Morning Wrap: ASX 200 eyes sixth day of losses, S&P 500 and Nasdaq eke out another record high

ASX 200 futures are down 61 pts (-0.69%) as of 8:30 am AEST.

In this article

ASX 200 futures are down 61 pts (-0.69%) as of 8:30 am AEST.

In a nutshell:

S&P 500 (+0.12%) and Nasdaq (+0.20%) eked out another fresh all-time high, largely driven by Mag-7 strength

Dow (-0.13%) and Equal-weight S&P 500 (-0.12%) struggled for upside amid weakness from Staples, Real Estate, Discretionary, Healthcare and Materials

Nvidia (+4.0%) recorded a second straight all-time high, now up 31% since 30-Mar, though iShares Semiconductor ETF (-1.3%) snapped a historic 18-day win streak

Iran offers deal to US to reopen Strait and defer nuclear negotiations, Rubio says offer is not acceptable

Let's dive in.

Overnight Summary

Name | Value | % Chg |

|---|---|---|

Major Indices | ||

S&P 500 | 7,174 | +0.12% |

Dow Jones | 49,168 | -0.13% |

NASDAQ Comp | 24,887 | +0.20% |

Russell 2000 | 2,788 | +0.04% |

Country Indices | ||

Canada | 33,818 | -0.25% |

China | 4,086 | +0.16% |

Germany | 24,084 | -0.19% |

Hong Kong | 25,926 | -0.20% |

India | 77,304 | +0.83% |

Japan | 60,537 | +1.38% |

United Kingdom | 10,321 | -0.56% |

Name | Value | % Chg |

|---|---|---|

Commodities (USD) | ||

Gold | 4,688.93 | -0.43% |

Copper | 6.02 | -0.12% |

WTI Oil | 96.37 | +2.09% |

Currency | ||

AUD/USD | 0.7187 | +0.02% |

Cryptocurrency | ||

Bitcoin (USD) | 76,838 | -1.91% |

Ethereum (AUD) | 3,182 | -3.49% |

Miscellaneous | ||

US 10 Yr T-bond | 4.336 | +0.60% |

VIX | 18.02 | -3.69% |

US Sectors

Sector | % Chg |

|---|---|

| Communication Services | +0.94% |

| Financials | +0.65% |

| Information Technology | +0.46% |

| Utilities | -0.02% |

| Industrials | -0.03% |

| Energy | -0.25% |

Sector | % Chg |

|---|---|

| Materials | -0.51% |

| Health Care | -0.54% |

| Consumer Discretionary | -0.76% |

| Real Estate | -0.84% |

| Consumer Staples | -1.18% |

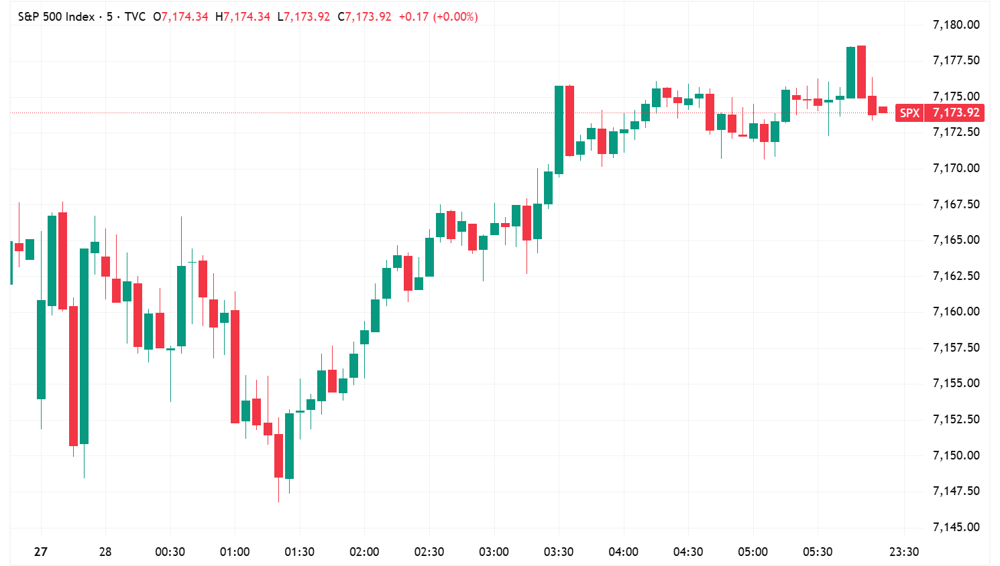

S&P 500 SESSION CHART

S&P 500 higher after a choppy open (Source: TradingView)

OVERNIGHT MARKETS

US benchmarks closed mixed, with the S&P 500 and Nasdaq grinding to fresh record highs in choppy trade after a soft open as the Dow lagged

Breadth was soft, with the Equal-weight S&P 500 (-0.12%) fading early gains of 0.45% amid softness from Staples, Real Estate and Discretionary

A relatively uneventful session ahead of a big week for corporate earnings (~42% of the S&P 500 and 5 Mag-7), FOMC on Thursday and still-volatile Iran headlines

Emerging-market equities hit a record high, with the MSCI EM Index up as much as 1.5% as TSMC surged 6% to a record. The gauge is up 16% year-to-date, three times the S&P 500's gain (BBG)

Busiest day of IG bond issuance since early March with Walmart, Intel and American Airlines all selling debt (BBG)

Short sellers more than double bets against US life insurance industry to >$5bn amid concerns about private credit exposure (RT)

Bill Ackman's Pershing Square IPO expected to raise ~$5bn (BBG)

ENERGY

Goldman Sachs lifted Q4 2026 Brent forecast to US$90 from US$80 a barrel and WTI to US$83 from US$75, citing "extreme" inventory draws of 11-12 million barrels per day in April (BBG)

IRAN

Iran submitted a new proposal via Pakistani mediators offering to reopen the Strait of Hormuz and end the war in exchange for the US lifting its blockade, with nuclear negotiations deferred to a later phase (AX)

Rubio says Iranian offer on the Strait of Hormuz is not acceptable (TI)

Iran's IRGC said it has no intention of unblocking the Strait of Hormuz (AJ)

STOCKS

Microsoft and OpenAI scrapped exclusivity, with Microsoft retaining a non-exclusive license to OpenAI IP through 2032 and ending revenue-share payments to OpenAI. OpenAI can now ship products on AWS and Google Cloud (BBG)

Qualcomm briefly surged ~8% after analyst Ming-Chi Kuo reported the chipmaker is partnering with OpenAI and MediaTek to develop smartphone processors, mass production targeted for 2028 (BBG)

Domino's Pizza Q1 FY26: revenue up 3.5% to $1.15bn, EPS $4.13 missed ests by 3.5%, US same-store sales rose just 0.9% vs. 2.7% ests, shares down 8.8% (RT)

Memory stocks rallied with Micron up 5% and Sandisk up 8% after Melius Research said the AI cycle should sustain memory demand through the decade (CNBC)

Eli Lilly threatened hospitals with "imminent loss" of 340bn discounted pricing unless claims data is submitted, prompting the AHA to urge HRSA action (AHA)

China halts Meta's $2bn acquisition of Manus, citing security concerns (CNBC)

TARIFFS & TRADE

Bessent says businesses working with Iranian airlines risk US sanctions, broadening the financial pressure campaign on Tehran (WSJ)

CENTRAL BANKS

Fed FOMC meeting kicks off Thursday at 4 am AEST, markets expect a hold at 3.50-3.75%, with traders pricing in less than one cut for all of 2026 amid Iran-driven inflation risks (MS)

Bank of Japan decision today, consensus expects a hold at 0.75% though ING sees a non-consensus hike risk after March core CPI accelerated to 1.8%, the first acceleration in five months (IVST)

ECB rate decision later this week, Lagarde signalled the bank is "ready to hike" if the Iran-driven inflation overshoot becomes large but "not too persistent," even as Eurozone composite PMI hit a 17-month low of 48.3 (CNBC)

ECONOMY

China industrial profits jumped 15.8% year-on-year in March and 15.5% in Q1, accelerating from 15.2% in January-February. Equipment manufacturing profits rose 21% and high-tech manufacturing 47.4% (BBG)

Chinese exports grew 14.7% year-on-year in Q1 in US dollar terms, the fastest pace since early 2022, supporting industrial profitability before the Iran shock fully feeds through (CNBC)

Industry ETFs

Name | Value | % Chg |

|---|---|---|

Commodities | ||

| Uranium | 56.7 | +2.51% |

| Strategic Metals | 100.95 | +2.42% |

| Lithium & Battery Tech | 84.95 | +1.38% |

| Steel | 101.69 | +0.13% |

| Silver | 68.33 | -0.67% |

| Copper Miners | 81.7 | -0.81% |

| Gold Miners | 92.59 | -1.85% |

Industrials | ||

| Agriculture | 27.57 | +0.66% |

| Construction | 107.997 | +0.46% |

| Aerospace & Defense | 216.04 | +0.11% |

| Global Jets | 25.53 | -1.81% |

Healthcare | ||

| Biotechnology | 169.02 | -0.45% |

Name | Value | % Chg |

|---|---|---|

Cryptocurrency | ||

| Bitcoin | 10.54 | -1.03% |

Renewables | ||

| Solar | 58.69 | +0.63% |

| CleanTech | 66.2966 | -0.50% |

| Hydrogen | 51.42 | -0.66% |

Technology | ||

| Robotics & AI | 38.49 | +3.02% |

| Cybersecurity | 26.81 | +1.21% |

| Cloud Computing | 19.88 | +0.81% |

| Electric Vehicles | 36.36 | +0.53% |

| Sports Betting/Gaming | 19.3579 | +0.07% |

| Video Games/eSports | 92.3204 | -0.14% |

| E-commerce | 28.43 | -0.63% |

| FinTech | 25.61 | -0.81% |

| Semiconductor | 455.41 | -1.34% |

ASX TODAY

European Lithium poised to announce $1.2bn bid from Nasdaq-listed Critical Metals Corp, offer price pegged at 58 cents per share vs. last close of 28 cents (AFR)

Fletcher Building to sell Fletcher Reinforcing and Wire business to United Industries for NZ$15.7m, expects to recognise loss on sale between NZ$20-23m (FBU)

Hyperion cops rare Morningstar downgrade (AFR)

WHAT TO WATCH TODAY

Calm before the storm: A relatively quiet overnight lead, ahead of a massive week for US earnings and central banks. Some softness for gold, a small bounce of uranium and continued strength in lithium. ASX 200 futures pointing towards a sixth straight day of declines as US sectors (ex-Tech) finished lower and Brent pushed back above US$100 a barrel. The Index is trading just ~0.5% above the key 200-day moving average. Interesting to note that in the last three sessions, the ASX 200 has managed to close 0.4-0.5% off session lows, so various heavyweight sectors like Banks and Miners have seen some dip buying activity. ASX 200 Financials Index down ten of the last eleven sessions, also approaching the 200-day.

BROKER MOVES

Webjet Group downgraded to Neutral from Buy; target cut to $0.62 from $0.72 (Goldman Sachs)

Key Events

Stocks trading ex-dividend:

Tue 28 Apr: Alternative Investment Trust (AIQ) – $0.034

Wed 29 Apr: 360 Capital Mortgage REIT (TCF) – $0.05, Acrow (ACF) – $0.02, Gryphon Capital Income Trust (GCI) – $0.01, KKR Credit Income Fund (KKC) – $0.01, Waterco (WAT) – $0.07

Thu 30 Apr: Future Generation Australia (FGX) – $0.036, Metrics Income Opportunities Trust (MOT) – $0.012, Metrics Master Income Trust (MXT) – $0.014, Metrics Real Estate Multi-Strategy Fund (MRE) – $0.009

Fri 1 May: Wam Strategic Value (WAR) – $0.033

Other ASX corporate actions today:

Economic calendar (AEDT):

1:00 pm: BoJ Interest Rate Decision