Origin Energy soars on profit beat, Utilities sector within 2% of all-time highs

ORG’s electricity-led beat delivers a stellar half-year result, reversing the early February slump

Source: Source: Shutterstock

Mentioned

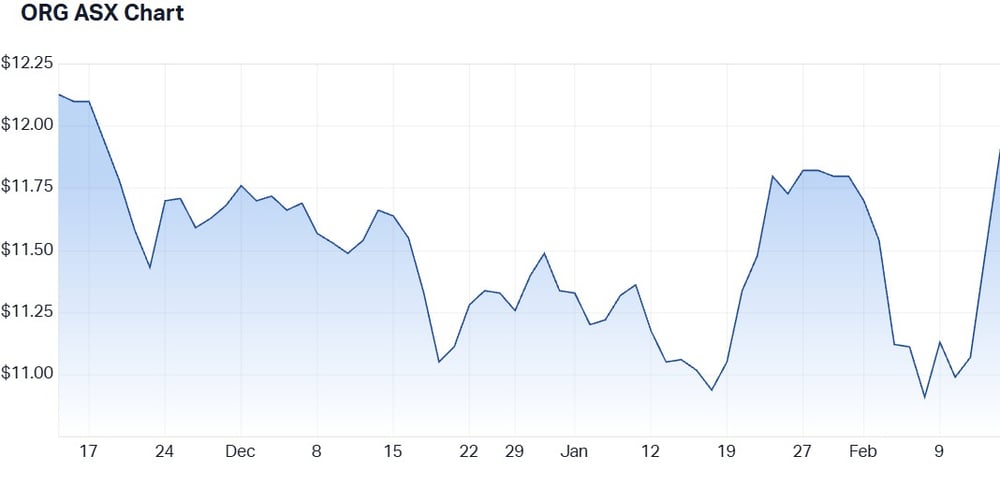

Origin Energy (ORG) shares surged 8.2% over the last two sessions after its 1H FY26 result, as a clear electricity gross profit beat pushed Energy Markets earnings ahead of expectations and supported a higher FY26 outlook. Stronger customer tariffs and lower net pool and green scheme costs, plus reduced solar feed in tariffs, delivered an EBITDA beat that more than offset softer Integrated Gas and a larger first half loss at Octopus.

The company tightened FY26 Energy Markets underlying EBITDA guidance to $1.55-1.75bn, lifting the midpoint about 6.5%. It flagged lower wholesale prices as a FY27 headwind, while Jarden said lower coal costs and incremental battery earnings should help offset the impact.

Key numbers

Revenue down 2.3% to $7.99bn vs $8.18bn ests (2.3% miss)

Adjusted EBITDA up 3.2% to $1.59bn vs $1.54bn ests (3.2% beat)

Underlying NPAT up 7.6% to $593m vs $551.3m ests (7.6% beat)

Outlook: FY26 Energy Markets EBITDA guidance $1.55-1.75bn vs. prior guidance of $1.4-1.7bn (midpoint up 6.5%)

How the result stacked up

Brokers largely centred their scorecards on the electricity gross profit line.

RBC Capital Markets described Energy Markets as ahead of expectations on tariff repricing and lower scheme and solar feed in costs, with Integrated Gas better than feared and Octopus still loss making but FY26 guidance maintained. It left the target unchanged at $13.50.

Jarden attributed the beat to electricity gross profit and said it underpinned the 6.5% FY26 Energy Markets midpoint upgrade, raised target from $11.65 to $12.00. It noted that Octopus ran weaker in 1H but guidance was reiterated.

UBS highlighted Energy Markets EBITDA about 6% above consensus, target unchanged at $14.00 and said electricity margins exceeded through the cycle settings.

The stock rallied as much as 7.4% on the result, but finished the session 3.8% higher at $11.50.

Where to from here

Analysts leaned into FY27 earnings durability and the value of Octopus and Kraken.

Jarden said lower coal costs and battery earnings should help offset softer wholesale pricing into FY27.

UBS pointed to multi-year upside from customer growth, lower cost to serve and batteries, and argued the market is undervaluing the Octopus and Kraken stake versus recent funding round pricing.

Softer tech multiples were noted as a headwind for Kraken valuation, but brokers remained constructive given Origin’s low-end leverage position and FY26 guidance upgrade.

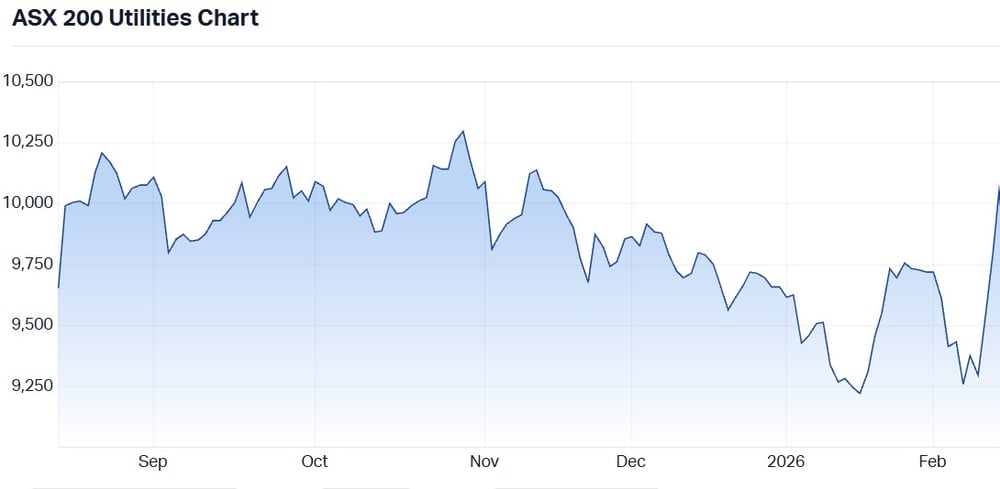

Overall, it’s been a very strong results season for utilities, with both Origin and AGL rallying off the back of better-than-expected earnings. The S&P/ASX 200 Utilities Index has rallied 8.7% in the last three sessions, now trading at a fresh three-month high.