs prior guidance of $435-460m at the lower end

UBS estimates for FY26 underlying NPAT was $408m (new guidance is a 24% miss at the midpoint)

Cochlear reported $194.8m in underlying NPAT for 1H26, this implies just ~$115m for the second half

This implies a 1H/2H split of 63%/37% (vs. FY25 where the split was 52%/48%)

Global Lithium signs binding term sheet with Lopal

[9:52 am] Global Lithium has secured a multi-part strategic agreement with Chinese lithium processor Jiangsu Lopal Tech, providing project financing support for the Manna Lithium Project alongside a new long-term offtake and asset divestment.

Lopal will subscribe for 13.8 million GL1 shares at $0.52875 per share, raising $7.3m, representing an 11.9% discount to the last close of $0.60

Lopal will provide a US$75m offtake prepayment to fund development, construction and commissioning of Manna, subject to completion of the placement and GL1 making a positive FID

The prepayment carries a 5% annual cost on the outstanding balance with a 12-month grace period from first product supply and a final repayment date four years after supply commences

The 10-year offtake (with a four-year extension option) covers 40% of Manna's annual spodumene production, with GL1 targeting 70,000 tonnes per annum for Lopal

Combined with the existing 30% offtake to Canmax, 70% of production is now committed, leaving the remaining 30% at GL1's discretion

A floor price of US$1,000/tonne CIF applies for the first three years of the offtake with no upside price cap

Lopal will acquire GL1's Marble Bar exploration tenements for total consideration of $14.9m, comprising $11.9m on satisfaction of conditions precedent and a $3.0m contingent payment upon grant of a mining lease over the tenements

Company page: Global Lithium Resources (GL1)

Scentre Group Q1 update: Visitation and sales tracking ahead, FY26 guidance maintained

[9:49 am] Scentre delivered a solid Q1 operating update with visitation, sales and occupancy all trending positively, as the group maintains its FY26 FFO growth target of at least 4%.

Customer visitation of 160 million across 42 Westfield destinations from 1 January to 19 April, up 3.1% or 4.9 million visits on the same period in 2025

Total business partner sales of $7.0bn for Q1 2026, up 5.0%

Portfolio occupancy of 99.8% at 31 March 2026, up 20 bps year-on-year

Capital management activity was active in the period: Settled the 19.9% Westfield Sydney divestment to Australian Retirement Trust for $864m at a 4.69% cap rate, redeemed US$750m of 2030 senior bonds, issued a new $750m 6-year domestic senior note at a credit margin of 1.20%, and divested a $50m interest in the Dexus-managed fund holding a 25% stake in Westfield Chermside

FY26 FFO guidance maintained at at least 23.73 cents per security, representing at least 4.0% growth, with distributions expected to grow 4.0% to 18.43 cents per security

Management acknowledged current geopolitical volatility and its potential impact on the consumer, flagging it is monitoring any flow-through to the business and 2026 outlook

Company page: Scentre Group (SCG)

Meteoric raises $40m at no discount to advance Caldeira rare earths DFS

[9:45 am] Meteoric has secured firm commitments for a $40 million placement priced at $0.17 per share, with proceeds directed toward advancing the Caldeira ionic adsorption clay rare earths project toward a FID in 2026.

Placement of ~235 million shares priced at $0.17, representing nil discount to last close, with the raise described as significantly oversubscribed

Pro-forma cash balance of ~$58m following settlement, based on the 31 March 2026 cash position, providing a well-capitalised runway through key de-risking milestones

Proceeds to fund completion of the Definitive Feasibility Study and Environmental Impact Assessment, front-end engineering and design, land acquisition, early contractor engagement, and near-mine infill drilling to increase Mining Reserve confidence

A nil discount and oversubscription is definitely a good look post-raise. Meteoric also has to digest the good news from yesterday, where USA Rare Earth acquired Brazil’s Serra Verde Group in a US$2.8 billion cash-and-stock deal. This drove peers like Viridis Mining (+28.9%) and Brazilian Rare Earths (+9.1%) sharply higher on Tuesday.

Company page: Meteoric Resources (MEI)

Treasury Wine Estates 3Q26: Depletions momentum improves, new regional operating model

[9:38 am] TWE reaffirmed its FY26 outlook, with 3Q26 depletions growth across key markets. For context, depletions refer to the volume of wine sold by distributors/wholesalers to retailers (as opposed to reporting shipments to distribution channels).

Penfolds depletions in China up 40% year-on-year on a seasonally adjusted basis through Chinese New Year, with momentum continuing to end of 3Q26.

Treasury Americas US market depletions up 9.1% year-on-year in 3Q26, a marked improvement on 1H26 (down 2.6%). California returned to growth following the 1H26 distributor transition

ANZ depletions up 11% and Asia ex-China up 14% on a seasonally adjusted basis

FY26 outlook reiterated, with 2H26 EBITS expected to be higher than 1H26. Middle East conflict not expected to have a material cost impact

New regional operating model effective 1 October 2026, structured across four regions, targets $100m pa of operating cost savings over two to three years, with initial benefits in FY27

Company page: Treasury Wine Estates (TWE)

BHP 3Q25: Iron ore beats, copper guidance lifted to upper half

[9:27 am] BHP delivered a strong March quarter with record WAIO production and iron ore beating ests, while lifting FY26 copper guidance to the upper half and realising ~US$4.8bn from non-core divestments.

Q3 iron ore production of 62.8Mt vs 61.6Mt ests (2% beat)

WAIO production (100%) 69.8Mt vs 65.6Mt ests (6% beat), a record

Copper production 476.8kt vs 482.1kt ests (1% miss)

Met coal production 3.8Mt vs 4.0Mt ests (5% miss)

Energy coal production 4.0Mt vs 3.7Mt ests (8% beat)

FY26 copper guidance of 1,900-2,000kt now expected upper half (vs prior range), driven by Escondida (upper half) and Antamina (increased) offsetting Spence (lowered on variable ore challenges). Samarco now expected at top end. Iron ore (258-269Mt), steelmaking coal (18-20Mt) and energy coal (upper half of 14-16Mt) guidance unchanged

FY26 unit cost guidance improved at Escondida. BMA now guiding to top end of range, while other assets remain unchanged despite higher diesel and consumables costs

Realised ~US$4.8bn in the past month via the Antamina silver streaming deal with Wheaton Precious Metals (US$4.3bn upfront), Carajás divestment (US$240m on completion plus up to US$225m contingent), and cash from the earlier Blackwater/Daunia divestment

Brandon Craig to succeed Mike Henry as CEO from 1 July 2026, after Henry's six and a half years in the role. Craig most recently served as President Americas

Company page: BHP Group (BHP)

DroneShield 1Q26: Record cash receipts, revenue beats 8 April trading update

[9:23 am] DroneShield delivered its second-highest quarterly revenue and record customer cash receipts in 1Q26, with strong momentum carrying over from a record 2025 and committed FY26 revenues already well ahead of the prior corresponding period.

Revenue up 121% to $74.1m, the second-highest quarter on record (behind 3Q25 at $92.9m) and above the 8 April trading update figure of $62.6m due to timing of late March deliveries

Customer cash receipts up 360% to $77.4m, the highest on record

SaaS revenue up 205% to $5.1m (6.9% of revenue), tracking toward the goal of 30% recurring revenue by 2030. All new products carry SaaS with quarterly software updates

Net operating cashflow of $24.1m vs ($17.9m) in PCP, the fourth consecutive quarter of positive net operating cash flow

Cash balance up 13% to $222.8m (up $21.7m on Dec 2025), with no debt and funding available for investment and potential strategic M&A

FY26 committed revenues to date of $154.8m vs $94.4m at 1Q25, with a $59m increase since the start of 2026 driven by repeat and new end-user orders below the $20m materiality threshold

It's been a fairly calm year for Droneshield shares following a massive rip and dip in 2025. The stock is down 3.5% year-to-date.

Company page: DroneShield (DRO)

Bank of Queensland 1H26: Cash NPAT misses, DPS beats, Challenger capital partnership unlocks return

[9:16 am] BOQ's 1H26 cash NPAT came in below consensus, with NIM contracting and expenses up. Though the interim dividend topped consensus and the Challenger equipment finance deal paves the way for a buyback and special dividend.

Cash NPAT down 4% to $176m vs $181.7m ests (3% miss)

Statutory NPAT down 20% to $136m, including a $31m post-tax loss on classification of the equipment finance portfolio as held for sale

Net interest income up 4% to $755m vs $766m ests (1% miss)

NIM down 3 bps on 2H25 to 1.67%, reflecting a highly competitive environment and non-repeat of prior half cash rate benefits, partly offset by improved asset mix and funding spreads

NIM of 1.67% represents a wide miss vs. Macquarie ests of 1.73% (Apr-26)

Interim fully-franked DPS up 11% to 20c vs 19.6c ests (2% beat),

Loan impairment expense of $20m vs $3m in 1H25 (5bps of GLAs), with housing net provision release offset by a single-name exposure in asset finance

Home lending contracted 4% on 2H25, while commercial lending grew 7% on 2H25 (above system)

Company page: Bank of Queensland (BOQ)

South32 Q3 production: Worsley misses ests, FY26 guidance reaffirmed

[9:11 am] South32 reported a mixed March quarter with Worsley Alumina falling short of market expectations following a fatality on site, though commodity price tailwinds and strong performances elsewhere delivered positive net cash generation.

Worsley Alumina production of 886kt vs 924kt ests (4% miss). Work not critical to the safety and stability of Worsley was temporarily suspended following the 14 March fatality, with investigations ongoing

FY26 production guidance maintained across all operations except Australia Manganese, revised 6% lower to 3,000kwmt due to elevated site water levels, wet season rainfall and Tropical Cyclone Narelle

Net cash up US$121m in the quarter to a net cash position of US$96m, after US$158m of growth capex at Hermosa's Taylor zinc-lead-silver project

Brazil Alumina achieved record YTD production, Hillside Aluminium continued to test maximum technical capacity and Mozal transitioned to care and maintenance as planned, exceeding guidance by 3%

Hermosa reached a key FAST-41 federal permitting milestone with issuance of the Final Environmental Impact Statement and Draft Record of Decision. Assessment of project milestones and capex for Taylor to be completed in the June 2026 half

Company page: South32 (S32)

Cochlear set for obliteration

[9:10 am] That earnings downgrade is as ugly as it gets. Here's what I'm thinking about:

Cochlear is down 36% year-to-date but that largely reflects the 19% one-day selloff following its 1H26 result

The 1H26 result was slightly below market expectations across all key metrics

Analysts remain bullish on the stock (which will only amplify today's selloff)

Latest note from UBS (24-Mar) noted recent Cochlear weakness as a "an opportunity, with the business is positioned to deliver a solid earnings recovery over the next 12 months, underpinned by the Nexa launch"

UBS had a Buy rating with a $302.00 target price

The new guidance of $290-330 million represents a ~30% downgrade compared to prior guidance (at the midpoint) and down ~20% compared to FY25 underlying NPAT. As a business that's still priced at 32x, negative growth is not acceptable.

Interestingly, short interest in the stock has been vertical for the last twelve months, though only pushing 6% (so not as bad as some other highly shorted names at 12-15% short interest).

Cochlear short interest (Source: Shortman)

Cochlear slashes FY26 profit guidance by ~30% as developed market volumes disappoint

[8:58 am] Cochlear has cut its FY26 underlying NPAT guidance sharply, citing softness in developed market cochlear implant volumes, Middle East uncertainty, a stronger Australian dollar and restructuring costs.

FY26 underlying NPAT guidance cut to $290-330m (midpoint $310m) vs prior guidance of $435-460m at the lower end, a reduction of ~30%, with the downgrade driven by a combination of volume, FX, margin and one-off cost headwinds

Developed market cochlear implant revenue was flat in Q1 in constant currency, with hospital capacity constraints and reduced hearing aid referral activity weighing on volumes

The US tracked in line until mid-February before declining in March, while Western Europe faces growing surgical waiting lists in the UK and Germany and industrial action in Italy and Spain

FX is a material headwind, with the stronger Australian dollar expected to cost approximately $25m after tax in H2

Additional drags include a roughly $20m net profit impact from lower gross margins due to a reduced production plan, up to $10m from potential Middle East receivables provisioning, and $18-25m in above-the-line costs from a restructuring of the cost base

Emerging markets remain a relative bright spot with solid demand growth, though China is facing a reduction in reimbursement in special access zones that will weigh on premium tier sales in H2

Company page: Cochlear (COH)

Iluka Q1 production misses, Cataby idles and Balranald ramps

[8:56 am] Iluka's Q1 production came in well below estimates, driven by a significant zircon sand miss, though rutile and ilmenite were ahead of expectations.

Total Z/R/SR production down to 47.6Kt vs 58.1Kt ests (18% miss)

Mineral sands revenue of $147m vs $158.3m ests (7% miss)

Zircon sand production of 10.5Kt vs 35.6Kt ests, a substantial miss reflecting the idling of Cataby (no zircon or rutile production) and Balranald still in commissioning with finished goods not expected until H2

Z/R/SR sales of 70.2Kt vs 81.0Kt ests (13% miss), with a further 9Kt of zircon sand rolling into Q2 due to logistics constraints

Q1 weighted average zircon sand price flat quarter-on-quarter at US$1,491/t

Q2 zircon outlook is more constructive, with 50Kt contracted incorporating price increases of up to US$120/t, though after rising logistics costs, the net FOB price uplift is expected to be approximately US$45/t

Net debt at 31 March was $417m for the mineral sands business and $693m non-recourse for the rare earths refinery, where total capex has reached $977m with engineering 99% complete

Company page: Iluka Resources (ILU)

Gold prices tumble on US dollar strength, higher yields

[8:48 am] A very heavy overnight session for gold, with prices down 2.1% to US$4,719/oz. This drove broad weakness across gold miners, with the VanEck Gold Miners ETF down 6.1% and a bellwether name like Newmont down 4.8%. Both closed at session lows.

Gold daily price chart (Source: TradingView)

NZ inflation surprises higher, July RBNZ hike now fully priced

[8:43 am] New Zealand Q1 CPI came in hotter than expected on Tuesday, with markets bringing forward rate hike expectations as the Iran war oil shock is yet to flow through.

Q1 CPI up 3.1% year-on-year vs 2.9% ests, matching Q4's pace and above the top of the RBNZ's 1-3% target band

RBNZ provisionally estimates inflation will accelerate to 4.2% in the current quarter, with ASB flagging a return to the target band is off the cards until mid-2027

Markets are now fully pricing a July rate hike, up from a 75% chance prior to the print

Non-tradables inflation (key domestic pressure gauge) held at 3.5% , showing zero progress

Petrol prices rose 3.5% in the quarter and other fuels/lubricants jumped 11%, but the full Iran war oil shock and flow-through to freight costs will only show up in Q2 data. Q1 business confidence slumped to its lowest since mid-2024, with firms flagging reduced investment and job cuts

Strait of Hormuz remains near-empty as double blockade deepens supply disruption

[8:41 am] Commercial traffic through the Strait of Hormuz has ground to a near-halt under a dual blockade, with oil traders warning the supply disruption is set to worsen.

The waterway is operating under a double blockade: Iran restricting other nations' transits, and the US blocking Tehran-linked shipments

The limited traffic observed is confined to a narrow northern lane near Iranian islands of Larak and Qeshm, the only route Tehran has approved, with most vessels carrying ties to Iran and staying local

Tracking data is likely understating the true disruption as vessels are switching off AIS signals to avoid detection, meaning actual transit figures may be revised higher only when ships resurface days later in distant waters

Kevin Warsh's Fed hearing: Regime change agenda intact but confirmation path unclear

[8:39 am] Warsh used his Senate Banking Committee hearing to lay out a sweeping overhaul agenda for the Fed, though his path to confirmation remains uncertain given political headwinds.

Warsh called for "regime change" at the Fed, arguing the institution has lost credibility with markets and the public, with plans to abandon forward guidance, move away from core PCE as the preferred inflation measure, and revisit the structure of post-meeting press conferences

Denied Trump ever instructed him to commit to a specific rate path, though Democrats including Senator Warren labelled him a "sock puppet," reflecting deep scepticism about his independence

Former Fed Chair Yellen expressed doubt Warsh could sway the FOMC, noting he would need a majority of 11 other votes to change rates and saying "I really don't see the FOMC accepting this in the short run"

Confirmation is in limbo as retiring Republican Senator Tillis has said he will not support any Trump Fed nominee until the administration resolves its investigation into Fed building renovation cost overruns, and Trump on CNBC today reinforced the importance of the probe; a Tillis "no" vote would create a 12-12 deadlock in committee

Prediction markets put the odds of Warsh being sworn in before Powell's term expires on 15 May at just ~30%, meaning the Fed chair role could fall vacant in the near term

Sell-side turns more positive on Q1 earnings season

[8:38 am] JPMorgan and Goldman Sachs have both struck an upbeat tone heading into Q1 reporting, with early metrics tracking well and AI investment viewed as a key driver.

JPMorgan expects a more favourable Q1 season than last quarter, when AI fatigue and capex scrutiny weighed on sentiment. Raised 2026 S&P 500 EPS estimate to $330 (from $315) and 2027 to $385 (from $355)

JPMorgan lifted its year-end S&P 500 target to 7,600, after cutting it to 7,200 from 7,500 last month

Goldman Sachs also targets 7,600 by year-end and expects new highs in the coming months on continued earnings growth, noting 2026 and 2027 consensus estimates have risen 4% since late January. Estimates AI investment will drive around 40% of S&P 500 EPS growth this year

Early Q1 metrics are tracking strong, with S&P 500 blended growth at 13.2%, 86% of reporters beating consensus and an average upside surprise of 11%

US March retail sales beat expectations

[8:38 am] US March retail sales posted their biggest monthly gain in over a year, with broad-based strength across categories despite an oil price shock from the Iran war.

Headline retail sales up 1.7% m/m vs 1.6% ests, with February revised higher to +0.7% (from +0.6%), marking the largest monthly increase since January 2023

Retail sales ex-autos up 1.9% m/m vs 1.4% ests

Control group sales (which feed into GDP) up 0.7% m/m vs 0.2% ests, likely prompting upward revisions to Q1 GDP estimates ahead of the 30 April BEA release

Gains were broad-based, led by a record jump at gas stations (+15.5%) on higher pump prices, followed by furniture (+2.2%), general merchandise (+1.0%), online (+1.0%) and electronics (+0.9%). Excluding gas stations, sales still rose a firm 0.6%

Trump extends Iran ceasefire indefinitely, oil retreats

[8:36 am] Trump announced an indefinite extension of the US-Iran ceasefire at Pakistan's request, though the US naval blockade of Iranian ports remains in place and fresh talks have stalled.

US will maintain its blockade of the Strait of Hormuz, keeping a structural risk premium in energy markets

Path to a lasting deal looks uncertain as Iran refused to send a delegation to the planned second round of talks in Islamabad, citing "unacceptable actions" by the US including the blockade

Tone shifted sharply, with Trump earlier telling CNBC "I expect to be bombing" if conditions were not met before reversing course, underscoring headline risk for energy and broader risk assets

Core sticking points remain unresolved, including Iran's nuclear enrichment program, its regional proxies and control of the Strait of Hormuz, with a senior IRGC commander threatening to destroy regional oil infrastructure if fighting resumes

Good morning!

[8:24 am] ASX 200 futures are down 63 pts (-0.70%) as of 8:30 am AEST.

Major US benchmarks lower and finished near worst levels, down for a second straight day

Markets weighed by lack of Iran de-escalation as ceasefire expiry date is fast approaching

Brent rallied 5.5% to a one-week high of US$99.02, driving a classic yields up, commodities down and stocks down session

Fed Chair nominee Kevin Warsh speaks at the Senate Banking Committee, faced significant questioning on his finances and compliance, Warsh discussed his view on a new Fed inflation framework