ASX 200 Live Today - Friday, 22nd May

The S&P/ASX 200 is up for a second straight session as miners bounce. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Friday, May 22. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

Stocks recoup weekly losses, Miners rally on US-Iran peace talks

[2:00 pm] The S&P/ASX 200 is up 0.50% and trading around session highs as markets continue to hope for a peace settlement between the US and Iran. Oil prices have edged slightly lower on Friday, but down 6.0% in the last three sessions to US$104.25 a barrel. The Aussie 10-year yield is also on track to fall for a third straight session, down 18 bps to 4.92%. This pullback for oil and yields has propped up commodities prices, driving the S&P/ASX 200 Materials Index up 1.6% today and up ~4.2% in the last two sessions.

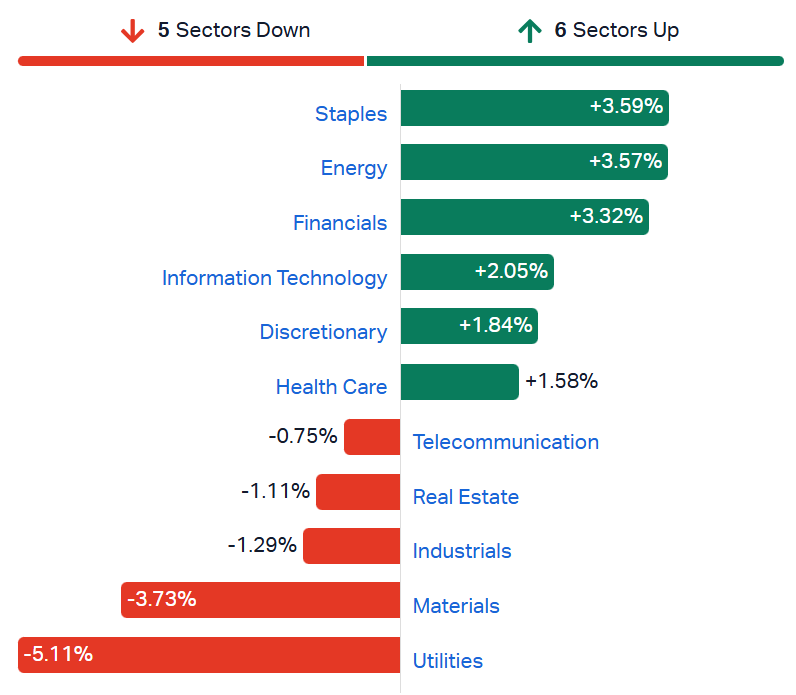

Overall, a very dicey week for markets, with volatile sector returns. Staples, Financials and Discretionary are bouncing from steep drawdowns, Materials still down for the week and Utilities on a three-day skid to the lowest since 17 March.

S&P/ASX 200 sectors, weekly performance (Source: Market Index)

A rather busy week that featured:

Another beat and raise from Nvidia (great for the insatiable AI-demand thematic)

An unexpected increase in Aussie unemployment from 4.3% to 4.5% in April (which pushed back June rate hike expectations, though a 25 bp hike is still fully priced for August)

Westpac–Melbourne Institute Consumer Sentiment Index rose 3.5% to 83 in May from 80.1 in April. Though forward-looking views deteriorated further, with the 'Economy, next 12 months' and 'Economy, next 5 years' sub-indexes dipping to 74.2 and 89.3 respectively, marking the weakest combined read since November 2022

Eurozone, UK and US PMIs all flagged a sharp increase in input costs, most of which accelerated to 2022 highs

The details of a supposed US-Iran peace deal are expected to drop today, and that'll likely be the next major market-moving catalyst (or lack thereof). Have a great weekend, and we'll see you next week.

Analysts trim Energy One target

[1:21 pm] EnergyOne delivered its first update under new CEO Ben Tranier on Thursday, flagging FY26 ARR growth of ~13% in constant currency, below the prior 15-20% guidance, with the shortfall attributed to timing as two large industrial clients pushed ~$1 million of ARR into FY27 rather than any structural or competitive weakness. The stock dipped as much as 15.0% on Thursday, closing the session down 5.9%. It's down a further 5.3% today.

Canaccord Genuity retained Buy, lowered target from $20.79 to $17.85. Viewed the ARR miss as timing rather than structural demand weakness, with pipeline growth supporting medium-term confidence but FY27 estimates carrying downside risk absent cost offsets.

Bell Potter retained Buy, lowered target from $18.00 to $17.10. Saw AI displacement fears as unwarranted and ICE's extended trading hours as a direct outsourcing tailwind, with the one-stop-shop model increasingly differentiated.

Materials bounce back continues

[1:17 pm] The S&P/ASX 200 Materials Index is currently up 1.6% and up 4.2% in the last two sessions. Though still ~4.0% off the recent 13-May high. Strong is very broad-based, spanning gold, copper, rare earths, lithium and more.

The below table observes the top ten Materials names by market cap.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

BHP | BHP Group | 1.6% | $60.04 | 55.7% |

RIO | Rio Tinto | 2.7% | $186.56 | 56.3% |

FMG | Fortescue | 0.2% | $21.76 | 35.5% |

NST | Northern Star | -0.7% | $18.81 | -3.2% |

AMC | Amcor | 1.3% | $53.97 | -23.4% |

EVN | Evolution Mining | 2.8% | $12.13 | 40.6% |

PLS | PLS Group | 2.8% | $6.33 | 368.9% |

LYC | Lynas Rare Earths | 1.5% | $18.86 | 144.9% |

S32 | South32 | 4.0% | $4.31 | 42.1% |

JHX | James Hardie | 3.2% | $28.88 | -20.5% |

Coles and Brownes fined over Dairy Code breaches

[12:52 pm] The ACCC has penalised Coles and Brownes Foods Operations for breaching the Dairy Code of Conduct over their WA milk supply arrangements.

Coles and Brownes Foods Operations were each fined $39,600 for breaches of the Dairy Code of Conduct relating to their milk supply agreements.

The breaches stemmed from terms forcing suppliers to provide milk exclusively to Coles, subject to a maximum production capacity cap.

Brownes separately contravened the Code by failing to provide suppliers with a minimum price or any explanation for pricing.

The ACCC flagged volume caps in exclusive supply agreements as a particular concern, noting they can limit farmer output and restrict supply to multiple processors.

Analysts' take on SGH

[12:50 pm] Management reiterated earnings guidance and introduced a medium-term aspiration for >10% rolling three-year EBIT growth through balanced organic and inorganic expansion, while signalling a strategic shift toward offshore acquisition opportunities given changing Australian policy and tax settings.

UBS commentary highlighted the company's sustained operating excellence and portfolio of privileged assets with high barriers to entry, while noting below-target Coates utilisation and near-term Crux first gas (no rating or target specified).

JPMorgan retained Neutral, target unchanged at $42.50, viewing domestic expansion as the most logical path despite offshore openness, with disciplined return requirements likely to extend the inorganic timeline.

RBC retained Outperform, target unchanged at $47.00, arguing the Crux project is poorly understood with minimal earnings in consensus and expecting substantial cash generation at full production plateau.

Analysts' take on Northern Star

[12:45 pm] Northern Star Resources announced on Thursday that long-serving Managing Director and CEO Stuart Tonkin will step down in Q1 FY27 after a 13-year tenure.

Analyst reaction was mixed, with brokers acknowledging the logical timing but flagging execution risks and uncertainty around the leadership handover, with some trimming targets and downgrading conviction. Shares eased 2.1% on the news.

Argonaut Securities retained Buy, lowered target from $31.00 to $29.00, flagging a tight timeline for the MD search and ongoing operational instability at KCGM, with FY26 guidance delivery and mill commissioning seen as key catalysts.

Macquarie retained Outperform, target unchanged at $25.00, noting the new leadership will weigh portfolio optimisation and Hemi decisions, though Hemi reserve and resource update timing points to potential downside versus initial expectations.

Lithium stocks broadly higher

[11:51 am] Lithium stocks are trading mostly higher at noon, though most names are on track to finish the week flattish or slightly lower. Chinese lithium carbonate futures are currently down 1.5% to 178,760 yuan a tonne, and down ~5% in the last five sessions.

Ticker | Company | % Chg | Price | 1 Week |

|---|---|---|---|---|

EUR | European Lithium | 9.9% | $0.45 | 8.5% |

PMT | Pmet Resources | 5.3% | $0.70 | -9.7% |

DLI | Delta Lithium | 2.4% | $0.21 | -8.7% |

GL1 | Global Lithium Resources | 2.0% | $0.51 | -5.6% |

AGY | Argosy Minerals | 1.5% | $0.07 | -19.5% |

PLS | Pls Group | 1.5% | $6.25 | 1.8% |

LTR | Liontown | 1.1% | $2.28 | -5.6% |

PAT | Patriot Resources | 1.1% | $0.09 | -21.7% |

IGO | IGO | 0.8% | $9.15 | 6.5% |

VUL | Vulcan Energy Resources. | 0.4% | $3.49 | -5.8% |

MIN | Mineral Resources | 0.2% | $69.41 | 2.9% |

CXO | Core Lithium | -4.9% | $0.29 | -14.7% |

INR | Ioneer | -5.3% | $0.14 | -8.4% |

Copper stocks mostly higher

[11:44 am] Copper names are trading mostly higher, with bellwether names like Sandfire up 3.7% (but still down ~1.5% for the week).

It was a volatile overnight session for copper prices, which reversed a 1.5% dip to close fractionally higher at US$6.36/lb.

Ticker | Company | % Chg | Price |

|---|---|---|---|

FFM | Firefly Metals | 3.95% | $1.98 |

SFR | Sandfire Resources | 3.72% | $18.68 |

CSC | Capstone Copper | 3.00% | $13.74 |

HGO | Hillgrove Resources | 2.33% | $0.04 |

BHP | BHP | 1.54% | $60.01 |

AR1 | Austral Resources | 1.22% | $0.08 |

29M | 29Metals | 0.78% | $0.26 |

AIS | Aeris Resources | 0.00% | $0.42 |

MC2 | Marimaca Copper | -0.82% | $8.43 |

CYM | Cyprium Metals | -1.25% | $0.40 |

HCH | Hot Chili | -1.46% | $1.69 |

CPM | Cooper Metals | -1.64% | $0.06 |

Japan core inflation slows to four-year low, clouding BOJ rate path

[11:37 am] Japan's core inflation rose at its slowest pace in four years in April and below all economist estimates, complicating expectations for a Bank of Japan rate hike next month.

Core CPI (ex fresh food) rose 1.4% year-on-year in April, the slowest in four years and below all estimates in a Bloomberg survey, while CPI ex fresh food and energy rose 1.9%, also below expectations

Government subsidies are helping contain price growth, with PM Takaichi backtracking to flag an extra budget and the reinstatement of energy subsidies

The soft reading complicates the case for a BOJ hike in June, though policymakers remain wary inflation could spread beyond energy as firms keep passing on higher labour and materials costs

Bloomberg Economics still expects the BOJ to lift its policy rate to 1% in June, citing higher oil prices likely to ripple through a broad range of items

Source: Bloomberg

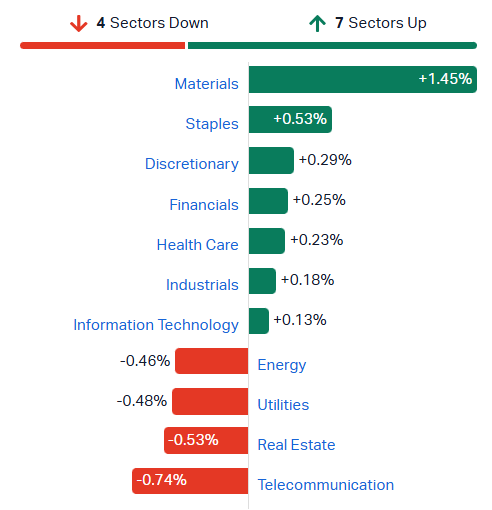

The bounce continues, ASX 200 set for a higher weekly close

[10:41 am] The ASX 200 is up 0.56% in early trade, and currently up 0.45% week-to-date. The index is receiving a big kick from Materials, which snapped a five-day losing streak on Thursday. It's now up 4.3% in the last two sessions, buoyed by strength across copper, lithium, iron ore and gold miners. Breadth is relatively positive, with 122 constituents higher (61%), though some softness in defensive pockets of the market.

ASX 200 sectors (Source: Market Index)

Guzman Y Gomez conference call adds detail on US exit

[10:35 am] GYG's business update call provided further colour on the US wind-up, with management flagging a higher FY26 dividend and a strengthening Australian growth pipeline.

FY26 dividend now projected to increase, reflecting higher group earnings and reduced US operating losses, a more positive signal than the announcement's "no impact" framing

US exit to be an orderly wind-up with all US restaurants traded or closed in 2026, and the $30-40m one-off P&L impact mostly non-cash

Australia segment underlying EBITDA guidance reiterated at ~$85m for FY26 (+29% y/y), with 32 new restaurants planned in FY26 and the medium-term target lifted to 40 openings per annum

Australian real estate pipeline continues to grow by 4 to 5 sites per month, with an 18 to 24 month lead time from commercial terms to restaurant opening

Cost discipline maintained with COGS targeted near 30% and menu price increases a last resort, aiming to keep menu inflation below industry and CPI levels

Company page: Guzman y Gomez (GYG)

Top ASX 200 gainers

[10:33 am] Rare earths, copper, aluminium and gold miners are trading broadly higher.

Ticker | Company | % Chg | Price |

|---|---|---|---|

SRL | Sunrise Energy Metals | 9.69% | $13.98 |

PDN | Paladin Energy | 5.07% | $10.98 |

ILU | Iluka Resources | 4.58% | $8.00 |

SFR | Sandfire Resources | 4.11% | $18.75 |

AAI | Alcoa Corporation | 3.57% | $93.11 |

S32 | South32 | 3.50% | $4.29 |

JHX | James Hardie | 3.29% | $28.91 |

EVN | Evolution Mining | 3.14% | $12.17 |

GNP | Genusplus Group | 3.10% | $9.83 |

GMD | Genesis Minerals | 3.00% | $6.02 |

Top ASX 200 losers

[10:33 am] Tech, REITs and energy stocks have edged lower in early trade.

Ticker | Company | % Chg | Price |

|---|---|---|---|

IAG | Insurance Australia Group | -3.44% | $7.87 |

XYZ | Block | -2.94% | $96.31 |

LLC | Lendlease Group | -2.84% | $2.91 |

GMG | Goodman Group | -1.96% | $30.25 |

MGH | Maas Group | -1.74% | $4.81 |

ALK | Alkane Resources | -1.35% | $1.47 |

BPT | Beach Energy | -1.32% | $1.12 |

XRO | Xero | -1.32% | $75.53 |

VEA | Viva Energy Group | -1.30% | $2.27 |

BXB | Brambles | -1.12% | $16.78 |

Guzman Y Gomez soars 19%

[10:18 am] Guzman Y Gomez is catching an aggressive bid after upgrading its FY26 Australian segment EBITDA and US market exit. The stock opened 10.6% higher, currently up 18.9% to $21.51.

Arafura launches $350m placement to fully fund Nolans rare earths project

[9:47 am] Arafura Rare Earths has launched a ~$350 million two-tranche institutional placement at 26 cents per share, backed by Hancock Prospecting, which alongside prior funding fully covers the equity component of the Nolans Rare Earths Project.

Two tranches (~$175.5m Tranche 1 and ~$174.5m Tranche 2, subject to shareholder approval), plus an SPP of up to $25m at the same price

Offer price of 26 cents per share or a 16% discount to last close

Largest shareholder Hancock Prospecting committed to ~$85m of the Placement, taking its interest to ~17.5%

Pro forma cash balance post settlement of ~$911m (on a 31 March 2026 basis)

Combined with ~$430m from binding equity commitments from KfW (GRMF), EFA and NRFC, and ~$481m raised in Q4 2025, the Placement fully funds the equity component required to develop the Nolans Project

Company page: Arafura Rare Earths (ARU)

Ainsworth flags sharp profit drop in 1H26

[9:43 am] Ainsworth has flagged a steep profit decline in first half of 2026 driven by reduced North American sales, partly offset by improving APAC contributions.

Revenue down 24% to $116m

Underlying EBITDA (ex currency) down 52% to $13m

Profit before tax (ex-items) down 93% to $1m

North America was the primary driver of the weakness, reflecting reduced outright sales and fewer units under gaming operations amid increased competition and adverse economic conditions

Company page: Ainsworth Game Technology (AGI)

AMP appoints Jackie Cleary as CFO

[9:33 am] AMP has appointed Jackie Cleary as Chief Financial Officer reporting to CEO Blair Vernon, finalising the executive team under the new CEO.

Cleary brings over 25 years of financial services experience, joining from Jefferies Australia where she was Managing Director and Head of Financial Institutions, prior to which she was a Managing Director at Bank of America in the Financial Institutions Group in New York

Appointment finalises AMP's executive team under Blair Vernon, following internal appointments of Rebecca McDermott as Chief People Officer and Rob Jarrett as Chief Operating Officer, with the CMO role also elevated to the executive team

Cleary will be based in Sydney and is expected to commence on 20 July 2026, subject to customary regulatory approvals

Company page: AMP (AMP)

Thoughts on Guzman y Gomez US exit

[9:30 am] GYG's decision to exit the US market and upgraded FY26 Australian EBITDA guidance seems like a net positive. Here's why.

UBS had already flagged a challenging US outlook with brand awareness as the key issue

US one-off charge of US$30-40m is materially larger than UBS estimates of US EBITDA loss of $7.9m for the second half, though the exit removes the ongoing US drag on Group earnings

UBS expected FY26 Australian EBITDA of $82.6m vs. today's guidance of $85m (2.9% beat)

Reiteration of 32 Australia openings in FY26 is consistent with UBS commentary on 19 openings completed to date

The US segment was expected to remain loss-making for years, with UBS forecasting underlying EBITDA losses of ($16.2m) in FY26, ($14.2m) in FY27 and ($12.9m) in FY28, and no clear indication of when the region would break even. Eliminating this overhang is a net positive, on top of the slight upgrade to core Australian growth expectations.

GYG shares are down 16% year-to-date, though abruptly rallied 13% on Thursday. Short interest in the stock remains elevated, at 13.82%.

Arafura halts trading pending capital raise

[9:22 am] Arafura has requested a trading halt pending an announcement regarding a proposed capital raising.

Halt to remain in place until the earlier of the Company releasing an announcement regarding the proposed capital raising, or the commencement of trading on Tuesday 26 May 2026

Arafura made a Final Investment Decision for its Nolans Rare Earths Project on Thursday, 21 May

The company has secured long-term offtakes with a portfolio of tier-one counterparties in the US, Europe and South Korea, totalling ~80% of annual NdPr production

Arafura recently raised $475m in October 2025

Company page: Arafura Rare Earths (ARU)

GYG exits US market, lifts Australia EBITDA guidance

[9:10 am] Guzman y Gomez has decided to exit the US market with immediate effect by ceasing its Chicago restaurants, while lifting Australia segment guidance and outlining the financial impact of the wind-down.

Australia segment underlying EBITDA guidance of approximately $85m in FY26, representing 29% growth on the prior year

US exit to result in a one-off P&L impact of US$30-40m in FY26 full year results, with the cash component not expected to exceed US$15m, and the one-offs not expected to impact the final FY26 dividend

Founder and Co-CEO Steven Marks said the US business was unlikely to deliver performance justifying continued investment of shareholder capital, with a turnaround requiring significantly more time and capital than expected

Australia remains the core focus with the company on track to open 32 restaurants this financial year, targeting a long-term goal of 1,000 restaurants and segment underlying EBITDA at 10% of network sales

Master franchise markets continue to perform, with Singapore opening its 24th restaurant this week and Japan planning new openings in the next 12 months

Buyback program remains active and the blackout period has been amended to commence from close of ASX trading on 30 June 2026 (previously 31 May 2026)

Company page: Guzman y Gomez (GYG)

Monadelphous secures $120m in new contracts across resources and renewables

[9:08 am] Monadelphous has announced approximately $120 million in aggregate new construction and maintenance contracts spanning Rio Tinto, Fortescue and Port Waratah Coal Services.

New five-year panel contract with Rio Tinto to provide mobile crane and lifting services across the Pilbara port and mine facilities

Three-year contract continuation with Rio Tinto for multidisciplinary sustaining capital services

Awarded the construction of a battery energy storage system (BESS) at Fortescue's Cloudbreak mine site, marking the third BESS project supporting Fortescue's decarbonisation, with work to complete in H2 2026

Appointed to a three-year panel for structural and mechanical maintenance services at Port Waratah Coal Services at the Port of Newcastle, NSW

Strong contracting momentum has seen MND shares soar 68% in the last twelve months, and up 10.7% year-to-date.

Company page: Monadelphous Group (MND)

Anthropic revenue set to more than double to $10.9bn in Q2

[9:06 am] Anthropic's revenue is projected to more than double to $10.9bn in Q2, delivering its first operating profit and likely pushing its valuation above OpenAI as part of an ongoing funding round, the WSJ reports.

Q2 revenue projected at $10.9bn, up from $4.8bn in Q1 (more than double), with the company set to deliver its first operating profit of $559m

Growth rate now exceeding Zoom during the pandemic and Google and Facebook in the run-up to their IPOs

Profitability arriving well ahead of schedule, with the company previously guiding investors last summer that full-year profit was not expected until at least 2028

Compute efficiency improving, with spending falling from 71 cents per dollar of revenue in Q1 to an expected 56 cents in Q2, helped by primarily using cheaper Google and Amazon chips rather than Nvidia

Operating profit excludes stock-based compensation and accounting methodology differs from OpenAI (Anthropic counts cloud partner sales as revenue, OpenAI does not), making direct comparisons difficult

Source: WSJ

Eurozone PMI deepens contraction, points to stagflation

[8:59 am] The Eurozone flash composite PMI fell further below 50 in May with output declining at the sharpest pace in over two and a half years, while input cost inflation hit a 3.5-year high.

Composite PMI fell to 47.5 in May from 48.8 in April, marking the second consecutive contraction and the sharpest monthly decline in output since October 2023

Services activity contracted at the fastest pace since February 2021, while manufacturing growth slowed to the weakest since January as new orders ticked down

S&P Global estimates the Eurozone economy is set to contract by 0.2% in Q2, with France leading the slowdown and Germany also contracting

Input cost inflation hit a 3.5-year high (seventh consecutive monthly acceleration), selling prices rose at the fastest pace in 38 months, and survey gauges hint at inflation running close to 4% in coming months

Employment fell for the fifth straight month at the largest pace since November 2020, with services shedding workers for the first time since early 2021

Business sentiment for the year ahead dropped to a 32-month low, with services confidence the weakest since September 2022 and France posting its first pessimism in over a year

UK PMI slumps into contraction as Middle East war weighs

[8:58 am] The UK's flash composite PMI fell into contraction for the first time since April 2025, with S&P Global flagging stagflation risk and a major quandary for the Bank of England.

Composite PMI fell to 48.5 in May from 52.6 in April, signalling a modest reduction in private sector output and ending a 12-month period of expansion

Services PMI signalled the sharpest decline in business activity since January 2021, and the lowest reading since July 2016 ex-pandemic, while manufacturing accelerated to a three-month high on customer front-loading

S&P Global estimates the economy contracted at a 0.2% quarterly rate in May, with the support from precautionary stock building likely to fade once warehouses fill

Private sector payrolls fell for the 20th consecutive month and business optimism dropped to the lowest since April 2025

Input cost inflation moderated slightly from April's 41-month high, but factory gate prices rose at the fastest pace since July 2022 on fuel surcharges and raw material pass-through from the Middle East war

US flash PMI signals stagflation risk as costs surge

[8:58 am] S&P Global's May flash PMI showed steady but modest growth alongside the sharpest input cost surge since 2022, pointing to a cooling economy with rising inflation pressure.

Composite PMI held steady at 51.7 in May, with growth over the past three months the weakest since the start of 2024, and S&P Global noting Q2 GDP may struggle to manage much more than 1% annualised

Manufacturing PMI rose to 55.3 (highest since May 2022) supported by precautionary stock building, while services growth remained sluggish and is on track for its weakest calendar quarter since late 2023

Input costs jumped at the steepest rate since late 2022 on war-related supply constraints and rising energy costs, with selling price inflation hitting its highest since August 2022

Employment fell for the second time in three months at the fastest rate since August 2024, with services jobs cut sharply while manufacturing payrolls rose to meet new orders

Sector outlooks diverged with manufacturers at their most optimistic since February 2025 on reshoring tailwinds, while services optimism hit its weakest since April 2025

Supplier delivery times lengthened to the greatest degree since August 2022, and service exports fell at the sharpest rate in six years

US and Iran reportedly close to Pakistan-mediated ceasefire deal

[8:57 am] Iran's ILNA news agency, citing Al-Arabiya TV, reports a draft US-Iran ceasefire agreement mediated by Pakistan is expected to be announced shortly.

Draft includes an immediate, comprehensive and unconditional ceasefire across land, sea and air, with mutual commitments not to target military, civilian or economic infrastructure

Freedom of navigation guaranteed in the Persian Gulf, Strait of Hormuz and Sea of Oman under a joint monitoring and dispute resolution mechanism, a key positive for oil shipping and global trade

US sanctions to be gradually lifted in exchange for Iran's compliance with the terms of the deal

Negotiations on outstanding issues to begin within a maximum of seven days

SpaceX files for record Nasdaq IPO under SPCX

[8:55 am] SpaceX has officially filed its S-1 to list on the Nasdaq in what is shaping up as a record IPO, with Starlink driving the bulk of revenue and ambitious AI and solar initiatives flagged.

IPO to list under ticker SPCX on Nasdaq with Goldman Sachs lead left followed by Morgan Stanley, BofA, Citi and JPMorgan, with the roadshow expected to kick off 8 June

Last valued at $1.25tn in February following the xAI merger, meaning new investors are buying in at a historically high price

Q1 revenue of $4.69bn with Starlink generating $3.26bn or 69% of total across 10.3 million subscribers, however Connectivity is the only profitable segment at $1.19bn while Space lost $619m and AI lost $2.5bn

AI segment R&D costs up over 300% to $5.06bn driven by GPU depreciation and infrastructure spend, with $25.45bn in contractual commitments though 95% sits in 2026 and 2027

Filing flags a $28.5tn total addressable market spanning Starlink broadband ($870bn), Starlink mobile ($740bn), X advertising ($600bn), AI infrastructure ($2.4tn) and enterprise applications ($22.7tn), which the company calls "the largest actionable TAM in human history"

Forward initiatives include orbital data centres as early as 2028 and a planned 10GW solar manufacturing facility in Bastrop, Texas, for context First Solar has about 14GW of annual domestic capacity

Some seriously cool stuff at an unworldly valuation. I don't know how analysts managed to cough up a $28.5 trillion total addressable market, I guess this is where Wall Street tells you "it's more art than science". Here's the PnL statement for your entertainment.

Source: SpaceX S-1 filing

Nvidia slips on Q1 earnings beat and guidance upgrade

[8:45 am] Nvidia shares slipped 1.7% overnight despite beating Q1 earnings expectations and lifting its Q2 guidance.

Revenue up 85% to $81.6bn vs $79.0bn ests (3% beat)

Adjusted EPS up 140% to $1.87 vs $1.77 ests (6% beat)

Data Centre revenue up 92% to $75.2bn vs $73bn ests (3% beat)

Adjusted gross margin of 75.0% vs 74.5% ests (50 bp beat)

Q2 revenue guided to ~$91.0bn vs $87.2bn ests (4% beat), assuming no Data Centre compute revenue from China

$80bn additional buyback authorisation approved and quarterly dividend lifted from $0.01 to $0.25 per share, with ~$20bn returned in Q1

Walmart Q1 tops revenue ests but guidance disappoints

[8:42 am] Walmart delivered a top line beat with strong US comps, though FY27 and Q2 EPS guidance came in below market expectations. The stock fell 7.2% overnight.

Revenue up 7% to $177.75bn vs $174.98bn ests (2% beat)

Adj EPS of $0.66 vs $0.66 ests (in line)

Walmart US comp sales up 4.1% vs ests of up 3.82% (beat)

FY27 adj EPS guidance of $2.75-2.85 vs $2.92 ests (4% miss)

Q2 FY27 adj EPS guidance of $0.72-$0.74 vs $0.75 ests (3% miss)

Management commentary on US: "Strong growth in grocery and general merchandise categories; partially offset by 100 bps headwind from maximum fair pricing legislation in pharmacy. Broad-based share gains across categories and income tiers led by upper-income households."

CFO on fuel costs: "We absorbed ~ $175 million or about 250 basis points of operating income growth from higher-than-planned fuel costs in our global distribution and fulfillment operations."

US stocks higher on ceasefire hopes and AI momentum

[8:36 am] US equities reversed earlier declines on a Saudi-mediated Iran ceasefire report, with AI-driven momentum providing further support.

Dow (+0.55%) at all-time highs, S&P 500 (+0.17%) and Nasdaq (+0.09%) eked out a small gain, clawed back earlier declines

Stocks turned higher on a Saudi media report of a potential mediated ceasefire including immediate cessation and freedom of navigation in the Strait of Hormuz, though nothing on nuclear, sparking a Treasury rally and oil selloff

Brent settled 0.2% lower to US$104.91, reversing an earlier ~4% spike to US$109

Nvidia posted a strong beat and raise on insatiable AI demand with positive takeaways on a $200bn CPU TAM, new segmentation and frontier share gains via Anthropic, though the bar remains high

Anthropic revenue projected to double to $10.9bn in Q2, achieving its first operating profit, and will rent servers using MSFT AI chips

SpaceX IPO filing revealed a $4.9bn net loss on $18.7bn in revenue in 2025

Good morning!

[8:25 am] ASX 200 futures are up 35 pts (+0.40%). The overnight session in a nutshell:

Dow Jones closed at an all-time high of 50,291 as oil pulled back, with the S&P 500 and Nasdaq eking out gains in a volatile session

US and Iran appeared to reach a draft agreement with Tehran saying the latest Washington proposal "partly bridged the gap," but details remained scarce and Supreme Leader Khamenei's decree barring enriched uranium from leaving the country clouded the outlook

Nvidia finished slightly lower despite a Q1 FY27 beat as Q2 guidance only marginally topped buy-side expectations, Walmart fell sharply on weak FY27 guidance citing fuel-cost pressures, and SpaceX publicly filed its S-1 for a record-breaking IPO at a $1.5-2 trillion valuation