ASX 200 Live Today - Friday, 30th January

The S&P/ASX 200 is set to bounce after a volatile overnight session. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Friday, January 30. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

ASX 200 tumbles as commodities dip

[1:40 pm] What a massive reversal. The ASX 200 is now down 0.60% despite rallying 0.49% in early trade. There's been a massive reversal across the commodity complex, notably platinum (-8.7%), copper (-5.4%), silver (-5.1%), palladium (-4.9%), gold (-3.9%) and nickel (-3.3%). Cryptocurrencies are also getting hammered, with Bitcoin down 3.5% to US$84,520, the lowest since 9 April 2025. I guess this is what happens when all commodity-related price charts are overextended, over-levered and vulnerable to pullbacks. This doesn't mean the vertical ascent can't continue, but with that, comes more volatility. While the resource sector is down 3.4%, other pockets of the market are also getting smashed, including Tech (-1.6%) and the Emerging Companies Index (-3.9%). That's all for today. Let's see how the dust settles overnight and I'll catch you all on Monday. Have a good weekend!

Analysts raise MinRes target

[12:06 pm] MinRes reported a stronger-than-expected December quarter, with broad production beats across its lithium and iron ore portfolio as well as improved cash flow and faster-than-expected debt reduction. Management upgraded their FY26 lithium production guidance at both Wodgina and Mt Marion, while Onslow's guidance of 35Mtpa was maintained.

Macquarie: Upgraded to Outperform, raised target from $56.00 to $70.00. Strong recoveries and throughput, Onslow production exceeded expectations, positive on Mt Marion underground potential.

RBC Capital Markets: Maintains Outperform, raised target from $65.00 to $67.00. Operational outperformance, stable cash generation, Onslow throughput consistent, H2 lithium costs a risk.

Jarden: Maintains Sell, raised target from $20.00 to $21.70. Net debt reduction progressing, lithium upgrades reflected in base case, Onslow upside noted, Bald Hill restart low-risk optionality.

Defence stocks broadly lower

[12:03 pm] Defence stocks are trading broadly lower on Friday, though the catalyst remains unclear. Notable decliners include Elsight (-12.6%), Orbital Corp (-11.5%), Droneshield (-4.4%), Electro Optic Systems (-3.2%) and Veem (-2.4%).

Analysts downgrade Whitehaven Coal

[11:24 am] Whitehaven delivered a strong Q2 result on Thursday, with production and sales topping market expectations. The stock rallied as much as 4.3% on the day, and finished the session 2.9% higher. Analysts were generally positive on the quarterly, but valuation emerged as a key concern.

E&P: Downgraded to Neutral, raised target from $8.00 to $9.60. Operational delivery supported by Narrabri uplift, but realised pricing weak; interim dividend forecast despite thin earnings.

Macquarie: Downgraded to Neutral, raised target from $8.75 to $10.00. Guidance tracking top end, price realisation lagged, refinance market more constructive.

Bell Potter: Downgraded to Sell, target $8.40. Narrabri lifted production and sales, but NSW pricing pressured and met coal prices expected to ease.

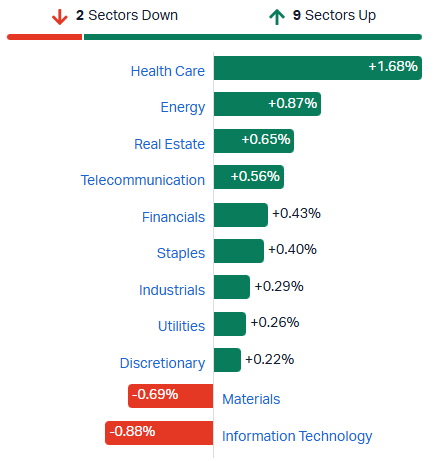

ASX 200 hits three month high, Healthcare stocks bounce

[10:59 am] ASX 200 up 0.47% in early trade, pushing intraday highs and on track to close at the highest since 29 October 2025. Healthcare sector has topped the leaderboard, though only just starting to bounce off multi-year lows. ResMed (+5.1%) sharply higher off the back of a strong Q2 result, which may be driving peers like CSL (+2.1%) and Cochlear (+1.5%) higher as well.

ASX 200 sectors (Soruce: Market Index)

Tech stocks continue to tumble

[10:15 am] Tech stocks continue to spiral lower, with the S&P/ASX 200 Tech Index down another 1.5% to the lowest since Feb-24.

The index is now down 9.1% year-to-date and down 30% in the past twelve months.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

NXL | Nuix | -4.9% | $1.75 | -3.9% |

360 | Life360 | -4.7% | $27.62 | -14.2% |

BVS | Bravura Solutions | -4.1% | $2.01 | -22.0% |

WBT | Weebit Nano | -3.5% | $5.46 | 9.2% |

CAT | Catapult Sports | -2.9% | $3.37 | -19.0% |

XRO | Xero | -2.0% | $92.97 | -18.4% |

PPS | Praemium | -1.9% | $0.78 | -2.5% |

OCL | Objective Corporation | -1.9% | $15.33 | -7.4% |

TNE | Technology One | -1.7% | $25.41 | -7.8% |

WTC | Wisetech Global. | -1.7% | $58.42 | -14.7% |

SDR | Siteminder | -1.3% | $5.14 | -16.2% |

AD8 | Audinate Group. | -1.2% | $4.24 | 4.4% |

MP1 | Megaport. | -1.0% | $11.83 | -3.2% |

HSN | Hansen Technologies | -1.0% | $5.02 | -4.9% |

MAQ | Macquarie Technology Group | -1.0% | $68.31 | 2.0% |

DTL | Data#3 | -0.9% | $9.68 | 7.9% |

CDA | Codan | -0.8% | $39.27 | 38.2% |

DDR | Dicker Data | 0.1% | $10.02 | -2.5% |

IRE | Iress | 0.2% | $8.23 | -1.8% |

ELS | Elsight | 0.4% | $4.94 | 58.1% |

NXT | NextDC | 1.1% | $13.35 | 6.2% |

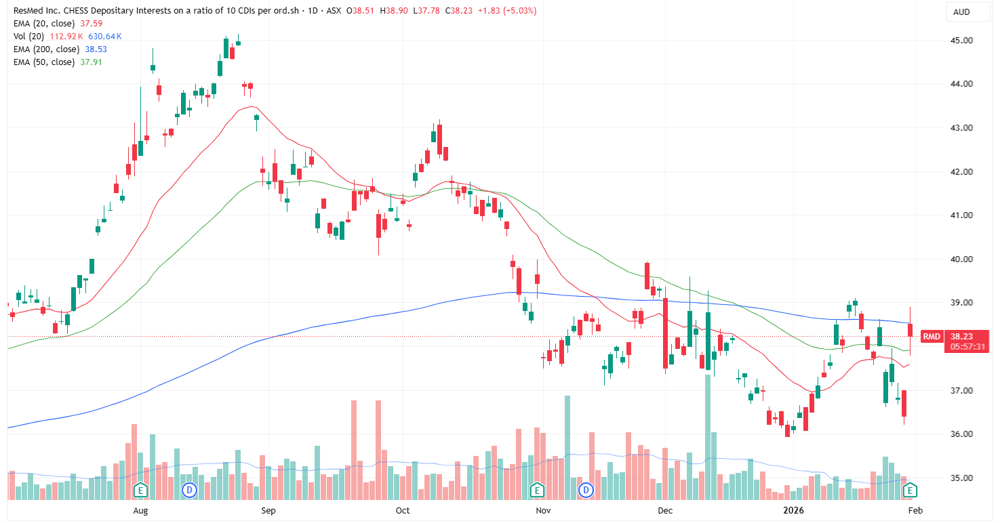

ResMed opens sharply higher

[10:03 am] A rather volatile open for ResMed, currently bouncing between a 3-6% gain after reporting a relatively clean set of numbers for the December quarter.

Revenue up 11% to $1.42bn vs $1.40bn ests (1.4% beat)

Operating income up 19% to $517.2m vs $503.9m ests (2.7% beat)

EPS ex-itemsup 16% to $2.81 vs $2.74 ests (2.6% beat)

Non-GAAP gross margin of 62.3% vs. 61.9% (40 bp beat)

ResMed is down ~15% from its August record high and mostly unchanged since late 2024.

ResMed daily price chart (Source: TradingView)

Nine Entertainment to acquire QMS and sell Nine Radio

[9:51 am] Nine Entertainment is acquiring QMS for $850 million and selling its broadcast radio assets, with both transactions expected to be EPS accretive and create near-term gains.

QMS acquisition for $850m cash and debt-free, CY26 EBITDA multiple 6.8x (effectively 6.5x after $32m cash tax benefits)

Acquisition expected to be marginally EPS accretive in FY26 (pre-synergies) and low-double digit EPS accretive including cost synergies

NPATA accretion mid-single digits pre-synergies and mid-teen including synergies

Sale of Nine Radio assets for $56m, expected completion before 30 June 2026

Total cash outlay of ~$780m, partially offset by ~$178m in cash tax losses

1H26 EBITDA growth expected

Company page: Nine Entertainment (NEC)

Origin Energy: APLNG Q2 steady production, energy markets mixed

[9:45 am] Origin Energy delivered steady APLNG production and revenue in the December quarter while electricity and gas sales declined, with new battery assets coming online and Octopus Energy expanding its customer base.

Q2 APLNG production down 0.5% quarter-on-quarter to 169.0PJ vs 169.9PJ

APLNG revenue down 1% QoQ $2.10bn

Energy Markets noted electricity sales down 7% QoQ to 8.6TWh and gas sales down 24% QoQ to 39.7PJ

Octopus Energy added ~630,000 retail customers (190,000 UK, 440,000 international), Kraken investment provides 22.7% economic interest with US$8.65bn valuation

FY26 APLNG production guidance slightly higher to 645–680PJ, up from prior 635–680PJ (0.8% upgrade at the midpoint)

FY26 capex and opex guidance unchanged at $2.9–3.2bn

Company page: Origin Energy (ORG)

Atlas Arteria Q4 toll revenue up 9.5%

[9:41 am] Atlas Arteria saw strong toll revenue growth driven by higher traffic in key assets, toll increases, and favourable FX.

Q4 proportionate toll revenue up 9.5% to $4.91bn

Q4 traffic: APRR +0.1%, A79 +7.5%, ADELAC +0.7%, Warnow -9.8%, Chicago Skyway +2.3%, Dulles Greenway +4.8%

Full-year revenue up 9.4% on 2024 supported by France traffic growth, Dulles congestion, and toll increases

Traffic at Warnow affected by prior period roadworks, others stable or growing

Company page: Atlas Arteria (ALX)

Carma delivers record December quarter

[9:38 am] Carma delivered record vehicle sales and revenue growth, supported by expanded reconditioning capacity and IPO proceeds.

Total units sold 1,199, up 66% year-on-year, including retail 746 (+29%), wholesale 453 (+166%)

Revenue up 48% to $27.4m

Gross profit up 88% to $2.5m, with gross profit per unit up 45% to $3,400

Average vehicles reconditioned per shift of 12.4, up 91%

Completed IPO raising $100m, including $70m from new shares

Expanded ‘Sell-to Carma’ footprint with three new centres and St Peters reconditioning facility scaling operations

Carma was arguably one of the most overhyped IPOs last year. The company raised $100 million at $2.70 per share, only to tumble as low as $1.50 (down 44% from the raise price) by 2 December.

Company page: Carma (CMA)

Ganfeng trims Pilbara stake for profit

[9:31 am] Ganfeng Lithium announced a reduction in its holding in Pilbara Minerals, crystallising gains while keeping its strategic partnership intact.

The Chinese lithium producer sold 32.1 million shares via block trades for $160.2 million this month, lowering its stake from 5.36% to 4.36%. The disposal is expected to generate cumulative pre-tax profits of 709 million yuan (A$145m).

Management said the sale does not affect its offtake agreements or broader cooperation with PLS.

PLS Group Q2 revenue and prices beat, production slightly below expectations

[9:30 am] PLS Group delivered higher revenue driven by stronger realised prices, though unit costs rose sharply.

Spodumene production down 7% to 208.0kt vs 214.4kt ests (3% miss)

Spodumene shipments up 8% to 232.0kt vs 219.4kt ests (6% beat)

Unit operating cost FOB A$585/t (unclear of comparable to A$397/t ests)

Realised price A$1,161 a tonne

Revenue up 49% to $373m vs $266.5m ests (40% beat)

Cash balance up 12% to $954m vs $944.7m ests (1% beat)

FY26 guidance reaffirmed, including production of 820–870kt, unit costs at A$560–600/t and capex A$300–330m

PLS also noted "strong inbound interest for offtake volumes", with "additional production capacity from the restart of the ~200ktpa Ngungaju plant is being assessed."

Company page: PLS Group (PLS)

ResMed Q2 beats expectations with strong margin expansion

[9:16 am] “Year-over-year, we delivered 11% headline revenue growth, 310 basis points of non‑GAAP gross margin expansion, and continued operating excellence ... These results reflect strong ongoing demand for our market‑leading sleep and respiratory care devices," said Resmed’s Chairman and CEO, Mick Farrell.

Revenue up 11% to $1.42bn vs $1.40bn ests (1.4% beat)

Operating income up 19% to $517.2m vs $503.9m ests (2.7% beat)

EPS ex-itemsup 16% to $2.81 vs $2.74 ests (2.6% beat)

Non-GAAP gross margin of 62.3% vs. 61.9% (40 bp beat)

NYSE-listed ResMed shares are up 2.0% after hours.

Company page: ResMed (RMD)

Apple edges higher after Q1 earnings beat

[9:13 am] Apple posted higher-than-expected overall revenue and iPhone sales, offset by weaker Mac and Wearables results. The stock is currently up 1.1% in after hours.

Revenue up 16% to $143.76bn vs $137bn ests (4.9% beat)

EPS $2.84 vs $2.67 ests (6% beat)

iPhone $85.27bn vs $78.31bn ests (9% beat)

Services $30.01bn vs $30bn ests (in-line)

Greater China $25.53bn vs $21.8bn ests (17% beat)

Segment performance:

Mac $8.39bn vs $9.13bn ests (8% miss)

iPad $8.60bn vs $8.18bn ests (5% beat)

Wearables, Home & Accessories $11.49bn vs $12.13bn ests (5% miss)

Products $113.74bn vs $107.69bn ests (6% beat)

Software sector hit by AI fears despite solid earnings

[9:08 am] Investors punish software stocks as concerns grow that AI could disrupt traditional business models and long-term revenue.

iShares Expanded Tech-Software ETF dipped 4.9% overnight, now down ~22% from recent highs and down ~13% month-to-date, worst month since Oct 2008.

ServiceNow shares down ~10% despite beating Q4 earnings and guidance, analysts say stable growth isn’t enough to shift investor narrative.

Microsoft down ~10% after slower cloud growth and softer-than-expected FY3 operating margin guidance.

SAP shares dipped 15.2% after Q4 cloud backlog growth of 16% missed 26% expectations, sparking disappointment.

Smaller software names also hit, including HubSpot -11.2%, Klaviyo -13.3%, Pegasystems -9.6%, Atlassian -10.7%, Cipher Mining -6.7%, Strategy -9.6%.

Consumer spending resilient, costs and AI shaping outcomes

[9:04 am] Some interesting takeaways as US reporting season begins to pick up steam, with companies reporting mixed trends across consumer demand, tariffs, input costs, and productivity gains from AI.

Mastercard notes strong consumer spending and balanced labour market supporting growth.

Royal Caribbean sees record start to year, leisure travel remains a consumer priority.

Southwest expects stronger RASM from pricing and new premium seating.

Levi Strauss posts strong holiday sales despite 150 bp margin hit from tariffs, plans to offset with pricing.

Caterpillar expects tariffs to rise to $2.6bn in 2026; Whirlpool absorbed ~$300m in 2025.

Housing outlook mixed, with Whirlpool and Sherwin-Williams see weak demand from mortgage lock-in, while PulteGroup expects strong spring selling season with lower rates and higher wages.

Favourite quote: Meta's CFO highlighted the impact of AI coding tools at the company, "Since the beginning of 2025, we've seen a 30% increase in output per engineer, with the majority of that growth coming from the adoption of AI-generated coding, which saw a big jump in Q4. We're seeing even stronger gains with power users of AI coding tools whose output has increased 80% year over year. We expect this growth to accelerate through the next half."

Big wave of US corporate layoffs

[9:01 am] Big wave of layoffs announced in the last few days, with most centred around corporate jobs to shrink post-pandemic workforce and leverage AI efficiencies.

Amazon ~16,000 jobs

UPS up to 30,000 jobs

Nike 775 jobs

Home Depot 800 jobs

Dow ~4,500 jobs

Pinterest <15% of workforce

Expedia ~150 jobs

European miners surge as copper hits record highs

[8:59 am] Copper prices soar amid weaker US dollar, speculative flows, and geopolitical tension, lifting European miners despite near-term fundamentals.

Copper trading above US$14,000/t for the first time, up ~25% since early December, marking the largest gain in 16 years.

Intraday volatility driven by speculative flows, particularly from China.

European miners acting as high-beta proxies to copper, with investors overlooking near-term production shortfalls and capex risks

Top 50 listed European miners added ~$476bn in market cap (~20% rise) over the past month.

Rally supported by weaker US dollar, elevated geopolitical risk, and strong investor demand for real assets, LME forward curve in contango signals adequate near-term supply despite surging prices.

Speculative frenzy on Shanghai Futures Exchange with record volumes, prompting regulatory measures like higher margins and trading restrictions to cool the market.

Microsoft and Meta recap

[8:56 am] Big moves from the two tech titans that reported quarterly results after market close on Wednesday. Microsoft shares tumbled 9.9% (but off session lows of -12.5%), while Meta shares rallied 10.4% to a three month high.

Some of the key takeaways from the results include:

Microsoft Azure grew 38% in December quarter, slightly below expectations, with March quarter guidance at 37-38%

Commercial RPO up 110%, with 55% of balance outside OpenAI. Total RPO backlog of $625bn but ~45% ($281bn) is tied to OpenAI, creating concentration risk.

Heavy capex of $37.5bn spent this quarter on chips and data centres, building infrastructure for future contracts that may not fully materialise if OpenAI changes strategy or faces funding issues.

Meta Q1 revenue guidance ~7.5% above consensus at the midpoint, implied 2026 revenue up ~$50bn year-on-year, driven by AI investments boosting engagement and monetisation.

Meta expects capex $115-135bn and expenses $162-169bn in 2026, but strong revenue and ad metrics (impression growth +18%, pricing +6%) overshadow cost concerns.

Market sees lower odds of a partial US government shutdown

[8:50 am] Negotiations between Trump and Schumer on funding and ICE reforms has eased shutdown fears, but risks remain due to timing and House dynamics.

Reports say Trump and Senate Minority Leader Schumer are negotiating options to avert a partial shutdown as funding for major departments (Homeland Security, Defense, Labour, Transportation, HUD) is due to expire at midnight tomorrow.

Plan under discussion would strip off five of six spending bills and pass a short-term stopgap for Homeland Security, buying time to negotiate potential ICE policy changes with Democrats.

Democrats have outlined broad conditions for support of ICE funding, including a uniform code of conduct, stricter warrant requirements, and body cameras for agents.

Even if an agreement is reached, funding could still lapse briefly because the House is in recess until Monday and must vote on any deal

Prediction markets show declining odds of a shutdown: Polymarket at ~76% (down from 92% mid-week) and Kalshi at ~49% (down from recent highs near 76%).

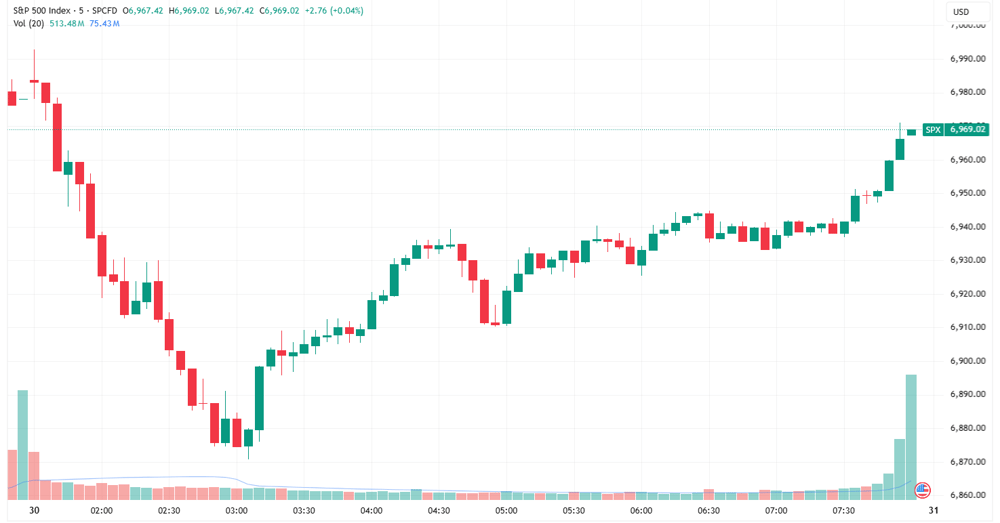

Massive overnight reversal

[8:47 am] Big overnight bounce for major US benchmarks overnight, including:

S&P 500 -0.13% vs. session low of -1.54%

Nasdaq -0.72% vs. session low of -2.62%

Russell 2000 +0.05% vs. session low of -1.41%

S&P 500 intraday chart (Source: TradingView)

Good morning!

[8:31 am] ASX 200 futures are up 23 pts (+0.25%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks mixed but finished well-above session lows

S&P 500 (-0.13%) managed to reverse a 1.5% dip in early trade and on-track for modest weekly gains

Microsoft shares (-9.9%) experience largest selloff since pandemic as Azure growth underwhelmed and AI capex sparked concerns

Gold prices set to finish the session slightly lower but experienced an almost 10% trading range on Thursday (between US$5,097 and US$5,598)

To catch up on all overnight developments, check out today's Morning Wrap.