ASX Big 4 Banks: What’s in store for ANZ, CBA, NAB and WBC?

CBA plunged after its results, yet WBC rocketed! What’s going on with the big ASX banks and are the experts thinking buy, hold, or sell?

Source: Shutterstock, Market Index

Mentioned

KEY POINTS

- The Big 4 ASX banks of ANZ Group (ANZ), Commonwealth Bank of Australia (CBA), National Australia Bank’s (NAB), and Westpac Banking Corp. (WBC) are cornerstones of most Aussie investors’ portfolios.

- Three of the Big 4 are in the process of providing critical market updates to investors, and their results are shaping investor opinion and stock prices alike.

- We review the latest major broker views on the Big 4 ASX banks, their latest ratings and target prices, as well as run the ruler over their all-important charts.

Priced for perfection. Overvalued. Unsustainable. Would rather stick pins in my eyes than buy (yes, that’s an actual fund manager statement!). The Big 4 Bank stocks of the ASX have both confounded and frustrated local fund managers for the better part of two years now with their strong collective share price performances.

Amidst burgeoning market capitalisations – thrusting Commonwealth Bank of Australia (CBA) to number one spot on the ASX’s biggest company list with a market capitalisation of over $300 billion at one point – three of Big 4 are in the process of updating investors on their recent progress. CBA was trounced yesterday after reporting its FY25 results, yet Westpac Banking Corp. (WBC) has rocketed today on the back of its third-quarter update.

With National Australia Bank’s (NAB) third-quarter update due Monday, let’s check in with the latest broker calls on the Big 4 to see if the experts are presently calling buy, hold, or sell. We’ll also review the key details of CBA’s update, and I’ll even do a little technical analysis to help you decide whether the Big 4 are still on the right side of the broader market. Let’s dive in!

The mighty has fallen, is CBA still the momentum leader?

In a ChartWatch ASX Scans article I wrote earlier in the week, I noted that when it comes to share price momentum, CBA has transformed from sector leader to sector laggard. The other 3, ANZ, NAB, and WBC (plus smalls Bank of Queensland (BOQ) and Judo Capital (JDO)) had each reprised their places in my Uptrends Scan List after a period of consolidation through the middle of the year. CBA was – and after Wednesday’s 5% post-earnings decline – remains the laggard.

%20chart%2014%20August%202025.png)

Commonwealth Bank of Australia (CBA) chart (click here for full size image)

{kind=link}

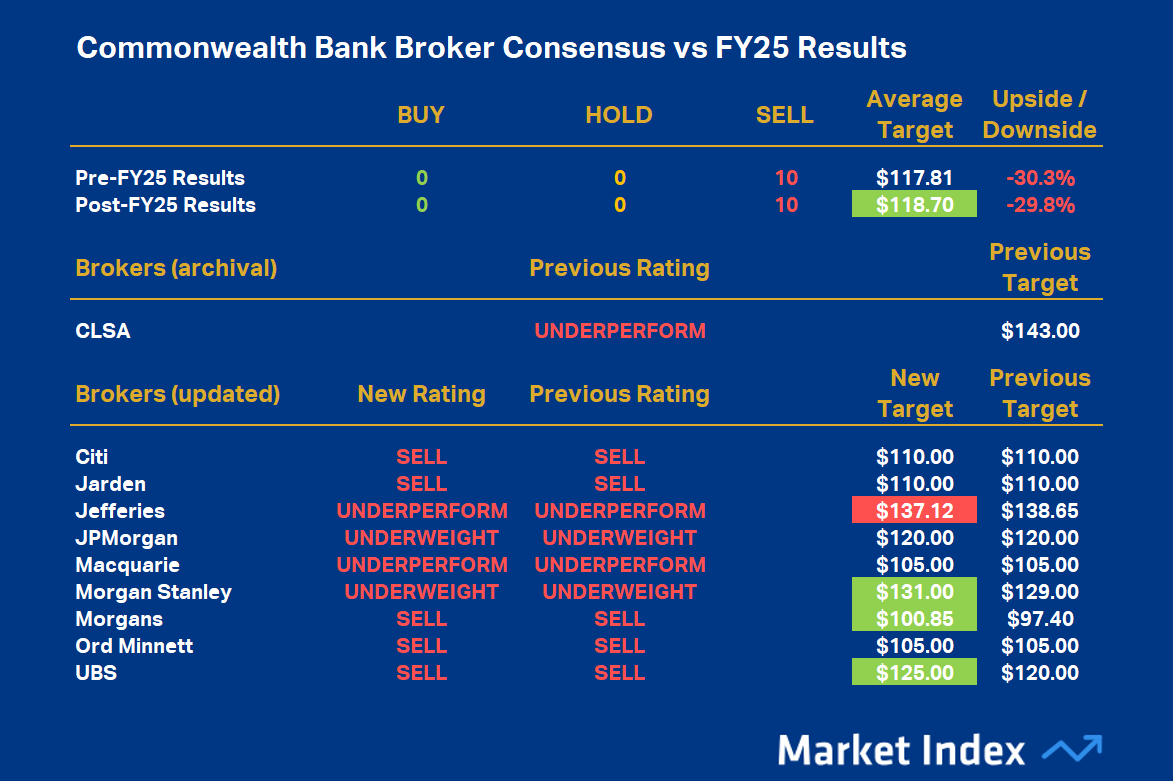

This is what the big brokers had to say about CBA’s FY25 results:

Jarden (Rating: Sell | Target Price: $110)

We see the result as just OK (albeit helped by below the line inclusions and good fortune in markets), growth is limited and returns are stable. Balance sheet is clearly well-managed and the higher dividend should please.

This is unlikely to drive material positive consensus earnings revisions.

CBA's exalted valuation (30x P/E Ratio / 4x Price to Book Value) appears to us more a function of non-fundamental flows and YFYS rebalancing increasing stock inelasticity than superior growth and return. We expect this makes it especially vulnerable to a slight miss and mean reversion.

JP Morgan (Rating: Underweight | Target Price: $120)

Overall, a consistent and strong full-year result with few surprises and we would expect immaterial changes to consensus forecasts.

NIM which at 2.08% was stable, but we expect pressure to re-emerge in 1H26 given the equity hedge benefit has ended and rate cuts will exert modest pressure.

CBA remains very expensive, trading on 28.6x FY26 P/E Ratio and 3.8x Price to Book Value for a 13.5% Return on Equity.

Macquarie (Rating: Underperform | Target Price: $105)

CBA delivered a broadly in-line result, but underlying trends were weaker.

Rate cuts present challenges for earnings, but CBA is focusing on the long-term increasing investment further above peers.

With earnings momentum turning and trading at ~28x FY26 forecast P/E Ratio, we believe reality will need to return to valuations.

Morgan Stanley (Rating: Underweight | Target Price: $131)

An inline result in terms of earnings, capital position, and dividend, with few positive surprises.

Doubt’s CBA’s ability to deliver on the market’s present high valuation, meaning there is little room for operational missteps

UBS (Rating: Underperform | Target Price: $105)

A strong wholesale banking result overshadowed weakness in retail division, but otherwise it was a broadly inline result.

CBA is best in class and deserves to be viewed as the ASX’s premier bank, but headwinds on costs and potential impacts on margins temper the near-term outlook.

Despite its positives, CBA remains too expensive in the broker’s view, as the current share price is detached from the fundamentals.

It seems that quality and best in class only goes so far with the experts – they generally agree that CBA is a great bank, it has a strong position in the Australian market, an excellent balance sheet, and is a consistent performer – but it’s just too darned expensive.

Well, the experts have been telling us CBA is expensive for a long time now – with near-unanimous sell ratings on CBA for over 12 months – which means that apart from its recent pullback, they’ve been very wrong. If you’d followed their collective advice and sold CBA 12 months ago, you would have missed out on a 30% return – more than double the ASX 200’s over that time (and don’t forget that much of the benchmark’s return was because of CBA!).

Here's the full, current broker consensus table for CBA (i.e., not much has changed!):

Commonwealth Bank of Australia (CBA) Broker Consensus (click here for full size image)

{kind=link}

For all of the stocks covered in this article, to obtain a Broker Consensus Rating, we assign a Rating Value of +1 to any broker rating better than HOLD/NEUTRAL/MARKETWEIGHT; a Rating Value of 0 for any broker rating equivalent to HOLD/NEUTRAL/MARKETWEIGHT; and a Rating Value of -1 to any broker rating worse than HOLD/NEUTRAL/MARKETWEIGHT.

We then take the average of all Rating Values and assign a Broker Consensus Rating of BUY to values +0.5 or above; a Broker Consensus Rating of HOLD for values between -0.5 and +0.5; and a Broker Consensus Rating of SELL for values -0.5 or below.

The Broker Consensus Target is simply the average of the target prices we have on file for each broker. Typically, brokers define their target price as a 12-month forecast, and each target price is based on a broker’s fundamental valuation assumptions. We have only assessed broker ratings and target prices within the last 3 months to account for recent relevance.

CBA’s average Rating Value is -1.0, resulting in a Broker Consensus Rating of SELL. This is unchanged from its prior average Rating Value of -1.0 and Broker Consensus Rating of SELL.

CBA’s Broker Consensus Target is $118.70 (up 0.8% from $117.81 prior to its FY25 results). This suggests brokers collectively believe the stock is around 29.8% overvalued based upon the closing price on Wednesday, 13 August of $169.12.

The best of the rest

WBC’s, and indeed the other big banks ANZ, and NAB, appear to be rebounding strongly after they followed CBA down on Wednesday. This is a pleasant surprise for me, as it confirms the resumption of their respective prevailing short term uptrends – and therefore their respective places in my Uptrends Scan List.

ANZ Group chart (click here for full size image)

{kind=link}

%20chart%2014%20August%202025.png)

National Australia Bank (NAB) chart (click here for full size image)

{kind=link}

%20chart%2014%20August%202025.png)

Westpac Banking Corp. (WBC) chart (click here for full size image)

{kind=link}

I don’t do ratings and price targets: My view is the trend. Uptrend equals happy to consider owning it (assuming it’s the best opportunity right now – and there are many opportunities based on my daily scans), versus Downtrend equals wouldn’t consider owning it / likely happy to short it.

I think ANZ, NAB, WBC, BOQ and JDO are currently in uptrends, make of that what you will. CBA is neutral (short term downtrend versus long term uptrend). Also understand that if any of those trends change tomorrow, my view will change accordingly. What I can say is that during the periods on the above charts where you see double green trend ribbons, my view was roughly the opposite of the big brokers!

As for those big brokers, here’s where they currently stand on the rest of the Big 4:

%20Broker%20Consensus%20vs%20FY25%20Results.png)

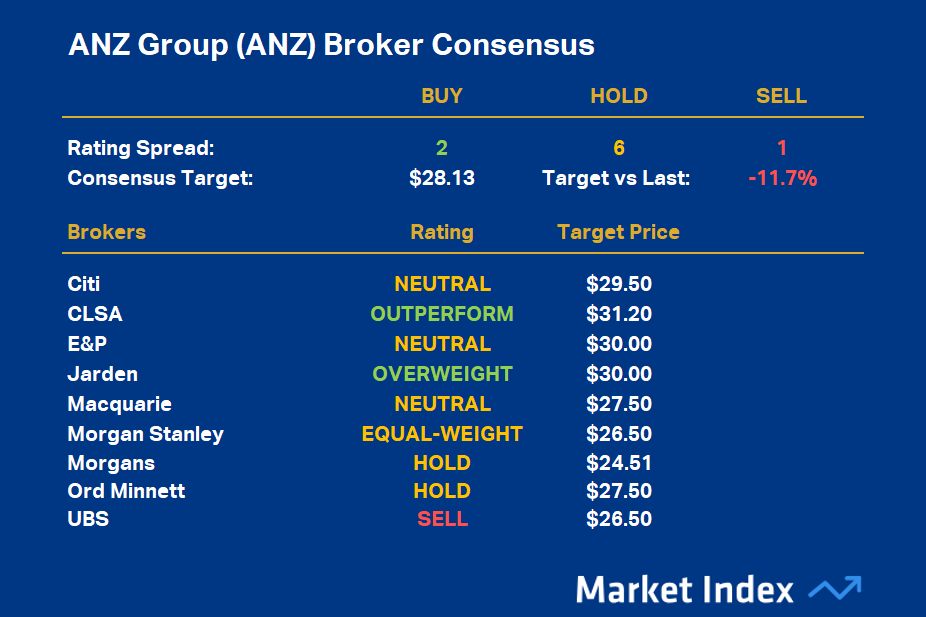

ANZ Group Broker Consensus (click here for full size image)

{kind=link}

ANZ’s average Rating Value is -1.0, resulting in a Broker Consensus Rating of SELL. ANZ’s Broker Consensus Target is $118.70. This suggests brokers collectively believe the stock is around 29.8% overvalued based upon the closing price on Wednesday, 13 August of $31.87.

%20Broker%20Consensus%20vs%20FY25%20Results.png)

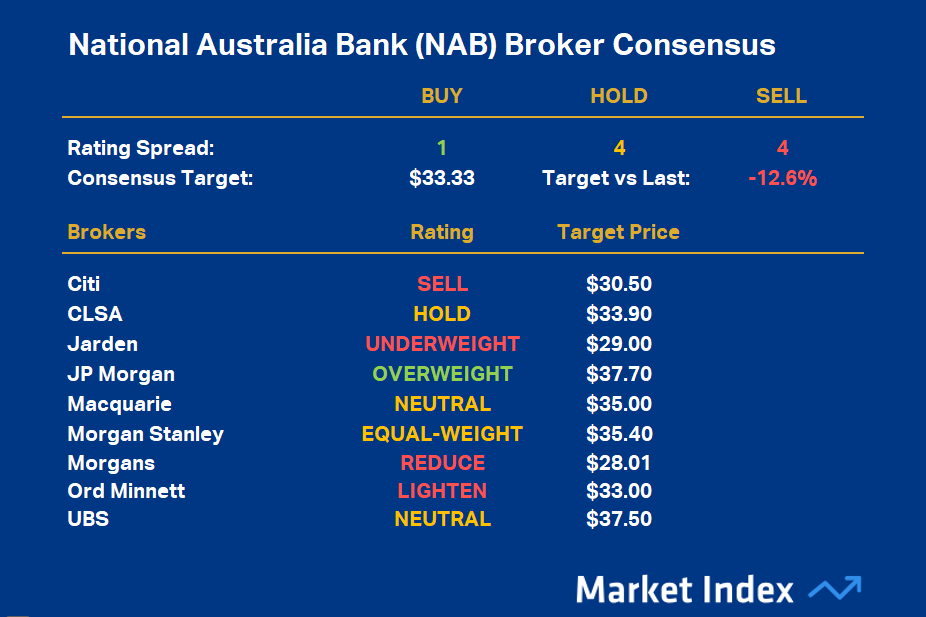

National Australia Bank (NAB) Broker Consensus (click here for full size image)

{kind=link}

NAB’s average Rating Value is -0.33, resulting in a Broker Consensus Rating of HOLD. NAB’s Broker Consensus Target is $33.33. This suggests brokers collectively believe the stock is around 12.6% overvalued based upon the closing price on Wednesday, 13 August of $38.16.

%20Broker%20Consensus.png)

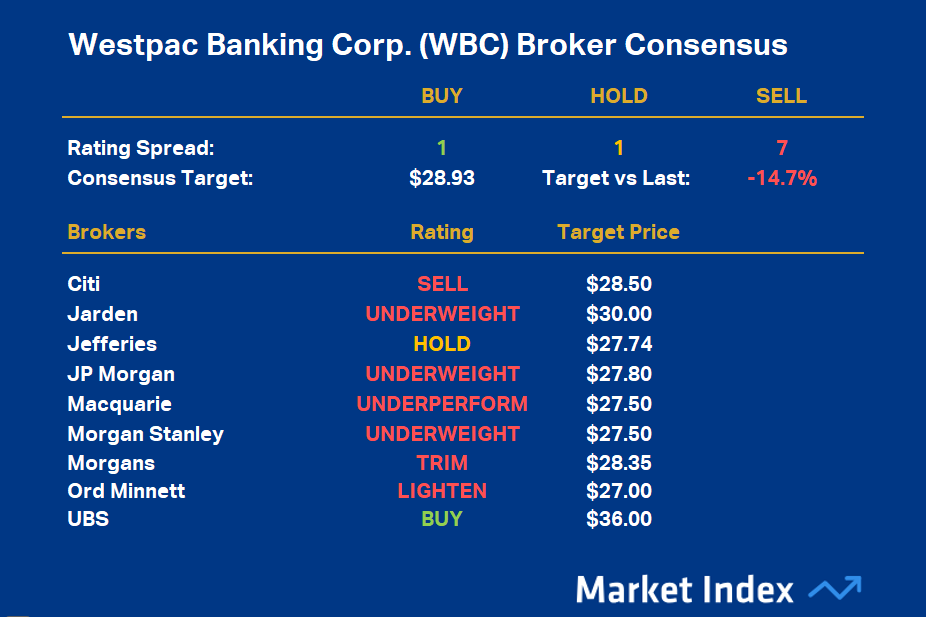

Westpac Banking Corp. (WBC) Broker Consensus (click here for full size image)

{kind=link}

WBC’s average Rating Value is -0.67, resulting in a Broker Consensus Rating of SELL. WBC’s Broker Consensus Target is $28.93. This suggests brokers collectively believe the stock is around 14.7% overvalued based upon the closing price on Wednesday, 13 August of $33.90.

A table for those who just love stats

I know that when it comes to the big banks, many don’t really care what the big brokers or the charts say, they just love getting big, fat dividend cheques every 6 months. Maybe for some, they want to see which bank has the lowest P/E Ratio (i.e., potentially therefore representing best value for that dividend yield). For everyone who just loves the stats, here’s the latest comparison table with forward estimates courtesy of Morgan Stanley:

Big 4 Banks 1-year forecast dividend and 1-year forward P/E Ratio. Data source: Morgan Stanley, based on closing prices 13 August 2025.

Conclusion: Beauty is in the eye of the beholder 😍

The best thing about the market is that everyone gets a say. If you like a stock, you’ll buy it. Most likely, though, you’ll be buying it from someone who doesn't like it (think about that for a second…why don't they like it!?). All is fair in love and war – and this is especially true in the markets!

At the end of the day, if more money is trying to get into a stock than is trying to get out, its price is probably going to go up, and vice versa. The brokers have their view, I have my view, and I hope by pulling together some of the threads above, I’ve helped you form your view.