Woolworths and Coles are surging. Here's what it means for the broader market

The ASX 200 staples sector is outperforming the broader market by a wide margin. History has a blunt warning for anyone tempted to chase it.

Source: iStock

Mentioned

KEY POINTS

- Staples surged almost 20% in seven weeks while the ASX 200 added just 2%. The spread sits in the 99th percentile, beaten only by the 2020 pandemic crash.

- This is a rare staples-led rally rather than a risk-off flight. Only five of the past 19 such episodes were driven by staples ripping higher in their own right.

- History says the trade mean reverts. After staples-led spikes the sector underperforms the broader market across most horizons, making it a historically poor entry point.

It's not often you see a slow-moving and defensive sector like staples rally almost 20% in just seven weeks. Over the same period, the S&P/ASX 200 has gained just 2%.

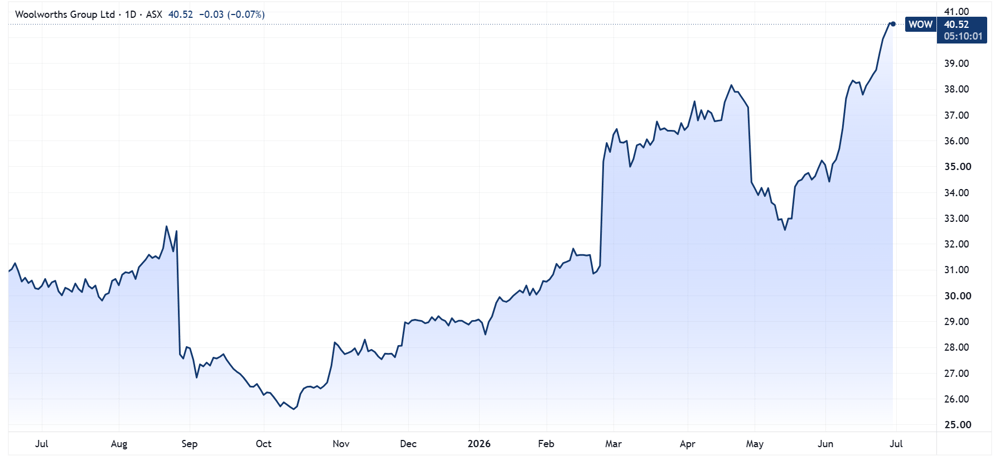

This pivot has brought heavyweights Woolworths to its highest since December 2021 and Coles to fresh all-time highs.

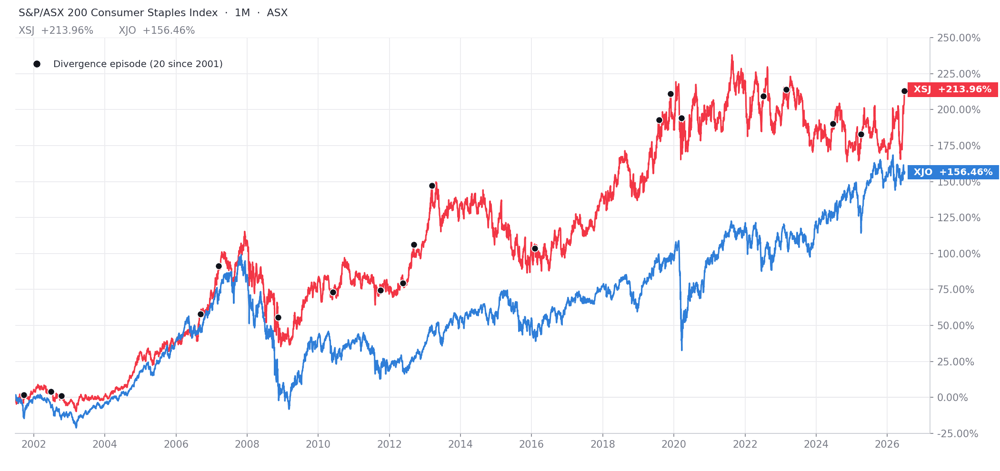

Now such outperformance isn't unusual and tends to happen roughly once a year. There have been 20 episodes of such wide outperformance since 2001, where the one-month spread between the two indices exceeded its 95th-percentile (5.8 percentage points).

S&P/ASX 200 (blue) vs. S&P/ASX 200 Staples index (red) | Source: TradingView

While the phenomenon is somewhat routine, the current scale is not. Today's strength sits around the 99th percentile of the data set, where only the pandemic crash was dramatically larger (~26 percentage points in March 2020).

Why it happens

The episodes split into two regimes:

Defensive or risk-off. This is when the broader market is falling and staples is simply holding up. These cluster on top of every major drawdown such as the 2008 GFC, 2020 pandemic, the 2011 Euro and US-downgrade crisis, 2016 China devaluation and oil rout, the 2002 dot-com trough, 2022-23 global rate hike cycle and the April 2025 tariff shock. Here, the spread widens as the index drops, not because staples rise. This is a rather textbook flight to earnings stability, and it reflects 14 of the past 19 episodes.

Staples-led. The market is flattish or up, and Staples rip higher in absolute terms. This reflects only 5 of the past 19 episodes, with prior examples taking place in September 2006, September 2012, March 2013 and twice in 2019. The recurring driver is a yield-and-rate driven defensive bid, along with sector-specific catalysts like M&A, regulatory relief and stronger-than-expected earnings.

What happens now?

Now despite this outperformance, history says the sector almost always mean reverts. On average, across the prior 19 episodes, the staples sector underperforms the broader market across every time horizon.

Whatever the trigger, if you join the Staples trade after such a spike, it has historically been a poor relative entry, and being on the short side has typically paid.

Taking a closer look, the path forward depends on which regime you're in.

After defensive episodes, the ASX 200 tends to rebound strongly, up 5.1% after three months and up 11.6% a year later. Meanwhile, the Staples index is down over the next 1-6 months, and up just 3.2% a year later (but positive just 50% of the time).

Source: Author's own calculations

After staples-led episodes, both the broader market and staples sector tend to trade lower over the next one and three months. The recurring theme is underperformance of the staples sector against the broader market, though by a slimmer margin, with a slight outperformance at the six-month mark.

Source: Author's own calculations

The bottom line

We're looking at a rare staples-led rally, powered by a recent bid for defensive and consumer-facing pockets of the market.

In the past month, three S&P/ASX 200 sectors have outperformed the rest by a wide margin: Staples (+13.9%), Healthcare (+13.5%) and Discretionary (+12.5%). This is against a backdrop where Australian consumer confidence recorded its largest monthly decline since the pandemic in April, to extremely pessimistic levels of 80.1. All three sectors have rallied off multi-year lows, where Staples was trading near a seven-year low, Healthcare near a nine-year low and Discretionary at a two-year low.

Back in February, Woolworths experienced its largest one-day rally on record, up 12.9% after reporting a better-than-expected 1H26 result and upgraded full-year outlook.

Revenue up 3.4% to $37.14bn vs. $37.21bn ests (in-line)

EBIT up 14.4% to $1.66bn vs. $1.56bn ests (6% beat)

NPAT ex-items up 16.4% to $859m vs. $798.3m ests (8% beat)

Interim dividend up 15.4% to 45 cps vs. 43 cps ests (4.6% beat)

FY26 EBIT growth now expected at the upper end of the mid-to-high single digit range, with Australian Food H2 sales tracking up 5.8% (7.2% ex-tobacco) in the first seven weeks

Fast forward to April, and Woolworths experienced a 7.7% tumble after tempering its full-year guidance at the Q3 update.

Woolworths price chart (Source: TradingView)

The announcement noted: "Reported FY26 Australian Food EBIT growth is still expected to be in the mid to high single digit range but no longer at the upper end of the range. This reflects incremental costs associated with direct fuel exposures in Q4 as well as investments to support customers in managing their budgets in a period of rising inflation including the Price Freeze announced today."

Since the Q3 update, Woolworths has rallied 18%, so it's interesting to see the stock re-rate so aggressively when the last catalyst was a negative one.