ASX 200 Live Today - Wednesday, 7th January

The S&P/ASX 200 is set to rally as commodity markets continue to heat up. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Wednesday, January 7. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

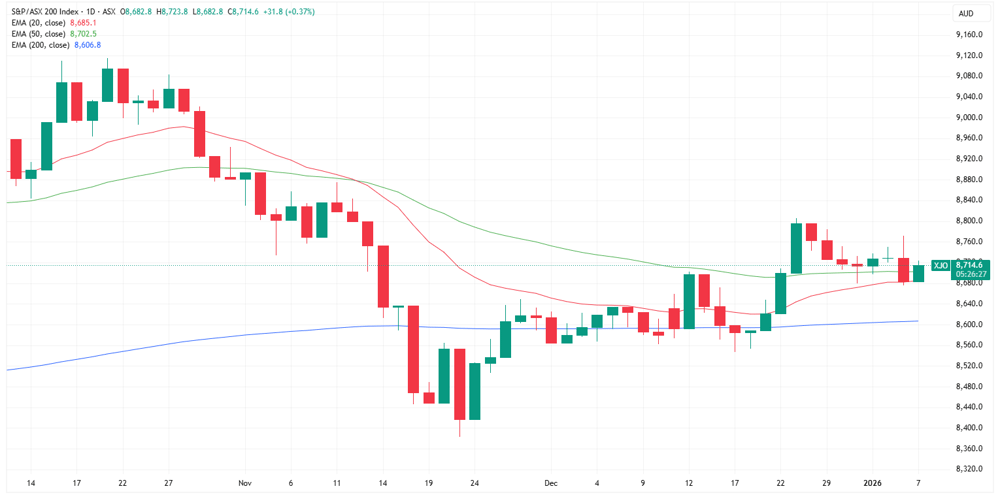

ASX 200 higher as tech and staples bounce

[2:10 pm] ASX 200 currently 0.30% higher in a relatively sideways session. Not much movement at the index level besides a brief rip and dip after the cooler-than-expected CPI print at 11:30 am.

A few sectors up a solid today, notably Tech (+1.86%), Staples (+1.32%), Materials (+1.25%) and Healthcare (+0.89%). But when you look at their daily charts, they've all been solid to oblivion (ex-Materials).

XHJ down 27% since late August and bouncing from the lowest level since June 2019 (though this is largely due to CSL)

XIJ down 30% since late September, closed at the lowest level since April's Liberation Day low on Tuesday

XSJ down 12% since late August and closed at the lowest level since March on Tuesday

Overall, the market continues to work its way through the recent pullback (mostly inflation/RBA rate repricing-related). The index is starting to look better off the back of higher highs and trading on the right side of key moving averages but still has a lot of work cut out for it. Participation needs to broader because at the moment, it's pretty much miners lifting the market (all sectors currently red YTD besides Materials).

AMP's take on November CPI

[1:57 pm] "The monthly Australian consumer price index (CPI) was flat over November, and up by 3.2% over the year on the headline measure, slightly below forecasts of a 3.6% increase (we expected 3.7%). This is good news, as the monthly CPI data has been surprising higher for the last 4 prints, prior to today," AMP’s Diana Mousina wrote in a note this afternoon.

"The February meeting is likely to be “live” which means it could be a close call between no change to rates and a rate hike, as the inflation data is too high for the RBA’s liking but may not be high enough to justify raising rates."

Despite the risk of a rate hike, Mousina believes the RBA will keep rates unchanged in February and throughout 2026.

Analysts' take on Bluescope

[1:54 pm] Bluescope shares rallied 20.8% to $29.54 on Tuesday after the company received a non-binding indicative offer from a consortium comprising SGH and Steel Dynamics to acquire the company at $30.00 a piece.

While the offer reflects a solid ~23% premium, analysts widely viewed it as undervaluing the business.

Jarden retained Neutral, raised target from $24.90 to $30.00. Sees North America as the primary value driver with additional upside from underappreciated property assets and recent capex, though Australian regulatory approval remains the key execution risk despite lower risk under a two-party consortium.

Macquarie retained Outperform, target unchanged at $25.50. Views the bid structure as skewed toward North America and ANZ valuation, with conditionality elevating completion risk, but believes property value and potential post-deal Asia divestments provide an important offset.

Lynas continues to rally intraday

[12:35 pm] Lynas (and most other rare earth stocks) continues to break fresh intraday highs, now up 10.1% ($14.48) vs. the 4.5% ($13.75) gain at the open.

As noted earlier this morning, China has hit Japan with export controls for dual-use exports, including:

All dual-use exports to Japan for military use are banned, with items also prohibited if they could enhance Japan’s military capabilities

The list covers over 800 items including chemicals, electronics, sensors, and aerospace/shipping equipment

Beijing cited Takaichi’s Taiwan remarks as violating the One-China principle and of “malicious nature with profoundly detrimental consequences”

Japan relies on China for roughly 70% of rare earth imports, including materials critical for both military and civilian technology, though current stockpiles may delay immediate impact

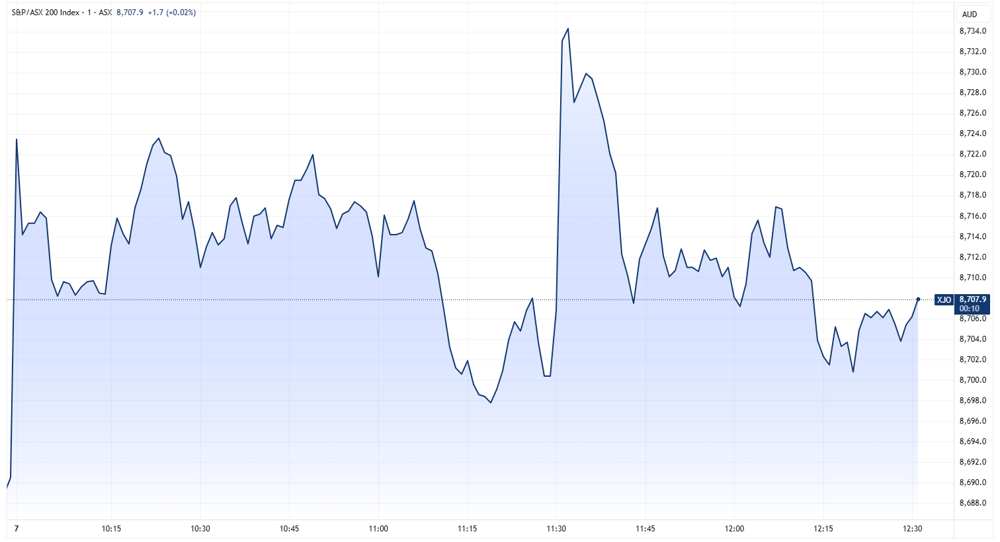

ASX 200 backtracks CPI gains

[12:32 pm] ASX 200 currently up 0.30% after briefly rallying as much as 0.59% following the cooler-than-expected CPI print.

ASX 200 intraday chart (Source: TradingView)

Aussie inflation unexpectedly cools

[11:34 am] ASX 200 trading ~0.5% higher after a solid inflation print for November.

Headline inflation flat month-on-month

Headline inflation up 3.4% year-on-year vs. 3.7% consensus and 3.8% in October

Trimmed mean inflation up 0.3% month-on-month and up 3.2% year-on-year

A few key takeaways from the ABS report include:

The largest contributor to annual inflation in November was Housing, up 5.2 per cent. This was followed by Food and non-alcoholic beverages, up 3.3 per cent, and Transport, which rose 2.7 per cent.

The main reason for lower annual Goods inflation in November was Electricity, which rose 19.7 per cent in the 12 months to November, compared to 37.1 per cent to October.

Annual Services inflation was 3.6 per cent in the 12 months to November, down from 3.9 per cent to October. Annual Services inflation eased due to Domestic holiday travel, following high demand in October from school holidays in all states and territories and major sporting events.

Top ASX 200 gainers and losers

[10:36 am] 4DMedical tops the leaderboard after announcing a commercial arrangement with UC San Diego Health. Meanwhile, Capstone Copper continues to trend lower amid a strike (commenced Mon 5-Jan) affecting its Mantoverde Mine in Chile. The strike represents approximately 50% of Mantoverde employees or 22% of its total workforce, set to lower production by at least 70%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

4DX | 4DMedical | 10.74% | $4.64 |

LYC | Lynas Rare Earths | 7.11% | $14.09 |

GGP | Greatland Resources | 6.96% | $11.53 |

SLX | Silex Systems | 5.85% | $6.88 |

DMP | Domino's Pizza | 5.02% | $22.28 |

NEM | Newmont Corporation | 4.47% | $161.16 |

WAF | West African Resources | 4.06% | $3.33 |

AAI | Alcoa Corporation | 3.54% | $93.67 |

ZIM | Zimplats | 3.18% | $24.35 |

NIC | Nickel Industries | 3.16% | $0.98 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

CSC | Capstone Copper Corp | -3.62% | $15.32 |

HVN | Harvey Norman | -3.48% | $6.66 |

MND | Monadelphous Group | -2.71% | $26.89 |

MIN | Mineral Resources | -2.53% | $56.31 |

IGO | IGO | -2.29% | $8.53 |

BPT | Beach Energy | -2.02% | $1.12 |

PLS | PLS Group | -1.96% | $4.75 |

STO | Santos | -1.56% | $6.01 |

PME | Pro Medicus | -1.51% | $210.53 |

CEN | Contact Energy | -1.48% | $7.97 |

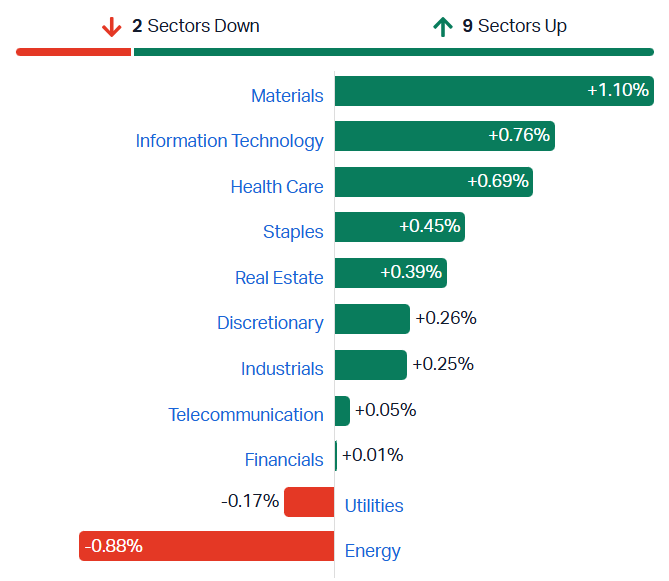

ASX 200 higher, miners extend gains

[10:34 am] ASX 200 up 0.3% in early trade, largely buoyed by Materials (+1.1%) and relatively broad strength among value/defensives like Healthcare, Staples and Real Estate. The market has been relatively choppy over the past couple of weeks, but starting to get on the right side of key moving averages.

ASX 200 sector performance (Source: Market Index)

ASX 200 daily chart (Source: TradingView)

Rare earth stocks trading sharply higher

[10:30 am] Rare earth and critical metal stocks opened sharply higher, with most names continuing to push intraday highs on the China news. A staple name like Lynas opened 4.5% higher ($13.75) and currently up 6.8% ($14.05).

Ticker | Company | % Chg | Price |

|---|---|---|---|

LYC | Lynas Rare Earths | 6.81% | $14.05 |

ASM | Australian Strategic Materials | 6.25% | $0.77 |

ARR | American Rare Earths | 5.71% | $0.37 |

AR3 | Australian Rare Earths | 4.65% | $0.23 |

HAS | Hastings Technology Metals | 4.42% | $0.59 |

ARU | Arafura Rare Earths | 3.45% | $0.30 |

MEI | Meteoric Resources | 2.70% | $0.19 |

BRE | Brazilian Rare Earths | 2.54% | $4.04 |

CHN | Chalice Mining | 1.67% | $2.43 |

Rare earths in the spotlight

[9:54 am] China has imposed immediate restrictions on exports of dual-use items to Japan for military purposes, escalating tensions after Japanese Prime Minister Sanae Takaichi’s comments on Taiwan. The news dropped around 7-8 pm on Tuesday.

All dual-use exports to Japan for military use are banned, with items also prohibited if they could enhance Japan’s military capabilities

The list covers over 800 items including chemicals, electronics, sensors, and aerospace/shipping equipment

Beijing cited Takaichi’s Taiwan remarks as violating the One-China principle and of “malicious nature with profoundly detrimental consequences”

Japan relies on China for roughly 70% of rare earth imports, including materials critical for both military and civilian technology, though current stockpiles may delay immediate impact

This could put a broad list of rare earth and critical metal stocks in the spotlight.

Meteoric secures EFA backing for Caldeira Project

[9:47 am] Meteoric Resources has received a non-binding Letter of Support from Export Finance Australia for up to US$50 million (~A$77m) to support development of its Caldeira Rare Earth Project, complementing prior US$250 million EXIM backing and ongoing funding discussions.

EFA support is intended to fund development using Australian engineering, procurement, construction and management contractors, reinforcing Australia–Brazil supply chain partnerships

The funding, combined with EXIM’s US$250m letter of interest, provides a strong foundation for Caldeira Project financing

Meteoric is also in discussions with the Brazilian Development Bank, other export credit agencies, and strategic investors to optimise funding solutions

The Caldeira Project has received its Preliminary Environmental Licence without restriction, commissioned a pilot plant, and produced its first mixed rare earth carbonate

Company page: Meteoric Resources NL (MEI)

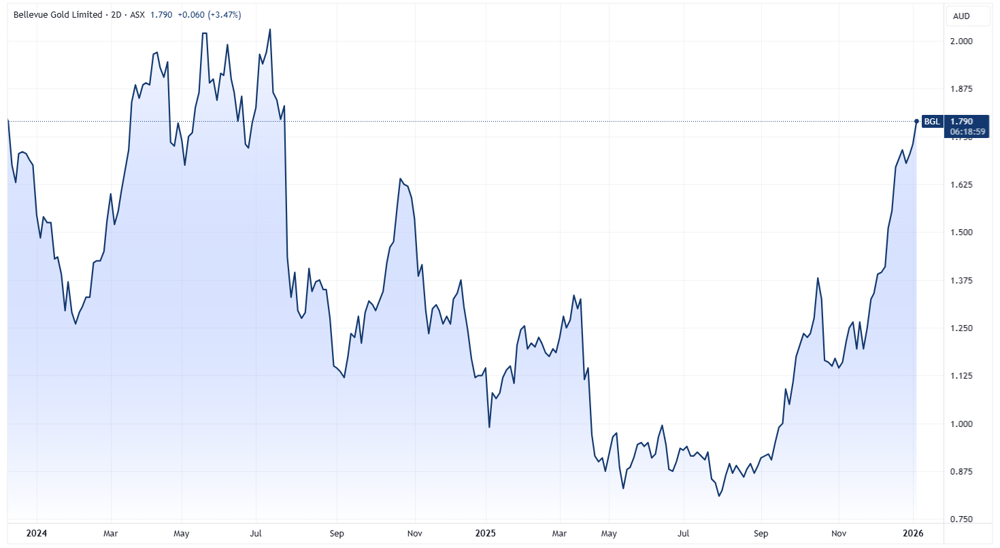

Bellevue Q2 gold production steady

[9:42 am] Bellevue Gold produced 37.0koz in the December quarter, with management reaffirming FY26 guidance of 130–150koz.

Q2 ore mined totaled 307kt at 3.8g/t, yielding 37.0koz of gold

Underlying free cash flow was $62m, up from $33m in the prior quarter

Production was limited at the end of December due to a safety incident suspending underground development and delayed access to high-grade headings at Deacon and Viago mines, with mining resuming 4 January 2026

Bellevue is almost back near record levels after suffering a ~60% drawdown between July 2024 and August 2025. The selloff was driven by repeated production downgrades due to geological variability and grade dilution, as well as unexpected capital raisings.

Company page: Bellevue Gold (BGL)

Capricorn on track for top end of FY26 guidance

[9:38 am] Capricorn Metals produced 30,476oz at Karlawinda in the December quarter, lifting YTD production to 62,794oz and keeping the company on track for the upper end of FY26 guidance of 115,000–125,000oz at an AISC of A$1,530–1,630/oz.

Mining fleet maintained expanded Karlawinda run rate for the third consecutive quarter, achieving pit face targets while supporting pre-stripping and infrastructure for the Karlawinda Expansion Project (KEP)

Cash and gold on hand at 31 December 2025 was $444.2m, up from $394.4m in September, with a quarterly cash build of $88.8m

Company page: Capricorn Metals (CMM)

Regis Q2 output steady, guidance unchanged

[9:32 am] No surprises from Regis' December quarter and guidance.

December quarter production of 96.6koz

Split between Duketon at 57.6koz and Tropicana at 39.0koz

First-half FY26 group production of 186.9koz

Cash and bullion increased by $255m during the quarter, after the payment of $38m in dividends

End-quarter cash and bullion balance rose to a record $930m

FY26 gold production guidance of 350-380koz reaffirmed

Company page: Regis Resources (RRL)

West African Resources FY production update

[9:25 am] West African Resources reported 2025 gold production of 300,383oz, which met its production guidance of 290-360koz (though misses the midpoint by ~7.6%).

December quarter production was up 17% quarter-on-quarter to 112,019oz as open pit mining continued to ramp up at the Kiaka project (up 76% QoQ).

Company page: West African Resources (WAF)

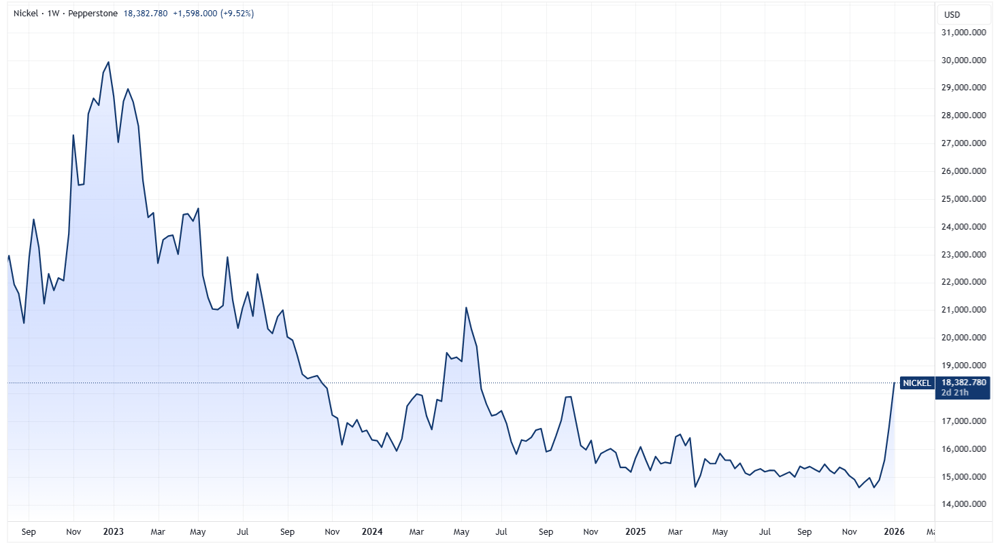

My 2 cents on nickel

[9:20 am] Nickel has been absolutely obliterated in recent years. Sentiment has been driven into the ground, with plenty of projects placed into care and maintenance or copping hefty impairments. We're now in the early innings of a potential comeback, though we probably need to see more strength and a clearer shift in fundamentals before calling it a bottom.

But if this is the bottom, there's a massive opportunity to pick up some of these beaten-down stocks. For example, Nico Resources (NC1):

Developing the Wingellina Project in WA, one of very few large scale nickel development projects outside of Indonesia

Sits on 1.56Mt of contained nickel and 123kt of contained cobalt

PFS (Dec-22) had post-tax NPV of A$3.34bn (assuming US$21,472/t nickel price vs. current US$18,382 spot)

The PFS is a bit outdated, but the point I'm highlighting is that the project has an NPV of over A$3 billion. Meanwhile, the stock is down more than 90% from its 2022 all-time highs and trading at a market cap of just $15 million (that's ~0.4% of project NPV). Notwithstanding plenty of other factors like project capex and funding, this leaves you with massive leverage should nickel prices actually recover.

Nickel joins the metals rally

[9:02 am] Nickel surged on Tuesday as Chinese investor flows and supply risk concerns drove a sharp rebound across base metal complex, marking a clear shift in market sentiment.

Nickel jumped more than 10% in London, the biggest gain in over three years, hitting a high of US$18,785 a tonne and extending gains to nearly 30% since mid-December

The rally comes despite an oversupplied market, with sentiment supported by rising production risks in Indonesia and heavy investment flows into China’s domestic metals markets

Trading patterns point to strong Chinese participation, with LME prices spiking on high volumes during Asian hours and extending gains during Shanghai Futures Exchange night trading

The rebound marks a revival for LME nickel after volumes collapsed following the 2022 short squeeze, with activity now spreading across copper and tin

Nickel price chart (Source: TradingView)

January effect gains traction

[8:54 am] Citadel Securities argues early-year flows, broadening participation, and supportive market structure are reinforcing the seasonal January rally across US equities.

Money-market balances remain elevated at a record $7.6tn, with cash from retirement contributions, bonuses and discretionary mandates rotating quickly into passive risk assets as markets reopen

Seasonal data supports the setup, with the Nasdaq 100 historically rising in January about 70% of the time since 1985, averaging a 2.5% gain and nearly 6% in years when the month finishes positive

Market leadership is broadening beyond crowded AI trades, with performance diffusing across sectors and supporting a more durable, market-wide earnings expansion

Retail participation is now a key driver, with individual investors buying call options in 35 of the past 36 weeks and accounting for roughly 60% of OCC customer options volume

Both retail and institutional flows are rotating into higher-risk and lagging sectors including energy, utilities, real estate and materials, while cross-asset correlations near one-year lows point to healthier market structure and scope for stock-specific returns

Source: Bloomberg

OBBBA lifts 2026 fiscal outlook

[8:52 am] The One Big Beautiful Bill Act widely viewed as a material fiscal tailwind for 2026, with tax relief and capex incentives supporting consumption and growth.

The bill includes a backdated TCJA extension, higher standard deduction with a 3% inflation adjustment, increased child tax credit, higher SALT cap, enhanced senior deduction, no tax on tips or overtime, and no tax on auto loan interest

Goldman Sachs estimates tax cuts will lift household consumption growth by 0.2pp in 2026, while Wells Fargo sees an average $800–850 uplift per tax filer, equating to a ~45bp boost to GDP

Deutsche Bank estimates a $50–60bn increase in consumer spending, Morgan Stanley sees a $65bn lift to personal income, and Bloomberg places total tailwinds in a broad $30–100bn range

Beyond households, analysts highlights capex support from full and immediate expensing of US manufacturing construction and 100% bonus depreciation

Nvidia's Rubin chips hit full production

[8:48 am] Nvidia used CES to reinforce that its next-generation AI roadmap is on schedule, demand remains supply-constrained, and upside risk to medium-term revenue expectations persists.

Rubin chips are now in full production and on track to ship in the second half of 2026, with management pointing to a step-change in capability at 3.5x better training performance and 5x better inference versus Blackwell

Jensen highlighted “skyrocketing” compute requirements as a key driver of sustained demand, supporting confidence in the ~$500bn Blackwell and Rubin pipeline outlined at GTC

Demand from China for H200 remains strong, with licence applications submitted and Nvidia stating it has sufficient supply without impacting shipments to other regions

Physical AI and robotics featured heavily in the keynote, signalling a strategic push beyond cloud workloads, though Omniverse and industrial digitisation are not yet delivering meaningful financial contribution

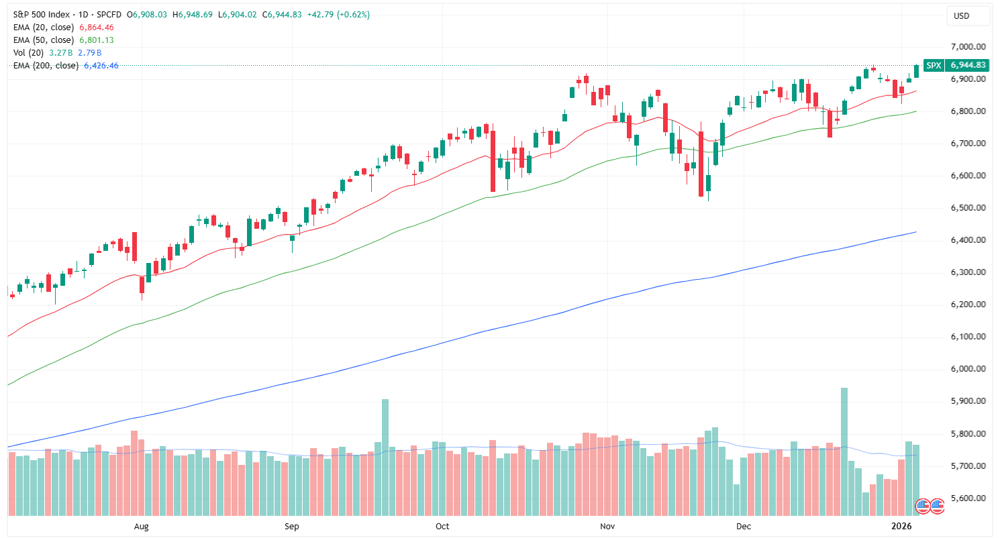

S&P 500 and Dow close at fresh all-time highs

[8:43 am] Very strong overnight session, with all sectors higher except Communication Services (-0.49%) and Energy (-2.81%). The S&P 500 logged its first record close since 24 December, while the Dow recorded its second straight all-time high.

S&P 500 daily price chart (Source: TradingView)

We're back!

[8:31 am] Hi there – Morning wraps, the blog and Evening wraps are back! So keen to dig into all the wild stuff that's been happening (pretty much every commodity price chart is vertical). Really hoping to crank up the news and insights on the blog this year. Just getting the Morning Wrap out. Will start talking overnight shenanigans in a momentum.

ASX 200 futures are up 43pts (+0.53%) as of 8:30 am AEDT.