Woolworths' shares surge on 1H26 earnings and dividend beat, sales gap with Coles narrows

Woolworths beat on every metric for the first-half of FY26, but at a trailing PE of 40x, the stock leaves little room for error.

Source: iStock

Mentioned

KEY POINTS

- Woolworths beat analyst estimates across every metric in H1 FY26, with underlying NPAT up 16.4% to $859m and the interim dividend lifted to 45 cents per share.

- Management upgraded its FY26 outlook, with Australian Food H2 sales tracking up 5.8% in the first seven weeks and EBIT growth now expected at the upper end of the mid-to-high single digit range.

- The stock trades at around 32x normalised earnings after an 18% year-to-date gain, raising the bar for further upside despite Morgans forecasting earnings growth of 13%, 14% and 9.6% across the next three financial years.

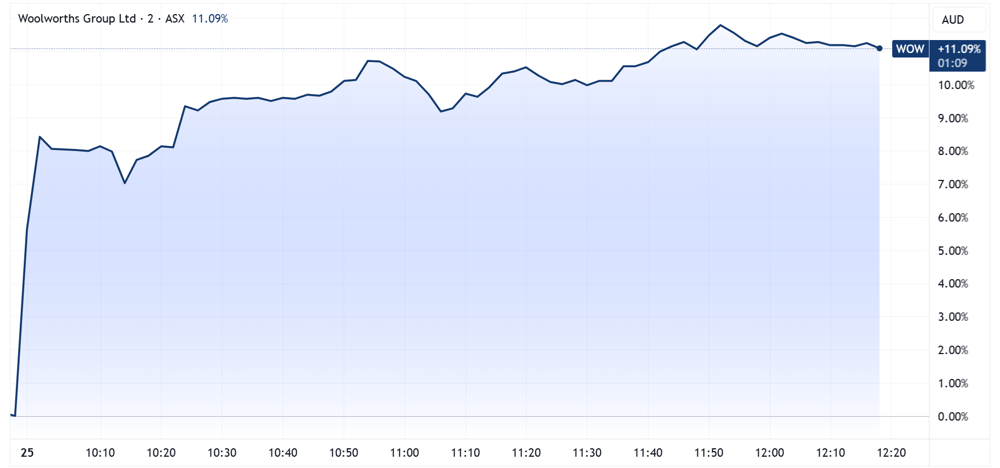

Woolworths (ASX: WOW) delivered a first-half result that beat analyst estimates across every key metric, and ongoing sales momentum gave management the confidence to upgrade FY26 guidance towards the upper end of its previous range. The stock is up 11.3% to $35.10, on track to close at its highest level since September 2024.

The result puts the company's turnaround narrative on firmer footing, though investors buying in today are doing so at a rather full valuation.

1H26 at a glance

Revenue up 3.4% to $37.14bn vs. $37.21bn ests (in-line)

EBIT up 14.4% to $1.66bn vs. $1.56bn ests (6% beat)

NPAT ex-items up 16.4% to $859m vs. $798.3m ests (8% beat)

Interim dividend up 15.4% to 45 cps vs. 43 cps ests (4.6% beat)

On a statutory basis, net profit after tax fell 49.4%, weighed down by $485 million in significant items relating to a provision for salaried team member remediation following a Federal Court ruling in early September.

Australian Food: The segment that matters most

The core Australian Food division grew sales 3.6% in the half, with food retail sales up 4.3% when stripping out the effects of prior-year industrial action and tobacco. Segment EBIT rose 9.9% with margins expanding 32 basis points, supported by eCommerce and the Media, Rewards and Services businesses.

Prior to the result, Morgans flagged Australian Food as the segment to watch, noting that Woolworths' sales growth of 2.1% in Q1 and around 3.2% in early Q2 still trailed Coles (up 4.8% in both periods). The expectation was that this gap would narrow as Woolworths cycled through the strike-related supply chain disruptions from November and December last year.

CEO Amanda Bardwell was measured but confident: "All customer metrics have improved, trading momentum is stronger and we are seeing market share stabilise ... As we look to H2, trading in Q3 to date has been strong in Australian Food, however, customers continue to be value-focused, shopping multiple retailers in a highly competitive environment."

Australian Food sales are tracking up 5.8% in the first seven weeks of the second half (7.2% ex-tobacco), and management now expects FY26 EBIT growth to land at the upper end of the mid-to-high single digit range, an upgrade on prior guidance. A strong outcome overall, with the beat and improving sales trajectory offering some vindication after a prolonged period of underperformance relative to Coles.

A strong result, rich valuation

Woolworths shares were up around 18% year-to-date heading into the result and now trade at a trailing price-to-earnings ratio of around 40x, or approximately 32x on a normalised basis. There's no denying that this is a rather full multiple for a supermarket.

That said, 2026 has seen a rotation into defensive parts of the market, with Staples the third best performing sector year-to-date at +8.0%, behind Energy (+13.4%) and Materials (+15.7%). This rotation has allowed valuations to run ahead of earnings, and the same dynamic is playing out on Wall Street, where Walmart has risen 12.4% year-to-date and trades at a trailing PE of 46x.

It was a clean beat across the board, with encouraging trading momentum heading into the second half, and management upgraded their guidance commentary towards the upper end of mid-to-high single digit EBIT growth. You can see the bullishness return for Woolworths, with the stock opening 4.6% higher ($31.54) and up 11.3% ($35.10) as at 12:30 pm AEDT – that's a lot of buying just two and a half hours in!

Woolworths intraday price chart (Source: TradingView)