Think the cost of living crisis is bad? Markets now tip three more rate hikes

Oil shocks are stoking inflation fears and markets now expect three more rate hikes, suggesting the cost of living crisis is far from over.

Source: Market Index using ChatGPT

KEY POINTS

- Escalating tensions in the Middle East have pushed oil prices sharply higher, reviving inflation risks just as central banks thought the worst was behind them.

- ASX cash rate futures now imply up to three additional RBA rate hikes by early 2027 — a dramatic shift that has accelerated sharply in recent weeks.

- Higher rates threaten a dangerous squeeze on households and businesses, raising the risks to the economy and housing market. We investigate the latest market view on rates and the potential impacts.

Just as it seemed the inflation battle was turning, global events have intervened. The escalation of conflict in the Middle East has sent oil prices surging — a classic supply shock that flows quickly into fuel, transport, and food costs. It’s exactly the kind of development central banks fear most: inflation rising for reasons they can’t control.

For our own Reserve Bank of Australia (“RBA”), the mandate is clear: keep inflation in check even if it comes at a cost to growth. This helps explain the RBA’s recent actions. The cash rate has already been lifted twice in quick succession, and the tone from policymakers has remained firmly hawkish.

Back in January, I flagged that markets had swung from expecting rate cuts to pricing rate hikes. Here we are, two months and two hikes later. But the bigger story is what’s going to happen next.

This article aims to alert investors to the latest move in market interest rates pricing — and the sharp escalation in just the last trading session that suggests more pain may be on the way.

Markets now see three more hikes ⬆️ + ⬆️ + ⬆️

To understand where interest rates may be headed, investors should look to the ASX 30 Day Interbank Cash Rate Futures market. These contracts represent where large, sophisticated market participants — banks, hedge funds, and asset managers — believe the RBA’s official cash rate is headed over time.

Right now, they’re sending a clear and troubling signal. For the first time since rates “lifted off” from near-zero levels following the COVID-19 pandemic, the futures curve is now implying three additional rate hikes — expected to occur by around March 2027.

That’s a major shift in market thinking.

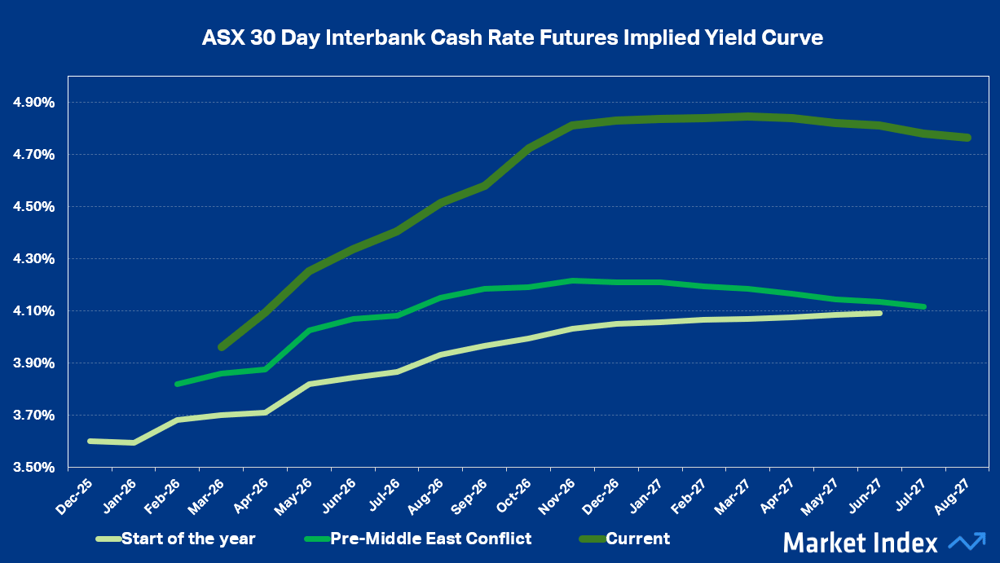

ASX 30 Day Interbank Cash Rate Futures over various lookback periods since January 1

The latest cash rate futures curve shows a sharp upward repricing since the start of the year, but more notably, a massive uptick in interest rate expectations in the wake of the Middle East conflict.

At the start of the year, the RBA’s cash rate stood at 3.35% p.a., with the market forecasting a total of three 0.25% p.a. hikes by the middle of next year. This was largely unchanged after February’s 0.25% p.a. increase.

However, following the US-Israel attacks on Iran on February 28, the curve has jolted sharply higher, peaking on Friday at 4.85% p.a. by March 2027. That’s 1.25% p.a. higher than the 3.60% low of the last cutting cycle, and 0.75% p.a. higher than the present 4.10% p.a. rate.

For Australian households, this escalation in market interest rate expectations comes at a precarious time. This is because market pricing inevitably flows through to key borrowing rates for homeowners, businesses, and investors. The latest developments in the cash rate futures curve suggests each group can expect substantially higher interest costs in the near term.

But for households — who have taken on record levels of debt — the ramifications could be dire. Cost of living pressures are already acute, and many budgets are stretched to breaking point. The idea that rates could rise further — and materially so — paints a disturbing picture.

What three more hikes really means

Three additional 25 basis point hikes may not sound like much in isolation. But for a typical Australian mortgage holder, they add up quickly. Higher interest rates feed directly into mortgage repayments, increasing the monthly burden on already stretched households. At the same time, those same rate hikes ripple through the broader economy.

Higher bond yields encourage saving versus spending

Business borrowing costs rise

Investment slows

Consumer spending weakens

These impacts are not coincidences — they’re exactly what the RBA is hoping to achieve from tighter monetary policy. The RBA expects the combination of the above outcomes will reduce excess demand in the economy, and put downward pressure on inflation.

While tightening cycles generally work by design — they don't transpire without consequence. As households cut discretionary spending, businesses begin to feel the pinch. Revenues soften. Margins come under pressure from higher input costs. Hiring slows — and in some cases, reverses.

Any deterioration in the labour market would place further pressure on highly leveraged households and could become the pin that pops Australia’s housing market bubble. It could be a slippery slide from that point into a recession.

Lessons from the past

Australia has faced this kind of dynamic before. The early 1990s recession and the Global Financial Crisis were very different in origin — but they share some important parallels:

Rising interest rates into economic weakness

Sharp deterioration in labour market conditions

Pressure on highly leveraged households and asset prices

In both cases, the transmission mechanism was similar: tighter financial conditions led to weaker spending, which fed into rising unemployment and broader economic stress.

Today, the starting point is arguably more fragile: household debt is higher, housing is more central to the economy, and arguably, the margin for error is thinner.

Stay alert (and beginning to be a little alarmed! ⚠️)

None of this is inevitable. If oil prices stabilise or fall, inflation pressures may ease, and the RBA could avoid further tightening. Markets, as always, will adjust to reflect these positives.

But right now, the direction of travel is clear — and it’s not comforting. The implication of current market pricing is that the cost of living crisis may not just persist — it may intensify.

For investors and homeowners alike, this is not a time for complacency. Understanding how interest rates flow through to mortgages, spending, employment, and asset prices is critical. Because if the market is right — the next phase of this cycle could be the most challenging yet.