ASX 200 Live Today - Monday, 20th April

The S&P/ASX 200 is trading lower as US-Iran tensions worsen, oil prices jump. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Monday, April 20. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 back at breakeven

[2:30 pm] ASX 200 pretty much flat after falling as much as 0.54% in early trade, reflecting:

Decent breadth, with 110 constituents (55%) trading higher, with notable strength from Discretionary (+1.49%), Staples (+1.01%), Real Estate (+0.78%), Industrials (+0.63%) and Tech (+0.53%)

Materials (-0.07%) has reversed back towards breakeven after falling 1.41% in early trade

Financials (-0.26%) also off session lows of -1.03%

Edit: US futures are currently trading slightly lower, with S&P 500 and Nasdaq futures down 0.58% and 0.56% respectively. Though no major changes to the US-Iran situation since this morning:

US Navy seized an Iranian-linked cargo ship

US negotiators heading to Islamabad for talks planned for Wednesday

Iranian officials signaled they did not intend to take part in these talks

Despite how volatile and unpredictable the developments may be, it does seem like markets continue to price in a positive outcome. US earnings season is also well underway, with Q1 S&P 500 EPS growth currently sitting at 13.2%, in-line with market expectations. Of the 10% of S&P 500 companies that have reported, 88% have beaten EPS expectations, above the five-year average of 78%. That's all for today, let's see if the Nasdaq can notch a historic 14-day win streak overnight.

CBA bounces, NAB tumbles

[1:21 pm] CBA is trading notably higher after falling ~3.6% in the prior four sessions, meanwhile NAB is in the midst of an ugly dip after a downbeat trading update this morning. NAB is now on a five day skid, down 9.1% to the lowest since 7-Jan-26.

Ticker | Company | % Chg | Price | 1 Year % Chg |

|---|---|---|---|---|

CBA | Commonwealth Bank | 1.09% | $180.17 | 12.80% |

WBC | Westpac | 0.26% | $39.84 | 27.43% |

JDO | Judo Capital | 0.13% | $1.51 | -10.56% |

ANZ | ANZ Group | -0.22% | $37.84 | 36.10% |

MQG | Macquarie Group | -0.31% | $239.13 | 33.76% |

BOQ | Bank Of Queensland | -0.41% | $7.28 | 4.00% |

BEN | Bendigo & Adelaide Bank | -0.72% | $11.03 | 5.45% |

NAB | National Australia Bank | -4.02% | $40.84 | 19.59% |

Zip extends gains

[1:19 pm] Zip is currently up 9.2%, trading at the highest since 19 February (when the stock suffered a 34% one-day selloff after a weaker-than-expected 1H26 result).

Zip daily price chart (Source: TradingView)

Gold stocks catch a bid

[12:01 pm] Gold stocks have reversed back into positive territory, with the S&P/ASX All Ords Gold Index now up 1.8% vs. early lows of -1.0%.

This move is in-line with the turnaround for gold prices, which dipped as much as 2.0% in early trade to US$4,737/oz, now down just 0.6% to US$4,805.

The below table observes the % change for large cap gold miners from today's open price.

Ticker | Company | % Chg from open | Price |

|---|---|---|---|

OBM | Ora Banda Mining | 5.70% | $1.58 |

VAU | Vault Minerals | 4.49% | $4.78 |

RRL | Regis Resources | 3.42% | $7.72 |

GMD | Genesis Minerals | 3.20% | $6.78 |

RMS | Ramelius Resources | 2.81% | $4.03 |

BGL | Bellevue Gold | 2.63% | $1.76 |

RSG | Resolute Mining | 2.28% | $1.44 |

EVN | Evolution Mining | 2.22% | $13.83 |

CMM | Capricorn Metals | 1.86% | $12.02 |

WGX | Westgold Resources | 1.75% | $6.41 |

NEM | Newmont | 1.57% | $159.98 |

EMR | Emerald Resources | 1.31% | $6.58 |

PRU | Perseus Mining | 1.25% | $5.66 |

NST | Northern Star Resources | 0.84% | $23.94 |

ALK | Alkane Resources | 0.28% | $1.80 |

Grocery price inflation easing near-term but Middle East conflict expected to drive fresh acceleration in 4Q26

[11:59 am] UBS' grocery price study shows food inflation continuing to moderate in 3Q26, though forward-looking indicators point to a re-acceleration driven by fuel and supply chain pressures from the Middle East conflict.

Industry food inflation (ex tobacco) averaged 1.7% in 3Q26 (2.0% 2Q26; 2.1% 1Q26), with March at 1.8%

Dry grocery (1.8%) ran marginally ahead of fresh (1.7%) in 3Q26, with dry costs reflecting enduring supplier pressures including labour, energy and mixed commodity costs, partially offset by price investment campaigns such as WOW's Lower Shelf Prices initiative

UBS supplier survey (Jan-26) points to 3.3% inflation expected over the next 12 months, up from 2.7% in the Jun-25 survey

The Middle East conflict is expected to drive a re-acceleration in food inflation from 4Q26, led by fresh (fuel surcharges and reduced availability), extending into FY27 via higher diesel and fertiliser costs for fresh

UBS forecasts peak COL and WOW inflation of 5.5% in 2Q27 (December quarter), below the COVID peak of 7.7% in 2Q23, with no full reversal expected as cost of goods pressure is anticipated to remain elevated.

Analysts' take on Paladin Energy

[11:53 am] Paladin Energy raised FY26 uranium production guidance last Friday, following strong operational performance at Langer Heinrich, driven by better ore grades, higher recovery rates and improved fleet deployment, while also cutting capex materially. The stock gained 2.7% on the day, closing at the highest since June 2024.

Key numbers from the FY26 guidance update include:

Q3 U3O8 production of 1.29Mlb vs. 1.18Mlb ests (9% beat)

Q3 U3O8 sold 1.03Mlb vs. 1.20Mlb ests (14% miss)

Company says the miss reflects timing rather than demand, with full-year sales guidance unchanged at 3.8-4.2Mlb

Average realised price of $68.3/lb vs. $73.8/lb ests (7% miss)

Cost of production of $40.3/lb vs. $45.3/lb ests (11% beat), driven by the successful mining fleet mobilisation and improved plant recovery rates

FY26 production guidance raised to 4.5-4.8Mlb from 4.0-4.4Mlb (10.7% upgrade at the midpoint)

FY26 capex guidance cut to $15-17m from $26-32m due to reprioritisation and deferral of expenditure

Despite the positive update, several analysts downgraded the stock on the view the share price has run ahead of fundamentals.

Macquarie downgraded to Neutral, raised target from $13.50 to $13.55. Stock viewed as having re-rated too far ahead of fundamentals, with FY27 production downside risks versus consensus and better value seen elsewhere in uranium equities.

JPMorgan maintained Underweight, lowered target from $9.40 to $9.30. Operational beat seen as masking longer-term headwinds, with valuation remaining stretched as cost and pricing dynamics create conflicting signals on true underlying value.

Canaccord Genuity maintained Buy, target maintained at $16.00. Management execution validates confidence in the business model, with Langer Heinrich's ramp-up trajectory and mining outperformance expected to continue supporting the share price near term.

Tech stocks edge higher

[11:25 am] Tech stocks have opened higher for a fifth straight session, with the S&P/ASX 200 currently up 0.50% and up 15% since last Monday.

Life360 (+5.6%) is trading sharply higher, but names like Wisetech and Pro Medicus are struggling for upside following the recent V-shaped move from lows.

Ticker | Company | % Chg | Price | 1 Yr % Chg |

|---|---|---|---|---|

360 | Life360 | 5.67% | $22.56 | 18.74% |

PPS | Praemium | 2.78% | $0.74 | 12.12% |

MAQ | Macquarie Technology Group | 2.28% | $69.21 | 19.67% |

BVS | Bravura Solutions | 1.63% | $2.19 | 3.07% |

HSN | Hansen Technologies | 1.39% | $5.09 | 1.39% |

CDA | Codan | 1.21% | $34.38 | 135.16% |

CAT | Catapult Sports | 0.94% | $3.23 | -11.51% |

XRO | Xero | 0.91% | $82.73 | -46.22% |

DDR | Dicker Data | 0.50% | $9.00 | 10.91% |

SDR | Siteminder | 0.45% | $3.35 | -10.56% |

OCL | Objective Corporation | 0.34% | $11.86 | -22.38% |

NXL | Nuix | 0.16% | $1.27 | -46.54% |

IRE | Iress | 0.14% | $7.10 | -8.51% |

WBT | Weebit Nano | 0.00% | $4.06 | 153.75% |

TNE | Technology One | -0.03% | $30.82 | 11.34% |

DTL | Data#3 | -0.14% | $7.39 | 1.93% |

WTC | Wisetech Global | -0.56% | $45.92 | -44.72% |

MP1 | Megaport | -1.06% | $8.40 | -14.29% |

PME | Pro Medicus | -1.52% | $146.48 | -28.03% |

DGT | Digico Infrastructure Reit | -1.92% | $2.04 | -18.40% |

AD8 | Audinate Group | -3.25% | $2.68 | -52.73% |

Chinese lithium futures open higher

[11:20 am] Chinese lithium carbonate futures up 2.4% in early trade to 179,860 yuan a tonne. Prices have now gained ~8.5% in the last five sessions and within 5% of early January highs of 189,440 yuan.

PLS Group dipped as much as 6.1% in early trade, now down just 2.1% ($5.91).

Analysts' take on Zip

[10:44 am] Zip Co delivered a materially better-than-expected Q3 result last Friday, with US credit losses coming in well controlled and top-line momentum accelerating, directly addressing the market's key concern around deteriorating credit quality. The stock rallied 13.6% on the day of the announcement, though faded from intraday highs of 23.9%.

The key numbers from the update include:

Cash EBTDA of $65.1m beat UBS's $62m estimate (5% beat)

Operating margin of 19.4% also exceeded UBS's implied expectations

Revenue/portfolio income of $332.2m beat UBS's $316m forecast by ~5-6%

US TTV growth of 43.1% y/y outpaced UBS's 38% estimate

Group net bad debts of 1.9% of TTV came in marginally above UBS's 1.85% forecast, though within management's stated comfort range of 1.5-2%

Group revenue margin of 8.4% was well above UBS's 7.3% group revenue yield estimate, a meaningful positive surprise

Zip upgraded FY26 cash EBTDA guidance to no less than $260m while UBS expected to be maintained

The result has attracted slight target price upgrades from most brokers, including:

Ord Minnett retained Buy, raised target from $3.90 to $4.00. US bad debts are improving with the worst now behind them, operating margins expanded on stronger net transaction margins, and the Stripe integration is driving meaningful merchant acquisition gains.

UBS retained Buy, raised target from $2.85 to $3.10. US bad debt guidance came in better than market expectations, valuation remains attractive relative to domestic banks and fintech peers, though conservative FY27 growth assumptions reflect appropriate caution around the macro backdrop.

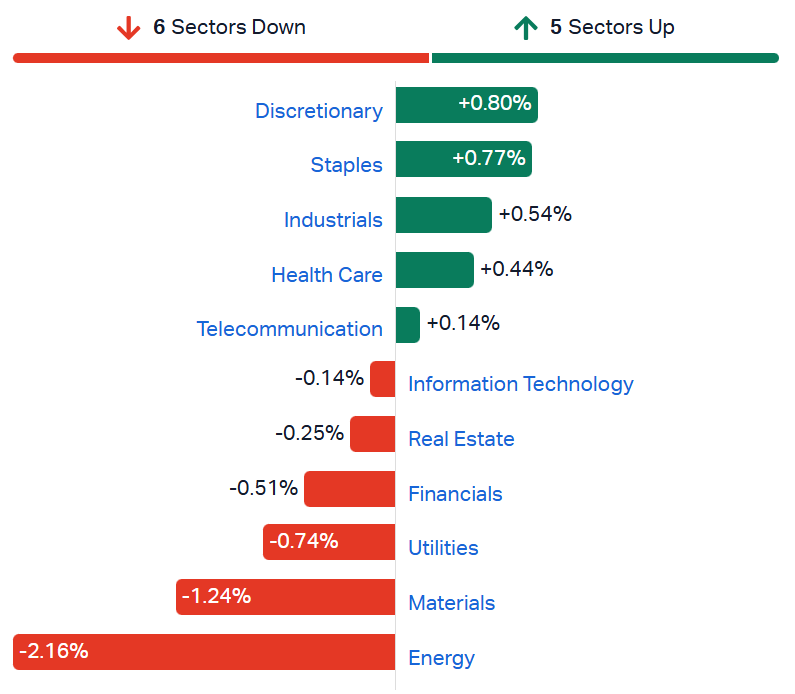

ASX 200 lower, positive breadth offset by banks and miners

[10:37 am] ASX 200 currently down 0.53% and trading at intraday lows.

Breadth is positive, with 114 constituents (57%) trading higher

Positive breadth offset by weakness among heavyweight banks and resources, with notable declines from NAB (-3.0%), Woodside (-2.0%), Rio Tinto (-1.3%), BHP (-0.8%) and CBA (-0.2%)

Energy stocks (-2.1%) now trading at the lowest since 19-Mar and down ~8% from early April peak. This is despite US-Iran talks breaking down over the weekend and oil prices bouncing on Monday

Financials (-0.5%) broadly lower, with NAB (-3.0%) weighing heavily on the index after a downbeat 1H26 trading update

ASX 200 sectors (Source: Market Index)

Top ASX 200 gainers

[10:17 am] A lot of dual-listed names like James Hardie, Life360, Amcor, Light & wonder and Block topping the leaderboards after a record setting overnight session for the S&P 500 and Nasdaq.

Ticker | Company | % Chg | Price |

|---|---|---|---|

ZIP | Zip Co | 4.94% | $2.45 |

JHX | James Hardie | 4.14% | $29.20 |

360 | Life360 | 3.84% | $22.17 |

AMC | Amcor | 3.23% | $57.85 |

LOV | Lovisa | 2.90% | $24.50 |

LNW | Light & Wonder | 2.06% | $124.00 |

OBM | Ora Banda Mining | 2.01% | $1.52 |

QAN | Qantas Airways | 1.82% | $9.25 |

MAH | Macmahon | 1.76% | $0.87 |

XYZ | Block | 1.69% | $98.31 |

Top ASX 200 losers

[10:17 am] Some froth coming out of lithium, uranium and energy stocks this morning.

Ticker | Company | % Chg | Price |

|---|---|---|---|

SRL | Sunrise Energy Metals | -6.41% | $11.97 |

VEA | Viva Energy Group | -5.93% | $2.38 |

PLS | PLS Group | -5.30% | $5.72 |

MIN | Mineral Resources | -4.39% | $60.75 |

PDN | Paladin Energy | -4.23% | $13.93 |

WOR | Worley | -3.98% | $11.35 |

DYL | Deep Yellow | -3.94% | $1.95 |

IGO | IGO | -3.89% | $8.89 |

LTR | Liontown | -3.86% | $2.12 |

NHC | New Hope Corporation | -3.60% | $5.09 |

4DMedical secures GSK contract and UK regulatory clearance

[10:01 am] 4DMedical has announced a series of commercial, regulatory and corporate milestones, capping a transformative 12 months that has seen the company re-rate materially and recently join the S&P/ASX 200 index.

GSK contract executed to supply 4DMedical's quantitative lung imaging analytics in support of pulmonary drug development, commencing 1 May 2026 under a one-year agreement

Contract value is commercially confidential and not individually material, but adds to an existing pharma roster that includes AstraZeneca

CT:VQ receives UKCA certification for clinical use in the UK, following CE Mark certification in March 2026

The company now holds regulatory clearance across the US, EU, UK, Canada and New Zealand, with UK clearance enabling immediate commercial deployment across public and private providers

CAC analysis receives Health Canada clearance, coinciding with 4DMedical's participation at the Canadian Association of Radiologists Annual Scientific Meeting in Montreal

In the US, CMS has established a dedicated reimbursement code (G0680) for AI-enabled opportunistic coronary artery calcium analysis from routine chest CTs, with reimbursement set at $15.50 per study in the hospital outpatient setting

4DMedical added to the S&P/ASX 200 Index effective today

Company page: 4DMedical (4DX)

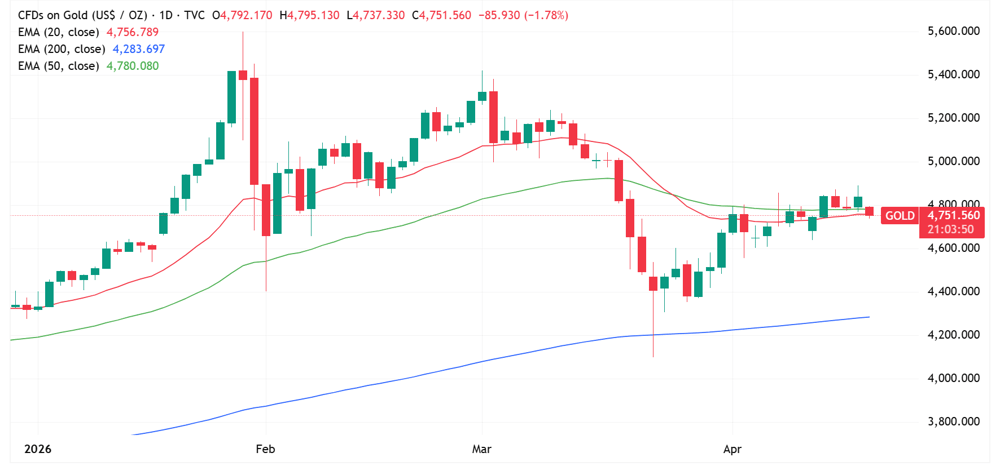

Gold prices dip in early trade

[9:57 am] Gold prices have dipped 1.7% in early trade to US$4,751/oz.

Last Friday, prices rallied as much as 2.1%, before closing the session up 1.05% to US$4,787.

Gold daily price chart (Source: TradingView)

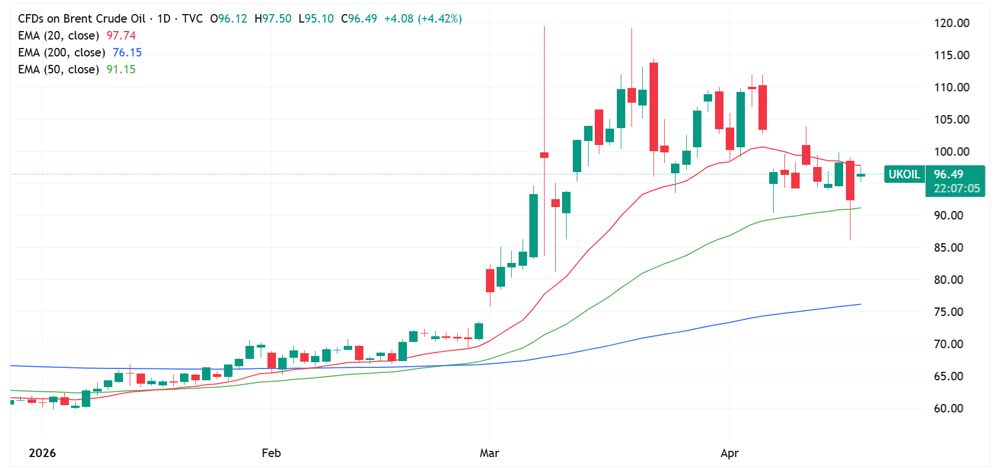

Oil prices bounce after Friday selloff

[9:55 am] Brent is trading 4.2% higher to US$96.40 a barrel after suffering a volatile dip last Friday.

The mixed messages from Trump and Iran drove oil prices down as much as 12.3% to US$86.09 last Friday, though prices clawed back early declines to finish 5.9% lower to US$92.40.

Including today's bounce, prices are down just 1.8% in the last two sessions.

Brent daily price chart (Source: TradingView)

Qube flags earnings headwinds from Middle East conflict and adverse weather

[9:50 am] Qube has quantified near-term earnings headwinds, though management framed the Middle East and weather impacts as largely temporary and reaffirmed its FY26 guidance.

The Middle East conflict is expected to weigh on FY26 EBITA by $10-20m, with the Logistics and Infrastructure division bearing the largest impact and Ports and Bulk seeing a more limited effect

Severe weather events across Australia and New Zealand in Q3 FY26 have added a further $3-5m EBITA headwind, bringing total combined earnings pressure to an estimated $13-25m for the year.

Qube continues to expect underlying earnings growth in FY26 on both an NPATA and EPSA basis

Management has flagged both impacts as largely non-recurring or short term, with most expected to reverse in FY27 assuming the conflict concludes

The agreed scheme with the MAM Consortium is unaffected by the revised outlook, keeping the takeover process on track

Company page: Qube (QUB)

NAB reviews credit and capital settings

[9:48 am] NAB has flagged a significant increase in first half credit impairment charges and announced changes to its software capitalisation policy, while moving to strengthen its capital position via a discounted dividend reinvestment plan.

1H26 credit impairment charges expected at $706m vs. $485m half-ago, driven by a $300m net increase in forward-looking collective provisions reflecting macro uncertainty tied to the Middle East conflict

The $300m provision build includes a $152m increase in the economic adjustment (lifting the Australian Downside scenario weighting by 2.5% to 45%), a $201m increase in forward-looking adjustments for sectors exposed to fuel supply and cost pressures, partially offset by a $53m release where expected risks have not materialised.

Underlying provision charges of $406m vs. $574m half-ago, reflecting individually assessed charges of $541m partially offset by a $135m write-back of the underlying collective provision.

Pro-forma group CET1 ratio expected at greater than 12.0% as at 31 March, inclusive of a 1.5% discounted and partially underwritten DRP expected to raise up to $1.8bn and contribute up to approximately 40 bps to CET1 in H2.

FY26 cash operating expense growth guidance of less than 4.6% reaffirmed

Company page: National Australia Bank (NAB)

Monash IVF rejects Soul Patts-Genesis takeover bid

[9:45 am] The Monash IVF board has unanimously rejected a revised non-binding indicative proposal from a Genesis Capital and Soul Patts consortium.

The bid was rejected on the basis that it represents a substantial discount to comparable IVF transactions in the Australian market

The board cited the recent appointment of new CEO Dr Victoria Atkinson as a key factor, expressing confidence in her strategy to return stability and growth to the business following a period of leadership instability.

Feedback from a number of non-consortium shareholders also informed the board's decision to reject the proposal.

Monash IVF remains open to change of control discussions at a higher valuation, though the board noted there is no certainty any transaction will eventuate

The stock was trading at ~67 cents prior to the takeover announcement

Company page: Monash IVF Group (MVF)

Worley flags $30-40m Middle East earnings hit

[9:32 am] The Middle East conflict is creating near-term headwinds for Worley through project delays, with the company still expecting to hold its margin guidance range for FY26.

The adverse impact on underlying EBITA from Middle East disruption is estimated at $30-40m, with no project cancellations to date but customers delaying commencement and award of new work

Though underlying EBITA growth in FY26 is described as "not unlikely"

FY26 underlying EBITA margin guidance is maintained at 9.0-9.5%, and the company continues to target higher aggregated revenue growth than FY25

Announcement noted: "We continue to speak with customers in the Middle East on the more immediate repair and rebuild efforts in the region ..."

Company page: Worley (WOR)

Viva Energy Q1 update

[9:30 am] A refinery fire and Hormuz-driven supply chain disruption have created near-term headwinds for Viva Energy, though strong Q1 refining margins, volume growth, and insurance cover provide meaningful offsets.

Q1 total fuel volumes of 4,302ML were up 5.1% on the prior year (4,092ML), driven by Commercial and Industrial volumes rising 7.1% to 3,021ML (vs. 2,821ML), with growth across aviation, agriculture, and resources sectors.

The Geelong Refinery delivered a standout Gross Refining Margin (GRM) of US$22.0/bbl in Q1 vs. US$7.9/bbl in the prior year

A fire at the Geelong refinery on 15 April has temporarily reduced output, with diesel and jet fuel expected at ~80% capacity and petrol at ~60% in the short term

A restart of the reformer and residue catalytic cracking unit lifts output to over 90% within weeks.

The company has insurance covering both property damage and business interruption.

Regional refining margins are expected to remain elevated through Q2 due to sustained Middle East conflict, though rising crude premia from increased competition for non-Hormuz crude are an emerging cost pressure

Viva's Geelong refinery does not source Middle Eastern crude, with supply predominantly from the Americas, South-East Asia, and Australia, with firm crude supply locked in through July

Convenience sales declined 6.1% to $402m (vs. $428m), driven by a 23.9% drop in tobacco sales, though convenience ex-tobacco was up 1.2%

Company page: Viva Energy Group (VEA)

L1 Group's gold fund IPO raises $950m ahead of ASX debut

[9:27 am] L1 Group has successfully completed the IPO of the L1 Gold Fund, raising $950 million at $1.10 per share ahead of its expected ASX listing on 24 April.

The L1 Gold Fund (LGF) will pay L1 Group a management fee of 1% per annum of portfolio value, and a performance fee of 20% on outperformance assessed over each six-month period.

L1 Capital founders Mark Landau and Raphael Lamm have committed a combined $140m into LGF

L1 Group itself has also committed $112m into the fund, bringing total insider investment to $252m or roughly 27% of the $950m raised.

Company page: L1 Group (L1G)

NextDC contracted utilisation surges, raises $1.5bn to accelerate delivery

[9:18 am] NextDC has reported a massive jump in demand metrics and launched a major equity raise to fund accelerated data centre development, with a forward earnings profile implying transformational scale by FY27.

Contracted utilisation reached 667MW as at 31 March, up 60% since 31 December 2025

Forward order book hit 544MW, up 83% over the same period

FY26 capex guidance has been lifted to $2.70-3.00bn from prior guidance of $2.40-2.70bn vs. ests of $2.62bn

FY26 net revenue and underlying EBITDA guidance is unchanged

Combined forward order book and existing billing utilisation is expected to generate EBITDA in excess of $1.0bn by FY30, representing more than 4x the midpoint of FY26 EBITDA guidance of $235m

As for the capital raise:

NextDC is raising $1.5bn via a fully underwritten, non-renounceable 1-for-5.4 entitlement offer at $12.70 per share share (a 10% discount to the last close of $14.12)

La Caisse has added a further $700m binding commitment to NextDC's hybrid securities offer, on top of its existing $1.0bn commitment, bringing total hybrid funding from the Canadian pension giant to $1.7bn.

FY27 capex is guided at $5.0bn, with NextDC flagging it intends to de-risk both S4 and S7 ahead of potential joint venture transactions with private capital partners from 2027.

Company page: NextDC (NXT)

Monash IVF board faces mounting pressure as takeover deadline looms

[9:08 am] A Tuesday deadline is forcing Monash IVF's board to respond to a $350 million bid from Soul Patts and Genesis Capital, with more than 12% of the register understood to be pushing for engagement, according to the AFR.

The Soul Patts and Genesis consortium lifted their offer from 80 cents to 90 cents earlier this month, along with a tight Tuesday deadline

The bid requires unanimous board approval and four weeks of exclusive due diligence, giving the Monash board limited room to negotiate terms without effectively accepting the proposal.

Over 12% of the register has privately communicated to directors that they want the board to engage and grant due diligence, viewing offer as reasonable given execution risk through the company's ongoing turnaround

Company page: Monash IVF (MVF)

Peninsula Energy suspended from trading

[9:03 am] Peninsula Energy has filed an urgent Supreme Court application after failing to make required disclosures on shares issued via a convertible loan conversion in February.

The issue stems from a cleansing notice failure tied to 19.9m shares issued on 12 February 2026 upon partial conversion of a convertible loan facility

Peninsula is seeking court orders declaring that any sale of those shares between 12 February and 7 April 2026 is not invalid despite the disclosure failure

The application is set to be heard on an urgent basis on Wednesday 22 April at 10am, with trading remaining suspended from the open on 21 April until the outcome is known.

Company page: Peninsula Energy (PEN)

S&P 500 re-rating driven by earnings upgrades, not multiple expansion

[9:00 am] Despite the S&P 500 trading above pre-war highs, the rally has been driven by fundamentals rather than sentiment, according to Goldman Sachs.

Consensus S&P 500 EPS estimates for both 2026 and 2027 have each risen 3% since the start of the war, providing a genuine earnings floor beneath the equity rally.

Forward PEs now sit 5% below where it was in January, meaning the market is cheaper on earnings today despite higher prices.

US markets starting to look expensive again

[8:58 am] The S&P 500 has returned to a 21x PE, placing it within the 81st percentile range of historical valuations.

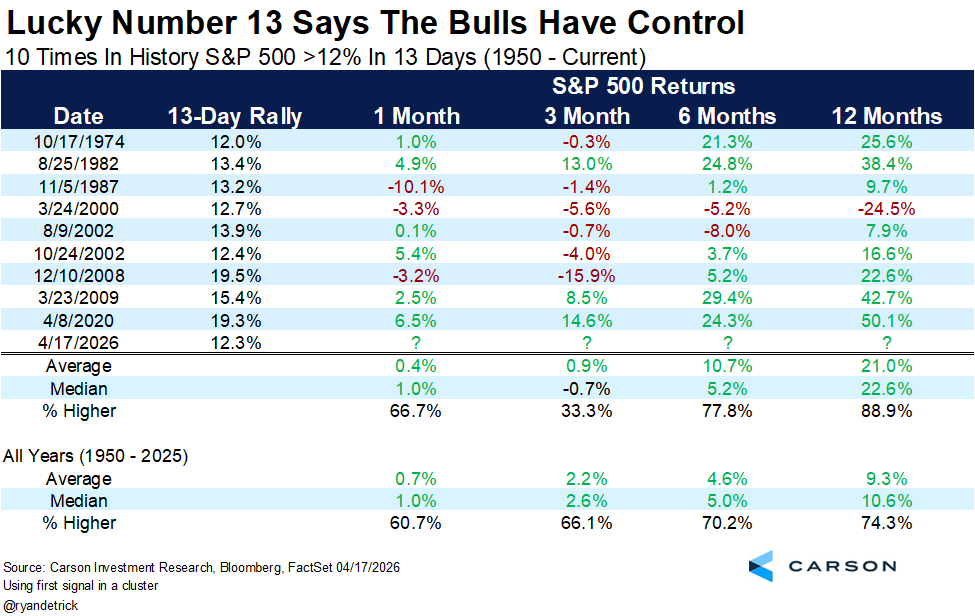

What happens after the S&P 500 rallies 12% in 13 days?

[8:55 am] There are only ten times in history where the S&P 500 rallied more than 12% in 13 days. Since 1974, historical forward returns remain bullish, with the S&P 500 up an average 21.0% and positive 88.9% of the time, according to Carson Research

Trump escalates Hormuz rhetoric

[8:53 am] Trump's latest Truth Social post marks a sharp escalation in tone, issuing direct military threats against Iran.

Trump accused Iran of violating the ceasefire by firing on vessels in the strait, specifically calling out attacks on a French ship and a UK freighter, reinforcing the narrative that Iran is the aggressor.

Trump confirmed US representatives are travelling to Islamabad for a second round of negotiations, suggesting back-channel diplomacy is still alive even as rhetoric hardens.

Trump argued Iran's decision to close the strait is self-defeating, claiming it costs Iran $500m per day while the US "loses nothing," with American ships redirecting to US ports in Texas, Louisiana, and Alaska to load domestic supply.

Trump threatened to "knock out every single Power Plant, and every single Bridge, in Iran" if a deal is not reached, framing it as a long-overdue reckoning 47 years in the making.

Source: Truth Social

Strait of Hormuz: Brief opening collapses into escalation

[8:48 am] A rather volatile sequence of events took place over the weekend. The Strait of Hormuz appeared set to reopen on Friday night, only for Iran to reverse course within 24 hours, leaving global oil markets and shipping in a more uncertain position than before.

Trump declared the strait "fully open," but the move proved premature as Iran quickly reversed its position when the US maintained its naval blockade

By Saturday, Iran's Revolutionary Guard had fired on tankers transiting the strait, including two Indian-flagged vessels and a French-flagged container ship (CMA CGM Everglade), confirming the waterway was back under strict Iranian military control

US Central Command reporting 23 ships turned back since the blockade began, and the military preparing to board and seize Iran-linked tankers in international waters in coming days

Diplomatic talks have broken down, with Iran pulling out of a second round of negotiations citing US "excessive demands," "constant shifts in stance," and the ongoing blockade as a ceasefire violation.

The two-week ceasefire expires Wednesday 22 April, with the core issues (Iran's uranium stockpile and Hormuz control) unresolved. Around 20% of global seaborne oil trade transits the strait, keeping supply disruption risk elevated

A narrow move to all-time highs

[8:46 am] Goldman Sachs notes the composition of the recent rally has been extremely narrow, with S&P 500 market breadth still at the lowest level since mid-2023.

Since the market low in late March, the S&P 500 Technology and Communication sectors have contributed roughly 70% of the market rebound, accounting for ~850 bps of the 12% S&P 500 rally.

Nasdaq's historic momentum surge signals near-term pullback

[8:45 am] The Nasdaq 100 just completed the fastest oversold-to-overbought RSI transition in its 40-year recorded history, with long-term forward returns historically bullish but a near-term pullback looking likely.

The Nasdaq 100's RSI moved from 28 (oversold) on 30 March to 70.5 (overbought) by 15 April in just 11 sessions, marking the fastest such transition on record. The previous fastest was 25 sessions, with the historical average exceeding 60 sessions.

Across 44 historical episodes where the Nasdaq gained 11% or more in 10 sessions, the 12-month forward return averaged +24% with a median of +30% and an 80% win rate. The 6-month win rate sits at 74%.

Near-term pain is historically near-certain however, with the average maximum drawdown following these signals at -18.39%, posing significant risk to over-leveraged portfolios even as the 12-month destination trends higher.

Based on the six most comparable historical analogues (COVID recovery, Liberation Day 2025, Fed pivot 2018, Asian crisis 1997), the most probable near-term pullback is 3-8% within the next 2-4 weeks

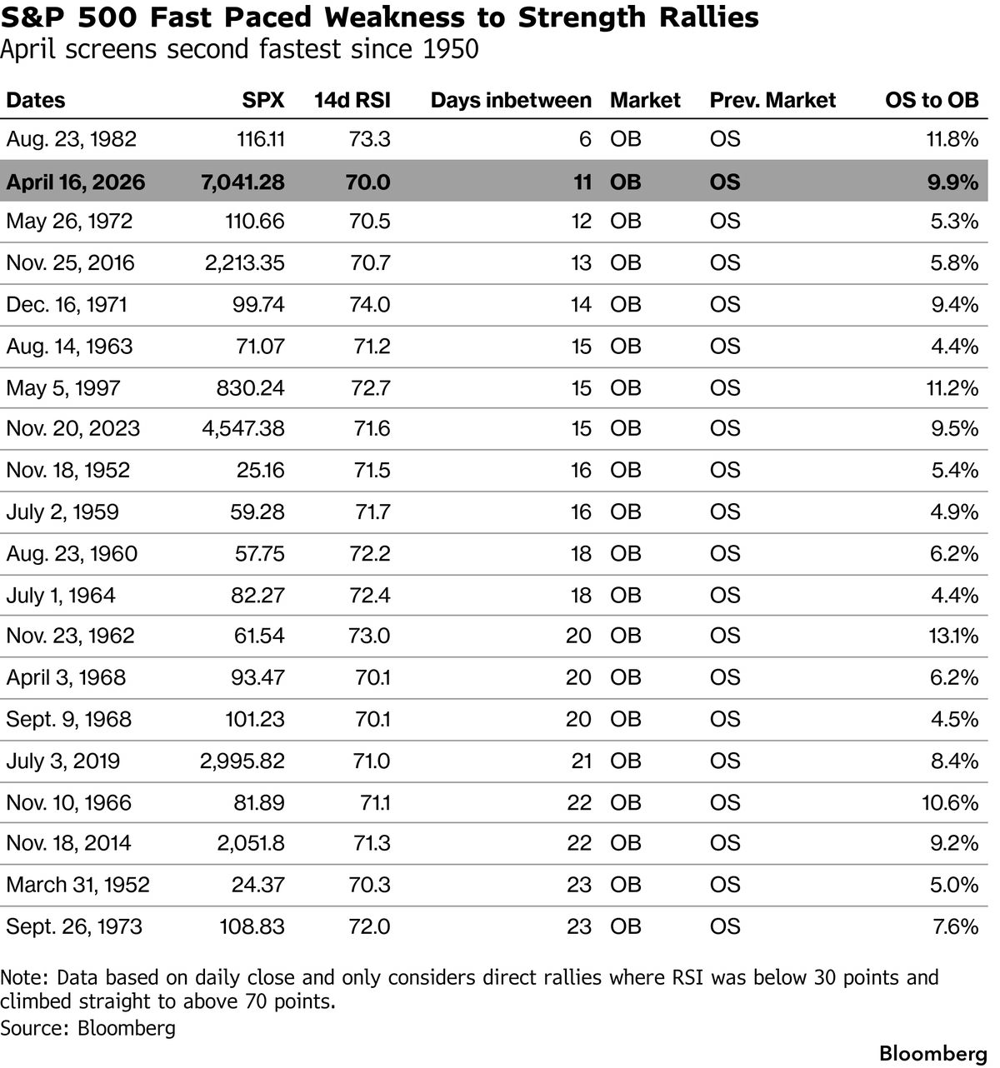

S&P 500: From oversold to overbought in two weeks

[8:42 am] The recent rally marks the second fastest shift from oversold to overbought on record, according to Bloomberg.

Good morning!

[8:29 am] ASX 200 futures are up 82 pts (+0.91%) as of 8:30 am AEST.

The overnight session in a nutshell:

S&P 500, Nasdaq and Russell all closed at fresh all-time highs

Nasdaq is now on a 13-day win streak, the longest since 1992 and the fifth longest streak on record

Volatile US-Iran developments, with Trump initially announcing the Strait of Hormuz is "fully open"

Iran later re-closed the Strait, noting the US naval blockade as a ceasefire violation

Brent dipped 5.9% on Friday to US$92.41 a barrel, but well-off session lows of -12.3%