ASX reporting season: Four metrics you must look out for

Guidance, earnings, margins and dividends are what drive share prices during reporting season. Everything else is noise.

Source: Shutterstock

Mentioned

KEY POINTS

- Macquarie analysis found company guidance versus consensus is the best indicator of share price reaction during reporting season, more correlated than any other fundamental factor

- Earnings, margins and dividends are equally important secondary metrics after guidance, with results that beat or miss across multiple factors typically seeing the strongest share price reactions

- Stocks with clean beats across earnings, margins, dividends and guidance tend to rally sharply, while broad misses across these metrics typically result in sustained selloffs

When results land, what matters most? The CEO praising a "strong" performance, the headline profit number, or whether it beat analyst forecasts?

You should focus on how reported numbers compare against analyst expectations every single time. The last thing you want is to think "wow, this looks strong" only to watch the stock open sharply lower and spend the whole day trending down.

It happened this morning with Credit Corp's (ASX: CCP) first-half FY26 result. Here are some excerpts from the announcement:

US collections up 23% year-on-year

Record lending volume and 7% loan book growth over the half year

Strong growth in the Australia and New Zealand debt ledger investment pipeline to $120 million

NPAT of $44.1 million was in-line with the prior year ... reflected reduced earnings in the first half arising from strong loan book growth and disruptions to the ANZ purchased debt ledger

Both these factors will produce higher second half earnings, and the company reaffirms its full-year NPAT growth of 6-17%

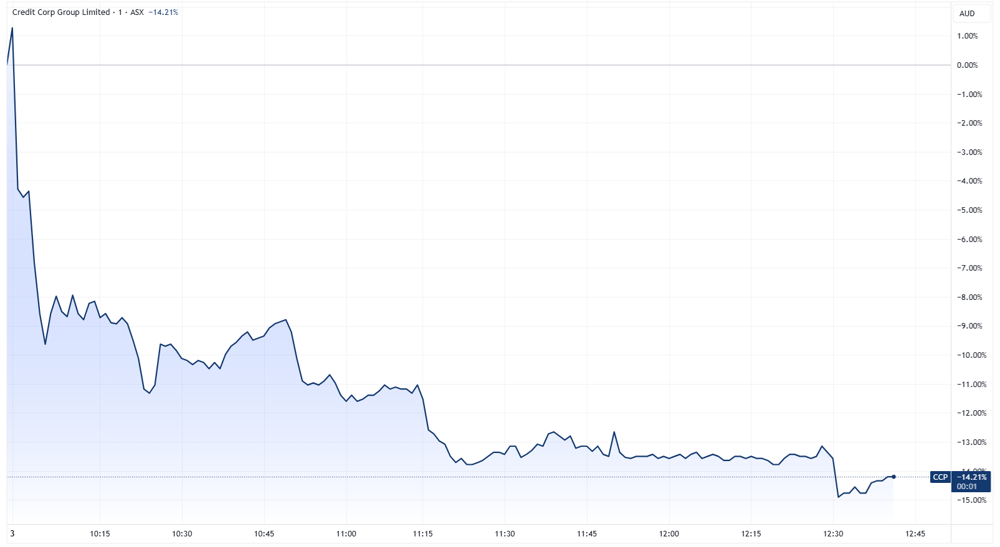

Credit Corp opened 1.7% higher but traded down in a straight line from there.

Credit Corp intraday price chart (Source: TradingView)

In reality, Credit Corp's first-half FY26 missed market expectations on the metrics that matter:

Revenue up 4% to $283.6m vs ests $277.5m (2% beat)

NPAT flat at $44.1m vs ests $48.9m (10% miss)

Interim dividend flat at 32 cps vs. Morgan ests of 35.5 (12.3% miss)

The company reaffirmed its FY26 guidance of $100-110 million net profit after tax, under the premise that strong loan book growth will produce higher second half earnings. A glass half empty view is that the second half must do the heavy lifting, otherwise the company will downgrade its FY26 guidance in the not too distant future.

The net outcome was negative, with earnings and dividends missing by sizeable margins alongside execution risks heading into the second half.

If you thought the result read well and bought the open, you'd be down almost 15% by noon.

Metrics that matter

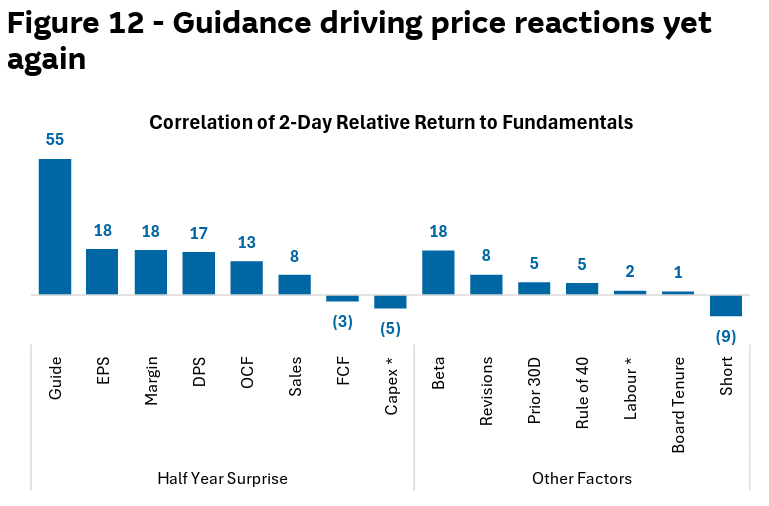

A September 2025 note from Macquarie found that "how company guidance compares to consensus is the best indicator of the share price reaction [over reporting season]."

The analysts observed that guidance was more correlated than "any other fundamental factor we track over reporting season."

Other metrics that were equally important (but less than guidance) were earnings, margin and dividends.

Source: Macquarie Research, August 2025

In other words, if a company reports a clean sweep of better-than-expected earnings, margins and dividends alongside above consensus guidance, there's a good chance the stock opens sharply higher and continues to run both intraday and over the short term.

Clean beats and misses

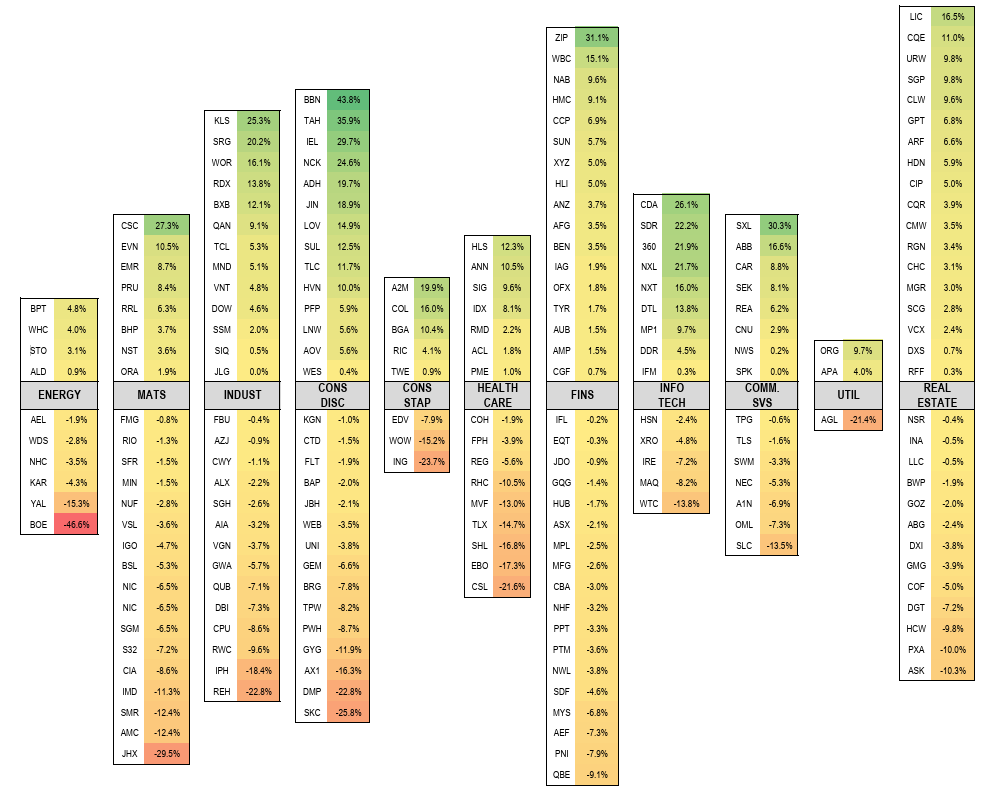

The table below shows post-result share price moves for various S&P/ASX 200 companies from August reporting season.

Source: UBS

We'll look at some stocks towards the tail end of the chart as those big share price movers tend to highlight the most notable beats and misses.

Kelsian (+25.3%): FY25 revenue, NPATA and full-year dividend was 0.9%, 6.1% and 2.9% ahead of market expectations. FY26 underlying EBITDA guidance of $297-310m was 1% ahead of $301m ests at the midpoint. Management highlighted near completion of the peak capex investment, with proforma leverage reduced to 2.7x and expected to fall to 2.0-2.5x by June 2026.

Reece (-22.8%): FY25 revenue was a 2% beat, NPAT down 24% year on year to $317m vs $323.2m ests (2% miss), total dividend was a 5% beat. No specific guidance, but management warned: "Looking ahead we anticipate a slow recovery in ANZ with a period of soft activity still to play out. In the US, we expect the housing market to be constrained for the next 12-18 months driven by persistently high mortgage rates and affordability challenges."

Domino's (-22.8%): FY25 underlying NPAT fell 2.8% to $117m vs $118.1m ests (1% miss), total dividend of 77 cps was a sizeable 27% miss vs UBS expectations of 106 cps. Same store sales fell 0.2% year on year compared to expectations of 0.2% growth. No guidance, but same store sales further decelerated in the first seven weeks of FY26 to -0.9%.

Coles (+16.0%): NPAT and total dividend beat expectations by 6.3% and 7.8% respectively, with the trading update highlighting 4.9% revenue growth in the first eight weeks of FY26 (which was also double Woolworths' trading update).

Inghams (-23.7%): Still struggling after losing a major Woolworths contract in February 2025. Management flagged earnings were "impacted by a shift to a lower-margin mix, weaker wholesale pricing and softer overall retail demand, all of which contributed to a meaningful deterioration in 4Q25 earnings." FY25 NPAT and dividend missed by 7.9% and 6.9%, respectively. FY26 guidance was no better, with underlying EBITDA of $215-230m vs UBS estimates of $258m.

It gets repetitive after a while, but as you can see, big rallies are characterised by a clean beat along with company-specific positives such as Kelsian highlighting declining leverage and Coles reporting better-than-expected revenue growth in the first eight weeks of FY26. Sharp selloffs were driven by broad misses across key metrics, along with downbeat commentary/guidance.

Our Live Blog highlights most of these beats/misses before the market opens (E.g. Zip's beat and Ingham's miss was flagged on the 22nd August blog)

The bottom line

Reporting season throws a mountain of numbers and commentary at us. To keep things simple, focus on what's important: guidance, earnings per share, margin and dividends. Everything else is secondary.