CBA, NAB, ANZ and Westpac clear the bar, but the easy gains may be behind them

All four majors beat expectations in February, but analysts see limited re-rating potential with P/E multiples near multi-year highs.

Source: iStock

Mentioned

KEY POINTS

- All four major banks beat consensus cash earnings forecasts by 4-11%, with bad debt charges significantly below expectations and consensus FY26-27 estimates upgraded by 2-5% following results.

- Valuations are a growing concern, with average price-to-earnings multiples around 21x and historical data showing RBA tightening cycles have consistently triggered de-ratings

- NAB is the preferred pick for both Macquarie and Morgan Stanley, while CBA and WBC are rated underweight by Morgan Stanley on valuation grounds, and ANZ is flagged as the value opportunity despite near-term revenue headwinds.

The Big Four Banks delivered a better-than-expected February reporting season, but analysts at Macquarie and Morgan Stanley are cautioning that elevated valuations and a shifting macro backdrop mean the sector's outperformance cycle could be drawing to a close.

Results were solid across the board

All four majors topped consensus expectations on cash earnings, with beats ranging from 4% to 11%. Revenue came in 0-4% ahead of forecasts, costs were roughly in line, and bad debt charges significantly undershot expectations, down 20-47% versus consensus estimates.

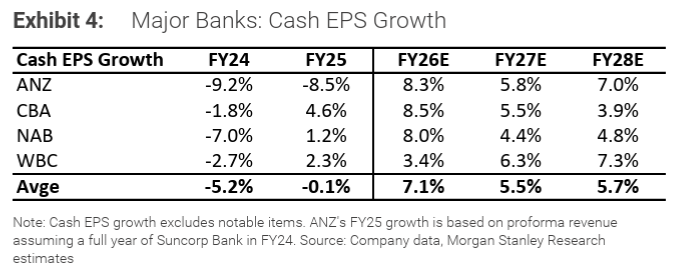

Following the results, consensus earnings forecasts for FY26 and FY27 were upgraded by 2-5%. Morgan Stanley now expects average cash EPS growth of 5-7% per year across the sector for the next three years, a marked turnaround from the earnings declines seen in FY24 and FY25.

Source: Morgan Stanley

Margins held up better than feared

Net interest margins were generally better than forecast, supported by replicating portfolio tailwinds, benign deposit competition, and favourable deposit mix trends.

Management commentary was notably less cautious. Westpac described current conditions as "a more stable environment for margins," while most banks flagged a moderation in business lending competition.

That said, both brokers expect margin pressure to become more of a story in FY27, as ANZ and WBC push to reclaim lost mortgage market share against a backdrop of dominant broker distribution and ongoing aggressive competition from Macquarie Group in both home loans and deposits.

Credit quality remains a bright spot

Loan loss ratios averaged just ~5 basis points across the majors in the December quarter, well below both historical averages and analyst estimates of around 7 bps. Non-performing loan trends improved at three of the four banks, consistent with a broader economic recovery and the lagged benefit of RBA rate cuts.

Both Macquarie and Morgan Stanley expect below-average loss rates to continue through FY27 and FY28, though Morgan Stanley flags that its macro team is forecasting a sharper economic slowdown from the second half of 2026, which could bring credit quality back into focus later this year.

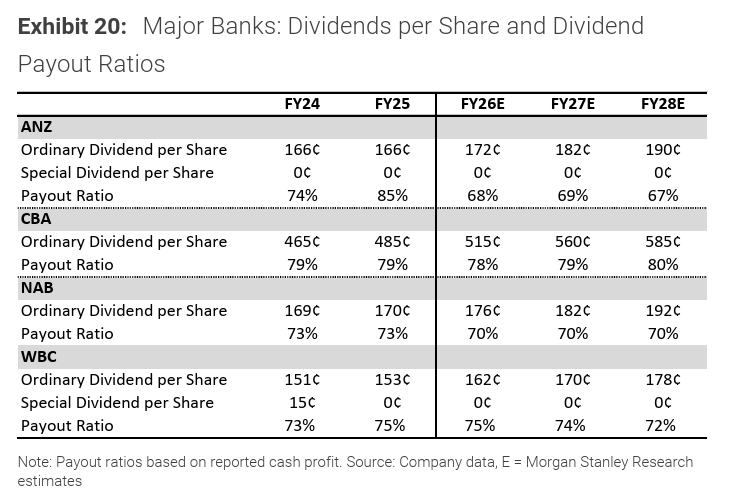

Capital and dividends

Organic capital generation improved across the sector, supported by stronger earnings. Macquarie has removed dividend cut assumptions from all four banks, though it now expects a partially underwritten dividend reinvestment plan for NAB in the second half of FY26.

Morgan Stanley estimates total capital buffers of $5-8 billion across the sector. However, it does not expect major capital management announcements in the near term. CBA and WBC buybacks remain subdued, and payout ratios are already near the top of target ranges. WBC could consider small special dividends, while ANZ may be positioned to announce a buyback in 2027 as its strategy delivers capital improvement.

Source: Morgan Stanley

Valuations are the key risk

The more pointed concern from both research houses is valuation. The average major bank price-to-earnings multiple is sitting at around 21x, roughly 5 points higher than it was at the start of the last two RBA tightening cycles. Historical analysis from Morgan Stanley shows that rate hike cycles have consistently triggered PE de-ratings:

6 points following 150 bps of hikes in 2009-10

3.5 points following 350 bps of hikes in 2022-23.

Superannuation funds have also been a significant buyer of bank shares, lifting their ownership to ~30.9% by September 2025 from ~27.9% two years earlier. APRA has flagged this concentration as a financial system risk it is monitoring.

Where analysts land on each stock

Morgan Stanley's order of preference:

ANZ (Overweight): Preferred pick despite revenue headwinds, due to its new management team's credibility on costs, improving capital trajectory, and a PE multiple of ~16x that looks cheap relative to peers

NAB (Equal-weight): Good margin and cost discipline, encouraging 1Q26 trends, but capital remains tight and a PE of ~19.5x leaves it exposed to a de-rating

WBC (Underweight): Sound operating trends, but market share ambitions cap upside on margins and costs, and the UNITE technology transformation adds execution risk

Commonwealth Bank (Underweight): Franchise strength is well recognised but already priced in, trading at ~27x FY26 earnings with limited capital management scope

Macquarie's preferred exposure is also NAB, while maintaining a neutral view on the sector overall. It sees near-term earnings risk skewed to the downside for ANZ and WBC, but more balanced at Commonwealth Bank and NAB.

The bottom line: Banks delivered a resounding beat this earnings season, with every key metric (revenue, net interest margins, costs, dividends, and credit quality) coming in ahead of expectations. The macro backdrop remains supportive, but much of the sector's re-rating appears to have already played out, with the ASX 200 Banks Index up 10.8% between February 10–20.