Tech crash deepens: Are ASX tech stocks heading to zero?

The ASX tech sector is as oversold as the dot-com crash, but AI disruption fears suggest the selloff may have further to run.

Source: Shutterstock

Mentioned

KEY POINTS

- The S&P/ASX 200 Tech Index has an RSI of 19, the most oversold since the dot-com bubble and far below pandemic or GFC levels

- AI disruption fears have intensified after Anthropic's Cowork release, with US software stocks posting their worst month since October 2008

- Despite the sharp selloff, most tech stocks still trade at relatively expensive multiples

The tech sector feels like the clearance section of a supermarket right now, the kind where items have stacked on multiple "quick sale" stickers.

The S&P/ASX 200 Technology Index is already down 16% year-to-date and down 40% since mid-September. It's moved in an almost straight line down, with only a handful of very short-lived bounces. For chartists, it undercut key areas like the 200-day moving average and the April 2025 Liberation Day low as if they were nothing.

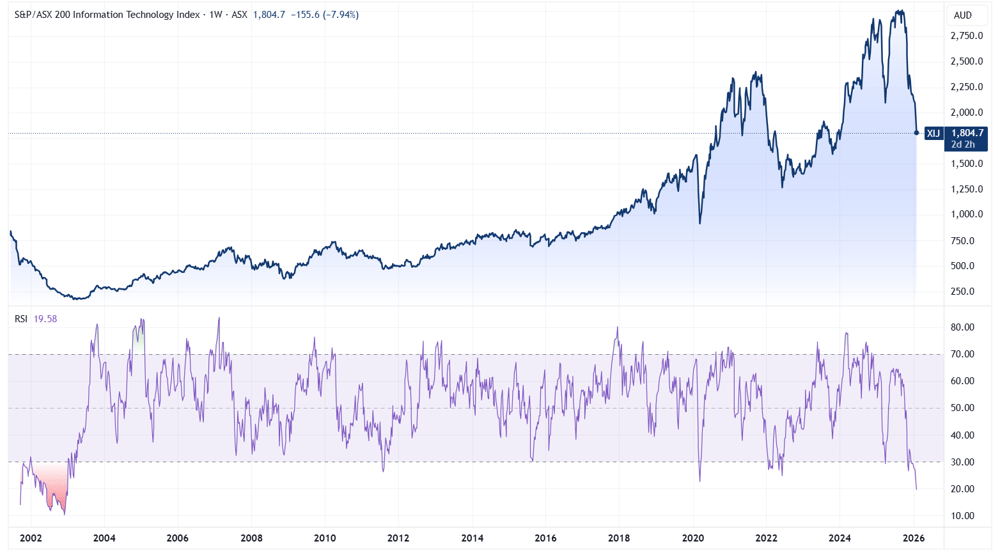

On the weekly chart, the RSI of the Tech Index has hit 19, far below Liberation Day (37), the pandemic (28) and the height of the GFC (26). Only the aftermath of the dot-com bubble (11) is comparable to how badly oversold the sector is today.

S&P/ASX 200 Tech Index with weekly RSI (Source: TradingView)

This leaves us with the million dollar question: how long will it go?

A quick recap

The Tech sector has been struggling for upside since June and started to roll over in October, when it hit a fresh five-month low and began trading below the 200-day moving average.

I didn't think much of this initial weakness, since a big driver of the Tech Index decline was:

Wisetech (ASX: WTC) almost halved between July and November, following a weaker-than-expected FY25 result (shares dipped 11%) and an Australian Federal Police raid on 27 October (shares down 15.9%). The company was also integrating a massive $3.2 billion acquisition of e2open and dealing with ongoing corporate governance headwinds from founder Richard White.

Xero (ASX: XRO) had also dipped around 40% over the same time period, largely driven by its $2.5 billion acquisition of US-based payments platform Melio. The business was acquired at a revenue multiple of approximately 13x. A revenue multiple was used since Melio is currently loss making.

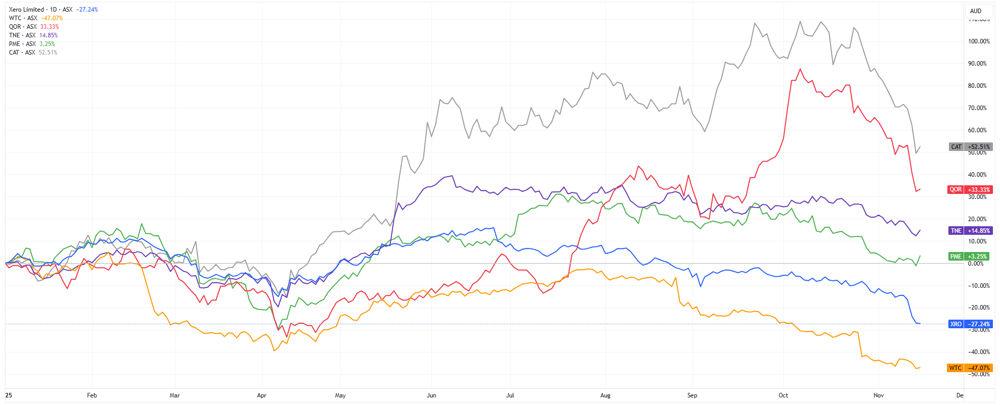

But by November, things started to look fishy as high-flying names like Life360, Catapult and Qoria started to tumble 10-20% in a short span of time.

Catapult (grey), Qoria (red), TechnologyOne (purple), Pro Medicus (green), Xero (blue) and Wisetech (yellow) | Source: TradingView

This November selloff was attributed to several factors including a hotter-than-expected inflation print (back in Nov-25), soaring Aussie bond yields, rich valuations (XRO, WTC and TNE all traded around 95-100x) and broader market weakness.

The n(ai)l in the coffin

AI disruption fears have triggered capitulation-style selling in software-related stocks. The selloff intensified after Anthropic released its newest AI agent platform, Cowork, on Tuesday.

Cowork enables the Claude model to go beyond chat and actually execute work on your computer or in specific workflows.

This triggered another sharp selloff overnight, with notable decliners including Intuit (-10.9%), Shopify (-9.8%), ServiceNow (-7.0%), Salesforce (-6.8%), Adobe (-7.3%) and SAP (-4.8%). The S&P North American Software Index is now down 15% in January, marking its worst month since October 2008.

What's driving the fear is not collapsing earnings, but collapsing confidence in future growth and pricing power. Only 67% of US software companies have beaten revenue expectations this reporting season vs. 83% for tech overall, and investors are increasingly worried about seat compression, vibe coding and AI-native competitors lowering switching costs.

An interesting comment crossed the Jefferies trading desk: "I ask clients, 'what's your hold-your-nose level?' and even with all the capitulation, I haven't heard any conviction on where that is. People are just selling everything and don't care about the price."

Wednesday proved to be a bloodbath for local tech stocks, with heavyweight names leading the downside move.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

XRO | Xero | -15.9% | $80.82 | -29.0% |

NXL | Nuix | -10.9% | $1.52 | -16.3% |

WTC | Wisetech | -10.7% | $51.25 | -25.2% |

TNE | Technology One | -10.5% | $22.65 | -17.8% |

SDR | Siteminder | -7.9% | $4.52 | -26.3% |

MAQ | Macquarie Technology | -7.1% | $63.43 | -5.3% |

BVS | Bravura Solutions | -7.1% | $1.84 | -28.6% |

CAT | Catapult Sports | -6.6% | $3.28 | -21.2% |

DTL | Data#3 | -6.3% | $9.48 | 5.7% |

WBT | Weebit Nano | -6.3% | $4.91 | -1.8% |

HSN | Hansen Technologies | -6.2% | $4.65 | -11.9% |

360 | Life360 | -5.9% | $26.94 | -16.4% |

MP1 | Megaport | -4.9% | $10.85 | -10.9% |

OCL | Objective Corporation | -4.4% | $14.63 | -11.6% |

IRE | Iress | -4.0% | $7.88 | -6.0% |

NXT | NextDC | -3.1% | $12.85 | 2.2% |

Where to from here?

This is the challenging part. But here's some food for thought.

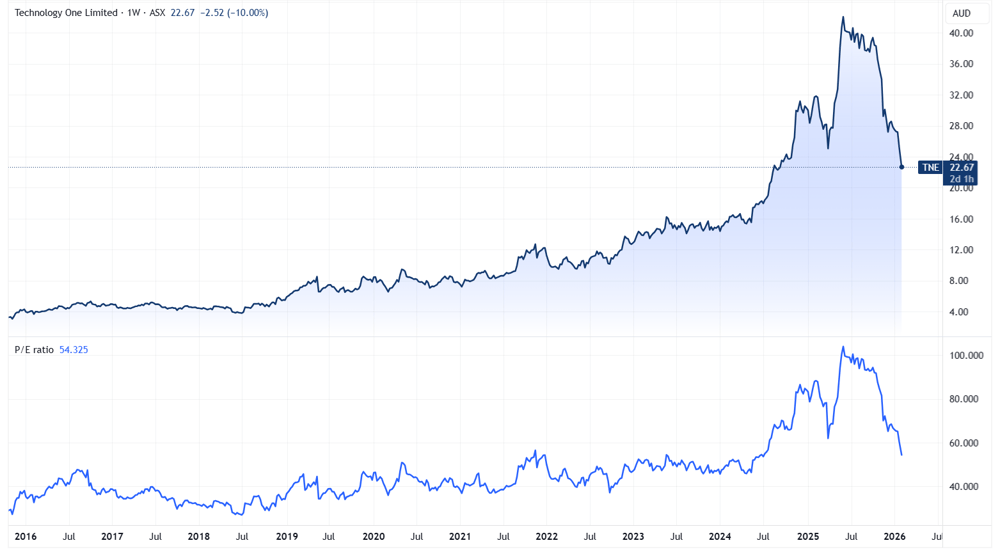

Let's take a look at Technology One (ASX: TNE). It's one of the most reliable, all-weather growth stocks out there, with a net profit compound average growth rate of 14.3% over the past ten years (FY16-FY25).

While mid-teens might not sound like much, that's seen its earnings grow from $41 million in FY16 to $137 million in FY25. UBS analysts expect the company to deliver earnings growth of 18-20% per annum through to FY30.

Since 2016, TNE has mostly traded at a price-to-earnings of 35-50x. But over the course of 2024-25, this multiple abruptly soared to a peak of almost 105x. In other words, the share price decided to double, despite the company growing at its usual clip.

TechnologyOne price chart (TOP), price-to-earnings (bottom) | Source: TradingView

Despite the stock falling almost 50% from its June 2025 peak, it could in theory fall another 20-30% to trade in line with those historic average multiples.

The bottom line is that these tech stocks started to trade at extreme multiples, despite not delivering anything extraordinary.

The thing is, multiples should expand and compress, depending on sentiment and market cycles. The difference between a stock trading at 100x and 50x is a long line of willing buyers that are happy to fork up such prices. It's no different to Labubu's.

The good thing is that most mid-to-large cap tech stocks have some intrinsic value to them (after the post-pandemic tech exodus). The stocks that have risen to mid-to-large cap territory are mostly profitable and cashflow positive, with a solid track record of growth.

So at some point, the sector will bottom, growth rates will suddenly look very attractive again and we'll return to multiple expansion.

But for now, the path of least resistance appears to be more 'quick sale' stickers (or AI actually eats up all these businesses and they go to zero).