ASX 200 Live Today - Friday, 15th May

The S&P/ASX 200 is set to snap a five-day losing streak, as Wall Street continues to rally into fresh highs. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Friday, May 15. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 gives up early gains

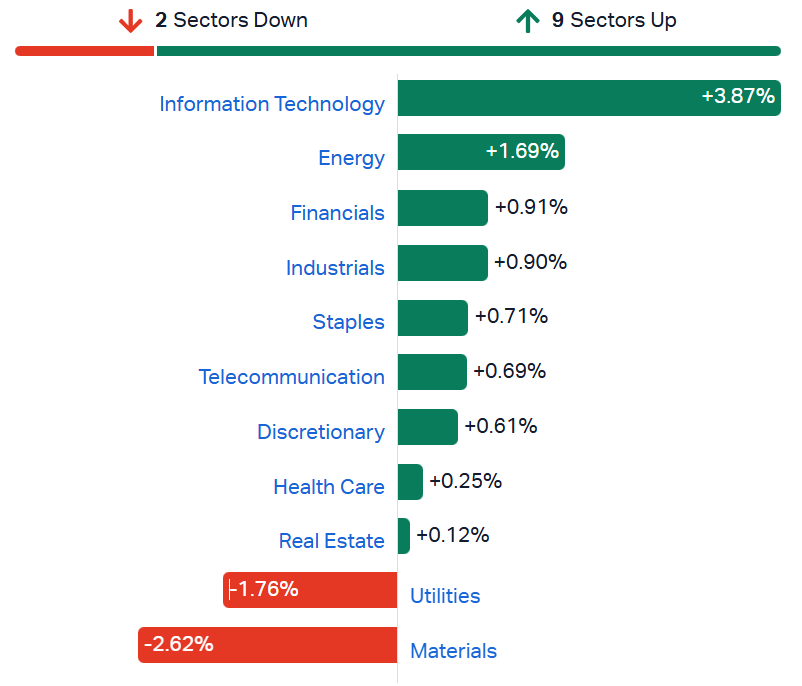

[1:55 pm] ASX 200 rallied as much as 0.59% in early trade, now down (-0.12%). Despite most sectors trading in positive territory, breadth is barely positive, with just 111 constituents higher (56%). The index is struggling after Financials (+0.91%) fell from session highs of 1.91% and Materials (-2.6%) experience a sharp pullback from near-record highs.

S&P/ASX 200 sectors (Source: Market Index)

The ASX 200 is currently down 1.27% for the week against a downbeat backdrop of government budget changes, rising bond yields (Aussie 10-year remains rangebound but at an elevated 5.05%) and a firmer US dollar (DXY at 99.04). Below are the best and worst performing S&P/ASX 200 stocks of the week. That's all for today, have a good weekend!

Ticker | Company | Price | 1 Week | 1 Year |

|---|---|---|---|---|

4DX | 4DMedical | $4.09 | 20.1% | 1261.7% |

MI6 | Minerals 260 | $0.85 | 13.4% | 503.6% |

CSC | Capstone Copper Corp. | $13.61 | 12.0% | 71.1% |

MAH | Macmahon | $0.86 | 11.9% | 213.5% |

CBO | Cobram Estate Olives. | $4.14 | 11.9% | 119.0% |

DNL | Dyno Nobel | $3.68 | 11.7% | 37.6% |

ALL | Aristocrat Leisure | $51.67 | 10.9% | -19.2% |

NWH | NRW | $7.68 | 10.4% | 228.0% |

LNW | Light & Wonder | $113.80 | 8.2% | -13.4% |

SFR | Sandfire Resources | $18.96 | 8.2% | 78.8% |

Ticker | Company | Price | 1 Week | 1 Year |

|---|---|---|---|---|

CSL | CSL | $97.52 | -19.8% | -59.2% |

ELV | Elevra Lithium | $11.17 | -16.7% | 337.8% |

PDN | Paladin Energy | $10.54 | -15.4% | 63.1% |

WTC | Wisetech Global | $38.28 | -13.0% | -62.4% |

KCN | Kingsgate | $6.05 | -12.2% | 205.6% |

DRO | Droneshield | $3.32 | -10.0% | 158.4% |

LYC | Lynas Rare Earths | $17.79 | -9.8% | 140.4% |

CBA | Commonwealth Bank | $159.71 | -9.6% | -5.5% |

REA | REA Group | $163.13 | -9.1% | -34.8% |

360 | Life360 | $18.37 | -8.1% | -38.5% |

Ventia renews Yarra Valley Water contract

[1:44 pm] Ventia Services Group has secured a nine-year, $405 million maintenance services contract renewal with Yarra Valley Water, extending a partnership dating back to 2015.

Contract valued at $405m over nine years, consolidating existing sewerage, water network reactive maintenance and mechanical/electrical planned and reactive maintenance

Ventia secured the South region under Yarra Valley Water's new two-partner delivery model (split into North and South)

New arrangements commence October 2026, extending a relationship in place since 2015

Company page: Ventia Services Group (VNT)

Lithium prices claw back losses

[1:42 pm] Chinese lithium carbonate futures currently down 0.5% to 194,680 yuan a tonne, up from session lows of (-3.8%). Despite the intraday reversal, most lithium stocks have yet to bounce.

Ticker | Company | % Chg | Price |

|---|---|---|---|

PMT | Pmet Resources | -8.23% | $0.73 |

MIN | Mineral Resources | -7.37% | $64.99 |

CXO | Core Lithium | -7.14% | $0.33 |

LTR | Liontown | -6.60% | $2.34 |

AGY | Argosy Minerals | -6.17% | $0.08 |

INR | Ioneer | -5.00% | $0.15 |

PLS | PLS Group | -4.62% | $6.09 |

DLI | Delta Lithium | -4.26% | $0.23 |

PAT | Patriot Resources | -4.17% | $0.12 |

IGO | IGO | -3.31% | $8.47 |

VUL | Vulcan Energy | -3.11% | $3.59 |

GL1 | Global Lithium | -2.86% | $0.51 |

EUR | European Lithium | -0.71% | $0.42 |

WR1 | Winsome Resources | 0.94% | $0.54 |

Top All Ords gainers and losers

[12:42 pm] Small-to-large cap tech stocks are posting outsized gains at noon, while resource stocks (spanning tungsten, lithium and gold) lag.

Ticker | Company | % Chg | Price |

|---|---|---|---|

WBT | Weebit Nano | 11.51% | $6.78 |

TYR | Tyro Payments | 9.71% | $0.76 |

ELS | Elsight | 9.68% | $6.57 |

XRO | Xero | 9.33% | $80.56 |

RAC | Racura Oncology | 8.66% | $2.76 |

DTR | Dateline Resources | 8.50% | $0.22 |

FRS | Forrestania Resources | 8.49% | $0.58 |

CVL | Civmec | 6.47% | $1.65 |

DUG | Dug Technology | 5.86% | $2.35 |

NXL | Nuix | 5.54% | $1.43 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

SPL | Starpharma | -9.85% | $0.60 |

KCN | Kingsgate | -9.75% | $6.16 |

EQR | EQ Resources | -8.36% | $0.25 |

PMT | Pmet Resources | -8.23% | $0.73 |

TGN | Tungsten Mining | -8.16% | $0.23 |

BNZ | Benz Mining Corp | -8.12% | $2.15 |

BGP | Briscoe Group | -8.08% | $3.64 |

MIN | Mineral Resources | -8.01% | $64.54 |

LTR | Liontown | -7.40% | $2.32 |

ELV | Elevra Lithium | -7.37% | $11.18 |

Japan's corporate goods prices surge

[12:40 pm] Japan's April corporate goods prices posted their largest monthly jump in 12 years, reinforcing expectations the BOJ will resume rate hikes at its June meeting.

Input prices up 2.3% month-on-month, a full percentage point above the highest Bloomberg survey estimate and the biggest jump since April 2014 (when the sales tax was raised)

Outside the 2014 tax-driven spike, this was the largest monthly increase since 1980

Producer prices up 4.9% year-on-year, the biggest gain in three years and above all projections

Gains led by higher oil and naphtha prices, with the war in Iran cited as boosting inflationary pressures and raising supply shortage concerns

Source: Bloomberg

Analysts' take on Xero

[11:59 am] Xero delivered a result in line with expectations on Thursday, with revenue and EBITDA marginally ahead of consensus and first-time FY27 guidance landing above market expectations. The stock tumbled 9.0%, which may be attributed to outsized R&D capitalisation, stock-based compensation and other factors that overstate true free cash flows.

JPMorgan retained Overweight, target unchanged at $150. FY27 guidance credibly establishes a path to Rule of 40, with Melio integration ahead of schedule and AI product launches addressing disruption concerns.

RBC Capital Markets retained Outperform, lowered target from $155 to $130. US segment is delivering growth while absorbing brand investment and Melio take-rate expansion shows operating leverage, though AI aggregator risks threaten bargaining power and margins.

Copper tumbles from record highs

[11:29 am] Copper is down 2.4% to US$6.43/lb in early trade, driving names like BHP and Sandfire ~3% lower.

Ticker | Company | % Chg | Price |

|---|---|---|---|

AR1 | Austral Resources | -6.67% | $0.10 |

HCH | Hot Chili | -6.65% | $1.76 |

FFM | Firefly Metals | -4.34% | $2.10 |

AIS | Aeris Resources | -4.26% | $0.45 |

HGO | Hillgrove Resources | -4.17% | $0.05 |

29M | 29Metals | -3.33% | $0.29 |

CYM | Cyprium Metals | -3.12% | $0.47 |

SFR | Sandfire Resources | -3.04% | $19.15 |

BHP | BHP Group | -2.98% | $60.21 |

CSC | Capstone Copper | -1.51% | $13.70 |

MC2 | Marimaca Copper | -0.44% | $9.11 |

Analysts' take on Megaport

[11:22 am] Megaport announced three major fixed-term contracts via its subsidiary Latitude.sh on Thursday, validating the acquisition thesis and signalling rapid expansion from network connectivity into full-stack cloud and AI infrastructure, with take-or-pay terms providing earnings visibility and ~2-year payback periods supporting attractive returns. The stock finished the session 27.7% higher.

E&P retained Positive, raised target from $23.58 to $25.08. Latitude deals roughly tripled the ARR base, with edge cloud positioning and hardware scarcity underpinning medium-term success.

Macquarie retained Outperform, raised target from $23.30 to $26.30. Contracts deliver >20% IRR while compute and storage products improve base network churn and margins, with multiples looking undemanding versus earnings growth.

JPMorgan retained Overweight, raised target from $14.00 to $16.00. Contract wins validate the full-stack cloud and AI strategy, with 3-year contracts and 2-year payback supporting strong asset economics amid hardware supply tightness.

Insider Trades: Mineral Resources

[10:47 am] Mineral Resources managing director Chris Ellison has disclosed his first sale of shares since December 2017, offloading 1.75 million shares for personal financial planning purposes.

Ellison sold 1,750,000 MinRes shares on-market between 11 and 14 May 2026

Sale proceeds for personal financial planning, including setting up a family office, and conducted under MinRes' Securities Trading Policy

First disposal by Ellison since December 2017

Retains 20,834,661 shares (10.54% of issued capital), remaining the company's largest shareholder after 33 years

Company page: Mineral Resources (MIN)

ASX 200 higher as battered tech and bank stocks bounce

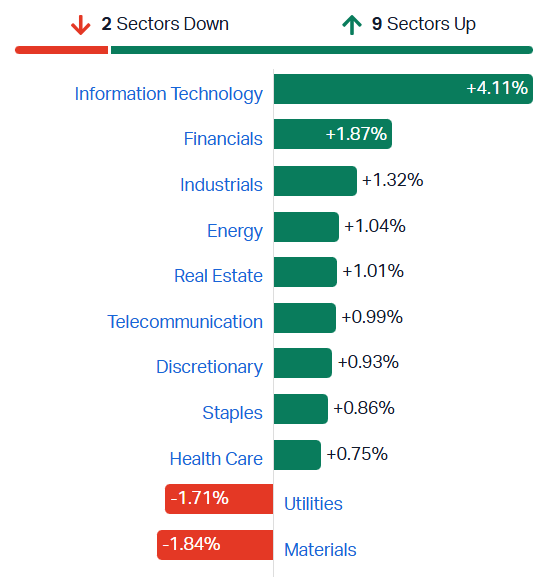

[10:44 am] The S&P/ASX 200 is up 0.47% in early trade, with relatively broad participation across most sectors. Tech and banks are bouncing after suffering sharp declines for most of this week. However, week-to-date, Materials (+1.6%) and Discretionary (+0.3%) are the only two sectors in positive territory.

S&P/ASX 200 sectors (Source: Market Index)

Banks bounce, still sharply lower for the week

[10:13 am] Most major banks up around 1% in early trade, but still down 3-5% for the week (with CBA down a massive 9.9% week-to-date).

Ticker | Company | % Chg | Price | 1 Week % |

|---|---|---|---|---|

JDO | Judo Capital | 2.17% | $1.41 | -5.05% |

CBA | Commonwealth Bank | 1.75% | $159.16 | -9.95% |

BEN | Bendigo & Adelaide Bank | 1.27% | $10.40 | -3.08% |

ANZ | ANZ Group | 1.12% | $35.23 | -4.68% |

BOQ | Bank Of Queensland | 0.97% | $6.23 | -1.58% |

WBC | Westpac | 0.95% | $36.06 | -4.85% |

NAB | National Australia Bank | 0.58% | $36.63 | -5.76% |

MQG | Macquarie Group | 0.32% | $245.32 | 0.46% |

Lithium prices test psychological resistance as Macquarie flags FOMO meets margin compression

[10:10 am] Macquarie sees 200,000 yuan a tonne (US$29,500/t LCE) as a key inflection point where investor FOMO meets downstream margin compression.

Spot spodumene (SC6%) trading above US$2,800 a tonne and China lithium carbonate at ~US$28,000 a tonne

The 200,000 yuan a tonne level flagged as the threshold where ESS project economics in Southeast Asia and China face pressure

Earnings sensitivity: PLS shows ~16% earnings impact per 10% lithium price move, ELV NPV most sensitive at +16% per 10% uplift, followed by PLS at 15%

Zimbabwe represents ~8% of global mine supply (LCE basis) and is the key near-term supply catalyst, with export quotas creating discretionary government approval framework and a hard concentrate export ban targeted by 1 January 2027

China auto manufacturing margins already compressing to 3.2% in Q1 CY26 from 3.4% in Q4 CY25 and 4.1% for CY25, an early warning on downstream demand elasticity

Multiple supply restarts in motion (PLS P2000), yet price strength persists on resilient ESS demand and Jianxiawo restart delay risk into 3Q CY26 or later

Lithium stocks tumble

[10:09 am] Lithium stocks are trading sharply lower after Chinese carbonate prices fell 5.0% on Thursday.

Ticker | Company | % Chg | Price |

|---|---|---|---|

MIN | Mineral Resources | -5.89% | $66.03 |

PMT | Pmet Resources | -5.06% | $0.75 |

LTR | Liontown | -4.00% | $2.40 |

CXO | Core Lithium | -3.71% | $0.34 |

AGY | Argosy Minerals | -3.70% | $0.08 |

PLS | Pls Group | -3.45% | $6.16 |

INR | Ioneer | -3.13% | $0.16 |

IGO | IGO | -2.45% | $8.55 |

DLI | Delta Lithium | -2.13% | $0.23 |

VUL | Vulcan Energy Resources | -1.76% | $3.64 |

GL1 | Global Lithium Resources | -0.95% | $0.52 |

EUR | European Lithium | 0.00% | $0.42 |

PAT | Patriot Resources | 0.00% | $0.12 |

WR1 | Winsome Resources | 0.94% | $0.54 |

Tech stocks bounce

[10:06 am] The S&P/ASX 200 Tech Index is up 3.3% in early trade, but still down ~3% in the last six sessions. Xero (+6.3%) experiencing a strong bounce after Thursday's results-driven selloff and Megaport continues to rally despite surging ~27% yesterday.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

XRO | Xero | 6.39% | $78.39 | -54.56% |

MP1 | Megaport | 5.41% | $13.26 | 1.61% |

WBT | Weebit Nano | 3.45% | $6.29 | 238.17% |

NXL | Nuix | 3.32% | $1.40 | -41.67% |

CAT | Catapult Sports | 3.06% | $3.20 | -22.83% |

HSN | Hansen Technologies | 2.97% | $4.86 | -2.02% |

SDR | Siteminder | 2.55% | $3.02 | -31.16% |

TNE | Technology One | 2.51% | $28.20 | -13.28% |

360 | Life360 | 2.50% | $18.85 | -36.85% |

OCL | Objective Corporation | 2.49% | $10.70 | -38.47% |

CDA | Codan | 2.49% | $41.22 | 142.61% |

WTC | Wisetech Global | 2.40% | $37.55 | -63.14% |

BVS | Bravura Solutions | 2.31% | $2.21 | 3.76% |

PPS | Praemium | 2.16% | $0.71 | -4.05% |

DTL | Data#3 | 1.88% | $8.12 | 2.78% |

NXT | NextDC | 1.69% | $15.05 | 9.88% |

AD8 | Audinate Group | 1.38% | $2.20 | -68.88% |

IRE | Iress | 1.28% | $5.94 | -30.58% |

DGT | Digico Infrastructure Reit | 0.73% | $2.75 | -16.92% |

MAQ | Macquarie Technology Group | 0.48% | $77.57 | 19.85% |

PME | Pro Medicus | -0.16% | $121.41 | -55.45% |

DDR | Dicker Data | -0.55% | $8.97 | 2.75% |

Macquarie cuts Bapcor target by 27%

[9:34 am] Macquarie maintains a Neutral rating on Bapcor with a lower target price after the company cut FY26 EBITDA guidance by ~5% at the midpoint, citing Middle East conflict and rate-driven trading deterioration since late March.

FY26 adjusted EBITDA guidance cut to $144-150m from $150-160m, a ~5% cut at the midpoint

Macquarie EPS estimates cut materially, with FY26 down 39%, FY27 down 38%, FY28 down 29%

Target price cut to $0.44 from $0.61, set at the bottom of the unchanged 10-12x EV/EBIT range

Feb-April sales growth was positive across all units but trading conditions materially deteriorating from late March

Net debt improved to ~$168m at end-April from proforma $195m at end-Dec 2025 post-equity raise, though softer revenue is deferring some working capital benefits into FY27

Three drivers of the downgrade: Softer trading from weaker consumer/business confidence, persistent fuel/freight/supplier cost pressure, and NZD/AUD depreciation hitting NZ earnings

Astral Resources hits 358m at 1.03 g/t Au at Mandilla

[9:32 am] Astral has returned a significant deep intercept at its Mandilla project in WA, with the mineralisation sitting largely outside the existing 1.4Moz Theia resource.

Headline intercept of 358.23m at 1.03 g/t Au from 256.17m, a thick bulk-tonnage style hit

Higher-grade zone of 15.70m at 3.40 g/t Au from 320.44m, including a spectacular 0.43m at 121.6 g/t

Further 81.46m at 1.35 g/t Au from 515.04m, including 1.13m at 42.7 g/t

Additional zones of 9.41m at 1.93 g/t (with hits of 14.6 g/t and 21.5 g/t) and 5.75m at 2.00 g/t

Mineralisation occurs largely outside the current 1.4Moz Theia MRE

Company page: Astral Resources (AAR)

Vicinity Centres acquires Eastern Creek Quarter for $400m

[9:29 am] Vicinity has exchanged contracts to acquire the Eastern Creek Quarter hybrid retail asset in Western Sydney from Frasers Property, lifting its metropolitan Sydney exposure and Outlet centre network.

Purchase price of $400m, expected to settle 30 June 2026 subject to landlord consent for ground lease assignment

ECQ comprises a ~20,000 sqm Outlet centre, ~10,000 sqm traditional shopping centre and ~11,000 sqm large format retail centre

Funded entirely from existing debt facilities, lifting gearing by c.200 basis points

Asset sits in Western Sydney's industrial and residential growth corridor with motorway, bus and heavy rail access

Strategic fit cited across two priorities: Upweighting metro Sydney exposure and strengthening the existing Outlet centre network, with development upside

Company page: Vicinity Centres (VCX)

Alkane Resources Q3: A record quarter across the board

[9:19 am] Alkane delivered record revenues, production and earnings in Q3 2026 with NPAT beating market expectations, supported by the Mandalay combination and stronger gold prices.

Revenue up 334% to $274.4m vs $275.8m ests (in line)

EBITDA up 474% to $161.2m

NPAT of $93.0m vs $85.7m ests (9% beat),

Gold equivalent production of 44,669oz and antimony production of 377t

Cash operating costs of A$2,037/oz gold equivalent, flat year-on-year,

FY26 guidance reaffirmed: Gold equivalent production of 155-168koz attributable and AISC of A$2,600-2,900/AuEq oz

Cash, bullion and listed investments of $374m

Company page: Alkane Resources (ALK)

Resolute Mining retracts ABC project scoping study

[9:14 am] Resolute Mining has withdrawn its ABC project scoping study after ASX flagged that the production targets and financials lacked a reasonable basis given full reliance on inferred resources.

Original study had touted NPV of US$1.2bn, a 12-year mine life, average production of 141kozpa, 39% IRR and 1.4-year payback

ASX advised the company it did not have a reasonable basis for the forward-looking statements due to 100% inferred resources underpinning the production targets

Published production targets and forecast financials deemed inconsistent with ASX Listing Rule 5.16 6

DFS completion was previously targeted for 2027, though timing now uncertain pending resolution

Company page: Resolute Mining (RSG)

Polynovo responds to ASX price query

[9:10 am] Polynovo received a speeding ticket at 3:57 pm on Thursday, with the ASX seeking answers to an abnormal volumes and price action. The company said it was not aware of any material non-public information.

Polynovo rallied 14.8% on 8.9 million volume (or ~354% higher than its daily average of ~1.9m).

Commodity prices slip

[9:10 am] A fairly weak overnight session for most commodities.

Commodity | % Chg | Price (US$) |

|---|---|---|

Lithium carbonate futs | -4.99% | 191,760 yuan |

Silver | -4.50% | $83.51 |

Palladium | -3.98% | $1,435 |

Platinum | -3.40% | $2,064 |

Nickel | -1.28% | $18,841 |

Gold | -0.85% | $4,649 |

Copper | -0.57% | $6.59 |

Aluminium | 0.27% | $3,647 |

Brent | 0.82% | $106.58 |

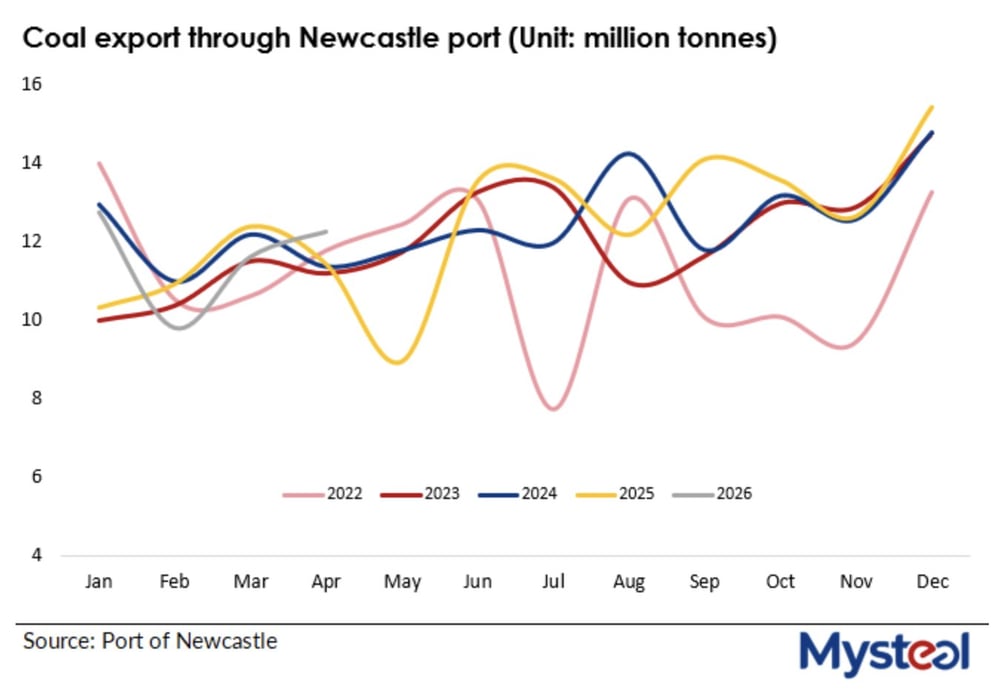

Newcastle coal exports hit five-year April high

[8:59 am] Newcastle port's April coal shipments surged on AEAN and Indian demand as the Iran war and Hormuz disruption force countries back to thermal coal to plug oil and gas shortfalls, according to Mysteel.

April coal exports up 7.3% year-on-year and 5.5% month-on-month to 12.24Mt, the highest April reading in five years

January-April cumulative throughput up 3% to 46.35Mt vs the same period last year

Exports to Malaysia up 58% year-on-year and 66% month-on-month to 615,628 tonnes as ASEAN nations including Thailand and Vietnam reactivate coal-fired generation

Steam coal shipments to India more than doubled month-on-month to 313,274 tonnes, with intense 40-45°C heat driving April power generation to a two-year high of 167.61bn kWh

Indian coal-fired generation up 2.6% year-on-year to 121.34bn kWh in April, with coal still ~70% of the country's power mix

Trump-Xi summit: Taiwan warning punctures cordial Beijing meeting

[8:54 am] Xi Jinping issued his most direct warning yet on Taiwan during Trump's first China visit, while the leaders discussed market access, energy purchases and Iran.

Xi told Trump mishandling Taiwan could push US-China relations into a "highly dangerous situation" with potential clashes

US readout omitted Taiwan entirely, instead highlighting expanded market access for US businesses and Xi's interest in buying more US energy and agriculture

Onshore yuan hit its strongest level since February 2023 (+0.1%) on reports of a potential $30bn trade deal

Leaders agreed Iran should not obtain nuclear weapons and discussed fentanyl precursor flows

Two more Xi-Trump meetings scheduled this year at APEC in Shenzhen (November) and G20 in Miami (December)

Source: Bloomberg

Boeing: China orders 200 jets in landmark return

[8:53 am] Boeing secured its first major China order in nearly a decade, though the 200-jet deal fell short of the 500 aircraft markets had hoped for.

Boeing shares fell as much as 5.4% to $227.50 on the disappointment

Order size missed upper expectations of 500 737 Max and widebody jets, Bloomberg Intelligence flagged the market was looking for 300+

China has only ordered 39 Boeing planes this decade, with Airbus securing ~700 orders from major Chinese carriers since July 2022

Deal still requires confirmation by an actual airline and past Chinese government plane agreements have not always been consummated (e.g. 2020 $77bn US goods pledge derailed by Covid)

Source: Bloomberg

Saudi crude output collapses to lowest since 1990 on Iran war

[8:52 am] Saudi production has fallen 42% since February as the Iran war chokes off Persian Gulf exports, with broader OPEC output dropping sharply.

Saudi output down 651,000 bpd in April to 6.316m bpd (lowest since Gulf War 1990)

Total OPEC output down 1.727m bpd to 18.98m bpd per secondary sources, with Saudis accounting for ~half the decline

Kuwait output roughly halved to 600,000 bpd, now pumping less than a quarter of prewar levels

OPEC trimmed 2026 global oil demand growth forecast to 1.2m bpd (from 1.4m), still well above IEA's forecast of a 420,000 bpd contraction (steepest since Covid)

Iran's Kharg Island jetties empty for fourth consecutive satellite snapshop

Source: Bloomberg

ECB: June rate hike less certain as inflation spillover stays contained

[8:50 am] A June ECB rate increase looks less obvious than two weeks ago as oil prices have not spiked as feared and the Eurozone economy stagnates.

Officials say the inflation outlook would need to deteriorate further to trigger action, vs. prior guidance that hikes would come unless conditions improved

Traders pricing three hikes starting in June, where Bloomberg-polled economists expect quarter-point moves in June and September

Medium and long-term inflation expectations remain anchored despite short-term survey pressure

Eurozone economy barely expanded in Q1 with subsequent services sector slump

Hawks (Nagel, Kocher, Kazimir) say only good news on Iran can avert a June hike, Schnabel says tightening only needed if energy shock "broadens"

Source: Bloomberg

Cerebras IPO: AI chipmaker doubles in blockbuster debut

[8:49 am] Cerebras Systems soared 68% on its Nasdaq debut, valuing the AI chipmaker at ~$95 billion in the largest US tech IPO since Uber in 2019.

Closed at $311.07 vs $185 IPO price (well above expected range), opened at $350 and peaked at $386

Revenue up 76% to $510m last year, with net income of $88m swinging from a $481.6m loss the prior year

Customer concentration risk remains, where G42 (Microsoft-backed UAE) was 24% of revenue last year (down from 85% in 2024), but Mohamed bin Zayed University of AI accounted for 62%

Signed a >US$20bn cloud deal with OpenAI in January expiring 2028, and AWS agreed in March to host Cerebras chips in its data centres

Signals potential wave of AI IPOs ahead with SpaceX, OpenAI and Anthropic potentially hitting markets

Source: CNBC

AI revival pushes S&P 500 above 7,500

[8:48 am] US stocks hit fresh records as renewed AI enthusiasm, strong Cisco results and resilient retail sales powered the rally despite war-driven energy cost pressures.

S&P 500 closed above 7,500 for the first time, with Nvidia's seven-day gain pushing its market cap close to $6tn and Cisco up 13% on a solid outlook

Q1 S&P 500 profits likely grew ~27% year-on-year per Bloomberg Intelligence, marking a sixth straight quarter of double-digit expansion and supporting the "wall of worry" bull case

April retail sales advanced for a third straight month with 9 of 13 categories posting increases, signalling consumer resilience despite soaring gas prices

Bitcoin topped US$80,000 after the Senate Banking Committee advanced a landmark US digital asset market structure bill

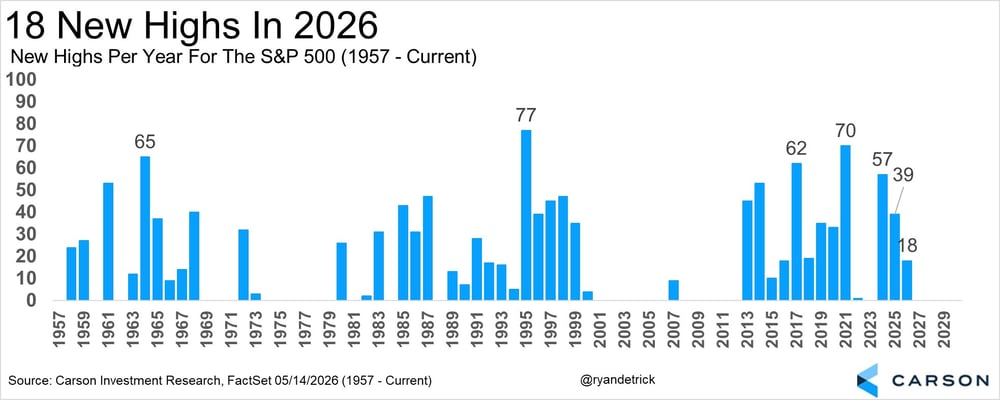

S&P 500 makes its 18th all-time high in 2026

[8:47 am] Pretty cool chart from Carson Investment Research. Since 1957, the S&P 500 has averaged 18.5 all-time highs a year, though the past decade has recorded a high volume of records.

US equities push higher on AI enthusiasm

[8:40 am] US stocks ended Thursday higher with the S&P and Nasdaq notching fresh all-time highs, led by AI-related names and strong Cisco earnings.

S&P 500 and Nasdaq set fresh all-time highs, finishing off best levels but on pace for solid weekly gains

Cisco a standout post-earnings gainer with order growth accelerating 17pp to ~35% and FY26 AI orders guided to $9bn (up from prior $5bn)

AI chipmaker Cerebras doubled in its trading debut from IPO pricing of $185 (already up from $150-160 range)

Nvidia received bullish updates on H200 AI chip sales to China though Chinese approval remains pending

April retail sales up 0.5% m/m (in-line with ests), decelerating from March's downwardly revised 1.6%

US import prices up 1.9% m/m vs 1.0% ests and export prices up 3.3% vs 1.1% ests, adding to the week's hotter inflation narrative

Market now pricing ~10bps of rate hikes through year-end

Good morning!

[8:34 am] ASX 200 futures are up 49 pts (+0.56%).

The overnight session in a nutshell:

S&P 500 closed above 7,500 for the first time ever (+0.77%), Dow reclaimed 50,000 and Nasdaq hit a record as the AI trade roared back on Cisco's blowout quarter and Cerebras' blockbuster IPO

Trump-Xi Beijing summit delivered a 200-jet Boeing order, US clearance for Nvidia H200 chip sales to 10 Chinese firms, and an agreement to (try) keep the Strait of Hormuz open

Resilient retail sales and yesterday's hot US PPI pushed the 10-year yield to a YTD high near 4.48%, with markets now fully pricing out a Fed rate cut this year as Warsh was confirmed as the next Fed chair