Property or shares? How the new CGT and negative gearing changes have transformed the investing landscape

Australia’s biggest investment tax shake-up in decades is changing the rules for property and shares. We highlight the winners and losers.

Source: Market Index

Mentioned

KEY POINTS

- For decades, negative gearing and the 50% CGT discount helped shape Australia’s obsession with property investing — and rewarded long-term capital growth over income.

- The Federal Budget’s tax overhaul changes that equation, reducing key advantages for investment property while favouring franked dividend income.

- Here’s what the new rules mean for property, ASX shares, growth stocks, dividend investing, and the investors trying to decide where to put their money.

For decades, Australians looking to build wealth have faced the same question: property or shares?

For many investors, the answer barely felt like a choice at all. Residential property offered generous tax advantages, easy access to leverage, and the perception that house prices only ever moved in one direction — up.

Meanwhile, shares were often seen as the riskier alternative. The share market could deliver enormous long-term returns, but it also came with volatility, including the occasional crash capable of wiping out years of gains in a matter of months.

That investing equation changed dramatically in this year’s Federal Budget. The Labor government’s decision to replace the 50% capital gains tax (CGT) discount with inflation indexation — while also restricting negative gearing on established investment properties — represents one of the biggest changes to Australia’s investment tax system in decades.

At the same time, investors can still negatively gear portfolios of shares, while the dividend imputation system — including Australia’s highly valuable franking credits — remains untouched.

The result is a very different investing landscape from the one Australians have known since the late 1990s. The new tax changes likely make growth-focused investing less tax efficient, while property investors will be forced to bear a greater share of their investment-related costs.

Property still offers advantages shares cannot easily replicate, including leverage, scarcity, and the tax-free status of the family home. Shares, meanwhile, retain key advantages of their own — including liquidity, diversification, lower entry costs, and the ability to fully negative gear a portfolio.

For investors trying to decide where to put their money, understanding the new rules — and the trade-offs between different asset classes — has never been more important.

In this beginner’s guide to Australia’s new investing landscape, we break down exactly how the CGT and negative gearing changes work, compare property and shares under the old and new systems, and explain what the reforms may mean for growth stocks, dividend investing, and long-term wealth creation.

Out with the old…

To understand why the new rules matter, it helps to first understand how Australia’s old investment tax system worked, and how it heavily shaped investor behaviour for more than two decades.

At the centre of the old system were two major tax advantages: the 50% capital gains tax (CGT) discount and negative gearing. Together, they rewarded investors who borrowed money to buy assets that could rise strongly in value over time — particularly property, but also shares and other investments.

What is capital gains tax?

Capital gains tax is the tax investors pay on profits made when selling an asset.

If an investor bought shares for $10,000 and later sold them for $15,000, the $5,000 profit would generally be treated as taxable income (i.e., at their marginal tax rate).

Before this year’s Budget changes, investors who held an asset for more than 12 months could access the 50% CGT discount. This meant only half of the profit was added to their taxable income.

For example:

An investor buys shares for $10,000

They later sell them for $30,000

Their capital gain is $20,000

Under the old system, only $10,000 would be taxable at the investor’s marginal tax rate

The longer an investor held an asset — and the more strongly it grew in value — the more valuable the tax discount became.

This was particularly attractive for investors focused on capital growth rather than income.

What is negative gearing?

Negative gearing occurs when the cost of holding an investment is greater than the income it generates.

For property investors, this often meant the rent received from tenants was not enough to cover expenses such as mortgage interest, council rates, insurance, maintenance, and strata fees.

Under the old system, investors could deduct those losses from their taxable income, reducing the amount of tax they paid each year.

For example:

A property investor earns $120,000 per year from their job

Their investment property loses $15,000 after expenses

Their taxable income falls to $105,000

The combination of negative gearing and the 50% CGT discount created a powerful incentive for investors to tolerate short-term losses in exchange for potentially large long-term capital gains.

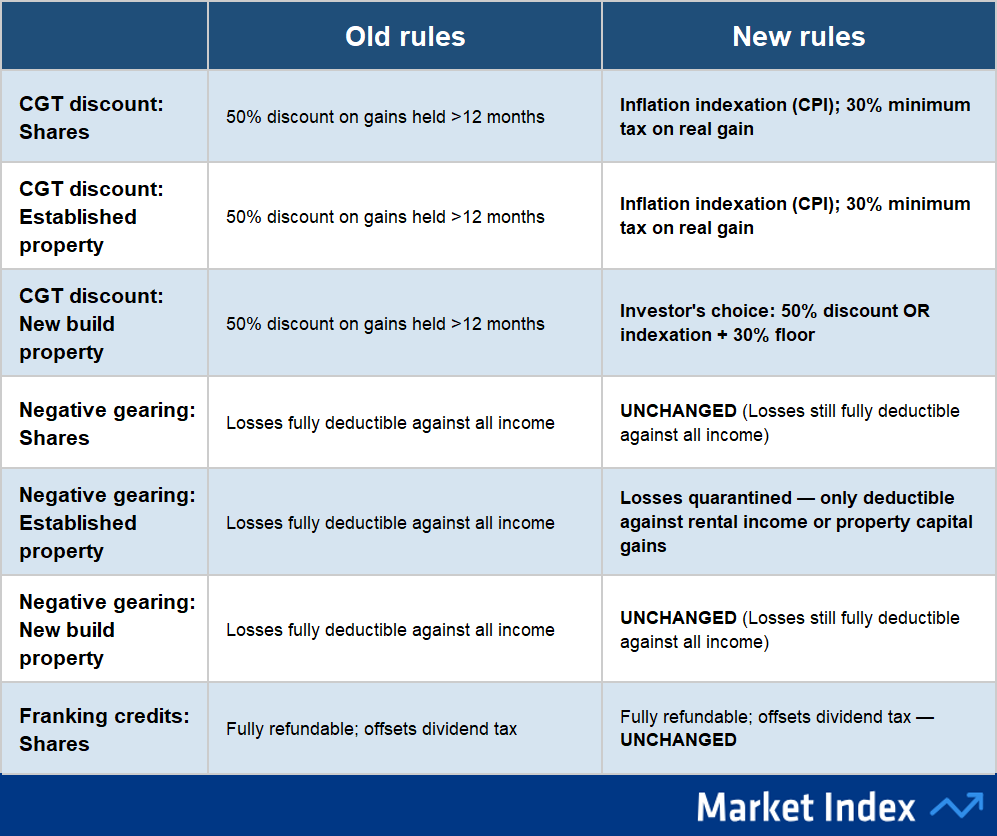

This bit is important: Under the new changes, investors can only negative gear newly built residential properties. However, the rules for negative gearing shares have not changed. This means investors can still claim investment losses against their taxable income if interest costs and other expenses exceed the dividend income generated by their portfolio.

What are franking credits?

Franking credits are one of the most distinctive features of Australia’s share market. They were introduced to prevent company profits from being taxed twice — once at the company level, and again when paid to shareholders as dividends.

When an Australian company pays tax on its profits, it can pass those tax credits on to shareholders through fully franked dividends.

For example:

A company earns $100 in profit

It pays $30 in company tax on the profit

The remaining $70 is paid to shareholders as a fully franked dividend

The shareholder also receives a $30 franking credit

Depending on their personal tax rate, an investor in the above company may:

Marginal tax rate > 30%: pay additional tax up to their marginal tax rate (e.g. for an investor with a 45% marginal tax rate: 45% x $100 = $45 tax. Less $30 franking credit = $15 additional tax to pay)

Marginal tax rate <30%: receive part of the franking credit back as a refund (e.g. for an investor with a 15% marginal tax rate: 15% x $100 = $15 tax. Less $30 franking credit = $15 refund)

Over time, the combination of franking credits, negative gearing, leverage, and the 50% CGT discount helped shape Australia into one of the world’s most property- and dividend-focused investing cultures.

What changed in the 2026 Federal Budget?

There were two big changes, and understanding both and how they interact, is the key to working out where your money works hardest under the new rules.

Change 1: The 50% CGT discount is gone

From 1 July 2027, when you sell an investment that you've held for more than 12 months, you can no longer halve the taxable gain. Instead, your cost base (i.e., what you originally paid) is adjusted upward for inflation using the Consumer Price Index (“CPI”). You're then taxed on the real gain (i.e., the bit above inflation) at your marginal tax rate. A 30% minimum tax rate applies, meaning even low-income investors pay at least 30% on any real capital gain.

Change 2: Negative gearing on established residential property is deferred

If you buy an established residential investment property after Budget night (12 May 2026), any annual losses can no longer be deducted against your salary or other income in the year they occur. Instead, they carry forward and can only be offset against future rental income or the capital gain when you sell.

The losses aren't lost — but the annual cash-flow benefit that made negatively geared property so attractive is gone. Investors must fund the shortfall out of their own pocket each year and wait and see on any tax relief. There is some comfort in how the numbers work at the point of sale, though: carried-forward losses are applied at full face value — they don't shrink with inflation — while the capital gain is indexed for CPI before tax is calculated. The two work together on exit in a way that softens the overall tax burden, even if it doesn't replace the annual relief investors previously enjoyed.

Note: New residential property builds are treated differently. Investors in newly constructed dwellings retain full negative gearing and get a bonus: when it comes time to sell, they can choose whichever CGT treatment is more favourable — the old 50% discount or the new inflation indexation.

The table below summarises what's changed across both asset classes.

Note: CGT changes apply to assets held for more than 12 months. Assets purchased and sold before 1 July 2027 are fully subject to the old rules. For assets held before 1 July 2027 and sold after, gains accrued before that date retain the 50% discount; only gains from 1 July 2027 onward are indexed. Age Pension recipients and JobSeeker recipients are exempt from the 30% minimum tax. Negative gearing for property rules commenced Budget Night, May 12, 2026.

Property vs shares under the new regime

Here's the part that hasn't made as many headlines as it should: the negative gearing rules for shares haven't changed at all.

If you borrow money to invest in a share portfolio and your interest costs exceed your dividend income, that loss is still fully deductible against your salary or wages — dollar for dollar, straight away. No quarantining. No waiting. Exactly as it always worked.

That's a meaningful shift in the relative appeal of the two asset classes. A property investor buying an established home today faces a fundamentally different tax equation from a share investor borrowing to build a portfolio. Both will still be subject to the same new CGT rules when they sell. But in the years leading up to that sale, the share investor retains a tax advantage the property investor has lost.

Property still has real advantages shares can't match. Leverage is the big one. With $100,000, a property investor might secure a $1 million mortgage and own a $1.1 million asset. A share investor using a margin loan on the same $100,000 might borrow another $60,000 — giving them $160,000 in total exposure. The math on leverage still strongly favours property, even under the new rules.

The family home also remains completely CGT-free — an advantage no share portfolio can replicate. And property offers the kind of enforced savings discipline that many investors genuinely need: it's hard to panic-sell a house at midnight because a war broke out in the Middle East!

But for investors weighing up where to put their money — particularly those considering borrowing to invest — the removal of negative gearing on established property tips the balance towards shares more than it has in decades.

Should you buy growth or income stocks now?

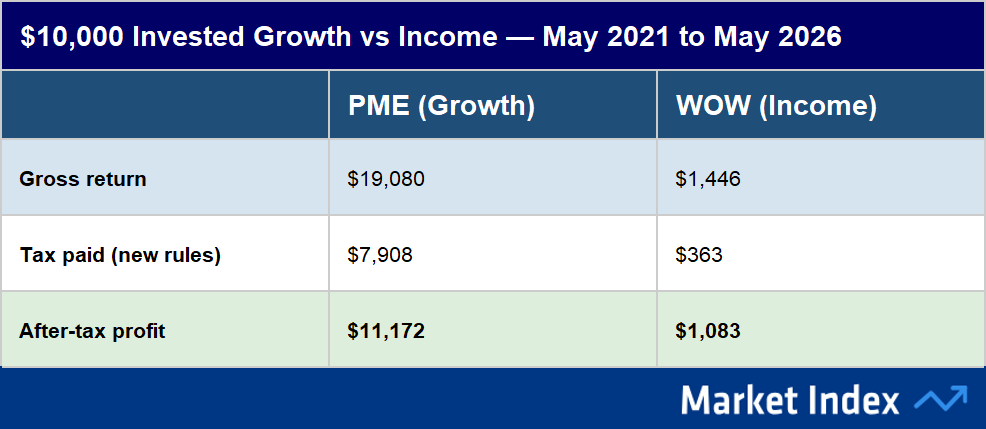

The new CGT rules hit different investors very differently depending on how they invest. To show exactly how, let's look at two real ASX stocks over the past five years — one a classic growth stock, one a classic income stock — and run the numbers under both the old and new rules.

Investor A chose Pro Medicus (PME) — a medical imaging software company that has grown earnings by roughly 39% per year for five consecutive years. PME pays a small but growing fully franked dividend, but the real story is its capital growth: PME’s share price has climbed from $45.41 in May 2021 to $130.18 in May 2026 (to be completely fair, it hit $336 in July last year!).

Investor B chose Woolworths (WOW) — Australia's largest supermarket chain. WOW pays a reliable fully franked dividend, but underlying earnings have been essentially flat over the same five years. As a result, the share price has gone almost nowhere, ending May 2026 at $34.94 — just 16 cents below where it started in May 2021.

Both investors invested $10,000. Both held for exactly five years. Both are assumed to be on the top marginal tax rate of 47%. Here's how their returns looked under the old and new CGT rules:

Investor A — Pro Medicus (PME)

%20-%2010K%20Invested%20May%202021%20to%20May%202026.png)

Note: CPI indexation calculated using actual ATO quarterly CPI data (All groups, weighted average of 8 capital cities). CPI at acquisition (June quarter 2021): 118.8. CPI at disposal (March quarter 2026, most recent complete quarter): 140.7. Indexation factor: 1.1843 (18.43% total inflation over the period). Indexed cost base: $11,843. Real capital gain: $18,668 − $1,843 = $16,825. Tax of 47% on $16,825 = $7,908.

Investor B — Woolworths (WOW)

%20-%2010K%20Invested%20May%202021%20to%20May%202026%20to%20May%202026.png)

Note: WOW dividends are 100% franked. The grossed-up dividend income is $2,133 ($1,493 ÷ 0.70). At 47% marginal rate, tax on grossed-up dividends is $1,002, less $640 in franking credits = $363 net tax payable. This treatment is identical under both old and new rules — franking credits are untouched by the Budget changes.

Head-to-head comparison

Growth or Income? The answer is: quality

The numbers tell a clear story. Yes, the new CGT rules cost the PME investor an extra $3,521 in tax compared with the old system. But even after paying $7,908 in capital gains tax under the new rules, the PME investor walks away with $11,172 in after-tax profit — more than ten times what the WOW investor made.

IMPORTANT: Don't let the tax tail wag the investment dog!

Which brings us to an important point. When it comes to investing, a higher tax bill on a great investment is still a far better outcome than a lower tax bill on a mediocre one. The new rules raise the cost of success — but they don't change the fundamental logic of seeking out quality growth companies.

There’s been a lot of talk in the media since Budget night that the new CGT changes will shift investor focus towards income stocks, but this case study shows that companies that deliver quality earnings growth — genuine, sustained, and compounding like PME's — are worth paying a bit of extra tax for.

How to negative gear a share portfolio

Under the new rules negative gearing is now one of shares' clearest advantages over investing in established properties, and it could be the carrot that coaxes over previously dyed in the wool property investors.

The concept is identical: borrow money to invest, and if the interest on that loan exceeds the income you earn from the investment, the net loss is tax-deductible. For shares, that means if your loan interest exceeds your dividend income, the shortfall reduces your taxable income immediately — saving you tax in the current financial year.

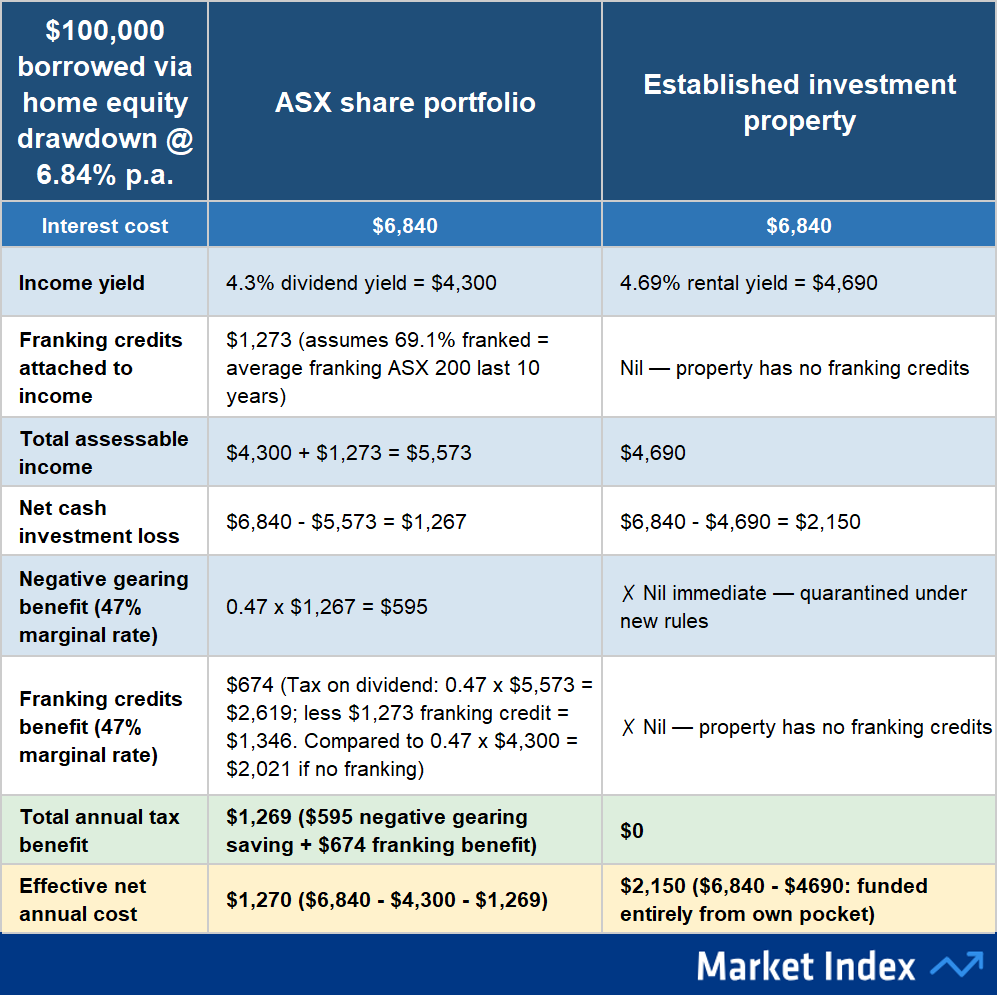

Here's a worked example comparing a $100,000 share portfolio and a hypothetical $100,000 residential investment property. Now, clearly, $100,000 isn’t going to buy you much of a house in today’s market, but let’s just see how the two asset classes compare on a like-for-like basis.

6.84% p.a. interest rate: average Australian variable mortgage rate per Finder.com.au, May 2026. 4.3% p.a. dividend yield: Morningstar 10-year average ASX 200 dividend yield. 69.1% average franking: ASX 200 10-year average (Intelligent Investor). Franking credits = (dividend income × 69.1%) × (30 ÷ 70) = $1,273. Tax on grossed-up dividends ($5,573) at 47% = $2,619, less $1,273 franking credits = $1,346 net dividend tax. Without franking credits, dividend tax would be $2,021 — a net franking benefit of $674. 4.69% p.a. rental yield: Global Property Guide, Q1 2026 gross yield, national average. Established investment property purchased after 12 May 2026 — losses quarantined under new Budget rules. For capital gains treatment, property running costs (rates, insurance, maintenance), and rental vacancy not included. Individual outcomes will vary; seek licensed financial advice before borrowing to invest.

The numbers above illustrate how the new rules have shifted the equation. Both investors borrow the same amount at the same rate. The property investor actually earns slightly more income from their investment — $4,690 in rent versus $4,300 in dividends. But between negative gearing and franking credits, the share investor receives $1,269 in annual tax benefits the property investor cannot access under the new rules.

The result: the share investor's effective net annual cost is just $1,270, while the property investor is $2,150 out of pocket. It's worth being clear about what "out of pocket" actually means, though. The property investor's annual losses aren't gone forever — they accumulate and can be used to reduce the capital gain when the property is eventually sold.

One more thing worth flagging: this comparison excludes property running costs — rates, insurance, maintenance, property management fees — which typically amount to an additional 1–2% of the property's value each year in out-of-pocket expenses. Include those, and the property investor's effective out-of-pocket cost rises further still. Shares have no equivalent ongoing holding cost.

Property vs shares: which is better under the new rules?

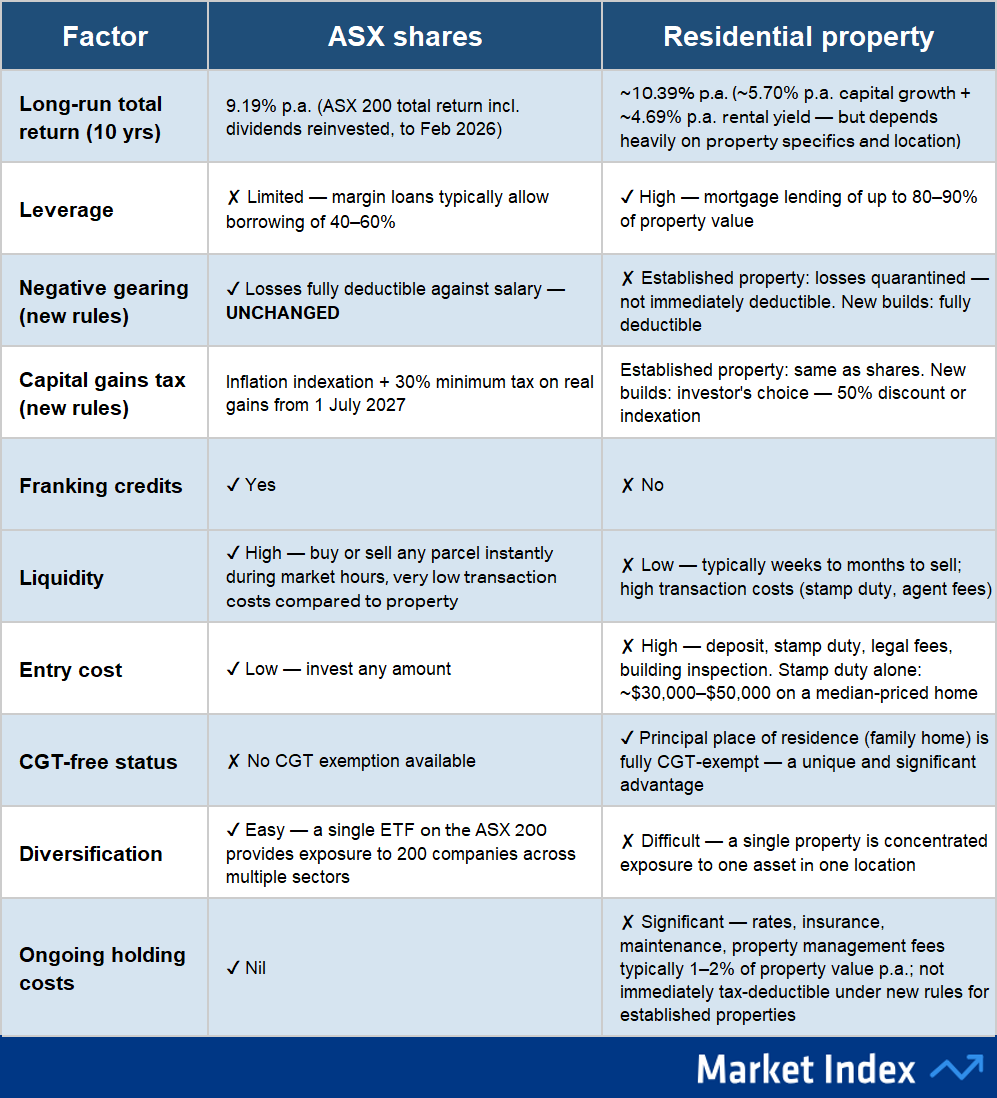

So where does all this leave the investor standing at the crossroads between property and shares? The honest answer is: it depends on your circumstances, your risk appetite, and your investment horizon. But the new rules have shifted the balance in some meaningful ways.

All return figures are historical and do not guarantee future performance. ASX 200 10-year total return: SPDR S&P/ASX 200 ETF (STW) annualised total return to February 2026, per Yahoo Finance/State Street. Property capital growth: ABS mean dwelling price data Dec 2015-Dec 2025. Gross rental yield: Global Property Guide, Q1 2026. Property and share returns are not directly comparable — property returns depend heavily on location, leverage, holding period, and costs. Stamp duty estimate based on median dwelling price of approximately $900,000 (Cotality, February 2026) in a typical state. This table is a general guide only and does not constitute financial advice.

Property's strongest remaining advantage is leverage. The ability to borrow ten times your deposit against a tangible asset — and capture the full capital gain on that larger sum — is something the share market's margin lending arrangements simply can't match. The family home's CGT exemption is also irreplaceable.

But the new tax landscape has tilted the playing field. Shares retain full negative gearing. They carry no stamp duty. They can be bought and sold in seconds. They offer built-in diversification across dozens of companies. And for income-focused investors, fully franked dividends — untouched by the Budget — deliver tax-efficient income that no other asset class in Australia can replicate at scale.

Most importantly: the case studies above show that the single biggest driver of long-term after-tax wealth isn't asset class selection — it's investment quality.

An investor in a genuinely great growth company, even paying more tax under the new rules, will accumulate far more wealth than an investor in a mediocre income stock paying less tax. The same could be said about the shares vs property debate: how closely will each asset class's returns over the next ten years resemble the last ten? The new rules haven't changed the calculus — they've reinforced it: Find quality, hold it, and pay the tax gladly.

References

This article draws on reporting from Livewire Markets (Keith Ford, Michael Bell & Solaris Investment Management, Vishal Teckchandani) and institutional analysis from Commonwealth Bank of Australia and National Australia Bank (all May 2026). Share price and dividend data sourced from Market Index. Consult your financial adviser before making any decisions about investing in shares or property.