ASX dividend stocks: A 5-7% yielder that's only had two bad months since 2024

DBI posted a 54% total return in 2025 with just one red month. Here's why its unique business model provides unmatched earnings certainty.

Source: Shutterstock

Mentioned

KEY POINTS

- DBI's business model provides unmatched earnings certainty by charging fees on contracted capacity regardless of coal volumes shipped through its terminal

- Recent debt refinancing cut borrowing costs from ~350 bps to 150-200 bps, adding $15 million in annual cashflow and potential dividend upside of 3 cents per share, according to Macquarie

- The stock's dividend yield acts as a price floor, with higher yields attracting buyers whenever the share price dips materially below recent trading ranges

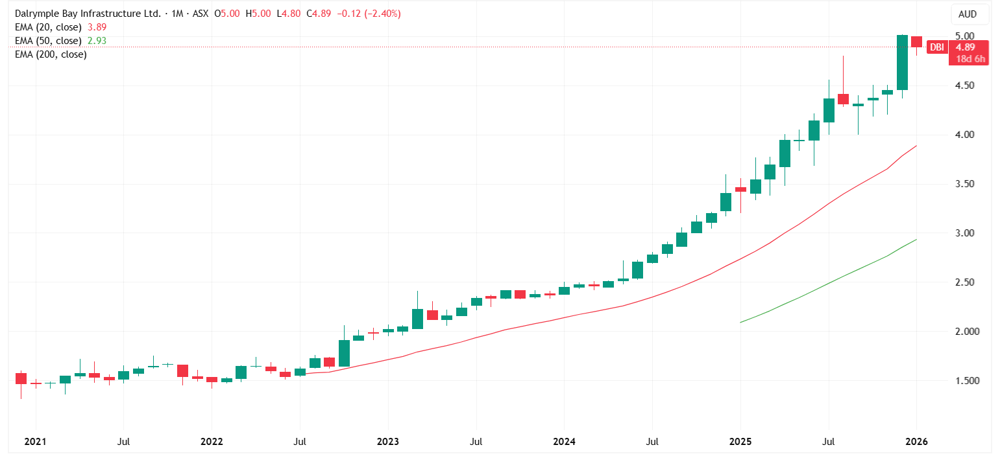

Dalrymple Bay Infrastructure (ASX: DBI) closed out 2025 with a 47.1% share price gain plus 24 cents in dividends – a yield of around 7%. The stock had only one down month during the year, which coincided with its FY25 result and ex-dividend date in August. Looking back over the past two years, it's posted just two red months total.

Dalrymple Bay Infrastructure monthly chart (Source: TradingView)

DBI has one of the most fascinating business models out there, which is why I revisit the company from time to time.

DBI in a nutshell

DBI operates the Dalrymple Bay Terminal (DBT), the lowest cost export pathway for Bowen Basin mines. It services some of the world's largest coal names including Peabody Energy, Stanmore Resources and Whitehaven Coal.

Since beginning operations, DBT has undergone seven phases of expansion, growing from 14.5Mtpa in 1983 to its current nameplate capacity of 85Mtpa. It doesn't own the terminal outright but holds a 99-year lease (50 years initial, plus a 49-year option) from the Queensland Government.

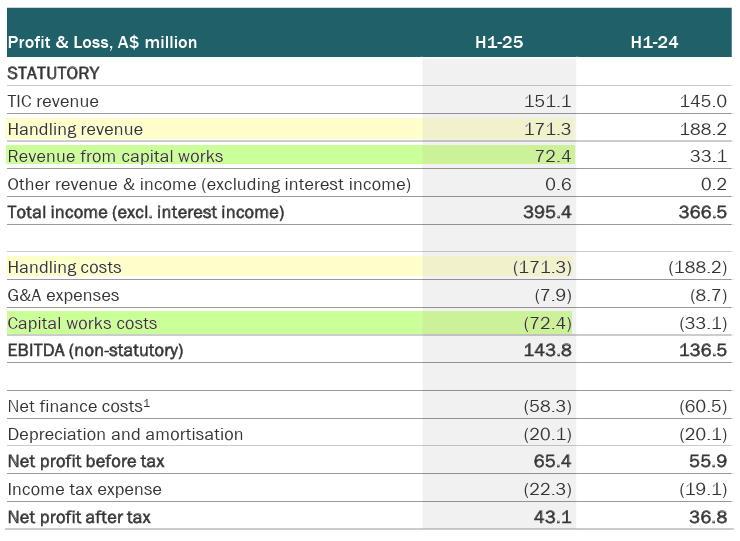

What makes DBI interesting is its business model, which becomes clear when you look at its profit and loss statement. Specifically, two pairs of offsetting line items.

In its latest result (1H25), $171.3 million in "Handling revenue" is offset by $171.3 million in "Handling costs," while $72.4 million in "Revenue from capital works" is offset by $72.4 million in "Capital work costs."

Source: Dalrymple Bay Infrastructure half-year FY25 results presentation

What this really means is:

Handling revenue: DBI passes all operating and maintenance costs straight to customers. Handling revenue always matches handling costs.

Revenue from capital works: DBI funds Non-Expansion Capital Expenditure (NECAP) projects, like safety upgrades or equipment replacements, with its own cash or debt. These costs are capitalised and recovered over time through price hikes, including a return tied to bond yields. Revenue from capital works equals capital works costs.

The line item at the very top TIC revenue is the company's core revenue stream, a fee charged per tonne of coal capacity contracted at DBT.

So regardless of tonnes exported, DBI receives the TIC on every tonne of the terminal's annual contracted capacity of 84.2mt. Despite current historically low coal prices, the mines shipping through DBT have long mine lives and sit predominantly in the bottom half of the global cost curve, meaning they remain generally profitable at these prices. What we're effectively left with is earnings certainty that is second to none.

Earnings visibility provides share price support

DBI is predominantly known as a dividend stock that has historically paid its distributions on a quarterly basis. Given its earnings visibility, it's hard for the stock to fall too much, as a lower share price would make its dividend yield increasingly attractive.

On 20 May 2025, DBI announced a dividend guidance for FY26 of 24.5 cents per share. Back then, the stock was trading at $3.95, implying a dividend yield of 6.2%.

In June 2025, DBI's largest shareholder Brookfield Infrastructure offloaded $428 million worth of stock (~23% of the company) in a block trade priced at $3.72 or a 7.9% discount to its last close. This resulted in a 6.2% selloff to $3.69 on the day of the announcement (12-Jun-25) but improved the dividend yield from 6.2% to 6.6%.

Funnily enough, DBI recovered the entire selloff over the next eight sessions. But imagine if the news had driven a more persistent selloff and dragged the stock to $3.50. That would have bumped the yield up to 7.0%.

Given the business model and earnings certainty mentioned above, it's hard to believe a scenario where the stock sells off to allow for such a market leading yield.

Where to from here?

DBI took another leg up in December after refinancing its 2020 debt and establishing $1.07 billion in new facilities.

The cost of future borrowing dropped materially as additional debt previously carried risk margins above 350 bps. That's now 150-200 bps, making all future NECAP financing significantly cheaper and lifting long-term value.

The refinancing adds around $15 million in annual cashflow over the next five years, potentially adding $0.03 per share to dividends, according to Macquarie. DBI could also refinance residual debt for further upside.

It might not sound like much, but DBI shares rallied 6.3% on the day of the announcement (10-Dec-25) to a fresh all-time high of $4.83. The stock has continued to trade around those levels, which means its dividend yield is hovering around the lower bound of recent ranges, about 5.0%.

Nevertheless, Macquarie analysts remain bullish on the stock, with last month's note highlighting: "We think DBI is a unique investment with dividend growth of 5% and a valuation EV/EBITDA multiple of 13x, which is below comparable port multiples."

Given DBI's earnings certainty, perhaps a better way to value the stock is by looking at its current dividend yield (be wary when yields are high and opportunistic when they're low).