ASX 200 Live Today - Friday, 1st May

The S&P/ASX 200 is set for a massive bounce after an eight-day losing streak. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Friday, May 1. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 back near session highs

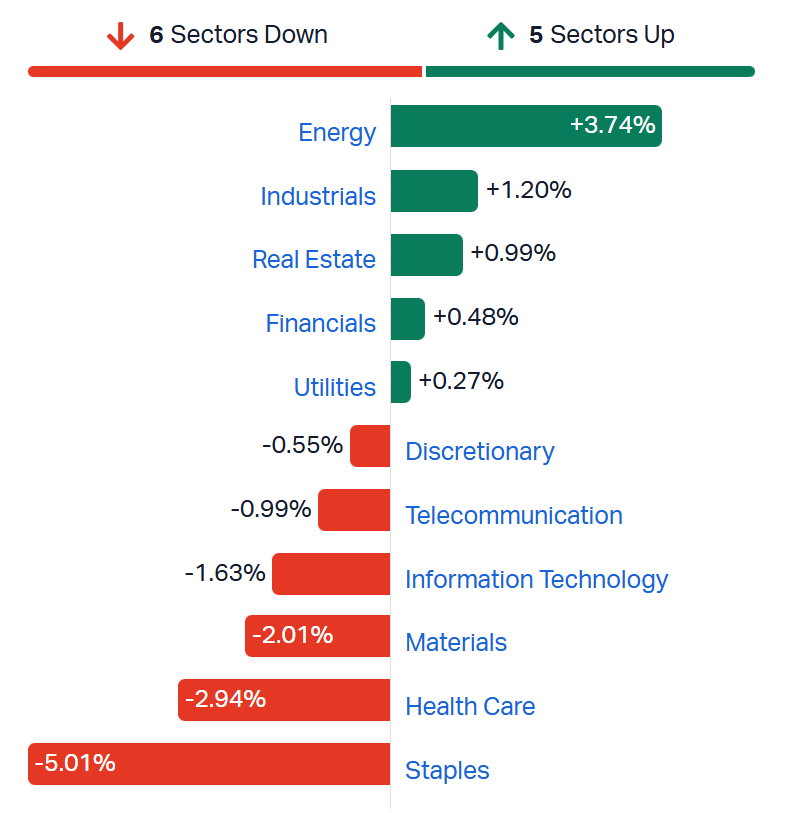

[2:10 pm] ASX 200 currently up 0.97%, trading near session highs but still down ~0.4% for the week. Broad participation, with all sectors green and 148 constituents (74%) higher. Though plenty of sectors are still trading down 1-3% for the week.

S&P/ASX 200 sectors, weekly performance (Source: Market Index)

Today mark's another mixed day for corporate updates. ANZ's 1H26 earnings came in slightly ahead of consensus, though lending revenue disappointed. Shares initially rallied 1.3% before reversing to –1.2%. Coles delivered a relatively solid Q3, but management flagged a sharp deterioration in liquor sales alongside ongoing cost pressures. The stock is up 3.4% but flat over the last two sessions.

Overall, the ASX is at this odd intersection, caught between a weak domestic backdrop and mixed global signals. Oil (Brent at US$111) and bond yields remain elevated, while Mag-7 strength continues to lift US equities without meaningfully flowing through to our market. The commodity complex remains solid, with copper trading around US$6/lb, iron ore at US$108 a tonne and gold at US$4,622/oz, despite some recent softness. Combined with Energy, that should keep ASX 200 earnings intact at the index level even as sector-level weakness accumulates. After a prolonged losing streak, the market is attempting a bounce. The near-term test is whether it can hold above the 200-day moving average and build some constructive price action from here. That's all for today, have a good weekend!

ANZ 1H26 earnings call highlights

[1:32 pm] ANZ's first half result highlighted disciplined mortgage growth, improving cost guidance and a constructive NIM outlook, with Suncorp integration tracking to plan.

NIM is expected to carry an upward bias into 2H26, driven by replicating portfolio tailwinds and the benefit of rate cuts flowing through the book

Cost reduction guidance has been upgraded to a 5% decrease for FY26, implying approximately $875m in savings, with Suncorp synergies tracked separately

Mortgage growth is being pursued selectively, with pricing discipline and process improvements prioritised over volume, reflecting a deliberate focus on margin preservation

Suncorp integration remains on track, with close to half of the migration work expected to be complete by end-2026 and no material deviations in investment spend anticipated; product harmonisation will follow migration with no significant margin headwind expected from rate alignment

The institutional book remains defensively positioned with over 90% investment grade exposure, low loss rates and strong provisioning coverage maintained even under severe stress scenarios

Coles Q3 earnings call highlights

[12:12 pm] Coles held its Q3 FY26 investor call, flagging elevated supplier price pressure and liquor market headwinds while pointing to strong e-commerce momentum and own brand growth as key offsets.

Supplier price increase requests have risen to COVID-era levels, concentrated in fresh categories including meat, dairy and produce, with elevated pressure expected to persist through the remainder of FY26

A direct fuel cost impact of $10-15m is anticipated in Q4 FY26, with management focused on cost mitigation and productivity initiatives to offset broader operational cost inflation

Liquor big box sales declined approximately 20% with subdued market-wide sentiment post-March

All e-commerce channels delivered double-digit growth, with the Uber-partnered immediacy offering the fastest-growing by percentage and CFC-led home delivery leading in dollar terms; double-digit growth is expected to be sustained over the next 12 months

Own brand sales rebounded strongly, supporting customer value amid cost-of-living pressures, with further exclusive product launches planned in Q4 FY26 alongside continued expansion of the EDLP portfolio

Supermarket sales revenue growth is expected to remain broadly in line with Q3 into Q4 FY26, with management noting no material earnings impact from current cost pressures given ongoing investment in customer value and availability

Analysts' take on MinRes

[11:46 am] Mineral Resources delivered a strong Q3 production result on Thursday, with volumes and realised pricing across iron ore and lithium broadly beating expectations despite disruption from two cyclones, and FY26 guidance upgraded across most segments.

RBC Capital Markets retained Outperform, raised target from $65.00 to $68.00. Focus is shifting from deleveraging toward FCF deployment, with lithium the standout beat and FY27 increasingly viewed as the capital return inflection point, underpinned by Onslow's credible cost performance despite diesel headwinds.

UBS retained Buy, maintained target at $73.00. Consistent operational outperformance and lithium tailwinds underpin conviction, with diesel sensitivity broadly in line with prior estimates, though a port dispute is flagged as a potential near-term overhang.

Analysts cut South32 target prices

[11:45 am] South32 announced a significant capital cost increase for its Hermosa underground zinc, lead and silver project on Thursday, with the blowout driven by contractor underperformance, labour and materials inflation, tariff pressures, and added access infrastructure.

First production has been delayed roughly one year to the second half of FY28, with nameplate capacity now not expected until FY31, and while management cited extended mine life and improved geological understanding as offsets, the magnitude of the increase exceeded market expectations.

Macquarie retained Outperform, lowered target from $5.80 to $4.50. Original feasibility assumptions proved too optimistic, with capex driven higher by shaft productivity issues, inflation and tariffs, though long-term optionality via the Clark decline is seen supporting future expansion at acceptable returns.

UBS retained Buy, lowered target from $5.20 to $4.50. Operating cost inflation and higher internal dilution reduce head grades and payables, weakening near-term cash flows, with shaft execution identified as the critical path and key remaining execution risk.

JPMorgan retained Overweight, lowered target from $5.10 to $4.80. The cost blowout reflects weak project execution and capability constraints, with the schedule delay removing near-term free cash flow delivery, and future value increasingly contingent on management discipline and operational execution.

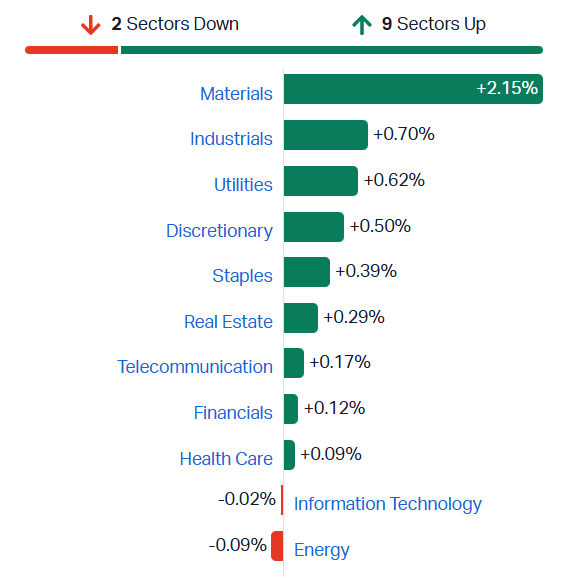

ASX 200 higher, off best levels

[10:58 am] ASX 200 currently up 0.71%, down from session highs of 1.13%. All sectors except Energy higher, and 146 constituents (73%) positive – not so surprising strength after the index fell for eight straight days.

S&P/ASX 200 sectors (Source: TradingView)

Top ASX 200 gainers

[10:15 am] Uranium, rare earth and lithium equities trading sharply higher, in-line with how peers performed overnight.

Ticker | Company | % Chg | Price |

|---|---|---|---|

NXG | Nexgen Energy | 6.56% | $17.39 |

DYL | Deep Yellow | 6.16% | $1.90 |

PDN | Paladin Energy | 5.25% | $12.13 |

ARU | Arafura Rare Earths | 4.17% | $0.38 |

LYC | Lynas Rare Earths | 3.89% | $19.75 |

MIN | Mineral Resources | 3.85% | $66.16 |

MSB | Mesoblast | 3.77% | $2.20 |

RIO | Rio Tinto | 3.55% | $173.34 |

SGM | Sims | 3.38% | $21.38 |

GGP | Greatland Resources | 3.14% | $13.79 |

Top ASX 200 losers

[10:15 am] Not many large caps trading lower today, as the ASX 200 bounces ~0.7% after an eight-day losing streak.

Ticker | Company | % Chg | Price |

|---|---|---|---|

ZIM | Zimplats | -7.84% | $16.23 |

ASK | Abacus Storage King | -1.76% | $1.40 |

MCY | Mercury Nz | -1.64% | $5.41 |

CBO | Cobram Estate Olives | -1.53% | $3.86 |

ELV | Elevra Lithium | -1.25% | $13.41 |

WDS | Woodside Energy Group | -0.88% | $33.26 |

SGP | Stockland | -0.62% | $4.03 |

LLC | Lendlease Group | -0.60% | $3.33 |

RMD | Resmed | -0.57% | $29.61 |

ALX | Atlas Arteria | -0.52% | $4.78 |

New Zealand consumer confidence slumps to three-year low

[10:13 am] New Zealand consumer confidence fell sharply in April as soaring fuel prices from the Iran war squeezed household budgets, with markets now fully pricing an RBNZ rate hike for July.

NZ consumer confidence index fell to 80.3 in April from 91.3, the lowest since May 2023

25% of consumers say it is a bad time to buy a major household item, the lowest reading since September 2024

Two-year-ahead inflation expectations jumped to 6.6% from 5.7% in March

Investors fully pricing a first 25 bp OCR hike for July, per swaps data

RBNZ has said it will look through the near-term inflation spike but remains vigilant on second-round effects on prices and wages

South Korea and Australia agree on energy supply cooperation

[10:13 am] South Korea and Australia agreed to enhance cooperation on energy security and stable diesel and LNG supplies amid Middle East-driven supply disruptions.

Joint statement signed by FMs Cho Hyun and Penny Wong covering energy resource security, including diesel, liquid fuels, LNG and condensate

Both sides agreed to notify and consult each other on any potential supply disruptions where practicable

Australia is South Korea's largest LNG supplier and a key supplier of condensate and critical minerals

South Korea is one of Australia's major suppliers of diesel and a key supplier of refined petroleum products

Source: Yonhap

Lithium stocks set to edge higher

[9:42 am] Chinese lithium carbonate futures rallied 5.0% on Thursday, surpassing 30-Jan highs of 189,440 yuan a tonne to close at 190,080 yuan.

This drove a strong response for lithium equities overnight, with Lithium Americas soaring 15.7%, Albemarle up 3.0% and SQM up 1.2%. The NYSE-listed Rare Earth/Strategic Metals ETF also gained 4.3%, breaking above its recent trading range, closing at the highest since August 2022.

Woodside struggles to sell Louisiana LNG volumes on pricing

[9:18 am] Woodside is reportedly facing pushback selling LNG volumes from its planned Louisiana export facility because its liquefaction fees sit above prevailing US market rates, with only one long-term offtake deal announced to date, according to Reuters.

Woodside initially sought liquefaction fees above $2.80/mmBtu vs. broader US market rates of $2.40-$2.50, sources told Reuters

Now reportedly offering at $2.60, in line with Cheniere, while Venture Global sits among the lowest at $2.30

Only one long-term SPA announced so far, a Uniper deal for up to 2mtpa, equivalent to about 25% of Woodside's share of plant output ex its 8mtpa portfolio retention

CEO Liz Westcott said customer interest remained strong and Woodside is "well priced in the market" as a lower-cost supplier in the next wave of LNG projects

Source: Reuters

Qantas extends capacity cuts into Q1 FY27 amid elevated fuel costs

[9:17 am] Qantas extended previously announced international and domestic schedule changes through September to mitigate sustained high fuel costs from the Middle East conflict while redeploying aircraft to capture strong Europe demand.

Group International capacity reduced by 2 percentage points for Q1 FY27 vs. previously planned levels

Domestic capacity reductions of 5 percentage points extended until end of September, predominantly on Qantas and Jetstar major capital city routes

Additional 2,000 seats per week added to and from Europe via aircraft redeployment

Perth-Rome flights extended another three months until end of October

Sydney-Bengaluru service temporarily suspended from August, resuming end of October

Trans-Tasman capacity reduced across both Qantas and Jetstar

Impacted customers being offered alternative flights or refunds

Company page: Qantas Airways (QAN)

Coles Q3 sales beat with Supermarkets momentum offsetting Liquor weakness

[9:15 am] Coles delivered a beat on group sales driven by 3.6% like-for-like growth in Supermarkets and 24.8% eCommerce growth, though Liquor missed amid weaker consumer sentiment.

Group sales up 3.1% year-on-year to $10.70bn vs. $10.66bn ests (0.4% beat)

Supermarkets sales up 4.0% to $9.78bn vs. $9.75bn ests (0.3% beat)

Supermarkets LFL up 3.6% vs. 3.3% ests, up 5.7% excluding tobacco

Liquor sales down 3.9% to $781m vs. $791.8m ests (1.4% miss)

eCommerce sales up 24.8% with penetration rising to 13.6%, reaching 14.2% in March

Supermarkets price inflation ex-tobacco moderated to 0.8% from 1.7% in Q2, reflecting fresh produce deflation

Outlook: Supermarkets sales growth broadly in line QoQ, but flagged increased supplier cost price increase requests and higher fuel, freight and packaging costs

Liquor update: continued impact from the step down in consumer sentiment observed in March, with H2 earnings to reflect reduced fixed cost fractionalisation

Coles suffered a 3.6% dip on Thursday, weighed by Woolworths' trading update which tempered FY26 earnings expectations.

The key line from Woolies' was: "Reported FY26 Australian Food EBIT growth is still expected to be in the mid to high single digit range but no longer at the upper end of the range. This reflects incremental costs associated with direct fuel exposures in Q4 as well as investments to support customers in managing their budgets in a period of rising inflation including the Price Freeze announced today."

Company page: Coles Group (COL)

ANZ H1 cash profit beats with strong returns improvement

[9:04 am] ANZ delivered a beat on cash profit driven by cost discipline and a sharp improvement in returns, with the dividend held flat but franking lifted, and management flagging FY28 and FY30 ROTE and cost-to-income targets.

Cash profit (ex-items) up 14% half-on-half to $3.78bn vs. $3.71bn ests (2% beat)

Net interest margin down 1 bp to 1.53%, in-line with Citi ests

CET1 ratio of 12.39% vs. 12.38% ests, up 36bps from September 2025

Interim dividend of 83 cps, flat YoY, franking lifted to 75% from 70%

Customer deposits up 3% to $771bn, net loans and advances down 1% to $822bn (up 1% ex-Markets)

FY28 targets: ROTE towards 12%, cost-to-income in the mid-40s sustained through FY30

FY30 ROTE target of towards 13%

FY26 gross cost savings of $875m flagged, with Suncorp Bank synergies of $500m at full run-rate by FY29

CEO Matos noted no material change in customer borrowing behaviour despite the geopolitical backdrop, with households entering the period with strong balance sheets

Company page: ANZ Group (ANZ)

ResMed Q3 beat with margin expansion and CFO transition

[8:55 am] ResMed delivered a beat on revenue and earnings driven by 11% revenue growth and 290 bps of gross margin expansion, while announcing the retirement of long-serving CFO Brett Sandercock.

Revenue up 11% to $1.43bn vs. $1.42bn ests (1% beat)

Adj. EPS of $2.88 vs. $2.80 ests (3% beat)

Non-GAAP gross margin up 290bps to 62.8%

Operating cash flow of $554m, with $262m returned to shareholders via buybacks and dividends

FY26 guidance reaffirmed: gross margin 62-63%, SG&A 19-20%, R&D 6-7%, effective tax rate 21-23%

CFO Brett Sandercock retiring effective 4 May 2026, succeeded by Aaron Bloomer who joins from Exact Sciences where he served as CFO

Company page: ResMed (RMD)

Mining ETFs more than double as supercycle thesis builds

[8:48 am] Capital is rotating sharply into hard assets, with mining ETF assets under management more than doubling year-on-year as investors position for AI infrastructure, defence and electrification demand.

Mining ETF AUM up 136% to $87.4bn at 31 March vs. $37bn a year earlier, per ETFGI data

Q1 mining inflows of $8.24bn, a $10.8bn swing from Q1 2025's $2.52bn outflow that followed Trump tariff announcements

Industrial metals favoured over gold, copper funds drew $198m in March while VanEck Gold Miners ETF (GDX) lost $710m, though still up nearly $1bn YTD

Major miners trade at 7 to 8x EV/EBITDA vs. 14x during the 2008-2010 boom, suggesting upside if the thesis plays out

BlackRock's Evy Hambro called it "the early stages of a commodity supercycle", citing grid, data centre, EV and charging infrastructure demand

Regal Partners' Charlie Aitken sees copper prices potentially doubling or tripling over the next decade

Source: Reuters

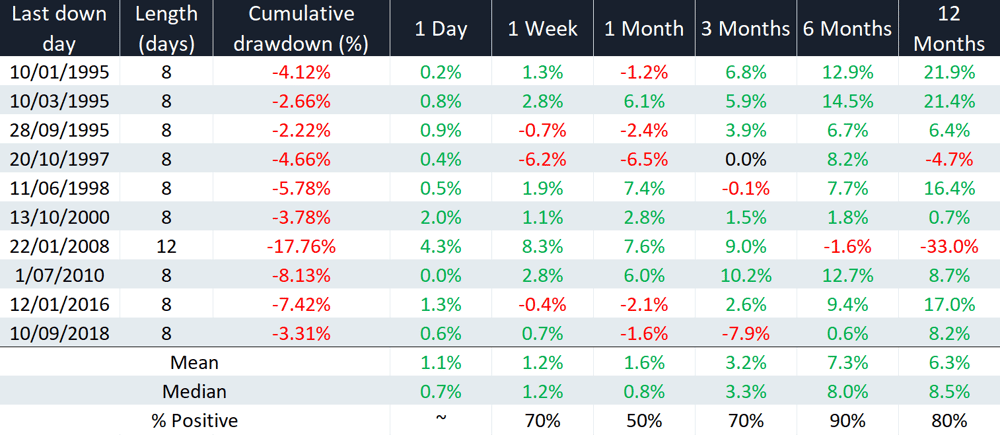

ASX 200 set to snap 8-day losing streak

[8:46 am] ASX 200 futures pointing towards a 1.46% bounce this morning.

Since 1994, the index has only recorded ten instances of falling for eight or more straight days. Nine of those were exactly eight days, while the January 2008 spiral ran for twelve. The green day that followed these losing streaks averaged a 1.1% gain.

Source: Market Index

Iran threatens "long and painful strikes" as Hormuz remains closed

[8:42 am] Iran warned of severe retaliation against any new US attack while restating its claim to the Strait of Hormuz.

Iran's Revolutionary Guards warned any new US attack, even limited, would trigger "long and painful strikes" on US regional positions

Trump reportedly weighing options including fresh strikes, ground forces to seize part of the strait, extending the US naval blockade, or declaring unilateral victory

US State Department invited partner nations to join a new Maritime Freedom Construct coalition to reopen the strait, though France, Britain and others say they will only assist once the conflict ends

Trump faces a formal Friday deadline to end the war or seek a Congressional extension, with analysts expecting a 30-day extension notification or the deadline simply being disregarded

ECB holds rates at 2% as Iran war complicates outlook

[8:41 am] The ECB kept its deposit rate at 2% but flagged intensifying upside inflation risks and downside growth risks tied to the Iran conflict, leaving June live for a potential hike.

Deposit facility rate held at 2%, with the ECB stressing upside risks to inflation and downside risks to growth have intensified

Euro zone flash inflation jumped to 3% in April, driven by energy costs, while Q1 GDP growth slowed to just 0.1%

Lagarde noted "the economic outlook is highly uncertain" and depends on the duration of the Middle East conflict and energy market spillovers

US economy splits as inflation reaccelerates and growth disappoints

[8:40 am] A trio of US data prints showed inflation pushing higher on Iran-driven energy costs, GDP growth missing expectations, and jobless claims hitting a generational low, complicating the Fed's path.

March core PCE up 0.3% m/m in line with 0.26% ests

Annualised core PCE of 3.2% y/y also in-line, but is the highest since Nov-23

Headline PCE up 0.7% m/m vs. 0.6% ests, with energy goods and services surging 11.6%

Q1 GDP up annualised 2.0% vs. 2.3% ests, with inventories and net exports a drag

Business spending on equipment and structures up 10.4%, the fastest in nearly three years, with equipment up 17% and IP up 13% reflecting AI capex

Initial jobless claims of 189,000 vs. 212,000 ests, the lowest since September 1969

Caterpillar Q1 beats, AI boom boosts power sales

[8:37 am] Caterpillar delivered a clean beat on both top and bottom line, with management seeing surging demand for its power and energy equipment. Chief Executive Joe Creed says the company's backlog for some power-generation equipment has more than tripled since 2024.

Revenue of $17.4bn vs. $16.49bn ests (6% beat)

EPS of $5.54 vs. $4.63 ests (20% beat)

Cat Financial revenue up 10% to $947m, profit up 11% to $144m, profit before tax up 12% to $195m

Retail new business volume up 8% to $3.19bn, total assets of $38.16bn

Past dues improved to 1.39% from 1.58% YoY, though write-offs net of recoveries rose to $29m from $20m

Caterpillar is the 22nd largest company on the S&P 500, and a key Dow component. The stock's 9.8% rally accounted for the bulk of the Dow move.

Eli Lilly Q1 beats and raises on GLP-1 momentum

[8:35 am] Eli Lilly delivered a major beat across the board with Mounjaro and Zepbound driving 56% revenue growth, and lifted FY26 guidance following FDA approval of its oral GLP-1 pill Foundayo.

Eli Lilly is the 12th largest stock on the S&P 500, and finished the session up 9.8%.

Revenue up 56% to $19.80bn vs. $17.77bn ests (11% beat)

Adj. EPS up 156% to $8.55 vs. $7.06 ests (21% beat)

Mounjaro up 125% to $8.66bn vs. $7.21bn ests (20% beat)

Zepbound up 80% to $4.16bn vs. $4.03bn ests (3% beat)

FY26 revenue guide raised to $82bn-$85bnvs. $80bn ests (4% beat) and prior $80bn-$83bn

FY26 adj. EPS guide raised to $35.50-$37.00 vs. $33.50 ests (8% beat) and prior $33.50-$35.00

FDA approval of Foundayo, the only approved GLP-1 pill that can be taken any time of day without food or water restrictions, flagged as meaningfully expanding the GLP-1 addressable patient base

Apple Q2 earnings beat with record March quarter

[8:33 am] Apple reported its Q2 after market close today, with a strong beat across revenue and EPS, driven by record iPhone demand and standout growth in Greater China.

Revenue up 16.6% to $111.18bn vs. $109.66bn ests (1% beat)

EPS up 21.8% to $2.01 vs. $1.96 ests (3% beat)

iPhone revenue up 21.7% to $56.99bn vs. $56.98bn ests (in line), a March quarter record fuelled by iPhone 17 demand

Services revenue up 16.3% to $30.98bn vs. $30.37bn ests (2% beat)

Greater China revenue up 28.1% to $20.50bn vs. $18.91bn ests (8% beat), the standout geographic performer

Operating cash flow over $28bn, dividend lifted 4% to $0.27 per share, additional buyback authorisation of up to $100bn

Management flagged double-digit growth across every geographic segment and a new all-time high installed base

Apple shares are currently up 3.7% in after hours trade.

US equities close out best month since 2020 on strong Q1 earnings

[8:30 am] US equities finished higher Thursday with the S&P 500, Nasdaq and Russell hitting fresh record closes, capping the best month since November 2020 on the back of strong Q1 earnings.

S&P 500 and Nasdaq closed at record highs with breadth very positive (equal-weight S&P 500 up 1.51%), while small-caps, most-shorted names and retail favourites also rallied

Mag 7 takeaways mixed but supportive of the dominant market theme of insatiable compute demand and massive capex

Alphabet the standout (63% Google Cloud growth, near doubling of Cloud backlog, 19% Search growth, big OI beat)

Amazon positive on fifth straight quarter of AWS acceleration

Microsoft and Meta lagged despite solid Azure prints and on underwhelming Q2 revenue guide/higher FY capex respectively

Nearly 60% of S&P 500 has reported with Q1 metrics looking very strong

AI compute/infrastructure remains the dominant secular theme

Consumer resilience and pricing power bright spots

Geopolitics, raw materials costs, travel slowdown and adverse early-2026 weather flagged as cautious takeaways

Good morning!

[8:23 am] ASX 200 futures are up 127 pts (+1.46%) as of 8:30 am AEST.

The overnight session in a nutshell:

S&P 500 (+1.02%), Nasdaq (+0.89%) and Russell 2000 (+2.21%) closed at fresh all-time highs

S&P 500 and Nasdaq rallied 10.4% and 15.2% respectively in April, the best monthly performances since November 2020

Sharp gains from Alphabet, Caterpillar and Eli Lilly, along with a slight pullback in oil prices and bond yields sent markets sharply higher

Commodity broadly higher after the recent 2-3 day losing streak