Why CSL is rallying like a growth stock again

CSL is up 35.5% since early June, clearing its 50-day moving average for the first time in nearly a year. Is the biotech giant back?

Source: Shutterstock

Mentioned

KEY POINTS

- CSL has rallied 35.5% since 3 June, recouping all losses from its 11 May earnings downgrade and meaningfully clearing its 50-day moving average for the first time since August 2025.

- Little has changed fundamentally. Brokers remain largely neutral, with Tavneos facing EU and US withdrawal but representing only around 1% of group revenue.

- Macquarie models benign growth through FY28, valuing CSL near 19.5x FY26 estimates. A low bar that even modest beats could reward.

When was the last time you heard of CSL (CSL) rallying more than 35% in a month? You'd probably have to cast your mind back to 2022–23, when the biotech giant still had something going for it.

For almost two years, CSL has been in an aggressive downtrend, with a handful of 10–15% bounces along the way, before another earnings downgrade drives another leg down to yet another fresh multi-year low.

But the past month has marked a genuine change of character, with the share price up 35.5% since 3 June. The strength has been so pronounced that the stock cleared its 50-day moving average for the first time since August 2025, and recouped all the losses from the latest earnings downgrade, when it tumbled 15.9% on 11 May.

A quiet two months

Not a whole lot has happened since CSL's latest downgrade on 11 May, which noted:

FY26 revenue guided to ~$15.2bn vs. $15.79bn ests (4% miss)

FY26 NPATA guided to ~$3.1bn vs. $3.34bn ests (7% miss)

Expects to recognise ~$5bn of non-cash, pre-tax impairments across FY26 and FY27 in addition to those announced at the first half result, including CSL Vifor intangibles and under-utilised property, plant and equipment

The only market sensitive news affecting the business relates to Tavneos, a treatment for a rare autoimmune condition that inflames small blood vessels. The CHMP recommended revoking its European marketing authorisation, following April news that the FDA is weighing a US withdrawal. Both cite data handling concerns in the pivotal Phase 3 trial, plus reports of liver damage in the US and Japan that have proven fatal in some cases. This product represents 6–7% of CSL's Vifor revenue and approximately 1% of group revenues.

The latest broker research also remains relatively neutral.

UBS (1-Jul): Retains Buy with a $158 target, arguing weaker Vifor forecasts (generics, Velphoro TDAPA expiry, potential Tavneos withdrawal) are largely priced in, but warns the upcoming result is unlikely to show improved competitive conditions or progress on a new CEO, and flags June's broad-based health rally looked driven by year-end rotation and the US biotech move rather than news

Citi (30-Jun): Stays Neutral with a $110 target, noting CHMP's 26 June recommendation to revoke Tavneos' EU authorisation, having already cut Tavneos estimates to sub US$10m a year from a peak forecast of ~US$170m, though it sees the drug as just 1.1% of FY26 revenue and the timing unhelpful as larger global therapeutics names attract buying

Macquarie (29-Jun): Maintains Neutral, lifting its target to $114 from $111 as EPS cuts of 0%/3%/4% across FY26 to FY28 are offset by a lower AUD/USD, and models a ~65% FY27 Tavneos revenue drop with no new EU patients, plus a Vifor gross margin easing to ~62.5% from FY27

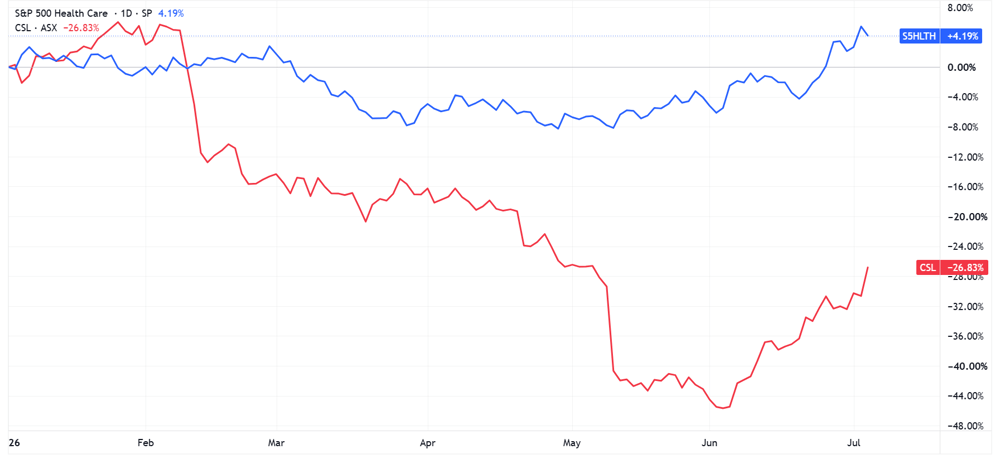

Since CSL bottomed on 3 June, the S&P 500 Healthcare sector has rallied 10.2% to fresh all-time highs.

S&P 500 Healthcare Index (blue) vs. CSL (red) | Source: TradingView

A low bar

Macquarie's 29 June modelling sees relatively benign growth over the next few years, including:

2026e | 2027e | 2028e | |

|---|---|---|---|

Revenue (US$m) | 14,907 | 15,000 | 15,449 |

Revenue growth (%) | 0.6 | 0.6 | 3.0 |

EBITDA (US$m) | 5,156 | 5,098 | 5,218 |

EBITDA growth (%) | 0.3 | (1.1) | 2.4 |

EPS (adj US cps) | 639.3 | 663.2 | 689.5 |

EPS growth (%) | (3.9%) | 3.7 | 4.0 |

Source: Macquarie Research June 2026

This values CSL at around 13.5x FY26 estimates. There's no point saying this is cheap relative to historical levels of 35–40x, when CSL had much higher and consistent growth rates. But given how battered it's become, even just meeting these expectations, or slightly exceeding them, could warrant some further upside.

For now, CSL is enjoying a comeback bounce against a backdrop of strong gains for the US healthcare sector, and momentum that's building on itself, as the share price begins to cross key moving averages.