Australian house prices could still fall 10% despite RBA rates hold

The RBA paused, but another hike is still a risk, tax changes are biting, and according to expert views – house prices are set to fall.

Source: ChatGPT

Mentioned

KEY POINTS

- The RBA held its official cash rate at 4.35%, but their next move is highly contested with the experts split on another hike this year versus a possible 2027 rate cut.

- Housing faces a double hit – the budget's property-investor tax changes plus tighter interest rates – with major investment banks now tipping house prices are set to fall.

- This article discusses the rapidly changing environment for the Australian housing market and the ASX stocks facing earnings headwinds if the experts are right on an impending downturn.

On Tuesday, the RBA said it will leave the cash rate target unchanged at 4.35%, citing the hold will give it time to assess the response of the economy to previous rate hikes. While analysts are mixed on their timelines, many now predict cuts are on the table for 2027. The big question is: will this rate pause provide any relief?

Certainly, it’s been a challenging year for real estate, three consecutive rate hikes and a budget rife with tax reforms around property investment have dented investor optimism. The risks are real, and arguably, the most challenging in a generation.

This article discusses the rapidly changing environment for the Australian housing market, the latest expert views – including forecasts of imminent falls in housing values – as well as the ASX stocks that will almost certainly face earnings headwinds.

Latest expert calls in interest rates

In research notes responding to this week’s RBA meeting, the big investment banks were mixed in their views on the future path of official interest rates:

UBS forecast one more hike to 4.60% in August 2026. It then believes that the RBA will be forced into cuts in November 2027 and February 2028 as inflation moderates and the Australian economy slows.

Macquarie is less committed, keeping another hike as a “live risk” rather than a forecast. The bank also refrained from forecasting the timing of cuts, with an emphasis on "higher-for-longer."

Morgan Stanley expects no further hikes, with the RBA to hold in the near-term before cutting later next year.

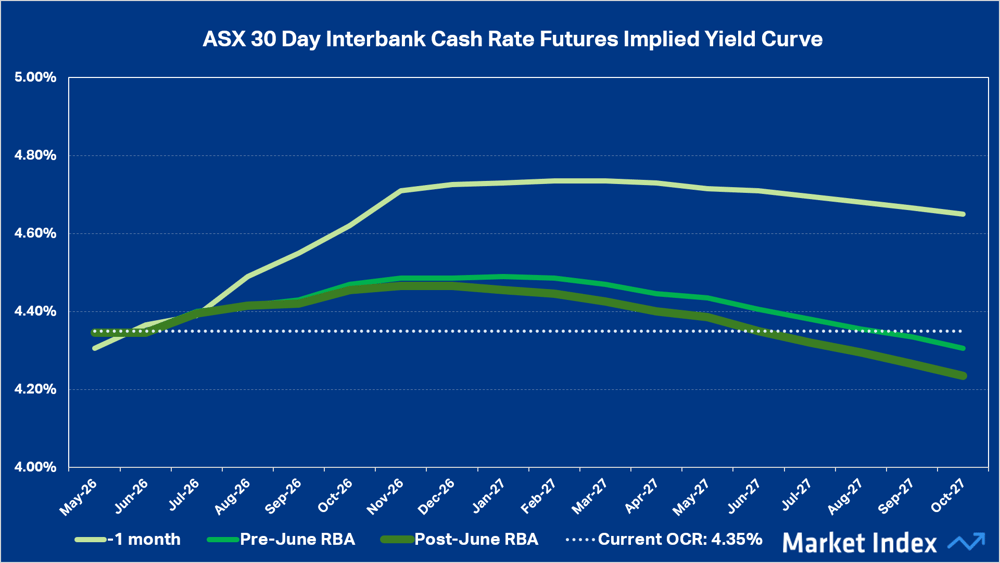

More broadly, the current ASX 30-day cash rate futures curve — an indicator of how the market expects the cash rate to change — shows the market growing more optimistic about rates staying as they are, with an increasing probability of a cut in the second half of next year.

Source: ASX, Market Index data.

How to interpret the ASX 30-day cash rate futures curve:

The curve is a schedule of where the market expects the RBA’s official cash rate (“OCR”) to be at the end of each month

A curve value >4.35% implies that the market sees at least some chance of another hike. One can calculate the probability of a hike as: (Curve Value — OCR) / 0.25% where 0.25% is a typical RBA OCR adjustment.

For Dec 2026, the curve value is 4.465%, meaning that the market is forecasting a (4.465% - 4.35%) / 0.25% or 46% chance of a 0.25% hike by the end of this year

For November 2027, the market is forecasting a 46% chance of a cut ((4.235% - 4.35%) / 0.25%).

Note how the curve has changed compared to before Tuesday’s RBA meeting (it has largely declined, indicating that the market is growing less concerned about another hike), and substantially from a month ago (when the market had viewed another hike before the end of this year as a certainty).

What the current rates outlook means for housing

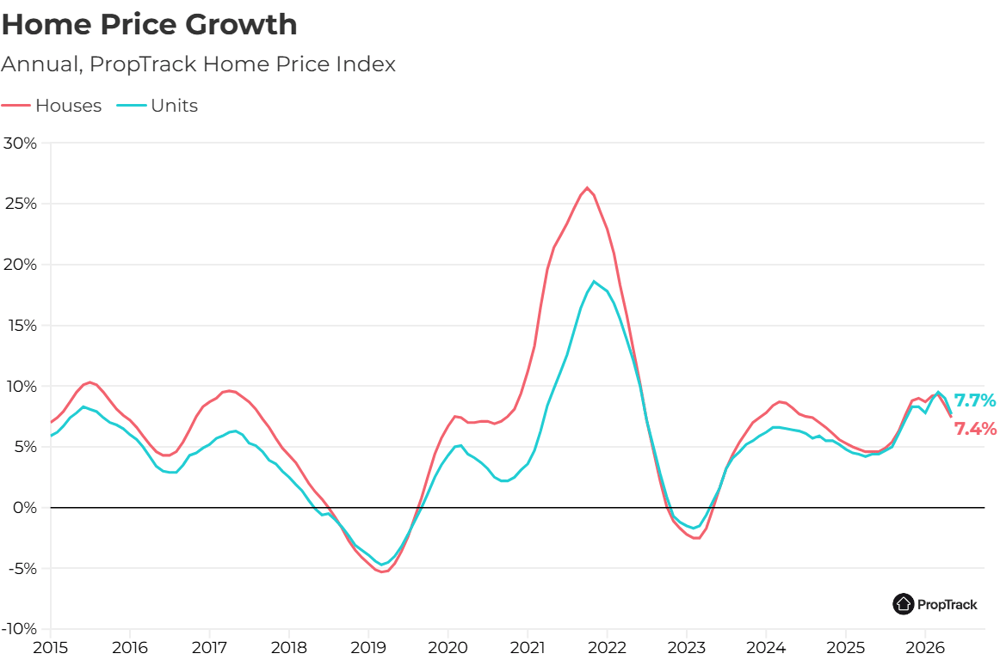

Average Australian house prices have been on a tear, rising 82% over the last 10 years. But that momentum appears to be slowing: according to data from PropTrack, national house prices fell 0.14% across April and May, and annual growth eased to 7.8% from 9.4%.

Source: PropTrack, from realestate.com.au

The experts believe the pullback has only just begun. According to UBS, the near-term outlook for Australian housing is clearly negative, with two headwinds meeting at once: the budget's tax changes targeting property investors and an expected RBA hike to 4.60% in August. UBS sees dwelling prices falling around 3–5% over the coming year, while home loan values could slump roughly 30% as prices fall and sales dry up.

Morgan Stanley thinks there will be a sharper housing downturn, with national prices expected to fall 5-10% and turnover down 20-30%, creating downside risk to FY27 discretionary earnings.

Negative housing to hit ASX consumer sector

The fallout from a slowing housing market is likely to impact residential property developers like Mirvac Group (MGR), Cedar Woods Property (GWP) and Stockland (SGP) as demand slows from investors. According to a recent Morgan Stanley research note, the impending housing slowdown is also likely to impact consumer stocks. The investment bank notes that there’s a direct link between fewer houses being bought and decorating and buying new appliances.

This link has moved Morgan Stanley to downgrade the entire ASX consumer sector from ‘in-line’ to ‘cautious’, noting housing-exposed discretionary retailers in particular (e.g., hardware and big-ticket) face genuine earnings risk. The investment bank cut its price targets for the stocks below, and explained why it believes these four are most likely to be in the firing line:

Wesfarmers (WES) — Rating: Equal-weight, Price Target $79.30 (from $78.70). Bunnings is the big exposure, but Kmart and WESCEF offset the drag. WES is held back by a full valuation.

Metcash (MTS) — Equal-weight, Price Target $3.40 (from $3.20). More trade-exposed than Bunnings, so more vulnerable, but downside likely limited as risks are already reflected in the valuation.

JB Hi-Fi (JBH) — Underweight, Price Target $68.80 (from $66.50). Hit by weaker electronics and appliance demand, plus memory-chip cost inflation. Valuation above mid-cycle averages means it still looks expensive.

Harvey Norman (HVN) — Equal-weight, price target $5.40 (from $4.70). Most tied to housing categories, similar challenges to JBH on electronics, however unchallenging valuation “limits absolute downside”.

Bottom line for investors: Housing exposed retailers face real earnings risk because of the uncertain housing market.

Looking forward – data points to watch

Though the cash rate hike pause offers welcome reprieve for homeowners with mortgages, there is still a real possibility of further tightening in monetary policy. According to RBA Governor Bullock: "If expectations of higher costs become embedded, it will lead to higher and more persistent inflation and it would require even more tightening in monetary policy to get it under control."

The experts foresee house prices falling up to 10%, and the latest data for April and May points to a slide having already begun. The next RBA meeting is in August, where we will see if inflation has slowed enough for them to settle the case for another hike – or confirm the market's growing bias towards a prolonged hold. Reporting season kicks off in just a few weeks, too, and this is where we’ll start to see the impact of recent developments on stocks exposed to housing.