ASX 200 Live Today - Monday, 11th May

The S&P/ASX 200 is set to slip after Trump rejected Iran's new peace offer over the weekend. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Monday, May 11. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 off lows

[2:00 pm] ASX 200 down 0.59%, off session lows of (1.15%) but back below the key 200-day moving average. A very wild session, comprised of:

Materials (+0.79%) edging higher as copper trades within an arms reach of all-time highs, iron ore almost crossing US$112 a tonne. Rio Tinto (+1.0%) is at fresh all-time highs, while BHP (+0.8%) is also within 2% of its 2-Mar record

Energy (+0.29%) really struggling to price-in any upside from recent oil moves. Brent is up 5.3% today to US$105.64 but energy stocks barely moved

Utilities, Discretionary and Staples all relatively unchanged

Financials (-1.24%) dipped as much as (-2.05%) in early trade, with most big four banks down 2-4%.

Healthcare (-7.4%) off session lows of (-10.1%) but so, so ugly. The index is now down 32% year-to-date and down 44% in the last twelve months. CSL is down 17.5% at the time of writing, which is also driving weakness across most large cap healthcare names today

It definitely feels like a very challenging market right now, where sticky inflation, further RBA rate hikes, a long list of corporate guidance downgrades and tomorrow's Federal Budget is weighing on the broader market. It's pretty hard to be bullish on anything outside of the resource complex.

As we wrap up the blog today, here are some interesting tidbits from UBS regarding the budget.

Speculated limits or removal of negative gearing on investment properties would reduce property's tax advantage and level the playing field versus equities, making shares relatively more competitive as an investment proposition

Replacing the 50% CGT discount with inflation indexation would make capital gains driven investments less attractive, shifting relative appeal toward income generating stocks with steady dividend streams over high PE growth names

UBS reaffirms underweight on Real Estate and Consumer Discretionary, noting similar property unfriendly policies pre 2019 Federal Election saw Real Estate equities underperform

Broader risk flagged is a negative wealth effect from softer property prices flowing through to domestic consumer facing equities

A strong day for copper miners

[1:32 pm] Copper prices rallied 2.6% last Friday to a near-record US$6.29/lb and up a further 0.90% today to US$6.35/lb. Despite copper returning to recent highs, most copper miners are trading lower year-to-date.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

CSC | Capstone Copper | 5.6% | $13.07 | -13.8% |

CYM | Cyprium Metals | 4.8% | $0.44 | -17.8% |

HCH | Hot Chili | 4.8% | $1.87 | 34.2% |

29M | 29Metals | 3.8% | $0.27 | -48.7% |

MC2 | Marimaca Copper | 3.1% | $8.36 | -33.1% |

SFR | Sandfire Resources | 2.7% | $18.51 | 3.0% |

AIS | Aeris Resources | 1.2% | $0.42 | -30.0% |

FFM | Firefly Metals | 0.9% | $1.94 | -5.7% |

BHP | BHP Group | 0.8% | $58.42 | 28.3% |

CPM | Cooper Metals | 0.0% | $0.05 | -10.7% |

HGO | Hillgrove Resources | 0.0% | $0.04 | -12.5% |

AR1 | Austral Resources Australia | -9.5% | $0.10 | 66.7% |

CSL: No bounce in sight

[1:27 pm] CSL is currently down 18.1% ($98.18), slightly off session lows but trading at levels not seen since December 2016. The stock is now down ~64% since August 2025.

CSL issued yet another earnings downgrade this morning, which noted:

FY26 revenue guided to ~$15.2bn vs. $15.79bn ests (4% miss)

FY26 NPATA guided to ~$3.1bn vs. $3.34bn ests (7% miss)

Expects to recognise ~$5bn of non-cash, pre-tax impairments across FY26 and FY27 in addition to those announced at the first half result, including CSL Vifor intangibles and under-utilised property, plant and equipment

The stock has been in an absolute death spiral since its FY25 result on 19 August. Here's a recap of how things came about:

19-Aug-25: Shares tumbled 17% after a relatively in-line FY25 result, but the FY26 guidance pointed to 7-10% NPATA growth vs. analyst expectations of around 15%.

28-Oct-25: Took another 15.8% dip after downgrading its FY26 NPATA growth guidance to 4-7% vs. prior 7-10%. CSL said uncertainty in US vaccination rates reduces group NPATA growth expectation to high single digits in FY27-28 vs. analyst expectations of ~10%.

10-Feb-26: CEO Paul McKenzie announced his retirement at 4:05 pm AEST, driving the stock 5% lower in the closing action (and day before its 1H26 result)

11-Feb-26: 1H26 revenue, NPATA and dividend missed consensus by 2-5%. FY26 guidance reaffirmed but shares still down 4.6%

China factory inflation hits fastest pace since 2022

[12:49 pm] China's producer prices accelerated sharply in April on Iran war-driven commodity costs, ending years of factory deflation but squeezing margins as weak domestic demand limits cost pass-through.

PPI up 2.8% YoY in April vs 1.8% ests and 0.5% in March, the fastest pace since July 2022 and above all economist estimates

CPI up 1.2% YoY vs 1.0% in March, surprising analysts who had expected a slowdown despite slumping food prices

Purchase price index rose 3.5% YoY, opening the widest gap with selling prices since August 2024 and pointing to compressed factory margins

JPMorgan lifts Kospi targets on AI-driven memory upcycle

[12:48 pm] JPMorgan raised its Kospi base and bull-case targets for the second time in under a month, citing a sustained memory chip upcycle, governance reforms and AI-driven earnings momentum.

Base Kospi target lifted to 9,000 and bull case to 10,000 (33% upside from Friday's close), up from 7,000 and 8,500 set in late April

Kospi surged as much as 5.1% today to an intraday record 7,876.60, extending YTD gains to ~86% and ranking as one of the world's top-performing benchmarks

Memory chip stocks make up 50% of Kospi weight and have driven ~70% of YTD gains, with JPMorgan flagging a potential two-year sustained upcycle on rising ASPs and volumes

JPMorgan acknowledges stretched technicals near term but argues memory cycle, governance reforms and thematic growth support staying positioned for further upside

Source: Bloomberg

Lithium stocks broadly higher

[12:09 pm] Chinese lithium carbonate futures ticking higher in early trade, up 2.4% to 203,160 yuan a tonne.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

CXO | Core Lithium | 5.1% | $0.35 | 402.9% |

INR | Ioneer | 5.0% | $0.15 | 8.9% |

DLI | Delta Lithium | 4.1% | $0.26 | 21.4% |

LTR | Liontown | 2.7% | $2.52 | 357.3% |

LKE | Lake Resources | 2.2% | $0.09 | 203.2% |

PMT | PMET Resources | 2.0% | $0.75 | 200.0% |

IGO | IGO | 2.0% | $8.51 | 107.4% |

PLS | PLS Group | 1.4% | $6.35 | 328.7% |

AGY | Argosy Minerals | 1.3% | $0.08 | 315.8% |

VUL | Vulcan Energy Resources | 1.2% | $3.78 | -2.3% |

MIN | Mineral Resources | 0.2% | $69.72 | 232.0% |

PAT | Patriot Resources | 0.0% | $0.12 | 91.7% |

WR1 | Winsome Resources | 0.0% | $0.53 | 221.2% |

EUR | European Lithium | 0.0% | $0.46 | 742.6% |

GL1 | Global Lithium Resources | -1.7% | $0.58 | 248.5% |

Australian Federal Budget preview and key reform pillars

[12:06 pm] Morgan Stanley expects the FY27 Federal Budget to deliver a modestly improved fiscal position alongside major reform announcements, with monetary and fiscal policy now aligned to slow domestic conditions.

FY27 deficit forecast to improve from -1.3% to -0.9% of GDP, aided by stronger commodity-driven revenues; announced policy impacts broadly neutral as cost-of-living support is offset by tax increases and slower spending growth

Equity implications: Capped index returns near term, de-rating risk for Banks and rate-sensitive sectors, margin risk for Consumer, activity risk for Housing, with rotation favouring Capex over Consumption

Wealth tax reforms in focus: 50% CGT discount likely replaced with inflation indexation (Treasury values current discount at $21.79bn in revenue foregone for FY26), negative gearing restrictions likely with grandfathering, and a reported 30% minimum tax on family trust distributions (estimated $4-5bn saving over four years)

NDIS reform targets ~$35bn budget improvement over four years, slowing scheme growth to ~2% pa and lowering projected FY30 costs from $70bn+ to ~$55bn

Energy resilience package above $10bn announced, including $7.5bn Fuel and Fertiliser Security Facility and $3.2bn government-owned fuel reserve; large new resources taxes look unlikely, with a 20% domestic gas reservation scheme from July 2027 instead

EV FBT exemption extended to end-March 2027 then narrowed to EVs under $75,000, moving to a permanent 25% FBT discount from April 2029 ($1.7bn saving over five years)

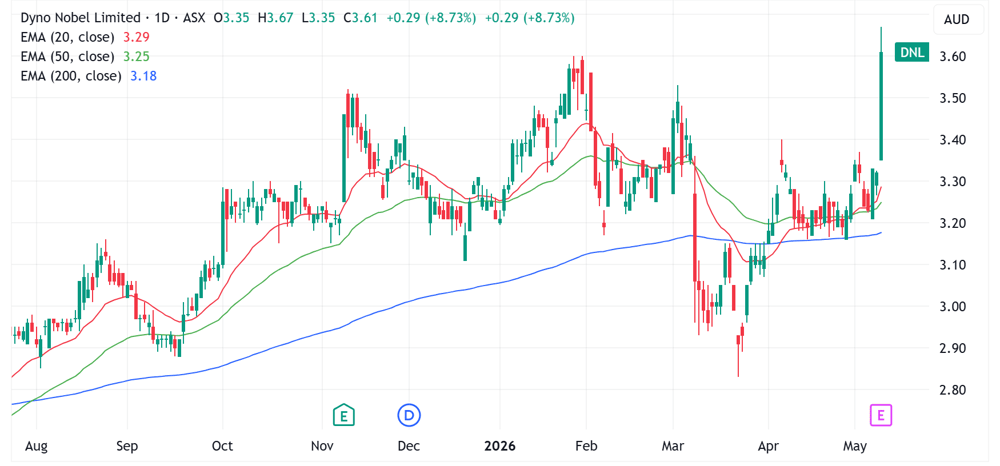

Dyno Nobel soars to three-year high

[11:15 am] Dyno Nobel caught a very aggressive bid this morning, opening 0.9% higher and currently up 8.7% to the highest since January 2023.

The company's 1H26 result was broadly ahead of market expectations, including a much stronger-than-expected interim dividend and reaffirmed FY26 guidance.

Revenue (incl. discontinued ops) of $1.90bn vs. $1.78bn ests (7% beat)

NPAT (ex IMIs) up 83% to $160.9m vs. $139.0m ests (16% beat)

Interim dividend of 4.6 cents per share vs. Macquarie ests of 4.0 cps

$558m of the $900m on-market buyback completed to date, with buyback set to recommence from 12-May

FY26 EBIT guidance reaffirmed at $460-500m

Dyno Nobel daily price chart (Source: TradingView)

Analysts lift Macquarie target price

[11:09 am] Macquarie's FY26 result delivered a substantial earnings beat with strong divisional growth across MAM, CGM and MacCap, though the composition relied heavily on asset realisations, performance fees and a lower tax rate, offset by elevated credit impairments.

Net profit up 30% to $4.85bn vs $4.42bn ests (10% beat)

EPS up 30% to $12.77 vs $11.60 ests (10% beat)

Full year dividend of $7.00 per share vs $7.32 ests (4% miss)

On-market share buyback concluded with $1.01bn acquired at an average $189.80, with no further purchases expected

T|he market reaction was muted as analysts debated the durability of near-term revenue drivers, with sentiment broadly upbeat but acknowledging current valuations already price in meaningful recovery.

JPMorgan retained Overweight, raised target from $240.00 to $265.00. Strong underlying momentum was offset by higher impairments and portfolio de-risking, with valuation reasonable but contingent on near-term earnings upgrades materialising.

UBS retained Neutral, raised target from $239.23 to $250.00. Record 2H result masked reliance on non-recurring items and tax benefits, with near-term earnings trajectory uncertain and dependent on market stabilisation.

Healthcare stocks: Sell now, ask questions later

[10:43 am] The CSL earnings downgrade is driving aggressive selling across the healthcare complex.

A similar instance occurred when Cochlear experienced its 40% one-day selloff on 22 April, which drove peers like CSL and Ebos 5.7% and 4.7% lower respectively.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

CSL | CSL | -17.7% | $98.68 | -58.7% |

PME | Pro Medicus | -3.1% | $125.45 | -49.0% |

FPH | Fisher & Paykel | -2.9% | $28.16 | -14.8% |

MSB | Mesoblast | -2.7% | $1.97 | 12.3% |

TLX | Telix Pharmaceuticals | -2.5% | $14.38 | -46.5% |

4DX | 4DMedical | -1.9% | $3.15 | 950.0% |

EBO | Ebos Group | -1.7% | $17.19 | -50.7% |

SHL | Sonic Healthcare | -1.6% | $18.65 | -29.8% |

COH | Cochlear | -1.5% | $98.39 | -62.9% |

RHC | Ramsay Health Care | -1.4% | $36.32 | 1.0% |

SIG | Sigma Healthcare | -1.2% | $2.82 | -6.5% |

ANN | Ansell | -0.9% | $26.18 | -17.7% |

RMD | Resmed | -0.6% | $28.38 | -25.3% |

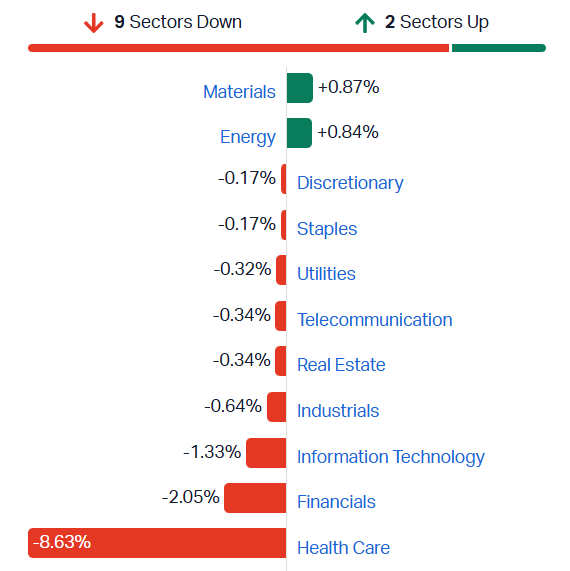

ASX 200 sharply lower as healthcare stocks tumble

[10:41 am] A very weak session outside of resources, with the S&P/ASX 200 Healthcare Index down 8.4% and trading at the lowest since October 2017. The index has effectively halved since August 2025. Financials also trading sharply lower, down CBA, ANZ, Westpac and NAB all down 1.7-3.2%.

ASX 200 sectors (Source: Market Index)

Top ASX 200 gainers

[10;21 am] Metcash and Dyno Nobel rallying off the back of today's trading updates/earnings, copper stocks also notably higher.

Ticker | Company | % Chg | Price |

|---|---|---|---|

MTS | Metcash | 9.49% | $3.00 |

DNL | Dyno Nobel | 7.68% | $3.58 |

CSC | Capstone Copper Corp | 3.88% | $12.85 |

DVP | Develop Global | 3.48% | $6.24 |

SFR | Sandfire Resources | 3.44% | $18.63 |

L1G | L1 Group | 2.92% | $1.24 |

IFT | Infratil | 2.90% | $12.76 |

PRN | Perenti | 2.15% | $2.00 |

S32 | South32 | 2.05% | $4.23 |

NWH | NRW | 1.99% | $7.17 |

Top ASX 200 losers

[10:20 am] CSL's FY26 earnings downgrade is driving broad-based selling across the healthcare complex, with names like Telix, Pro Medicus and Mesoblast all down 3-4%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CSL | CSL | -19.24% | $96.82 |

TLX | Telix Pharmaceuticals | -4.20% | $14.13 |

PME | Pro Medicus | -3.97% | $124.35 |

CBO | Cobram Estate Olives | -3.94% | $3.66 |

MSB | Mesoblast | -3.47% | $1.95 |

ANZ | ANZ Group | -3.45% | $35.52 |

ZIP | Zip Co | -3.19% | $2.43 |

EBO | Ebos Group | -3.12% | $16.95 |

MQG | Macquarie Group | -3.05% | $231.94 |

FPH | Fisher & Paykel | -3.03% | $28.12 |

CSL obliterated

[10:04 am] It doesn't get any bearish than that – CSL opened 9.0% lower ($109.00) and currently down 15.6% to $101.37.

How does CSL trade today?

[9:53 am] CSL is currently down ~5% pre-market. How do you think it'll trade today?

Dyno Nobel 1H26 beats expectations on resilient explosives performance

[9:43 am] Dyno Nobel delivered strong first half earnings growth driven by its explosives business with all key metrics beating consensus, while reaffirming FY26 guidance as it transitions to a pureplay global explosives leader.

Revenue (incl. discontinued ops) of $1.90bn vs. $1.78bn ests (7% beat)

EBIT (ex IMIs) up 39% to $242.7m vs. $227.4m ests (7% beat)

NPAT (ex IMIs) up 83% to $160.9m vs. $139.0m ests (16% beat)

Interim dividend of 4.6 cents per share vs. Macquarie ests of 4.0 cps

DNAP EBIT up 16% year-on-year to $130m on strong metals demand and geographic expansion, while DNA EBIT up 42% year-on-year to $101m on transformation initiatives and joint venture strength

$558m of the $900m on-market buyback completed to date, with buyback set to recommence from 12-May

FY26 EBIT guidance reaffirmed at $460-500m

Company page: Dyno Nobel (DNL)

Metcash sees sales momentum building in second half

[9:35 am] Metcash has guided FY26 underlying NPAT broadly in line with consensus, with positive sales momentum (ex-tobacco) continuing in the second half and additional cost initiatives flagged for FY27.

FY26 revenue guided to $19.6bn vs. $17.32bn ests (13% beat)

FY26 underlying NPAT guided to $268-270m vs. $268m ests (~1% beat at the midpoint)

Group revenue forecast to rise 0.7% year-on-year, +3.8% y/y ex-tobacco

Capex (ex-M&A) of ~$170m, ~$30m below guidance

Additional cost initiatives underway delivering at least ~$25m annualised savings in FY27 (~$15m labour, ~$10m non-trade procurement), with ~$6m restructuring cost and payback within 12 months

Liquor EBIT margin returned to long-term levels in H2, while Hardware & Tools sales momentum improved in H2 though trade market conditions remain soft

Cash realisation expected to exceed the 80-90% three-year target range, with debt leverage at the low end of the 1.0-1.75x target range

No material FY26 earnings impact from Middle East conflict, with ~$80m of precautionary inventory built up as a buffer

Company page: Metcash (MTS)

oOh!media receives another takeover bid

[9:26 am] oOh!media has received its second indicative offer in just two weeks.

I Squared Capital cash offer of $1.45 per share via scheme of arrangement, a ~15% premium to last close

Pacific Equity Partners (29-Apr) offered $1.40 cash per share

Board has determined that neither the I Squared nor PEP proposals adequately reflect the intrinsic value of oOh!

Board to grant both PEP and ISQ limited due diligence access to enable each party to put forward a revised proposal that may be capable of board recommendation

Company page: oOh!media (OML)

Elevra Lithium to divest Ewoyaa interest to Huayou

[9:24 am] Elevra Lithium has agreed to sell its entire rights and interests in the Ewoyaa Lithium Project in Ghana to Zhejiang Huayou Cobalt, providing a clean cash exit from the project.

Sale price of $71m cash for all of Elevra's rights and interests, inclusive of offtake rights, in the Ewoyaa Project

Transaction is not contingent on Huayou's separate acquisition of Atlantic Lithium, which was announced on 7-May via a $210m Scheme of Arrangement for 100% of Atlantic's interest in the project

Completion remains subject to Ghanaian regulatory approvals

Elevra had a net cash position of US$58.7 million as at 31 March 2026.

Company page: Elevra Lithium (ELV)

Inghams reaffirms FY26 guidance, flags Middle East cost pressures

[9:16 am] Inghams reaffirmed FY26 underlying EBITDA guidance at its investor day, with core poultry volumes and pricing slightly higher year-on-year, though Middle East geopolitical developments are driving material cost increases.

FY26 underlying EBITDA reaffirmed at $180-200m

FY26 (nine months) group core poultry volumes up 1.1% vs. pcp (AU +1.2%, NZ +0.5%)

FY26 (nine months) group core poultry net selling prices up 1.1% vs. pcp (AU +1.4%, NZ +2.7% in NZD terms)

Feed requirements for the remainder of FY26 fully covered in line with the 3-9 months forward cover policy, though higher feed costs are expected in FY27

Diesel fuel cost pass-through via transport providers expected to drive a $7-10m net FY26 impact after pricing actions and operational improvements, with packaging cost increases also emerging

Operating cost growth (ex-feed) materially offset by $60-80m in annualised savings from labour, procurement and site operations initiatives

Revised FY26 capex of ~$80m

Inghams has sold off fairly aggressively in recent weeks, down ~17% in the past month and trading at all-time lows. Reaffirming guidance does seem like a net positive, all things considered.

Company page: Inghams (ING)

CSL downgrades FY26 guidance

[9:14 am] CSL has lowered its FY26 guidance, with revenue and NPATA both falling short of market expectations, while flagging significant non-cash impairments across FY26-27.

FY26 revenue guided to ~$15.2bn vs. $15.79bn ests (4% miss)

FY26 NPATA guided to ~$3.1bn vs. $3.34bn ests (7% miss)

Expects to recognise ~$5bn of non-cash, pre-tax impairments across FY26 and FY27 in addition to those announced at the first half result, including CSL Vifor intangibles and under-utilised property, plant and equipment

US Immunoglobulin: ~$300m revenue impact from channel inventory normalisation, though end-customer demand growth still tracking mid-to-high single digits

Albumin in China: ~$200m revenue impact as market value declined, though CSL's share is expanding and volumes have stabilised

Other ~$150m revenue impact from Middle East conflict, revised HEMGENIX growth and iron competition

CSL Behring still expected to deliver H2 revenue growth, while CSL Seqirus performance is now expected to be moderately stronger than previously anticipated

Another ugly update from yet another healthcare heavyweight. CSL is already down 28% YTD and trading at the lowest since March 2017. The latest note from UBS (15-Apr) noted:

"Industry feedback leads us to conclude CSL’s FY26 guidance is unlikely to be met, given conditions in two key segments – US immunoglobulin and Chinese albumin."

"We have reduced our earnings forecasts to reflect these near-term pressures, while leaving our medium-term growth assumptions unchanged."

" A sustained share price recovery, however, will likely require improved supply-demand dynamics. We also look for an update on appointment of a permanent CEO."

Let's see if CSL can catch a bid if it gaps down this morning.

Company page: CSL (CSL)

Lottery Corp insiders buy shares following Victorian licence extension

[9:03 am] The Lottery Corp's CEO and chairman both bought shares after last week's Victorian Lottery licence extension.

CEO Wayne Pickup purchased 50k shares, taking his beneficial holding to 50k shares (new position)

Chairman Doug McTaggart purchased 20k shares, taking his beneficial holding to 88k shares (up 29% from 68k prior)

Last Wednesday TLC announced an early 40-year extension of its Victorian Lottery licence through to 2068, secured via a $1.15bn upfront premium funded entirely through debt

Deal broadly viewed as strategically positive, removing the renewal overhang and materially extending the weighted average remaining licence term across the portfolio

Some analysts remain cautious on the incremental net interest cost as a persistent drag on cash NPAT not fully offset by the dividend framework adjustment, with leverage rising toward the top end of the target range

Company page: The Lottery Corp (TLC)

What's bullish and bearish about markets

[8:59 am] A rundown of the key bullish and bearish drivers shaping market sentiment this week, with the AI rally extending and diplomatic traction on Iran offset by froth concerns and lagged inflation risks.

Bullish focus points:

Diplomatic solution to US-Iran conflict gained traction with reports the White House is moving toward an MoU to end the war, with ceasefire holding despite flare-ups

AI compute demand remains the dominant theme, the most notable move comes from AMD, which surged over 18% on data centre/agentic AI strength after doubling its 2030 CPU TAM estimate to over $120bn

Solid macro backdrop with US April nonfarm payrolls ~115k, unemployment steady at 4.3% and a 22nd straight month of ISM services expansion

Retail investors back in the fray at the 77th percentile vs. 1-year history, according to JPMorgan

Earnings breadth healthier than headline suggests, with BofA flagging median stock EPS growth of 11% (best since 2021) and Morgan Stanley putting it at 16%

Bearish focus points:

Near-term Iran resolution still complicated by nuclear and Strait of Hormuz sticking points, with one-sided messaging on diplomatic traction drawing scepticism

Froth concerns building with SOX 56% above its 200 day moving average, while Nasdaq top-ten names are up an average of ~784% year-on-year vs. 622% before the March 2000 peak

Physical supply disruption persists despite diplomatic headlines, with Exxon CEO warning markets aren't reflecting full fallout

Consumer resilience cracking with McDonald's flagging a worsening backdrop, citing heightened anxiety and gas price impacts on low-income consumers

Lagged inflation impact still ahead with US ISM services prices at 70.7 (highest since October 2022) and several respondents noting petroleum price increases yet to flow through

AI-related layoff announcements accelerating with Cloudflare (20% of workforce), BILL (30%), Upwork (24%), Coinbase (14%) and reportedly PayPal (20%) all cutting jobs

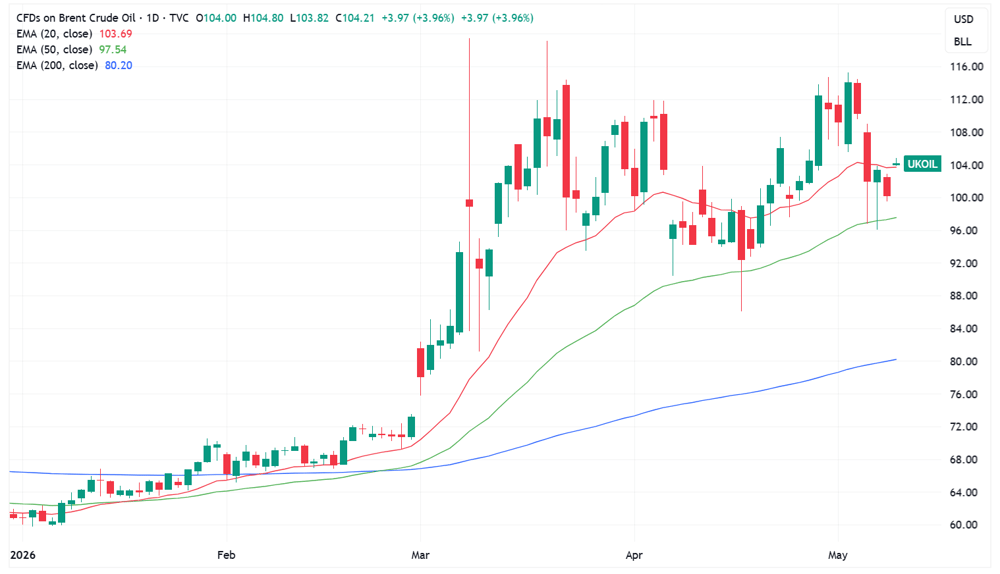

Oil prices open sharply higher

[8:52 am] Brent crude is up 4.1% in early trade on Monday to US$104.41 a barrel after Trump rejected Iran's latest peace proposal over the weekend. Though prices are still down around 8.5% from last Monday (~US$114).

Brent crude daily price chart (Source: TradingView)

Drone strike hits cargo vessel in Qatari waters as Iran ceasefire frays

[8:51 am] A drone attack briefly set a commercial ship ablaze in the Persian Gulf as markets await Iran's response to Trump's proposal to end 10 weeks of war and reopen the Strait of Hormuz.

A cargo vessel was struck in Qatari territorial waters on Sunday causing a limited fire with no injuries, while the UAE and Kuwait also intercepted hostile drones

Saudi Aramco CEO warned the oil market will only normalise in 2027 if trade and shipping remain curtailed beyond a few weeks

Aramco reported a 26% jump in Q1 profit on war-induced oil and refined fuel price gains, having redirected exports via a Red Sea pipeline

US forces struck two empty Iranian oil tankers late last week after they tried to break the blockade, with Iran calling it a ceasefire violation

Source: Bloomberg

Trump rejects Iran peace proposal as "totally unacceptable"

[8:48 am] Both sides rejected each other's latest peace proposals as the fragile ceasefire faces fresh strain, sending the US dollar and oil higher this morning.

Iran offered to transfer some highly enriched uranium to a third country but rejected dismantling its nuclear facilities, with Tehran demanding return guarantees if talks fail

Iran's demands include immediate war end, release of frozen assets, lifting of US oil sanctions, end of the Gulf of Oman blockade and ultimately Iranian management of the strait

Trump called the proposal “TOTALLY UNACCEPTABLE" in a social media post

Israeli PM Netanyahu warned the war is "not over" with more work needed to dismantle Iran's nuclear capability and remove enriched uranium stockpiles

Trump faces rising political pressure to bring down US gasoline prices ahead of the November midterm elections as Republicans aim to hold Congress

Source: Bloomberg

Trump-Xi Beijing summit eyed for trade, Iran and rare earths progress

[8:46 am] Trump's May 14-15 visit to China is expected to deliver a modest step toward stability in the world's most important bilateral relationship, with both leaders looking to claim wins.

The US wants PRC support to secure an Iran agreement and reopen Hormuz, plus Chinese commitments for significant US goods purchases (particularly agriculture) ahead of the November midterms

A new "Board of Trade" will be announced with senior officials from both countries to oversee implementation, addressing China's failure to follow through on 2020 Phase One commitments

The US is seeking expanded rare earth supply as agreed at last year's Busan meeting, plus further cooperation on blocking fentanyl precursor exports

Xi is expected to push for explicit US restrictions on Taiwan arms sales

Source: CSIS

Goldman pushes back Fed rate cuts

[8:45 am] Goldman Sachs delayed its Fed rate cut forecasts by one quarter as energy-driven inflation proves stickier than anticipated amid the ongoing Iran conflict.

Next two cuts now expected in December 2026 and March 2027, pushed back by one quarter from prior forecasts

Energy cost pass through is likely to keep core PCE inflation closer to 3% than the Fed's 2% target through the year

Terminal rate forecast kept unchanged at 3%-3.25% as FOMC participants' neutral rate projections have been fairly stable

US recession probability over next 12 months lowered to 25% from 30%, still above the 20% estimate before the Iran war began

Source: Bloomberg

US consumer sentiment hits fresh record low as gas prices bite

[8:45 am] University of Michigan sentiment fell to its lowest reading since records began in 1952 as the Iran war keeps energy prices elevated and squeezes household budgets.

Preliminary May sentiment printed 48.2, the lowest on records going back to 1952, with the Current Economic Conditions measure plunging 9% to 47.8

One-third of consumers spontaneously mentioned gasoline prices and ~30% mentioned tariffs

Sentiment is unlikely to rebound until Middle East supply disruptions are resolved and energy prices fall, with Hormuz still closed

Record-low sentiment unlikely to translate into a spending pullback given labour market resilience, with unemployment steady at 4.3% and 115k jobs added in April

US April nonfarm payrolls beat as labour market stays resilient

[8:43 am] April jobs data came in stronger than expected with non-inflationary wage growth, potentially giving the Fed more confidence to cut rates later this year.

Nonfarm payrolls up 115k vs. 65k ests

Unemployment rate ticked up to 4.34% from 4.26% vs. 4.3% ests

Average hourly earnings rose 0.2% month-on-month vs. 0.3% ests

Private payrolls contributed ~123k with job gains concentrated in health care (+37k), transport/warehousing (+30k) and retail trade (+22k)

Labour force participation fell 0.1pp to 61.8%, a fresh low since October 2021, though prime-age employment-population ratio held at 80.7%

US equities finish higher, S&P 500 and Nasdaq notch fresh record closes

[8:40 am] US stocks ended Friday near session highs, driven by another semi-led tech rally, while soft consumer sentiment and a stronger-than-expected payrolls print shaped the macro backdrop.

S&P and Nasdaq logged fresh record closes, though breadth was only narrowly positive with equal-weight S&P lagging the cap-weighted index by ~56bp

Semis/memory had a very strong session, with big tech gains led by Tesla (+4.0%), Nvidia (+1.7%) and Apple (+2.0%)

April nonfarm payrolls rose ~115k vs. ~62k ests, with March revised up to 185k from 178k, unemployment held at 4.3% and healthcare again led job gains

Preliminary May UMich consumer sentiment printed 48.2 vs. 49.5 ests, a fresh series low since 1952, with 1-year inflation expectations easing to 4.5% from 4.7%

With more than 89% of S&P companies reported for Q1, focus shifts next week to US inflation data and the Trump-Xi summit, where markets will watch for trade deal signs on rare earths, chips, soybeans and the yuan

Good morning!

[8:28 am] ASX 200 futures are down 42 pts (-0.48%) as of 8:30 am AEST.

The overnight session in a nutshell:

S&P 500 (+0.8%) and Nasdaq (+1.7%) closed at fresh record highs, capping a sixth straight week of gains on stronger-than-expected April jobs print (115k vs 65k expected), though Iran tensions clouded the weekend

Trump rejected Iran's latest peace proposal as "TOTALLY UNACCEPTABLE" Sunday after Tehran sent fresh drone attacks at UAE, Kuwait and Qatar, threatening to reignite the oil supply shock with Brent up ~4% this morning to US$104 a barrel

US consumer sentiment hit a fresh all-time low of 48.2 in early May, while Trump-Xi summit in Beijing this week (May 14-15) looms large for trade