Goodbye RBA rate cuts — hello two rate hikes, starting in May!

Mortgage holders beware: markets now price rate hikes, not cuts. Strong jobs and sticky inflation have the RBA cornered again.

Source: Shutterstock

KEY POINTS

- Falling rate expectations have helped fuel soaring house prices, with markets convinced in 2025 that the RBA would deliver further mortgage relief through rate cuts.

- That confidence has evaporated. Hot inflation and a red-hot jobs market have pushed rate-cut hopes aside, lifted bond yields, and dragged rate hikes firmly back into the picture.

- This article breaks down what changed, why inflation is still sticky, how markets are reading the signals — and what it means for mortgages, portfolios, and the outlook for monetary policy.

Just a few months ago, the debate around Australian monetary policy revolved around how many rate cuts the Reserve Bank of Australia (RBA) might still deliver this cycle. Then, in late October, a shock September-quarter inflation print killed rate-cut hopes outright, forcing markets into an uneasy holding pattern. Yesterday’s employment data has now shattered that pause.

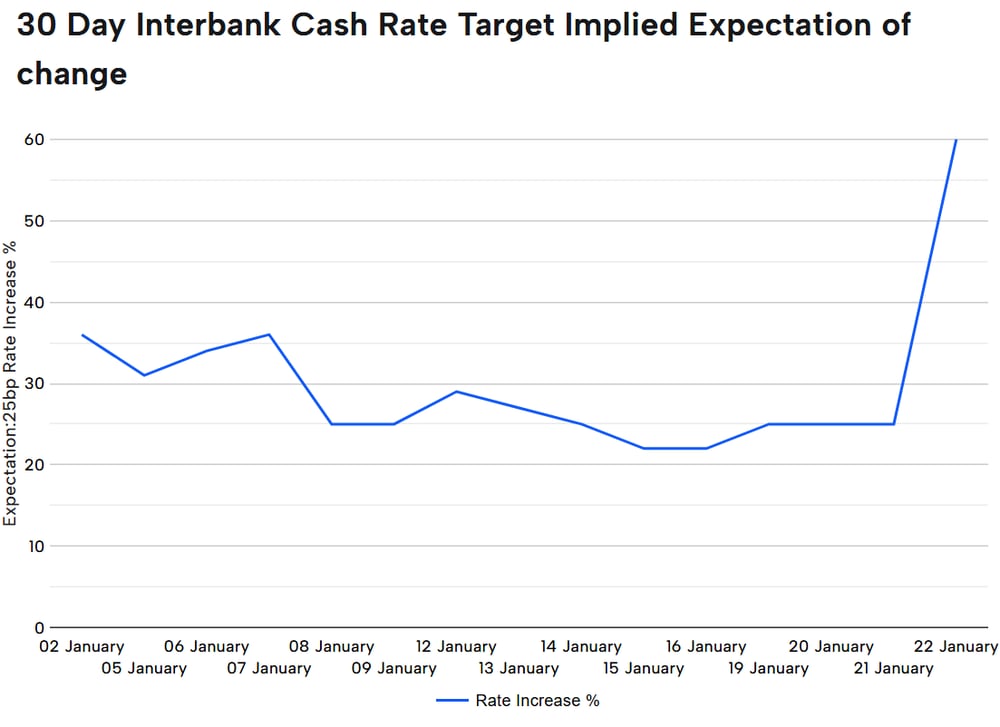

Markets are no longer asking if the next move in official interest rates is up, but when. In the space of just 24 hours, futures pricing moved roughly 6.5 basis points higher, with markets now assigning a 100% probability of a 25bp rate hike by May this year, and a second hike priced in by May 2027. That is a remarkable turnaround - and one that underscores just how uncomfortable the RBA’s policy position has become.

30 Day Interbank Cash Rate Target Implied Expectation of change. Source: ASX

This is a follow-up to my Kiss Your Rate Cuts Goodbye piece late last year, which documented the initial shift away from cuts. Here, I update what has changed since, explain why inflation is proving more stubborn than the RBA would like, and unpack why the central bank increasingly looks boxed in by the data.

Good news: Employment is strong. Bad news: Employment is strong!

The December labour force report was, by any reasonable standard, a blow-out. Employment surged by 65,200, overwhelmingly driven by full-time jobs, while the unemployment rate fell to 4.1%, its lowest level since May last year. Underemployment dropped sharply, hours worked rose, and the underutilisation rate slid below 10%.

Fantastic. Right? If you’ve got a job, you can pay the bills, keep up with the mortgage or rent, and feel a bit more confident about spending. That’s good news for households and the broader economy.

But it also creates a major issue for any homeowner with a mortgage or business with a loan. In short: this was not the kind of labour market data consistent with an economy that needs easier policy.

In a research note released after the data, RBC was blunt. “The picture we are left with here is not consistent with the RBA’s base case,” the bank wrote, adding that the labour market looks “tight here, likely sub-NAIRU,” and warning the data “adds further risk that the RBA will be forced into a fresh hiking cycle.” [1]

That warning matters because the RBA’s current forecasts assume unemployment drifts higher toward the mid-4% range. Instead, the labour market just moved in the opposite direction - and did so decisively.

Importantly, this strength is not being driven by a collapse in participation or a statistical quirk. Youth employment rose, underemployment fell, and the hours worked data confirmed that labour demand remains firm. As RBC noted, this is occurring “against a backdrop of ongoing capacity constraints across the supply side of the economy.”

“Capacity constraints”. Two words no central banker likes to hear. This is because it is precisely in such an environment that inflation risks emerge, or in this case, re-emerge.

Sticky inflation: why progress is slowing, not accelerating

Inflation is no longer surging — but it is also not retreating as cleanly as policymakers would like. Services inflation remains elevated and labour costs are still running too hot relative to productivity.

Morgan Stanley captures the tension well in its latest research note on the Australian economy, warning “there is little wiggle room in the RBA’s labour market forecasts if domestic momentum does slow.” Put simply, the RBA is already counting on a weaker jobs market — and if that doesn’t materialise, policy quickly looks too loose. [2]

The structural problem remains productivity. When businesses can’t easily find workers or lift output, higher costs tend to be passed on through prices — particularly in services.

AMP’s chief economist Diana Mousina puts it plainly in her latest update: “Services inflation has been broadly surprisingly sticky in the post-COVID world which probably reflects tight labour markets.” She adds that even with wages moderating, “business labour costs remain elevated” once weak productivity is taken into account. [3]

This helps explain why inflation progress feels incremental rather than decisive — and why the RBA cannot declare victory.

The OCR futures curve: markets expect rate hikes

The clearest signal of this shift is coming from the rates market.

For readers less familiar with futures pricing, the OCR futures curve represents where traders expect the RBA’s cash rate to sit at various points in the future. When the curve shifts higher, it reflects growing confidence that rates will stay elevated — or rise — rather than fall.

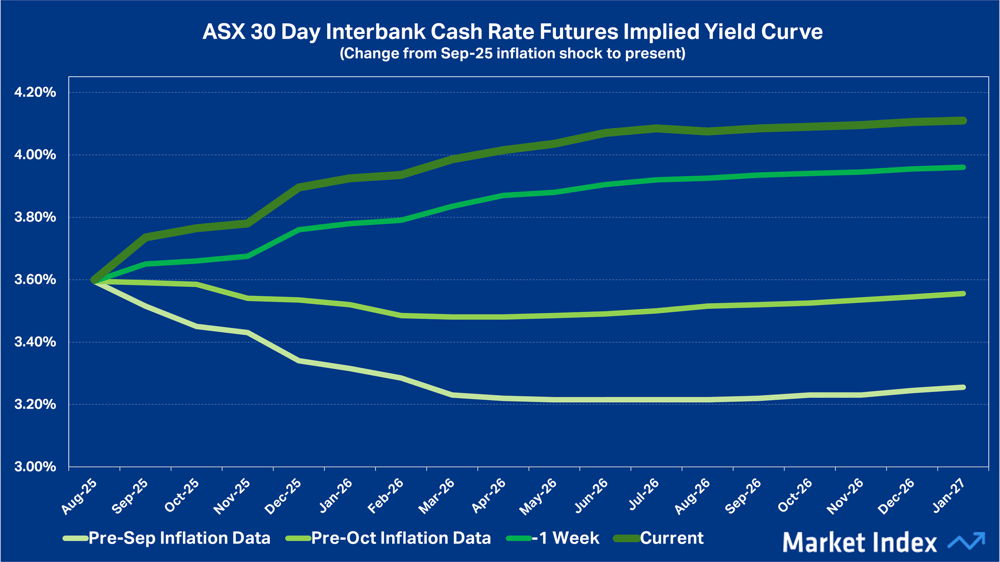

ASX 30 Day Interbank Cash Rate Futures Implied Yield Curve, Aug-25 to 22-Jan 2026

Since the September-quarter inflation shock in late October, the cash-rate futures curve has shifted both higher and steeper. Before that print, the curve sloped downward, reflecting expectations that the RBA would begin cutting rates through 2026.

After the inflation data, that downward slope flattened — and then began to tilt upward. In simple terms, markets stopped expecting cuts, moved to an “on hold” view, and then progressively priced in higher interest rates as fresh data reinforced the inflation risk. Each subsequent data point — most recently the employment report — has nudged the entire curve higher, lifting expected cash rates across nearly every future meeting.

What matters most is where the curve now sits and how it rises over time. By May this year, markets are pricing a full 25 basis-point rate hike. Further out, the curve continues to climb, implying another hike by May 2027. That upward slope tells a clear story: markets are pricing a world where rates stay higher for longer as inflation pressures prove more persistent than hoped.

For households and businesses, this matters because interest rates don’t wait for an RBA decision. When markets start pricing in higher rates, borrowing costs move higher straight away — mortgages, business loans, and funding costs all adjust in anticipation. The OCR futures curve is simply a snapshot of those expectations. In effect, financial conditions have tightened - without the RBA lifting a finger.

How investors can position themselves for higher interest rates

For investors, this tug-of-war between slowing growth and stubborn inflation matters far more than the academic debate around forecasts.

On one hand, the economy is not overheating in the classic sense. Household spending is uneven, insolvencies remain elevated, and sentiment is fragile. Morgan Stanley still expects unemployment to drift higher over time and inflation to ease gradually through 2026.

On the other hand, the labour market is telling a different story — one of persistent tightness, limited slack, and ongoing wage pressure in a low-productivity environment.

That leaves the RBA facing an unenviable choice:

Move too early, and risk choking off a private-sector recovery that has only just stabilised; or

Move too late, and risk entrenching inflation expectations that force more aggressive tightening later.

AMP warns that a “knee-jerk reaction” to higher inflation or strong data risks damaging the private sector but also acknowledges that financial conditions have already tightened materially through the transmission mechanisms we’ve discussed today — market expectations and the yield curve.

This is not a comfortable place for a central bank to be. The key takeaway is not that rate hikes are guaranteed, it’s that the balance of risks has flipped. Cuts are no longer the base case. Inflation is no longer fading cleanly. And the labour market is no longer cooperating.

For investors, this has several implications:

Bond yields are unlikely to fall meaningfully unless labour data softens decisively.

Rate-sensitive equities like financials, real estate, utilities and infrastructure, and consumer spending-linked sectors face ongoing headwinds.

Inflation-resilient assets, particularly those with pricing power like resources, will likely continue to hold investors’ attention.

Most importantly, policy uncertainty itself has become a macro factor. The journey from “how many cuts” to “how many hikes” has been rapid — and it isn’t finished. But if there is one certainty left in this cycle, it is this: no one would envy Michele Bullock’s job right now.

References

[1] RBC Capital Markets —RBC AU Rates Strategy: Dec labour force – wow, 22 January 2026.

[2] Morgan Stanley — Australia Macro+: State of Play, Key Debates and Positioning Ideas, 14 January 2025.

[3] Diana Mousina, Deputy Chief Economist, AMP — Econoinsights with Diana Mousina: 2026 “Wi$h LiSt”, 9 January 2025.