Why Flight Centre is rallying into an earnings downgrade

Flight Centre's update splits the room: A strong underlying business and FY27 tailwinds collide with an FY26 downgrade and Q4 leisure pain.

Source: Flight Centre

Mentioned

KEY POINTS

- FY26 underlying profit guidance cut to $275–295m, a 7% miss at midpoint, driven by a ~$50m Q4 leisure hit from Middle East cancellations, reroutes and deferred long-haul bookings.

- The underlying business is humming, growing underlying profit before tax (UPBT) nearly 10% over three quarters and accelerating to ~20% in Q3, with corporate buoyed by the new Blockskye US partnership.

- A new up-to-$200m buyback signals management sees value with shares down 65% from pre-pandemic levels; the Middle East peace deal is flagged as a key FY27 tailwind.

Flight Centre's (FLT) trading update had something for everyone. For bulls, it was the Middle East peace deal that'll bolster earnings from FY27, a new on-market buyback and still-solid fundamentals for the first three quarters of the year. For bears, it was the immediate reality of an FY26 earnings downgrade and a notable hit to the leisure segment driven by cancellations, re-routes and deferred bookings.

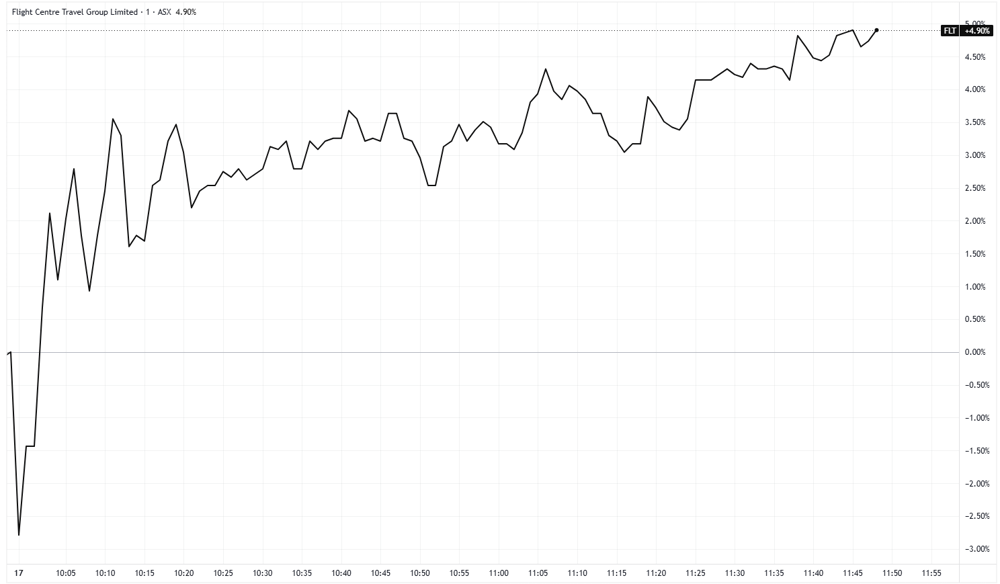

Early price action had something for everyone too, opening 2.8% lower, but V-shaped into positive territory, now up 5%.

Intraday chart for Flight Centre (Source: TradingView)

The $200 million share buyback Flight Centre flagged in its announcement could also be another positive catalyst. The stock is down 17% year-to-date and 65% from its pre-pandemic levels. At those prices, management clearly see the stock as relatively undervalued and an efficient way to use excess cash.

FY26 guidance takeaways

FY26 underlying profit before tax (UPBT) is now expected at $275-295m vs $307.7m ests (7% miss at midpoint)

Q4 leisure earnings to be circa $50m below prior expectations, with a further $5m hit to UK touring businesses and $5m-10m of adverse foreign exchange from a stronger AUD

Underlying business grew UPBT almost 10% to $227m in the first three quarters of FY26, accelerating to ~20% growth in Q3, with leisure tracking towards a $200m UPBT milestone before the Q4 disruption

Corporate business less affected and on track to deliver strong FY26 profit growth, supported by the new Blockskye US partnership and an accelerating contract win pipeline

Q4 leisure hit driven by cancellations and reroutes on UK/Europe bookings via the Middle East, plus deferred long-haul bookings as airfares spiked; Flight Centre brand Australia enquiry still up 18% month-to-date

New up-to-$200m on-market buyback follows May 2026's program that retired 16.2m shares (7.3% of issued capital), with the Middle East peace deal seen as a significant FY27 earnings tailwind

Putting it all together

In a May 14 note, Macquarie had an Outperform rating on Flight Centre, with a $15.54 target price. The analysts argued the company "has experience navigating market dislocations and is well positioned to deliver strong growth when conditions normalise," adding that "at these levels valuation remains attractive."

And things were going well for Flight Centre until the March quarter, where the Middle East conflict derailed its momentum. Underlying business profit rose 10% over the first three quarters of FY26, with the pace of growth picking up to 20% by the third quarter, and the leisure division in particular was on track to hit a profit milestone before the Middle East conflict hit in Q4.

Now peace is tantalisingly close, Flight Centre sees a "clearer runway into FY27 and a significant earnings tailwind," even as it concedes the timing is too late to rescue FY26. While today's rally into a earnings downgrade may be confusing, the market is clearly looking through FY26, and upbeat for what's in store for FY27.