The verdict is in! The big brokers think CSL is a buy after its FY24 results

CSL's results weren’t cheered if the drop in its shares is anything to go by. The dust has settled, what do the brokers think about it now?

Source: Shutterstock, Market Index

Mentioned

KEY POINTS

- CSL is a world leader in blood plasma products and vaccines, it’s widely recognised as quality growth story by many of the major brokers

- Shares fell sharply, though, after the release of its FY24 results but they had been rising steadily before

- Given the mixed share price response, do the big brokers think CSL is a buy, hold, or sell after its results? We have the low down!

Results overview:

Key metrics / Highlights (all figures in $US)

Revenue $14.74 billion, +11% vs consensus $14.65 billion

Behring $10.61 billion vs consensus $10.47 billion

Seqirus $2.13 billion vs consensus $2.07 billion

Vifor $2.06 billion vs consensus $2.09 billion

EBIT $4.28 billion vs consensus $4.26 billion

Behring $4.37 billion vs consensus $4.47 billion

Seqirus $1.12 billion vs consensus $1.09 billion

Vifor $956 million vs consensus $894.6 million

Final dividend of $1.45 per share (0% franked)

(*consensus estimates via StreetAccount by Factset)

Outlook

Net profit guidance (in constant currency terms “CC”) $3.2-$3.3 billion vs consensus $3.38 billion

Revenue growth guidance in CC +5-7%

Behring (immunology, hematology, cardiovascular and metabolic, respiratory, and transplant therapeutics)

Company expects continued strong performance to be driven by immunoglobulin demand, operational efficiency gains

Significant growth potential seen in HEMGENIX and Garadacimab products

Seqirus (vaccines including flu, COVID-19, antivenoms and Q fever)

Company acknowledges there market challenges remain, but that its highly differentiated portfolio positions it for outperformance

Vifor (iron deficiency and iron deficiency anaemia therapies)

Company notes increased competition, but continues to maintain long-term strategic focus

Broker response

Citi

Rating: BUY | Price target: $345.00⬆️ vs $335.00

Views:

FY24 net profit was a slight miss, but FY25 guidance missed by around 5.5% mainly due a lower than expected profit margin and slower Behring ramp up

Broker cuts FY25 and FY26 earnings forecast by 3-4%

Price target increase is due to lower capital expenditures (“CAPEX”), overall, the broker’s medium term outlook is largely unchanged

Jefferies

Rating: BUY | Price target: $352.00⬇️ vs $355.30

Views:

Broker expects CSL to return to pre-pandemic levels of performance as Behring gross margins slowly improve

Broker sees Behring and Specialty Products as the key growth drivers going forwards, particularly highly anticipated FY25 product launches

The only point of weakness, says the broker, is the highly competitive market Vifor faces, particularly with respect to generics Europe – this has triggered a small reduction in the brokers earnings forecasts, but the long term outlook for CSL remains positive

Macquarie

Rating: OUTPERFORM | Price target: $330.00

Views:

Result was generally in line with the broker’s expectations

Medium to longer term earnings outlook remains strong as Behring gains momentum

Shares are currently attractively priced

Morgans

Rating: ADD | Price target: $330.75⬆️ vs $315.35

Views:

Results were in line with the broker’s expectations, with Behring showing significant growth and improved gross margins, but Seqirus was below expectations despite resilient margins, and Vifor clearly also is facing challenges – however maintained its margins

FY25 guidance was conservative, major earnings driver to be Behring

Broker likes CSL’s medium growth outlook, confident in strategy execution

Ord Minnett

Rating: UPGRADE TO ACCUMULATE⬆️ vs HOLD | Price target: $319.00⬆️ vs $317.30

Views:

Broker notes earnings were 2% better than expected and ahead of the company’s previous guidance, all segments were in-line with or better than expected

Some disappointment with FY25 guidance of 10%-13% growth vs broker’s forecast for 15%-16%, but broker puts this down to typically conservative CSL guidance

Earnings forecasts for FY25-FY8 are raised by 2%, sees CSL generating a compound average earnings growth of 13% over this time

RBC Capital Markets

Rating: SECTOR PERFORM | Price target: $278.00⬇️ vs $319.00

Views:

Broker was disappointed with both CSL’s FY24 results and its FY25 guidance – hence the substantial cut to the broker’s price target

Broker acknowledges there were signs of improvement at Behring and Vifor, but it remains unsure about the company’s medium term outlook

Broker trimmed earnings forecasts due to concerns over sustainability of recovery in margins and the potential impact from competition from generics

UBS

Rating: BUY | Price target: $340.00

Views:

Results were largely in line with the broker’s forecasts

Looking forward, brokers sees Behring as major driver of growth, particularly in albumin, but cuts forecasts for Vifor due competition from generics in Europe, and notes Seqirus may also face weaker flu vaccine demand

Broker sees cash flow improvement as capex reduces, to aid in some deleveraging

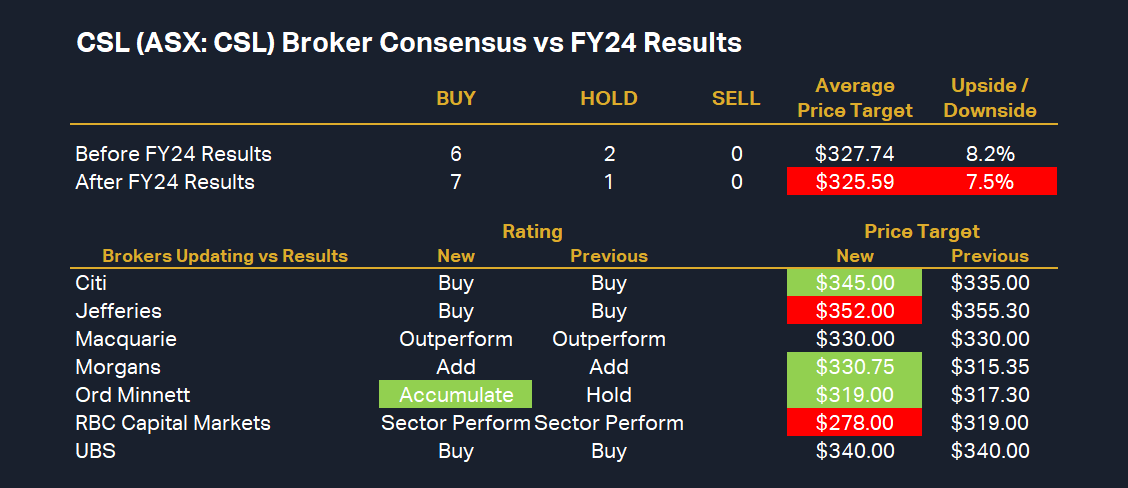

Broker consensus changes

%20Broker%20Consensus%20vs%20FY24%20Results.png)

CSL broker consensus changes (click here for full size image)

{kind=link}

To obtain a broker consensus rating, I like to assign a value of +1 to any rating better than HOLD/NEUTRAL/MARKETWEIGHT, 0 for HOLD/NEUTRAL/MARKETWEIGHT, and -1 to any rating worse than HOLD/NEUTRAL/MARKETWEIGHT. I associate an average rating value of greater than 0.5 as a BUY consensus, values between 0.5 and -0.5 a HOLD consensus, and values less than -0.5 as a SELL consensus.

Using this method, CSL’s average rating value of +0.88 (up from +0.75) earns it a consensus BUY rating.

The highest broker price target is $352, held by Jefferies, allowing for around +16% upside. The lowest broker price target is $278, held by RBC Capital Markets, allowing for around 8% downside.

CSL’s consensus price target fell to $325.59 from $327.74 (-0.7%). This implies the major brokers believe CSL shares are as much 7.5% undervalued on average based on the price at the time of writing of $303. (Note, if we remove RBC’s $278 target as an outlier, CSL’s average price target increases to $332.39, allowing for around 9.7% upside).

Brokers generally work on a 12 month basis for their price targets. CSL’s current annual dividend yield is around 1.3%, meaning investors in CSL shares could earn a total return of around 8.3% over the next 12 months based on the data presented here.