Morning Wrap: ASX 200 futures slip ahead of CPI print, OpenAI revenue miss drags S&P 500 lower

ASX 200 futures are down 37 pts (-0.42%) as of 8:30 am AEST.

In this article

ASX 200 futures are down 37 pts (-0.42%) as of 8:30 am AEST.

In a nutshell:

Major US benchmarks lower after OpenAI reportedly missed internal targets for new users and revenue, with CFO Sarah Friar warning that the company may not be able to pay for future computing contracts if revenue does not growth fast enough

US-Iran peace talks remain in a standstill, with Brent up 2.4% to US$104.49 overnight and analysts pushing out Hormuz reopening timelines towards May-June

UAE will exit OPEC next month after six decades of membership, marking a significant blow to the Group

A wild 24 hours ahead: Alphabet, Microsoft, Amazon and Meta earnings due tomorrow, Australian inflation data this morning and FOMC tonight

Let's dive in.

Overnight Summary

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

S&P 500 | 7,139 | -0.49% |

Dow Jones | 49,142 | -0.05% |

NASDAQ Comp | 24,664 | -0.90% |

Russell 2000 | 2,756 | -1.15% |

Country Indices | ||

Canada | 33,584 | -0.69% |

China | 4,079 | -0.19% |

Germany | 24,018 | -0.27% |

Hong Kong | 25,680 | -0.95% |

India | 76,887 | -0.54% |

Japan | 59,917 | -1.02% |

United Kingdom | 10,333 | +0.11% |

Name | Value | % Chg |

|---|---|---|

Commodities (USD) | ||

Gold | 4,596.17 | -1.86% |

Copper | 5.92 | -1.66% |

WTI Oil | 99.93 | +3.69% |

Currency | ||

AUD/USD | 0.7184 | +0.03% |

Cryptocurrency | ||

Bitcoin (USD) | 76,426 | -0.83% |

Ethereum (AUD) | 3,189 | +0.15% |

Miscellaneous | ||

US 10 Yr T-bond | 4.354 | +0.42% |

VIX | 17.83 | -1.05% |

US Sectors

Sector | % Chg |

|---|---|

| Energy | +1.65% |

| Real Estate | +0.99% |

| Consumer Staples | +0.99% |

| Health Care | +0.24% |

| Financials | +0.14% |

| Utilities | +0.13% |

Sector | % Chg |

|---|---|

| Communication Services | -0.23% |

| Consumer Discretionary | -0.68% |

| Industrials | -0.88% |

| Materials | -1.07% |

| Information Technology | -1.29% |

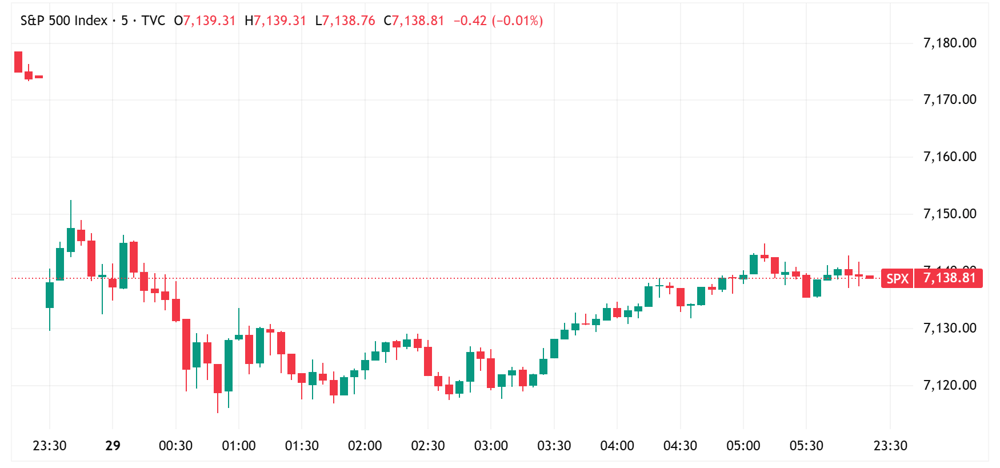

S&P 500 SESSION CHART

S&P 500 lower, off worst levels (Source: TradingView)

OVERNIGHT MARKETS

Major US benchmarks finished lower, as a WSJ report on OpenAI revenue weakness triggered a broad chip selloff, snapping the semis' 18-session rally

Markets on the defensive as AI capex growth under question, systematic re-risking facing exhaustion alongside big bounce in sentiment and month-end selling pressure, Brent also moving above US$100 as US-Iran remain at a standstill and analysts push out Hormuz reopening timeline

Still plenty of patches of green in Energy, Consumer Defensives, Healthcare, Utilities and Financials

A weak session for commodities, with Silver (-3.2%), Gold (-1.8%), Copper (-1.7%), Aluminium (-1.0%), weighed by a stronger US dollar, rising real yields and broader risk-off sentiment

OpenAI missed internal revenue and weekly active user targets of 1bn in early 2026 according to a WSJ report, with CFO Sarah Friar warning compute commitments may outpace revenue if growth slows (BBG)

Key AI/semi names like Oracle, Nvidia, AMD, Broadcom and CoreWeave broadly lower as investors questioned the durability of the OpenAI capex pipeline ahead of mega-cap tech earnings this week (CNBC)

Treasury holdings at Wall Street dealers reach highest since 2007 after Trump administration eased regulations (FT)

Jamie Dimon warns a possible credit market downturn could be worse than expected (BBG)

ENERGY

UAE confirmed it will exit OPEC and OPEC+ effective Friday May 1, ending 59 years of membership in a major blow to the cartel and Saudi Arabian leadership (CNBC)

Aramco is suspending LNG shipments next month after damage to main export facility in February (FP)

Saudi Arabia may reduce June crude prices to Asia amid cooling demand and disruptions (RT)

Iran seeks new oil storage methods to prevent production shutdown amid US naval blockade, stalled negotiations (WSJ)

Tanker traffic through the Strait of Hormuz remains near zero against pre-war daily transit of more than 100 ships, with the Pentagon estimating six months to fully clear Iranian sea mines (AlJ)

IEA chief Fatih Birol warned Europe has only "maybe six weeks" of jet fuel supply left, with Lufthansa cancelling 20,000 short-haul flights through October to conserve fuel (AlJ)

Shell CEO warns energy shortages caused by Iran war could extend into 2027 (BBG)

IRAN

Trump rejected Iran's latest peace proposal to reopen the Strait of Hormuz in exchange for lifting the US naval blockade, with Tehran's nuclear program the main sticking point per the New York Times (BBG)

Iran's hardline IRGC seizes wartime power, mitigating Supreme Leader's role (RT)

Iran expected to submit revised peace proposal to end war soon, according to Pakistani sources (WSJ)

Iran banned exports of steel products including slabs and sheets effective April 26 after Israeli airstrikes destroyed an estimated 70% of domestic capacity (CBS)

Israel struck Hezbollah infrastructure across southern Lebanon, with the IDF citing alleged ceasefire violations as the truce continues to fray nine weeks into the broader conflict (CBS)

STOCKS

Coca-Cola Q1 2026: revenue up 12% to $12.47bn, organic revenue up 10%, comparable EPS $0.86 beat ests by ~6%, raised FY26 EPS growth guidance to 8 to 9%, shares up ~4% (BBG)

General Motors Q1 2026: revenue $43.6bn beat by ~0.5%, adjusted EPS $3.70 beat by ~42% aided by a $500m Supreme Court tariff refund, raised FY26 EBIT-adjusted guidance to $13.5-15.5bn (CNBC)

Spotify Q1 2026: revenue €4.53bn up 8% year-on-year, MAU 761m up 12% year-on-year, premium subs 293m, operating income hit a record €715m, but shares fell around 12% on softer Q2 outlook (YF)

UPS Q1 2026: revenue $21.2bn down 1.6%, adjusted EPS $1.07 beat by ~5%, US Domestic operating profit nearly halved to $515m, reaffirmed FY26 revenue target of $89.7bn, shares down ~4% (CNBC)

Australia warns Meta, Google and TikTok of 2% levy if they don't pay local media (RT)

BP's quarterly profit more than doubles to $3.2bn, boosted by Iran war trading (BBG)

TARIFFS & TRADE

US Customs continued processing IEEPA tariff refund claims through the CAPE portal launched April 20, with up to $20bn in refunds owed across 300,000-plus importers (KL)

US denies ~15% of the 1.74M tariff refund claims filed so far (BBG)

CENTRAL BANKS

Bank of Japan held the rate at 0.75% in a 6-3 split vote, with three dissenters wanting a hike to 1% citing Iran-driven inflation risk (CNBC)

BOJ raised its FY26 core inflation forecast to 2.8% from 1.9%, cut FY26 GDP growth forecast to 0.5% from 1%, framing the move as a "hawkish hold." (BBG)

US FOMC began its two-day meeting, with markets pricing 100% odds of a hold at 3.50-3.75% in what is widely expected to be Powell's final meeting as chair (CNBC)

ECB and BoE rate decisions due later this week, with markets pricing potential rate hikes from both as Iran-driven energy inflation feeds through (TE)

ECONOMY

Australian Q1 CPI release due 11:30 am AEST today, a key input for the RBA's May meeting after Westpac-MI consumer sentiment plunged 12.5% in April to 80.1 on fuel and rate-rise fears (WBC)

Industry ETFs

Name | Value | % Chg |

|---|---|---|

Commodities | ||

| Steel | 102.26 | +0.56% |

| Lithium & Battery Tech | 83.77 | -1.39% |

| Strategic Metals | 97.91 | -3.01% |

| Silver | 66.2 | -3.12% |

| Copper Miners | 78.69 | -3.68% |

| Uranium | 54.23 | -4.36% |

| Gold Miners | 88.54 | -4.37% |

Industrials | ||

| Agriculture | 27.96 | +1.41% |

| Aerospace & Defense | 216.21 | +0.08% |

| Global Jets | 25.28 | -0.98% |

| Construction | 106.867 | -1.05% |

Healthcare | ||

| Biotechnology | 167.81 | -0.72% |

Name | Value | % Chg |

|---|---|---|

Cryptocurrency | ||

| Bitcoin | 10.46 | -0.76% |

Renewables | ||

| Solar | 57.62 | -1.82% |

| CleanTech | 65.17 | -2.32% |

| Hydrogen | 50.21 | -2.41% |

Technology | ||

| Cybersecurity | 26.81 | 0.00% |

| Video Games/eSports | 91.8529 | -0.43% |

| Cloud Computing | 19.78 | -0.50% |

| FinTech | 25.45 | -0.62% |

| E-commerce | 28.15 | -0.98% |

| Sports Betting/Gaming | 19.0 | -1.85% |

| Electric Vehicles | 35.6588 | -1.93% |

| Robotics & AI | 37.66 | -2.16% |

| Semiconductor | 438.71 | -3.67% |

ASX TODAY

Frontier Digital Ventures Chair Patrick Grove and Executive Director Lucas Elliott disclose purchase of 4.5m shares each (FDV)

oOh!Media confirms receipt of non-binding indicative offer from PEP to acquire the company at $1.40 per share or a 64% premium to its last close (OML)

WHAT TO WATCH TODAY

Nickel: Zhejiang Huayou Cobalt plans to cut output at a major nickel plant in Indonesia by ~50% citing abnormal price volatility in sulfur prices. Nickel prices are up ~13% since 10-Apr and trading at the highest since June 2024.

Energy: S&P 500 Energy (+1.65%) edged higher, now up ~5% in the last seven sessions after suffering a 13% drawdown in the prior ~3 weeks. A lot of reluctance for energy equities to underwrite the current oil price environment. BP's Q1 profits more than doubled year-on-year to $3.2bn, comfortably ahead of $2.63bn ests, management attributed this to "exceptional oil trading contribution and stronger midstream performance. Net debt still up ~13% year-on-year, though largely due to working capital build.

Commodity softness: Classic oil up, base/precious metals down. A fairly heavy session for our overnight ETF watchlist, with Gold Miners, Uranium, Copper, Strategic Metals all down 3-4%.

BROKER MOVES

Life360 initiated Outperform with $32.20 target (Macquarie)

TechnologyOne downgraded to Neutral from Buy; target cut to $32 from $38.70 (UBS)

Whitehaven Coal upgraded to Neutral from Underweight; target up to $8.70 from $8.30 (JPMorgan)

Key Events

Stocks trading ex-dividend:

Wed 29 Apr: 360 Capital Mortgage REIT (TCF) – $0.05, Acrow (ACF) – $0.02, Gryphon Capital Income Trust (GCI) – $0.01, KKR Credit Income Fund (KKC) – $0.01, Waterco (WAT) – $0.07

Thu 30 Apr: Future Generation Australia (FGX) – $0.036, Metrics Income Opportunities Trust (MOT) – $0.012, Metrics Master Income Trust (MXT) – $0.014, Metrics Real Estate Multi-Strategy Fund (MRE) – $0.009

Fri 1 May: Wam Strategic Value (WAR) – $0.033

Other ASX corporate actions today:

Economic calendar (AEST):

11:30 am: Australia March Inflation (Ests: 4.8% vs. 3.7% in Feb)

11:45 pm: Bank of Canada Interest Rate Decision (Ests: Hold at 2.25%)