ASX 200 Live Today - Tuesday, 3rd February

The S&P/ASX 200 is set to bounce after a four-day skid. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, February 3. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

RBA hikes rates by 25 bps, as expected

[2:30 pm] The RBA raised the cash rate by 25 bps to 3.85% after judging inflation and demand are running stronger than expected, with capacity and labour market pressures still elevated. Here are the key takeaways from the media release

Inflation picked up materially in the second half of 2025 and is expected to remain above target for some time

Private demand strengthened more than expected, driven by household spending and investment, with housing activity and prices also lifting

Financial conditions eased through 2025, credit remains readily available, and earlier rate cuts are yet to fully flow through to demand, prices and wages

Labour market remains a little tight, unemployment lower than expected, underutilisation low, and unit labour costs still high

RBA flagged uncertainty around how restrictive policy is, warning stronger demand and limited supply capacity could add further to inflation

The S&P/ASX 200 was trading around 1.07% higher heading into the RBA meeting, its currently up 0.67%.

ASX 200 higher, off best levels

[1:45 pm] ASX 200 currently 1.05% higher heading into the RBA rate decision at 2:30 pm AEDT.

Tech (+2.1%) index is trading broadly higher, with most names bouncing from 52 week lows, notably Life360 (+4.5%), NextDC (+3.3%), Xero (+2.5%), Technology One (+2.2%)

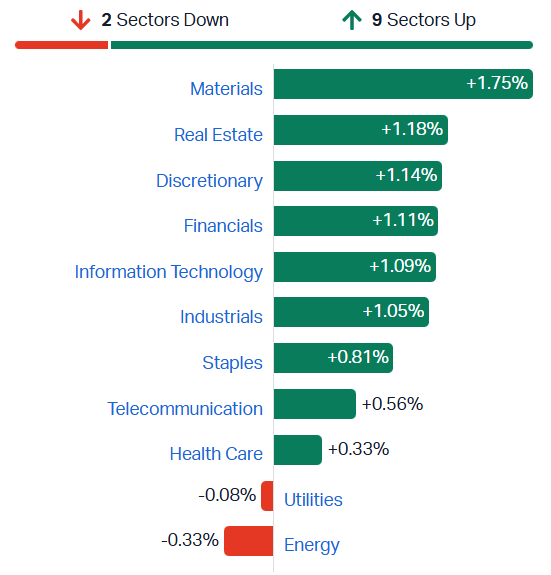

Materials (+1.75%) slipping from session highs of 2.3%. All Ords Gold Index (+3.1%) is still ~10.5% off recent highs

Financials (+0.8%) higher off the back of Big Four gains (up 0.8-1.2%) along with Macquarie (+2.3%)

Defensives lagging, with Utilities (-0.5%), Telcos (+0.4%), Healthcare (+0.4%), Industrials (+0.4%) and Staples (+0.6%) underperforming on a relative basis

Overall, a much needed bounce after four days of softness. The ASX 200 has mustered up a bounce off the 50-day (and also trading above the 20-day). Let's see how the market holds up after the widely expected RBA hike. We'll hang around till then.

Broad-based resource bounce

[1:13 pm] The S&P/ASX 200 Materials index is trading 1.9% higher, slightly off intraday highs. The bounce is relatively broad, with most copper, iron ore, gold, rare earths, lithium and nickel stocks up 2-5%.

Despite the bounce, the Materials index is still 4.7% off last Thursday's record high.

Gold edges higher

[12:29 am] Gold stocks are broadly higher and pushing intraday highs. Gold is bouncing in the current session after falling 14% in the last three days, prices are currently up 4.1% to US$4,854/oz. Newmont is leading the sector, up 5.8%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

NEM | Newmont Corporation | 5.78% | $164.98 |

EVN | Evolution Mining | 5.33% | $14.62 |

OBM | Ora Banda Mining | 4.46% | $1.22 |

RSG | Resolute Mining | 4.28% | $1.34 |

GMD | Genesis Minerals | 3.73% | $7.23 |

PNR | Pantoro Gold | 3.46% | $4.94 |

NST | Northern Star Resources | 3.12% | $27.43 |

RRL | Regis Resources | 2.91% | $7.77 |

RMS | Ramelius Resources | 2.72% | $4.53 |

BGL | Bellevue Gold | 2.31% | $1.77 |

By Warren Masilamony

Federal Court approves RPMGlobal acquisition by Caterpillar

[11:22 am] RPMGlobal shareholders will receive $5.00 per share following the Federal Court’s approval of the acquisition scheme by Caterpillar.

Scheme becomes effective once lodged with ASIC, expected Wednesday, 4 February 2026

ASX quotation of RPM shares to be suspended from close of trading on 4 February 2026

Implementation of the Scheme expected Wednesday, 18 February 2026

Eligible shareholders as at 7:00 pm Sydney time on 11 February 2026 (Scheme Record Date) will receive $5.00 per share

Company page: RPMGlobal (RUL)

Top ASX 200 gainers and losers

[10:31 am] Quite a few growth-oriented names like Droneshield, 4DMedical and Life360 topping the leaderboard this morning. Lynas and Iluka also rallying off the news about a $12 billion US strategic critical-minerals stockpile.

Ticker | Company | % Chg | Price |

|---|---|---|---|

DRO | Droneshield | 7.68% | $3.72 |

4DX | 4DMedical | 5.30% | $3.38 |

NWH | NRW | 5.03% | $5.43 |

CSC | Capstone Copper Corp | 4.90% | $16.70 |

LSF | L1 Long Short Fund | 4.80% | $4.15 |

NEM | Newmont Corporation | 4.68% | $163.26 |

LTR | Liontown | 3.76% | $1.85 |

LYC | Lynas Rare Earths | 3.59% | $15.30 |

360 | Life360 | 3.49% | $28.48 |

ILU | Iluka Resources | 3.26% | $5.23 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

NEU | Neuren Pharmaceuticals | -9.66% | $14.68 |

AZJ | Aurizon | -1.94% | $3.54 |

WGX | Westgold Resources | -1.44% | $6.85 |

MEZ | Meridian Energy | -1.42% | $4.87 |

TLX | Telix Pharmaceuticals | -1.24% | $10.35 |

ASX | ASX | -1.01% | $56.46 |

VNT | Ventia Services Group | -0.86% | $5.75 |

INA | Ingenia Communities | -0.84% | $4.70 |

DMP | Domino's Pizza | -0.79% | $22.66 |

GYG | Guzman Y Gomez | -0.68% | $21.79 |

Broad rally lifts the ASX 200

[10:26 am] ASX 200 up 1.10% in early trade, pushing intraday highs. Strong breadth with ~159 (80%) of constituents trading higher. Energy (-0.09%) stocks holding up relatively well despite a sharp pullback in oil prices overnight. Plenty of sub-sectors sharply higher, including Gold (XGD) up 1.8%, All Tech (XTX) up 1.1%, ASX 200 Banks (XBK) up 1.07%. Some much needed strength after a challenging last four sessions.

ASX 200 sectors (Source: Market Index)

Credit Corp tumbles in early trade

[10:03 am] Credit Corp opened 0.8% higher but tumbled as much as 5.4% within the first minute of trade. The 1H26 result missed across key metrics including NPAT and dividends, though the company reaffirmed its FY26 guidance.

Revenue up 4% to $283.6m vs ests $277.5m (2% beat)

NPAT flat at $44.1m vs ests $48.9m (10% miss)

Interim dividend 32 cps vs. Macquarie ests of 35 cents (8.5% miss)

It'll be interesting to see if the stock can stabilise, given what reads like a solid operational outcome and reaffirmed guidance (or continue trending lower due to the 1H26 miss).

NRW wins multiple infrastructure contracts

[9:42 am] NRW has secured several major contracts across mining and civil projects in WA, commencing in early 2026.

Rio Tinto West Angelas Sustaining Project (WASP): Bulk earthworks contract valued at ~$175m, covering access to five new satellite pits, haul road construction, concrete overpass arch construction, and associated infrastructure, expected completion in 2027

Toodyay Road Reconstruction: “Construct only” contract valued at $46m for road realignment at Jimperding Brook.

Dampier Link Bridge – Stage 2, Dampier Cargo Project: 50:50 JV with Brady Marine and Civil, valued at ~$49m for design and construction of a continuous wharf connecting Dampier Cargo Wharf and Dampier Bulk Handling Facility.

All contracts are scheduled to commence early in 2026 with procurement and construction activities underway

NRW shares have rallied 55% in the last twelve months, though up just 0.4% year-to-date.

Company page: NRW Holdings (NWH)

CBA to recognise $68m provision in 1H26

[9:40 am] CBA has provided details on items affecting 1H26 financial reporting, including provisions, non-recurring income and customer re-segmentation adjustments.

Operating expenses include a $68m pre-tax provision for additional goodwill payments to customers following ASIC’s Better Banking review

Operating income includes $53m pre-tax of non-recurring items, including a milestone from the Commonwealth Insurance sale and a fair value gain on Gemini IPO investment

Customer re-segmentation has led to reclassification of some customers across Retail Banking Services, Business Banking, and Institutional Banking and Markets

Changes do not affect cash NPAT but result in restated financial comparatives for affected divisions

Half-year results will be announced on 11 February 2026

Company page: Commonwealth Bank (CBA)

Xero investor briefing: AI, US payments and Melio integration

[9:32 am] Xero reaffirmed its FY26 guidance at its investor briefing. The presentation also highlighted plans about the company's global AI strategy and US SMB payments growth through the integration of Melio.

Xero is deploying multiple AI agents under JAX on Xero.com to enhance SMB accounting and decision-making capabilities

Melio integration combines accounting with payments to drive deeper US SMB engagement, increase ARPU and grow gross profit per customer

Key integration progress includes embedding Melio bill payments, unifying go-to-market teams, and consolidating US offices to realise operational synergies

Melio expected to reach Adjusted-EBITDA breakeven on a run-rate basis in the second half of FY28

Xero reiterates FY26 guidance, with total operating expenses ~70.5% of revenue

FY28 aspirations include: Significant acceleration in US revenue, aiming to more than double FY25 group revenue excluding anticipated revenue synergies, targeting Rule of 40 outcomes

Xero has been one of the worst performing large cap tech stocks, down 52% since it announced its Melio acquisition on 24 June 2025.

Company page: Xero (XRO)

Credit Corp 1H26 results: US collections and AU/NZ lending growth

[9:20 am] Credit Corp delivered a mixed 1H26, with a revenue beat but NPAT miss, supported by solid US collections and record AU/NZ loan volumes.

Revenue up 4% to $283.6m vs ests $277.5m (2% beat)

NPAT flat at $44.1m vs ests $48.9m (10% miss)

Interim dividend 32 cps, in-line with FY25 interim dividend

US collections up 23% year-on-year, productivity up 41%, payment arrangements book up 5%

AU/NZ loan book growth up 7%, new customer volume up 25%, record half-year lending volume

Reaffirms FY26 NPAT guidance of $100-110m vs. $105m ests, ledger investment $280-330m, gross lending $350-390m

Humm acquisition NBIO ongoing, due diligence not yet commenced

A Macquarie note from Aug-25 had 1H26 revenue ests at $289.7 million, NPAT at $49.9 million and an interim dividend of 35 cents. So 1H26 does read a little soft, however, FY26 NPAT guidance is in-line with consensus and Macquarie ests at the midpoint.

Company page: Credit Corp Group (CCP)

Qoria to merge with Aura

[9:11 am] Qoria shareholders are set to receive 1 Aura CDI for roughly every 17.2 Qoria shares, with the combined entity set to list under the ticker AXQ on the ASX.

Consideration shares represent 35% of Aura’s fully diluted capital before the equity placement.

Aura shareholders have committed to a US$75m (A$108m) equity placement at ~A$12.38 per share, implying $0.72 per Qoria share and a ~$3.0bn pre-money valuation.

Qoria’s board unanimously recommends approval, with directors collectively owning ~3.8% of Qoria voting in favour.

Company page: Qoria (QOR)

RBA set to raise rates amid persistent inflation

[9:07 am] The RBA is widely expected to hike rates at 2:30 pm AEST on Tuesday, reversing its cuts from last year, as inflation remains above target.

Economists widely expect a 25 bp hike, driven by elevated underlying inflation and a tighter labor market.

Recent data shows job ads surged to the highest monthly gain since February 2022, and home-price growth accelerated, highlighting economic strength.

The move would mark the first rate hike since November 2023, likely as a “single insurance” adjustment rather than a series of increases.

US rare earth stocks fade early gains

[9:05 am] US-listed rare earth names finished mostly flat, despite a brief rally driven by news of a potential US$12 billion strategic minerals stockpile.

MP Materials rallied as much as 6.9% but finished the session just 0.5% higher, USA Rare Earths slipped 1.3% despite rallying 16.0% in early trade and Trilogy Metals fell 1.9% vs. session highs of 6.9%.

US to launch $12bn strategic critical-minerals stockpile

[9:02 am] Trump administration is set to launch 'Project Vault' to secure rare earths and key metals for manufacturers.

A $12 billion initiative combines a $10bn loan from US Export-Import Bank with $1.67bn in private capital.

Stockpile aimed at automakers, tech firms, and other manufacturers to insulate against supply shocks.

Over a dozen companies participating, including GM, Boeing, Stellantis, Google, and Corning.

Rare earths and other critical minerals will be procured and stored, with manufacturers able to draw down inventory as needed.

Venture designed to stabilise prices and reduce volatility, similar to the US emergency oil stockpile model.

Source: Bloomberg

US Manufacturing PMIs signal moderate expansion in January

[8:59 am] US manufacturing shows moderate expansion in January, led by stronger production and new orders despite tariff and labour headwinds.

ISM Manufacturing surged to 52.6, highest since August 2022, well-ahead of 48.9 ests and 47.9 in the prior month

New orders jumped to 57.1, first expansion since August

Production rose to 55.9, highest since Feb-22

Prices index increased to 59.0, with tariffs, geopolitical tensions, and labour shortages cited as headwinds despite index gains

S&P 500 Q4 earnings growth stronger than expected

[8:55 am] FactSet data shows the Q4 S&P 500 EPS growth of 11.9%, above the 8.3% forecast, supporting a fifth consecutive quarter of double-digit growth.

Sell-side checks largely upbeat, noting elevated sales growth, record margins, and strong corporate sentiment.

Broadening of earnings strength across sectors, with solid guidance for 2026.

AI remains a major focus, driving expectations for continued hyperscaler capex increases.

Warsh shifts Fed focus from rates to balance sheet

[8:54 am] Trump’s pick of Kevin Warsh as Fed chair has pivoted market attention away from rate cuts and toward shrinking the Fed’s $6.6 trillion balance sheet and its role in markets.

Markets are now debating balance sheet reduction over short-term rates, with Warsh a long-time critic of QE and Fed asset expansion.

Speculation around faster drawdowns pushed long-term Treasury yields and the dollar higher, contributing to sharp falls in gold and silver as the “debasement trade” unwound.

Warsh’s hawkish stance risks clashing with Trump’s desire for lower borrowing costs, potentially forcing Treasury to play a bigger role in managing yields.

A smaller balance sheet could tighten financial conditions, though Warsh argues it may allow deeper cuts to the policy rate to offset that impact.

The Fed’s swollen balance sheet makes rapid shrinkage difficult, with money markets highly sensitive to liquidity changes, as seen in 2019 and late-2025 funding squeezes.

Source: Bloomberg

Gold volatility overtakes Bitcoin

[8:50 am] Gold’s parabolic rally has flipped into extreme swings, with price volatility now exceeding Bitcoin for the first time since the GFC era.

30-day gold volatility jumped above 44%, the highest since 2008, overtaking Bitcoin’s roughly 39%, an unusual reversal for a traditional safe haven.

Gold has only been more volatile than Bitcoin twice in 17 years, most recently during Trump tariff tensions last May.

Prices fell as much as 10% overnight to near $4,400/oz after peaking close to $5,600 last week, marking gold’s biggest plunge in more than a decade.

Despite the turbulence, gold remains the stronger hedge, up about 66% over 12 months vs. Bitcoin down 21%.

Source: Bloomberg

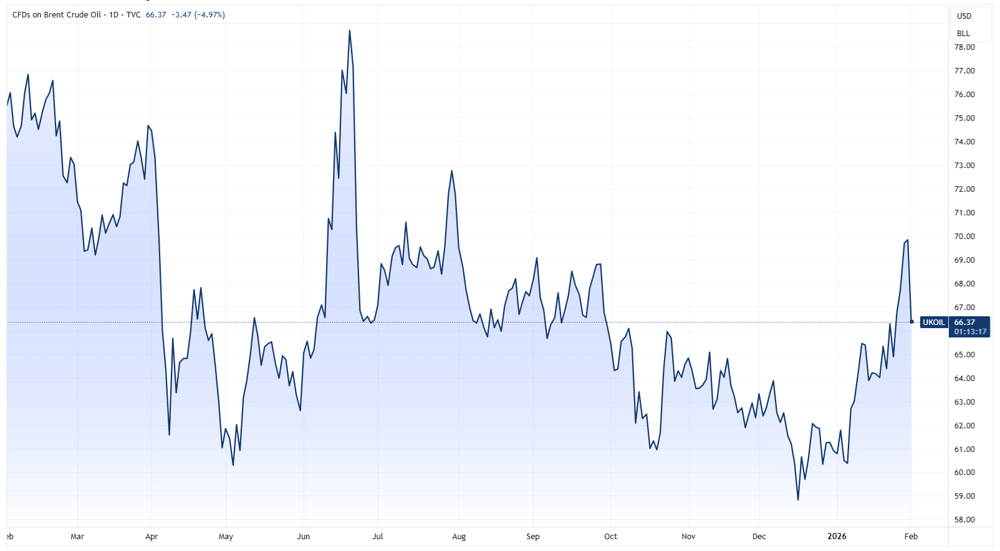

Oil tumbles as Iran risk premium unwinds

[8:47 am] Oil prices sold off sharply as signs of US-Iran de-escalation and a broader commodities rout stripped out geopolitical pricing from oil markets.

Brent fell 4.9% to US$66.37 a barrel, the biggest daily loss since June as Trump signalled hopes for a deal with Iran.

US envoy Steve Witkoff and Iran’s foreign minister set to meet in Istanbul later this week, reinforcing the view that near-term conflict risks are fading.

The move is seen as a positioning reset rather than a supply shift, with no new shock to fundamentals and elevated global inventories into 1H26.

Broader commodities weakness compounded the fall, with gold down as much as 10% and copper briefly dropping over 5%, dragging cross-asset risk lower.

Energy was the worst performing S&P 500 sector overnight, down 1.98%

Brent crude price chart (Source: TradingView)

Oracle to raise up to $50bn for AI cloud buildout

[8:45 am] Oracle is planning one of the largest tech financings in years to fund massive AI-driven data centre expansion, as investors debate returns and balance sheet risk.

Oracle plans to raise $45bn to $50bn via debt and equity to expand cloud infrastructure for AI clients including Nvidia, Meta, OpenAI, AMD, TikTok and xAI.

The company kicked off a $20bn to $25bn US dollar bond offering, with roughly half of total funding to come from equity-linked and common equity, including up to $20bn via at-the-market issuance.

Heavy AI capex has pushed free cash flow negative, expected to remain so until 2030, with tens of billions earmarked for chips and long-term leases.

Oracle shares are down about 50% from the September peak, wiping roughly $460bn in market value, making the stock a barometer for AI bubble concerns.

Source: Bloomberg

Major US benchmarks broadly higher

[8:43 am] A solid overnight session, where the S&P 500 opened ~0.20% lower and spent most of the session trending higher to finish 0.54% higher. The index is now within 0.3% of its Thursday, 22 January record close. Weakness from Nvidia (-2.8%) and Tesla (-2.0%) was offset by strength from Apple (+4.0%), Walmart (+4.1%) and Visa (+3.7%).

Breadth was solid, with the Equal-weight S&P 500 (+0.51%) performing in-line with the cap weighted index. Sectors including Staples, Industrials and Financials all finished 1-1.5% higher, though defensives like Real Estate (-1.1%) and Utilities (-1.5%) underperformed.

Good morning!

[8:32 am] ASX 200 futures are up 77 pts (+0.88%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks opened mostly lower, spent most of the day trending higher to close near best levels

Commodity market volatility continues, with gold currently down ~4.5% but fell as much as 10% (US$4,400) intraday

Despite commodity price volatility, gold and copper stocks finished relatively flat overnight

Credit Corp due to report 1H26 earnings this morning

To catch up on all overnight developments, check out today's Morning Wrap.