ASX 200 Live Today - Friday, 13th March

The S&P/ASX 200 is set to open lower as oil prices closed at the highest since August 2022. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Friday, March 13. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 back into positive territory

[1:45 pm] That's all for today. Things were looking rather grim, now ... ever so slightly less grim. The ASX 200 is currently up 0.13%, marking a decent bounce from session lows of -0.50%. The bulk of this reversal can be attributed to the banks, with the S&P/ASX 200 Financials Index up 1.28%. While the Big Four Banks opened around 0.5% higher, they're all up 1.0-1.5% at the time of writing. The Aussie 10-year has eased 6 bps to 4.93%, while WTI crude is currently trading flat at US$96.4 a barrel. Some calmness to close out the week is nice. Still lots of unanswered questions around energy and fertiliser flows, central bank outlooks and inflation impacts. I guess time will tell. Have a good weekend!

Lifestyle Communities rallies on block trade

[1:00 pm] Earlier this morning, the AFR speculated that land lease developer Hometown Australia was the buyer behind a 11.9 million share block trade in Lifestyle Communities. Done at $4.53, an 8% premium to its last close, the trade is the likely catalyst behind today's 14.5% rally.

Hometown Australia is owned by US prefab giant Hometown America, and the acquisition of a meaningful stake signals offshore interest in the Australian land lease sector

HMC Capital acquired its stake in November 2024 when Lifestyle Communities shares were down 26% and the company was under pressure following an ABC report criticising its deferred management fee model

The land lease sector is booming, housing more than 130,000 Australians with the $12 billion sector benefiting from an ageing population and acute housing shortage, attracting interest from majors including Stockland and Mirvac

Company page: Lifestyle Communities (LIC)

Energy stocks at April 2024 highs

[12:54 pm] Slowly but surely, the S&P/ASX 200 Energy Index has climbed 1.4% today and up 10.4% so far this month to a near one-year high.

As we noted earlier, Energy stocks tend to struggle for upside when oil prices experienced a rather unexpected spike. It's only in the aftermath, when prices show the ability to re-base at a higher level, do energy equities tend to re-rate.

Ticker | Company | % Chg | Price |

|---|---|---|---|

STO | Santos | 1.67% | $7.62 |

WDS | Woodside Energy Group | 1.51% | $31.52 |

BPT | Beach Energy | 1.47% | $1.17 |

ORG | Origin Energy | 0.13% | $11.61 |

KAR | Karoon Energy | -4.80% | $1.88 |

Lithium stocks edge higher

[12:51 pm] Lithium stocks have traded relatively flat over the past week despite broader market volatility. Chinese lithium futures are up 2.4% today to 160,000 yuan a tonne, still down ~15% from January highs but relatively flat this month.

Overall, resilient lithium prices have buoyed PLS shares 10% higher in the past month and up 15% year-to-date.

Ticker | Company | % Chg | Price |

|---|---|---|---|

LTR | Liontown | 4.32% | $1.69 |

IGO | IGO | 2.78% | $7.76 |

PLS | PLS Group | 2.41% | $4.90 |

MIN | Mineral Resources | 0.04% | $58.28 |

Tech stocks mixed

[12:49 pm] S&P/ASX 200 Tech Index up 0.19% after falling 7.7% in the last four sessions. Very mixed day, with Xero gains offsetting Wisetech declines at the index level.

Ticker | Company | % Chg | Price |

|---|---|---|---|

NXT | NextDC | 2.52% | $13.02 |

XRO | Xero | 1.78% | $79.88 |

TNE | Technology One | 0.49% | $26.54 |

CDA | Codan | -1.06% | $34.60 |

PME | Pro Medicus | -1.20% | $131.95 |

WTC | Wisetech Global | -2.01% | $47.00 |

360 | Life360 | -3.04% | $19.77 |

Analysts' take on Collins Foods

[11:40 am] Collins Foods' shares rallied as much as 13.2% on Thursday, but closed the session just 5.2% higher. The company announced the acquisition of eight KFC restaurants in Germany and reaffirmed its FY26 NPAT guidance. Here's what analysts are thinking:

Morgans upgraded to Buy from Accumulate, raised target from $12.40 to $12.70. Acquisition seen as disciplined and returns-focused, adding strategic credibility to the Germany story, with re-rating dependent on execution.

UBS maintained Buy, raised target from $13.10 to $13.50. Germany flagged as the standout region, with the acquisition adding scale and greenfield ambitions lifting medium-term upside, though delivery proof remains key.

A massive week for coal stocks

[11:34 am] The Iran conflict is pumping life back into coal stocks. Back in 2022, a name like Whitehaven Coal rallied ~250% between February and October.

Ticker | Company | 1-Week % Chg | Price |

|---|---|---|---|

TER | Terracom | 28.05% | $0.11 |

YAL | Yancoal Australia | 25.20% | $7.85 |

WHC | Whitehaven Coal | 11.26% | $9.39 |

NHC | New Hope Corporation | 8.47% | $5.38 |

SMR | Stanmore Resources | 2.11% | $2.90 |

CRN | Coronado Global | -3.71% | $0.34 |

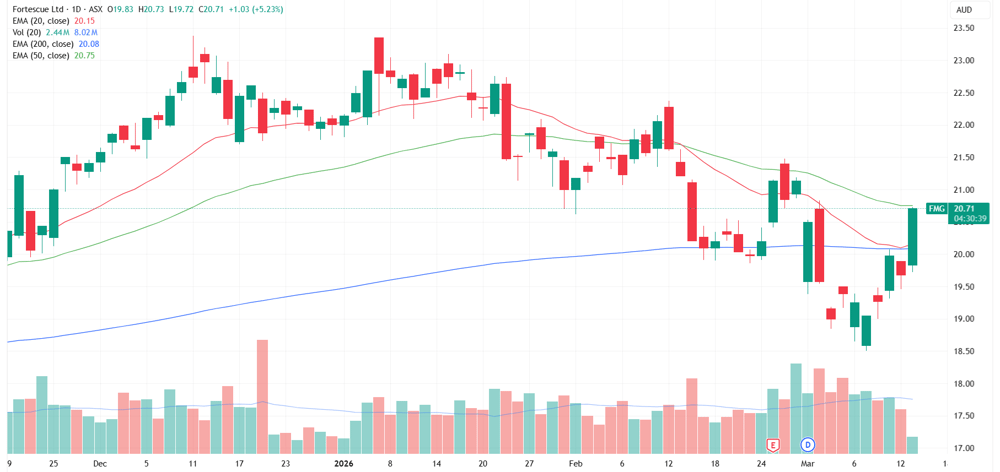

Fortescue eyes best day since April 2025

[11:32 am] Fortescue opened just 0.7% higher, now up 5.2% amid a sharp spike in Singapore iron ore futures overnight.

Fortescue daily price chart (Source: TradingView)

Middle East conflict disrupts iron ore shipments and tightens pellet supply

[11:28 am] Iron ore cargoes are being diverted mid-voyage as the Strait of Hormuz crisis scrambles commodity trade flows, with the pellet market facing a particularly acute squeeze, according to the AFR.

Benchmark iron ore futures surged more than 4% toward $110/tonne in Singapore, with elevated freight and bunker costs adding further pressure on shipment economics

At least three Anglo American cargoes and two Vale vessels originally bound for Middle Eastern ports have been diverted to destinations including Singapore, Vietnam, China and Malaysia

The disruption is hitting the iron ore pellet market hard, with Oman and Bahrain both key pellet producers and importers of pellet feed, and any sustained outage threatening to ripple quickly through the direct reduced iron sector

China has already lost approximately 10 million tonnes per year of iron ore pellets it was sourcing from Iran, and output from Bahrain and Oman is now also under threat, materially tightening global pellet supply

Source: AFR

Top ASX 200 gainers

[11:24 pm] Electro Optic Systems has topped the leaderboard after securing two new unconditional orders for counter-drone systems, with a total value of A$64 million. A few resource-related names spanning iron ore, coal, lithium and aluminium also notably higher.

Ticker | Company | % Chg | Price |

|---|---|---|---|

EOS | Electro Optic Systems | 7.26% | $10.64 |

FMG | Fortescue | 5.11% | $20.69 |

DBI | Dalrymple Bay Infrastructure | 5.05% | $4.89 |

AAI | Alcoa Corporation | 4.06% | $94.25 |

SMR | Stanmore Resources | 3.90% | $2.93 |

MFG | Magellan Financial Group | 3.68% | $10.15 |

NHF | NIB | 3.61% | $6.02 |

LTR | Liontown | 3.40% | $1.68 |

RYM | Ryman Healthcare | 3.28% | $1.89 |

VEA | Viva Energy Group | 3.14% | $2.14 |

Top ASX 200 losers

[11:24 pm] Northern Star trading sharply lower after downgrading its FY26 production guidance, while tech and growth names are also broadly 3-4% lower.

Ticker | Company | % Chg | Price |

|---|---|---|---|

NST | Northern Star Resources | -14.61% | $22.86 |

IPX | Iperionx | -9.56% | $5.54 |

OBM | Ora Banda Mining | -4.88% | $1.37 |

XYZ | Block | -4.19% | $85.31 |

GMD | Genesis Minerals | -4.05% | $6.39 |

AMC | Amcor | -3.92% | $57.25 |

360 | Life360 | -3.63% | $19.65 |

GYG | Guzman Y Gomez | -3.59% | $17.47 |

CAR | Car Group | -3.48% | $24.41 |

REG | Regis Healthcare | -3.41% | $6.24 |

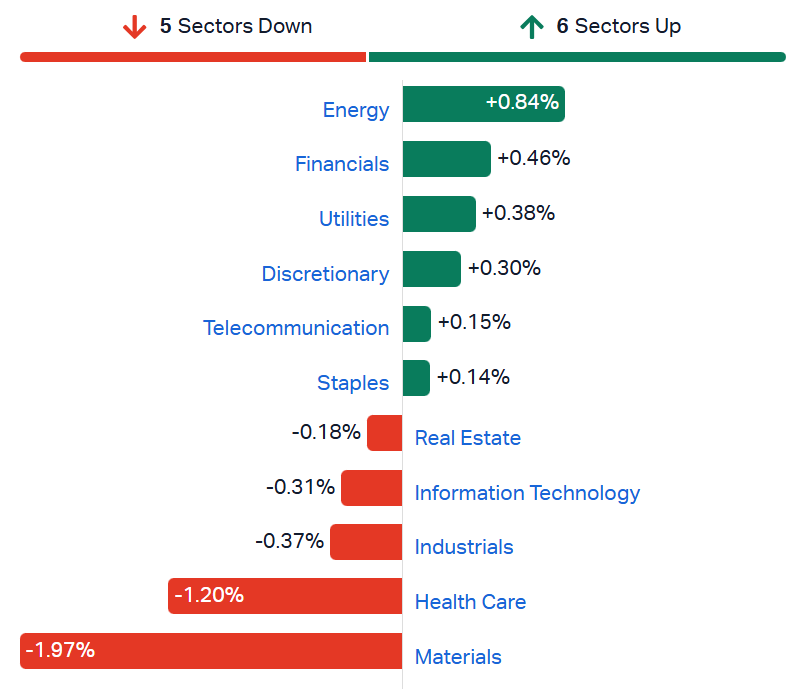

ASX 200 back near recent lows

[10:30 am] ASX 200 down 0.35% in early trade, back around Monday's lows (the day where the market tumbled 2.8%). Breadth is surprisingly ok, with an even split of constituents trading higher and lower. Pockets of strength from Energy, Banks and defensives like Utilities and Staples has offset weakness across miners and healthcare stocks. The Big Four Banks are all up around 0.5%, while the Energy Index is up 1.1% to the highest since April 2024. This has softened sizeable declines across miners, with BHP down 2.3% and Northern Star dipping 14% after an FY26 production downgrade.

ASX 200 sectors (Source: Market Index)

Immutep nosedives 90% after halting lung cancer trial

[10:20 am] An independent monitoring committee has recommended Immutep to discontinue its lead asset/flagship study evaluating eftilagimod alfa in first-line non-small cell lung cancer. The 95% dip is not a typo, with Immutep shares trading at 39.5 cents prior to the trading halt and opening 92% lower at 3.1 cents today.

The IDMC recommended discontinuation of the TACTI-004 Phase III trial following a planned interim futility analysis, concluding the study was unlikely to meet its endpoints based on available safety and efficacy data

Enrolment will be halted and the company will begin an orderly wind down of the study

Company page: Immutep (IMM)

Karoon Energy flags Brazilian export tax headwind

[10:12 am] Brazil has introduced a 12% levy on crude oil exports, directly impacting Karoon's operations in the country. Karoon shares dipped as much as 7.3% in early trade, now down 2.5%.

The tax is framed as windfall profit sharing given the current oil price environment and is effective immediately

It is expected to be deductible for corporate income tax purposes, partially offsetting the impact

The levy will lapse after 120 days unless ratified by Brazilian Congress, leaving some uncertainty around its permanence

Company page: Karoon Energy (KAR)

Collins Foods settles employee class action

[10:08 am] Collins Foods has reached a binding agreement to settle a class action over 10-minute rest breaks, with the company contributing up to $9m as part of a multi-party settlement.

The class action was commenced in December 2023 regarding rest break entitlements, with Collins Foods settling without any admission of liability

The $9m figure is subject to a cap and collar structure based on the number of group members who register to participate, meaning the final amount could be lower, or respondents could opt to terminate or make an additional payment if registrations exceed expectations

Settlement is still subject to Federal Court approval before it is formalised via a Settlement Deed

Company page: Collins Foods (CKF)

US ITC rules against Syrah in graphite dumping case

[10:05 am] The US International Trade Commission has made a final negative determination in the anti-dumping and countervailing duty investigation into Chinese active anode material imports, a significant setback for Syrah's Vidalia facility.

Syrah shares are down 18% in early trade.

The ITC's final negative determination means rates of 160-170% on Chinese AAM imports, as set by the US Department of Commerce, will not come into effect, reversing a preliminary affirmative finding from January 2025

The ruling is a material negative for Syrah's Vidalia AAM facility, with the company flagging it may delay AAM sales and limit near-term demand growth for domestically produced AAM and Balama natural graphite as feedstock

Syrah maintains its position that Chinese AAM is being sold into the US at unfairly low and subsidised prices, to the detriment of the domestic industry

The company will continue ramping up Vidalia and pursuing commercial AAM sales, with offtake agreements in place with Tesla and Lucid for the 11.25ktpa facility

Company page: Syrah Resources (SYR)

Northern Star cuts FY26 production guidance

[9:45 am] Northern Star has trimmed its FY26 gold production outlook, with mill throughput issues at KCGM and weaker mining productivity at Jundee weighing on near-term output.

FY26 gold production guidance cut to above 1.50Moz, down from prior guidance of 1.60-1.70Moz, a ~9% downgrade at the midpoint

March quarter-to-date sales affected by weaker milling performance at KCGM and reduced mining productivity, particularly at Jundee

Management has flagged that pushing hard to meet the revised FY26 target could compromise the transition to the new plant and negatively impact 1Q27

The KCGM Mill Expansion Project remains on track for commissioning early FY27, with open pit high-grade ore at KCGM averaging 1.6g/t over January and February

Guidance outcome remains particularly dependent on mill throughput at KCGM, with both downside and upside potential flagged

Not a good look for Northern Star, considering its bumpy production track record. In early January, the company's December quarter update downgraded FY26 production and increased cost guidance (shares dipped 8.4% on 22-Jan).

Company page: Northern Star Resources (NST)

US, Japan and EU set to form critical minerals trading bloc

[9:34 am] The US, Japan and EU are preparing to announce a trade framework for critical minerals that includes price floors and tariffs, aimed at countering China's dominance over global supply chains.

Negotiations led by the US are targeting an April start, with the EU-Japan-US framework expected to closely mirror the action plan already signed with Mexico in February

A key feature is a price floor mechanism to incentivise investment in non-Chinese supply and prevent Beijing from undercutting the bloc with cheaper exports

The move follows China's sweeping export controls on rare earths and critical minerals introduced last year in retaliation for Trump's Liberation Day tariffs, which imposed a 10% levy on nearly all US imports

While the supply crunch has eased from its peak last northern summer, companies continue to report receiving less than the quantities ordered from Chinese suppliers

Source: Bloomberg

Insider trades: Vulcan Steel

[9:31 am] Vulcan Steel CEO Gavin Street purchased ~8,000 shares, doubling his beneficial shareholding by 100% to ~16,000 shares.

Company page: Vulcan Steel (VSL)

Insider trades: AMA Group

[9:30 am] AMA Group chair Brian Austin purchased 1.5 million shares, increasing his beneficial shareholding by ~17% to 10.1 million shares.

Company page: AMA Group (AMA)

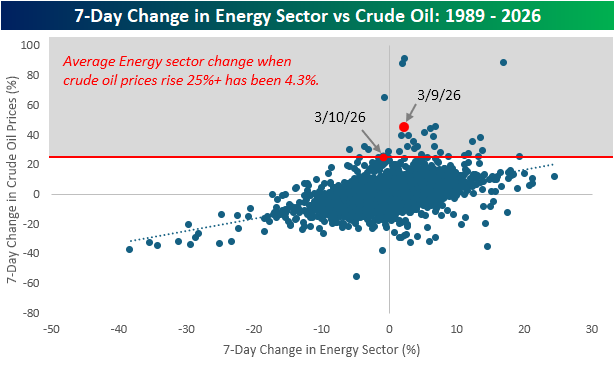

Energy stocks tend to struggle for upside

[9:28 am] Bespoke Investment Group notes the S&P 500 Energy sector has historically averaged a 4.3% gain when crude oil rallies at least 25% in a week.

Source: Bespoke Investment Group

The lack of energy sector upside amid surging oil prices may reflect:

Stock prices reflect discounted future cash flows across all future production, not just today's spot price. When markets are in deep backwardation (spot well above futures), only a small slice of output is realised at the elevated price

Producers cannot simply hedge all forward production to "lock in" high spot prices as posting margin on futures positions ties up significant collateral, and companies have been blown out historically when markets moved against their hedges

Production is inherently uncertain due to variable yields, operating conditions and credit availability, meaning there is embedded reflexivity that producers cannot or will not hedge away

Commodity stocks are still equities and move with broader equity risk premiums, and leverage means profits are also sensitive to borrowing costs that can spike in volatile environments

Business mix matters. Indian oil companies, for example, import crude and sell into price-capped domestic markets, meaning they can trade with a negative correlation to oil prices, while supply disruptions affect producers and refiners in entirely opposite ways

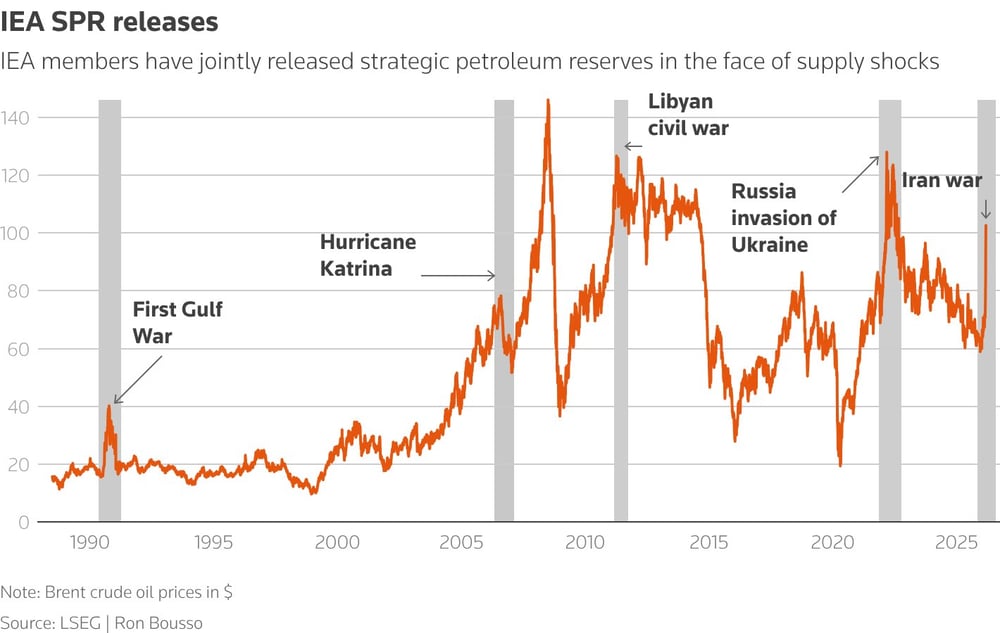

Historic IEA SPR releases

[9:22 am] Here's a chart from LSEG which outlines periods where IEA member states have released oil from their strategic reserves.

Source: LSEG

WTI rallies 9%, closes above US$95 for first time since August 2022

[9:10 am] Oil prices shrugged off any reprieve from SPR releases, closing the overnight session 9.0% to US$96.3 a barrel. This marks the highest close since August 2022. Prices continue to trend higher in the current session, up 1.10% in early trade to US$97.3.

WTI crude daily price chart (Source: TradingView)

EU warns inflation could top 3%

[9:05 am] The European Commission has flagged a significant inflation and growth risk for the bloc if elevated oil and gas prices persist, with Goldman Sachs modelling an even more severe scenario.

Under the EU's adverse scenario, with Brent around $100 and European gas prices at around €75/MWh, inflation could exceed 3% in 2026, some 0.7-1 percentage point above the prior forecast of 2.1%

Economic growth would also take a hit, with 2026 GDP potentially 0.4 percentage points lower than the previously forecast 1.4% pace

European gas prices have surged since the conflict began, trading around €52/MWh on Thursday after approaching €70 earlier in the week, with Brent near $100/barrel

IEA calls Iran conflict largest oil supply disruption in history

[9:03 am] The war is wiping out 7.5% of global oil supply, prompting an unprecedented emergency reserve release as markets reel from the near-total closure of the Strait of Hormuz.

The IEA estimates the conflict is slashing global oil supply by 8 million barrels per day this month, roughly 250 million barrels in total, with flows through the Strait of Hormuz down more than 90%

Gulf producers have been forced to collectively shutter around 10 million barrels of daily production as the strait closure blocks exports, eroding what was previously projected to be a record global supply glut

The IEA has cut its 2026 global demand growth forecast by roughly 25% to 640,000 barrels per day, the lowest since forecasts for the year were introduced, as price surges and economic uncertainty weigh on consumption

The projected 2026 global surplus has been trimmed by over a third to 2.4 million barrels per day, with risks skewed further to the downside given approximately 4 million barrels per day of regional refining capacity also under threat

Source: Bloomberg

US taps emergency oil reserve amid Iran war supply shock

[9:01 am] The Trump administration will release 172 million barrels from the Strategic Petroleum Reserve as part of a coordinated 400 million barrel IEA response to oil supply disruptions caused by the US-Iran war.

The 172 million barrel release will take ~120 days to fully deliver, though real-world SPR release capacity is likely limited to 1.4-2.1 million barrels/day, well below the theoretical maximum of 4.4 million barrels/day

The SPR currently holds ~415 million barrels (~60% capacity) after a series of Biden-era withdrawals, including a record 180 million barrel release following Russia's invasion of Ukraine in 2022

The administration says it has arranged to refill ~200 million barrels within the next year at no cost to taxpayers, likely via royalty-in-kind arrangements with domestic producers

Source: Bloomberg

Iran using Strait of Hormuz as diplomatic lever

[8:59 am] Tehran is granting shipping access through the strait to neutral countries while blocking those it considers aligned with the US and Israel, adding a new dimension to the global energy crisis.

Iran's deputy foreign minister confirmed select countries have been granted passage through the Strait of Hormuz, with access determined by whether a nation is seen as supporting the US-Israeli offensive

The strait has been effectively closed to commercial shipping since the conflict began on 28 February, with the disruption now in its 13th day and triggering a global energy crisis

Supreme Leader Mojtaba Khamenei is maintaining a hardline stance, calling for the strait to remain closed and demanding Gulf countries shut all US military bases on their soil

Middle East conflict escalates, threatening global oil supply

[8:57 am] Escalating attacks on oil infrastructure across the Persian Gulf are disrupting supply flows and driving crude prices sharply higher.

Brent crude surged as much as 10% on Thursday as tanker strikes, port evacuations, and the near-closure of the Strait of Hormuz deepened fears over regional supply disruption

Two tankers were struck in Iraqi territorial waters, prompting Iraq to suspend operations at its oil terminals.

Ships were evacuated from Oman's Mina Al Fahal terminal (exporting ~1 million barrels per day), with drones also striking fuel tanks at Salalah Port.

The near-closure of Hormuz has already forced Iraq, Kuwait, and Saudi Arabia to cut output, with some shipowners also avoiding Fujairah, one of the few remaining viable export points

Source: Bloomberg

S&P: AI won't trigger software credit downgrades

[8:56 am] S&P Global Ratings says AI disruption in software will be uneven and case-by-case, making a broad wave of credit rating downgrades unlikely.

S&P frames the current environment as "structural technological evolution" rather than a macro shock, meaning rating impacts will be more gradual than events like Covid-19

Companies with debt maturing in 2027-28 are most at risk if market volatility persists, potentially facing higher funding costs or reduced access to financing

Private credit has significant software exposure (~20% of borrowers), but credit quality has remained resilient to date. Though S&P cautioned this data reflects 2024 deals and 2025 trends may differ

Software firms with proprietary data and deep domain expertise are seen as most insulated, while commoditised, rule-based point-solutions face the greatest margin pressure and displacement risk

Downgrades for vulnerable issuers would likely be triggered by observable signs of competitive erosion and revenue decline, rather than pre-emptive action

Source: Bloomberg

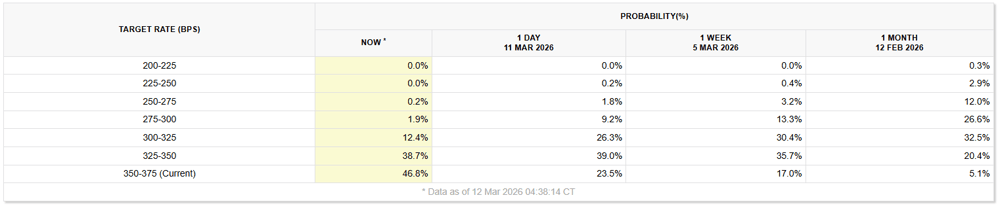

Goodbye Fed rate cuts

[8:56 am] Fed rate cut expectations have effectively vapourised in the last few days. The below table show's CME Fedwatch tool, which outlines the probability of where US interest rates will land by year end.

The base case is now a 46.8% likelihood of a hold. The likelihood of two 25 bp cuts has dipped from 30.4% a week ago and 26.3% yesterday to just 12.4% today.

Source: CME Fedwatch tool

US Treasuries rattled as oil surge revives inflation fears

[8:50 am] The Iran conflict has sent oil above US$100/barrel for the first time since 2022, triggering a sharp selloff in US Treasuries and pushing back rate cut expectations.

Two-year yields climbed as much as 10 basis points to 3.75%, briefly trading above the Fed's reserve balance rate and triggering stop-loss selling in crowded long positions

Goldman Sachs scrapped its June cut forecast and pushing expectations to September and December

Higher oil prices are stoking stagflation fears, with the Fed seen as unable to cut rates even if the economy slows, as inflation risks dominate the outlook

War financing requiring increased Treasury issuance, compounded by the Supreme Court's February ruling striking down tariffs that had been a revenue source

Source: Bloomberg

A heavy overnight session

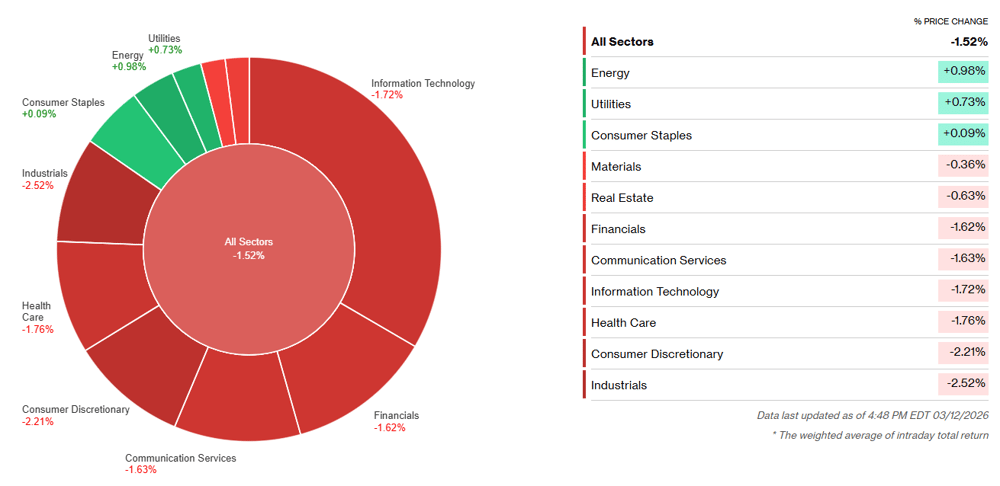

[8:48 am] A rather weak overnight session, where the S&P 500 opened 0.52% lower and finished the session down 1.52%, the lowest since November. While sectors like Energy, Utilities and Staples bucked the trend to finish higher, others like Tech, Healthcare, Discretionary and Industrials all tumbled more than 1%.

S&P 500 intraday chart (Source: TradingView)

S&P 500 sectors (Source: Bloomberg)

Good morning!

[8:30 am] ASX 200 futures are down 28 pts (-0.32%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks spent the session trending lower as oil prices continued to climb to levels not seen since August 2022

Iran hit vessels in Gulf waters, while new leader Mojtaba Khamenei reiterates plans to keep the Strait closed and use it as a weapon against enemies

Brent and WTI up 8-9% to close above US$100 and US$95 respectively, suggesting conflict is far from ending and driving hawkish outlooks/commentary from global central banks