ASX 200 Live Today - Wednesday, 4th March

The S&P/ASX 200 is set to open sharply lower amid a major escalation in the Middle East. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Wednesday, March 4. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 back near session lows

[2:09 pm] That's all for today. ASX 200 is down 1.98%, near session lows of -2.15%, with 168 constituents (84%) in the red and every sector lower except Tech, which is barely holding positive at +0.05%. The Iran conflict and Strait of Hormuz situation will likely continue to dominate headlines and drive market direction. UBS released an interesting report about the conflict, noting:

The key risk is not the near-term oil price spike but how long the disruption sustains, with even a partial impairment of Hormuz flow for several weeks enough to strongly upset oil and global markets

Historical oil shocks since 1980 saw both oil prices and equities recover to pre-shock levels in around 4-5 months, but today's S&P 500 is trading at 22.2x earnings versus a median of 14.3x at the time of prior shocks, leaving far less valuation buffer

Low stock and sector correlation has kept index-level volatility subdued as investors focused on micro themes, but a sustained oil disruption puts the benign growth-inflation mix underpinning that at risk

Three equity rotations seen as likely to fail in this environment are large cap to small cap, growth to value, and high quality to low quality, while the US to global rotation may sustain but is also not without risk

Australia GDP growth tops expectations

[1:50 pm] Australian GDP rose 0.8% in the December quarter and up 2.6% compared to a year ago, according to the ABS. The figures topped expectations of 0.6% and 2.2% respectively.

Key takeaways from the ABS:

"There was broad based economic growth in the quarter, with rises observed in a large majority of industries. Public and private demand each contributed 0.3 percentage points to GDP growth," said ABS Head of National Accounts, Grace Kim

"GDP per capita increased for the fourth consecutive quarter and is now 0.9% higher than a year ago, the highest through the year growth since December quarter 2022."

Household spending up 0.3% in the quarter and 2.4% through the year

Expenditure on electricity, gas and other fuels fell 9.5 per cent, driven by decreased electricity usage (detracting 3.3 percentage points) and reduced out of pocket expenditure due to Government rebates

There were increased levels of production in 17 out of 19 industries. Mining production increased 2.6 per cent, contributing 0.3 percentage points to GDP growth as mines resumed work following scheduled maintenance in the previous quarter.

Private investment increased for the fifth consecutive quarter, growing by 0.7 per cent and contributing 0.1 percentage points to GDP growth.

Household disposable income rose 1.8 per cent, significantly higher than the nominal increase in household spending of 1.1 per cent.

Source: ABS

Energy stocks slip

[1:45 pm] A fairly uneventful day for energy stocks, with most trading slightly lower following a sharp reversal in oil prices overnight. Brent was up as much as 9.0% to US$85.1 around 1 am on Wednesday, but dipped as low as US$78 after Trump ordered the US Development Finance Corporation to provide political risk insurance and guarantees for all maritime trade traveling through the Persian Gulf. He also said the US Navy will begin escorting tankers through the Strait of Hormuz.

Ticker | Company | % Chg | Price |

|---|---|---|---|

WDS | Woodside Energy | 0.23% | $30.55 |

STO | Santos | -1.24% | $7.19 |

AGL | Agl Energy | -1.53% | $9.64 |

BPT | Beach Energy | -1.56% | $1.14 |

ORG | Origin Energy | -1.67% | $11.79 |

Gold stocks recover early losses

[12:59 pm] Gold is currently up 1.7%, following a 4.3% dip overnight. Most gold stocks are still trading lower, but well-off session lows. The below chart shows the gains they've made since the open.

Ticker | Company | % Chg from Open | Price |

|---|---|---|---|

CMM | Capricorn Metals | 6.95% | $14.55 |

RMS | Ramelius Resources | 6.31% | $4.55 |

GGP | Greatland Resources | 5.24% | $13.45 |

NST | Northern Star Resources | 5.04% | $29.83 |

VAU | Vault Minerals | 4.68% | $5.59 |

OBM | Ora Banda Mining | 4.25% | $1.35 |

GMD | Genesis Minerals | 4.01% | $7.65 |

BGL | Bellevue Gold | 3.85% | $1.76 |

Tech stocks bounce

[12:02 pm] S&P/ASX 200 Tech Index is the only sector that's green today, up 1.25%. This follows a strong overnight session for software stocks, where the iShares Expanded Tech-Software ETF gained 1.6%. Plenty of heavyweight names like Life360, Xero and Wisetech trading 2-3% higher, though the same can't be said about smaller names like Dicker Data, Audinate and Siteminder.

Ticker | Company | % Chg | Price |

|---|---|---|---|

360 | Life360 | 3.54% | $21.08 |

XRO | Xero | 3.26% | $81.43 |

WTC | Wisetech Global | 2.46% | $45.35 |

TNE | Technology One | 2.18% | $25.31 |

CAT | Catapult Sports | 1.98% | $3.36 |

BVS | Bravura Solutions | 1.97% | $2.07 |

OCL | Objective Corporation | 0.39% | $12.76 |

DTL | Data#3 | -0.66% | $6.81 |

HSN | Hansen Technologies | -0.77% | $5.14 |

NXL | Nuix | -1.07% | $1.85 |

NXT | NextDC | -1.56% | $13.29 |

IRE | Iress | -1.70% | $7.25 |

PPS | Praemium | -2.01% | $0.73 |

CDA | Codan | -2.02% | $36.82 |

MP1 | Megaport | -2.23% | $7.90 |

SDR | Siteminder | -2.32% | $3.16 |

MAQ | Macquarie Technology Group | -2.66% | $60.94 |

AD8 | Audinate Group | -3.62% | $2.80 |

DDR | Dicker Data | -3.70% | $8.85 |

Miners moving off lows

[11:59 am] The Materials Index (XMJ) currently down 2.80%, bouncing off session lows of ~4%. Commodity prices also broadly higher after a sharp selloff overnight, notably gold (+1.02%), silver (+2.02%) and copper (+0.46%).

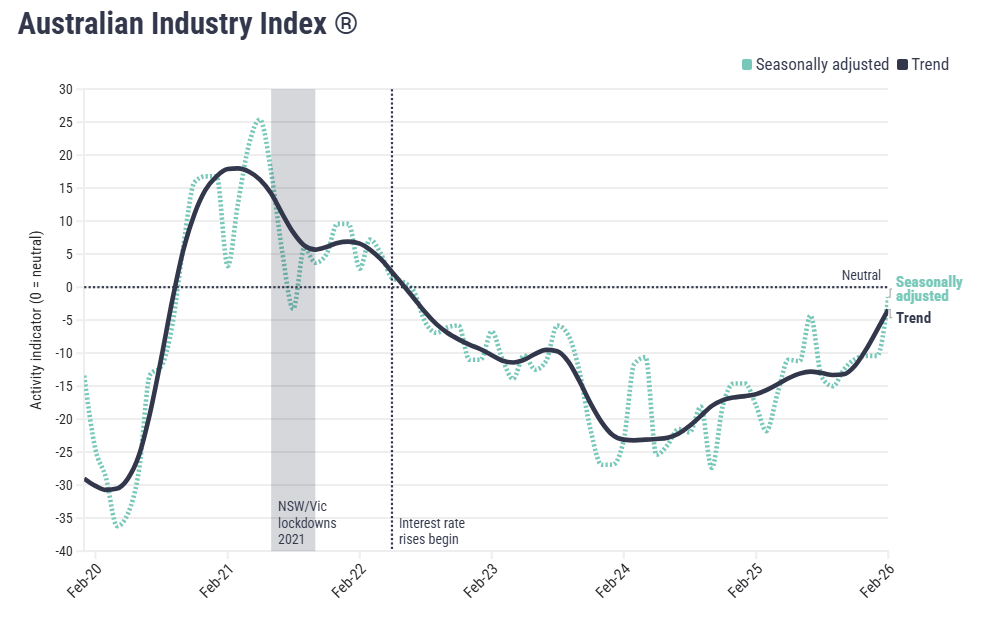

Australian industry showing green shoots, but recovery uneven

[10:56 am] The Australian Industry Index rose sharply in February, its strongest result in four years, though the improvement is concentrated in services and leading indicators rather than broad-based activity.

The headline index jumped 9.0 points to near neutral in February, led by business services, while construction and manufacturing remained under pressure from regulatory burden, skills shortages and soft demand

New orders rose 11.4 points to -2.1 and input volumes moved back into positive territory at 8.1, suggesting selective restocking and early-stage project activity rather than a genuine demand recovery

Employment turned positive for the first time in three years at +12.8, though the divergence from still-negative activity points to labour hoarding in anticipation of recovery rather than current demand strength

Margin pressure persists with input prices at 43.5 versus a sales price index of just 5.3, meaning firms continue absorbing cost increases with limited ability to pass them through

Wage growth (35.5) reflects skills scarcity and retention pressures rather than output-driven demand, and has held in the 35-40 range for the past year

Source: Ai Group Industry Index

Endeavour Group whipsaws into negative territory

[10:42 am] Endeavour shares dabbled between positive and negative territory, up as much as 1.0% in early trade but now down 3.7% after reporting its 1H26 result this morning.

Underlying NPAT down 6.7% to $278m vs $275.9m ests (0.8% beat)

Interim dividend down 13.6% to 10.8 cps (in line with ests)

Retail sales up 0.2% to $5.5bn, with Q2 improving, Dan Murphy's and BWS up 0.7% to $5.4bn with four consecutive months of growth

Hotels sales up 4.4% to $1.2bn, with gaming uplift and refurbished venues driving Q2 strength, both segments recorded their strongest ever monthly sales in December

Early 2H26 trading shows Retail +1.3% and Hotels +4.5% in the first seven weeks, though both moderated in February

While hotels remained resilient, retail trends were softer-than-expected, with margins pressured amid continue promotional efforts and competitive pricing.

Bapcor chair lifts stake with on-market purchase

[10:39 am] Lachlan Edwards purchased 152,000 shares, lifting his beneficial holding to 175,000 shares. A very large increase in percentage terms (670%) but the initial exposure was relatively low.

The announcement noted a purchase price "between $0.75 and $1.00 per share" between 27 February and 2 March.

Bapcor is currently trading at 71 cents.

Company page: Bapcor (BAP)

Analysts' take on Life360

[10:29 am] Life360 reported a better-than-expected 4Q25 result on Tuesday, with revenue growth ahead and EBITDA well-above consensus expectations. The stock opened 15% higher, but experienced an aggressive intraday selloff, closing the session down 18%. A key driver of the reversal was commentary pointing to a much weaker margin profile in the first quarter and second half weighted performance guidance for FY26. Here's what analysts had to say this morning.

JPMorgan retained Overweight, lowered target from $47.00 to $38.00. Margin weakness viewed as timing-related, with user growth expected to accelerate in H2 and the core monetisation thesis remaining intact.

Goldman Sachs retained Buy, lowered target from $41.20 to $38.40. Market concerns around the outlook considered overdone, with advertising and partnerships highlighted as major growth drivers underpinning an improving long-term profitability trajectory.

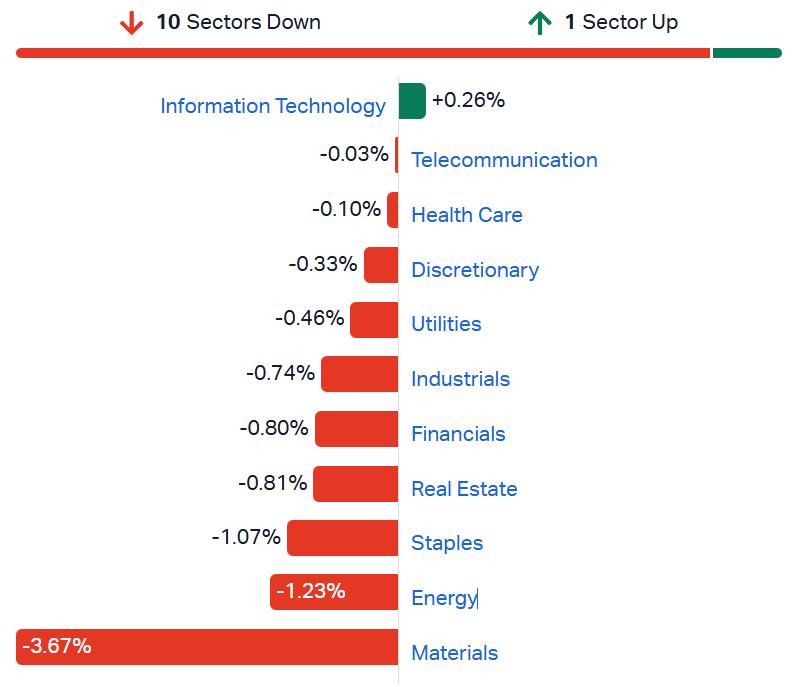

ASX 200 sharply lower, Miners smashed

[10:25 am] ASX 200 down 1.49% in early trade. All sectors lower except for Tech (I know right?). The index has now given back 2.8% in the last two sessions, trading at a two-week low.

Materials Index down 3.9% following a broad-based selloff for commodities (ex-Energy) overnight. The materials sector hasn't seen a fall of this magnitude since Trump's Liberation Day tariff announcement on 7-Apr-25. Most commodity prices have started to bounce in early Wednesday trade (e.g. gold up 0.6%) but equities remain volatile.

ASX 200 sectors (Source: Market Index)

Treasury Wine CFO announces retirement

[10:02 am] Chief Financial and Strategy Officer Stuart Boxer will retire on 30 September 2026, kicking off a formal succession process.

Stuart Boxer's retirement date is set for 30 September 2026

TWE will run an internal and external search for a successor, with Boxer staying on to support the appointment and transition.

Boxer joined in 2020 and became Chief Financial and Strategy Officer in November 2023

CEO Sam Fischer framed the move as orderly and said the focus remains on “execution” and shaping the business through the TWE Ascent program.

By Warren Masilamony | Company page: Treasury Wine Estates (TWE)

GenusPlus acquires rail services provider at attractive multiple

[9:43 am] GenusPlus is acquiring Railtrain Holdings for up to $55 million, adding a nationally diversified rail services business at a compelling valuation.

Upfront cash consideration of $36.5m, with contingent earnouts of up to $8.5m in CY26 and $10m in CY27 subject to EBITDA targets of $15m and $20m respectively

Acquisition multiple of 2.75x EV/EBITDA assuming maximum earnout, which is pretty low for an infrastructure services business

Railtrain generated pro-forma normalised revenue of ~$96m and EBITDA of ~$16m in FY25, implying an EBITDA margin of ~17%

FY26 is expected to be softer due to project delays, though the deal is flagged as immediately earnings accretive for GenusPlus

Funded from existing cash and a new syndicated facility, with completion expected by end of March

Company page: GenusPlus Group (GNP)

Endeavour Group 1H26 results in line, Hotels momentum building

[9:28 am] Endeavour delivered a solid first half with earnings broadly in line with estimates, as Hotels momentum accelerated and Retail returned to growth heading into the second half.

Revenue up 0.9% to $6.68bn

Underlying EBIT down 5.4% to $563m vs $560.4m ests (0.5% beat)

Underlying NPAT down 6.7% to $278m vs $275.9m ests (0.8% beat)

Interim dividend down 13.6% to 10.8 cps (in line with ests)

Retail sales up 0.2% to $5.5bn, with Q2 improving, Dan Murphy's and BWS up 0.7% to $5.4bn with four consecutive months of growth

Hotels sales up 4.4% to $1.2bn, with gaming uplift and refurbished venues driving Q2 strength, both segments recorded their strongest ever monthly sales in December

Early 2H26 trading shows Retail +1.3% and Hotels +4.5% in the first seven weeks, though both moderated in February

Capex guidance lifted to $460-500m from $420-470m, reflecting accelerated Hotels renewals investment

Group confirmed it will maintain its combined Retail and Hotels portfolio as the best path to shareholder value

Company page: Endeavour Group (EDV)

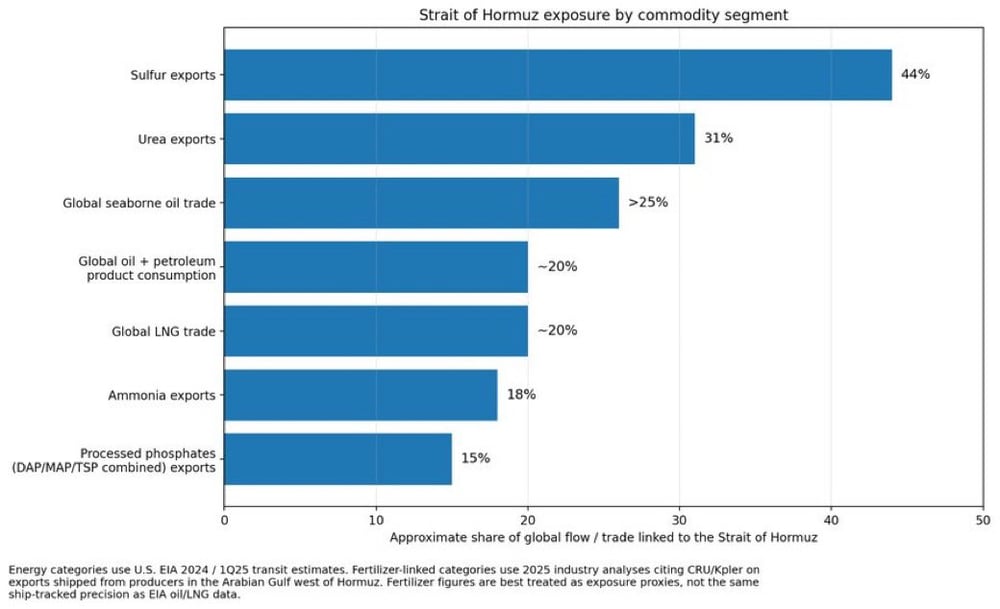

No one's talking about fertiliser disruption

[9:23 am] Plenty of headlines and data out there about oil and LNG disruption, but none about fertilisers. A significant amount of fertiliser components flow through the Strait of Hormuz, including:

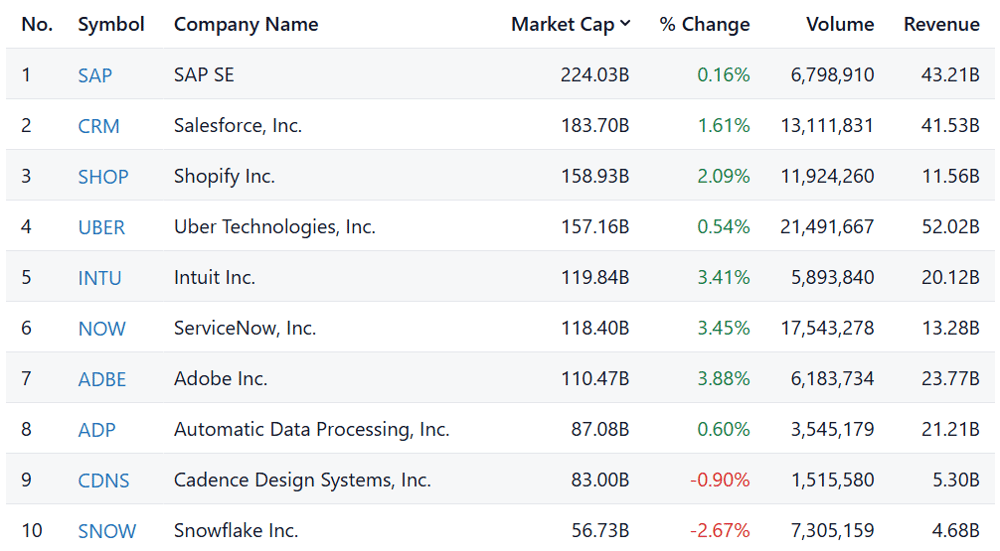

Software is a ... safe haven?

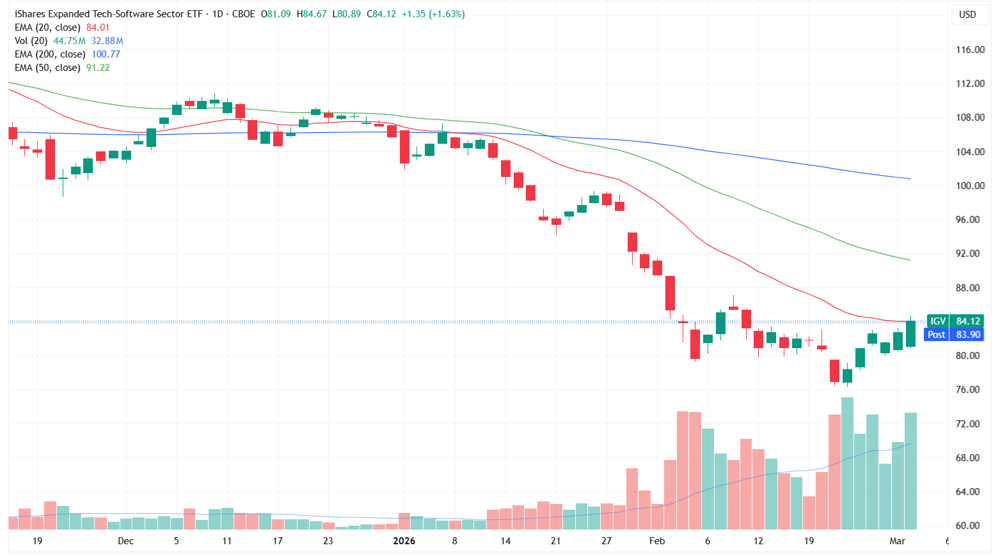

[9:13 am] Software stocks managed to finish mostly higher overnight, with high-profile names like Shopify, Salesforce and Adobe all up 1-3%.

Source: Stock Analysis

The iShares Expanded Tech-Software ETF is the most commented benchmark/barometer for software stocks. It opened 2.0% lower but spent most of the session trending higher, closing up 1.6% to the highest since 11 February. The session marked the ETFs fourth highest volume on record (behind 24-Feb, 5-Feb and 4-Feb).

iShares Expanded Tech-Software ETF daily chart (Source: TradingView)

Commodity prices smashed

[9:07 am] A very heavy overnight session for commodity prices, with most trading slightly off intraday lows.

Commodity | % Chg | Price (US$) |

|---|---|---|

Platinum | -9.5% | $2,088 |

Silver | -8.1% | $81.99 |

Palladium | -7.2% | $1,646 |

Gold | -4.4% | $5,087 |

Copper | -2.1% | $5.83 |

Zinc | -1.0% | $3,251 |

Nickel | -0.3% | $17,054 |

Aluminium | +2.8% | $3,261 |

Brent | +4.9% | $81.93 |

Asia braces for energy shock

[8:56 am] Iran's shutdown of the world's most critical oil chokepoint is triggering an energy security crisis, with Asia bearing the brunt of supply and price risks.

Qatar accounts for roughly 20% of global LNG exports and 30% of China's LNG supply.

South Asia faces the most disruption. Qatar and the UAE account for 99% of Pakistan's LNG imports, 72% of Bangladesh's and 53% of India's. Around 60% of India's oil imports also originate from the Middle East.

China is materially exposed, with roughly 40% of oil imports and 30% of LNG imports transiting the strait. Beijing has made its most direct public call yet for safe passage, urging all parties to cease military operations and protect navigation.

Japan and South Korea are also vulnerable, with the Middle East supplying around 75% and 70% of their oil imports respectively. LNG reserves in both countries cover only two to four weeks of demand.

Thailand stands out as the biggest current account loser in Southeast Asia, with net oil imports at 4.7% of GDP.

Source: CNBC

Iran war seen lifting inflation, growth impact limited for now

[8:54 am] A Bloomberg survey of global economists finds the conflict is expected to accelerate inflation across major economies, though GDP impacts remain contained unless the war drags on.

Around half of surveyed economists expect somewhat quicker inflation in both the US and Eurozone, with nearly 40% predicting the same for China, defined as a 0.3 to 0.9 percentage-point acceleration from prior expectations

The primary inflation driver is oil and gas prices, with roughly one-fifth of the world's seaborne energy supply normally transiting the Strait of Hormuz, which has effectively ground to a halt

Secondary inflation risks include higher airfares, distribution costs and broader supply-chain disruption if the conflict is prolonged

The majority of respondents see minimal GDP impact across the US, Eurozone and China for now, though duration of the conflict is flagged as the critical variable

Source: Bloomberg

Fed speakers strike cautious tone as Iran conflict and tariffs cloud inflation outlook

[8:54 am] Three regional Fed presidents flagged rising uncertainty around the path for rate cuts, citing energy price risks, tariff pass-through, and sticky services inflation.

Kashkari (Minneapolis): Had pencilled in one cut for the year but said the Iran conflict has made him less certain, flagging persistent energy price inflation as the key unknown, and adding he would welcome Powell staying on beyond his May term expiry

Williams (New York): Said tariffs have overwhelmingly been absorbed by US firms and consumers, with NY Fed research estimating up to 90% of costs passed domestically, contributing around 0.5-0.75 percentage points to the current ~3% inflation rate and stalling progress toward the 2% target, though he expects the impact to be temporary with the Fed hitting its goal by 2027

Schmid (Kansas City): Struck the most hawkish tone, warning inflation has been above target for nearly five years and there is no room for complacency, with price pressures evident in both tariff-affected goods and services, and healthcare wage inflation posing an additional upside risk

Private credit stress signals mount

[8:51 am] Redemption pressures, markdowns and dividend cuts are emerging across major private credit vehicles, raising questions about portfolio quality.

Blackstone's flagship private credit fund allowed investors to redeem a record 7.9% of shares, with requests of $3.7-3.8bn exceeding the 7% threshold. Blackstone and employees injected $400m to cover the overage.

Blue Owl took the opposite approach, halting quarterly redemptions entirely to sell assets and return capital.

Markdowns were recorded at FS KKR and Blackstone Secured Lending Fund, with both cutting dividends. Soros CIO Dawn Fitzpatrick warned the pressure will trigger a "culling" of alternative asset managers who fail to honour redemption commitments.

Fitzpatrick flagged a "painful 18 to 24 months" ahead, and Brookfield CEO Connor Teskey acknowledged "undoubted concerns" in direct lending despite broader credit markets holding up.

Source: Bloomberg

Middle East energy infrastructure under attack

[8:47 am] Iranian drone strikes have hit multiple critical oil and gas facilities across the Gulf region, threatening a significant share of global energy supply.

Ras Tanura, one of the world's largest oil export terminals (~550K bpd capacity), has been struck and temporarily shut down, directly impacting Saudi Aramco's export capacity

The Strait of Hormuz has been declared "closed" by IRGC command, with tankers targeted and vessels struck or set ablaze. Roughly 20% of global oil supply transits this chokepoint

QatarEnergy's Ras Laffan LNG complex, one of the world's largest LNG export hubs, was hit by drone strikes and has halted production, with immediate implications for global LNG markets and key importers including Japan, South Korea and Europe

Additional facilities affected include Mesaieed Industrial City (Qatar), Fujairah oil trading hub (UAE) and Port of Jebel Ali (Dubai), broadening the geographic footprint of the strikes

Iraqi Kurdistan has halted its ~200K bpd oil exports as a precautionary measure, adding further supply pressure

US-Iran war escalates with major economic risks in focus

[8:47 am] Trump signals further strikes ahead as global diplomatic efforts mount and energy market disruption deepens.

Trump outlined war objectives including destroying Iran's missile capabilities, ending its nuclear programme and stopping arms flows to militant groups, with the "big wave" of attacks still to come targeting missiles, drones and naval assets

Overnight strikes hit a US embassy in Saudi Arabia, killed six US servicemembers in Kuwait, and caused a major fire at UAE's Fujairah oil trading hub from intercepted drone debris, highlighting Iran's capacity to sustain asymmetric warfare cheaply

Ships have largely halted traffic through the Strait of Hormuz despite no formal closure, with JPMorgan warning Gulf producers could sustain output for no more than 25 days under full disruption

Energy infrastructure across Qatar and Saudi Arabia is at risk if Iran escalates retaliation, with a NYT analysis warning a cornered Iranian government could target regional oil and gas capacity

UAE, Qatar, France and China are all pursuing diplomatic de-escalation, though the path to a ceasefire remains unclear given Trump's stated objectives

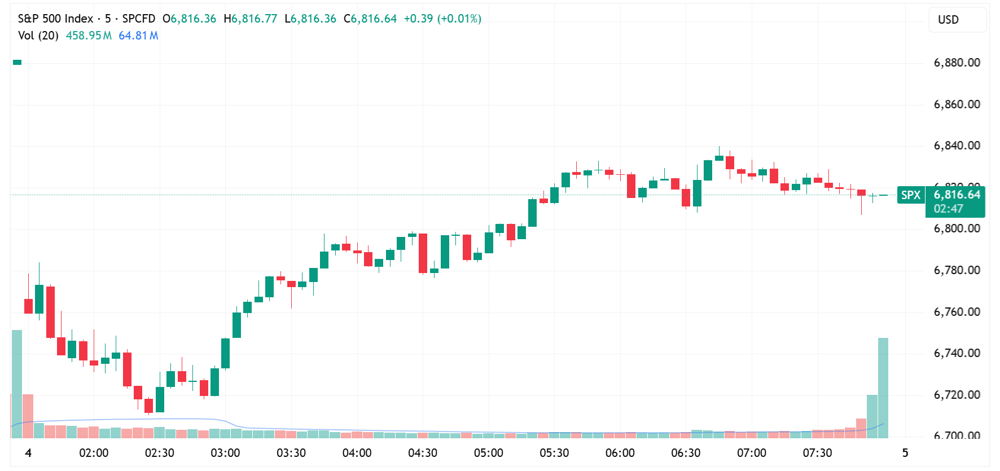

US stocks lower but off worst levels

[8:44 am] Major US benchmarks finished broadly lower but well-off worst levels. Wall Street experienced a sharp dip in the first hour of trade, then trended higher for most of the session to close towards the top end of the intraday range.

S&P 500 intraday chart (Source: TradingView)

Overnight recap (close vs. session low):

S&P 500 -0.94% vs. -2.49%

Dow -0.83% vs. -2.61%

Nasdaq -1.02% vs. -2.74%

Russell 2000 -1.79% vs. -3.95%

Good morning!

[8:30 am] ASX 200 futures are down 116 pts (-1.30%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks lower but well-off worst levels (e.g. S&P 500 closed 0.94% lower vs. session low of 2.49%)

Equities, bonds and commodities all moved in tandem (for once)

Commodity prices smashed, with gold down ~4% but still above US$5,000/oz, while silver, platinum and palladium down 7-8%

Major escalation in the Middle East, Trump still planning further 'big wave of attacks', while energy infrastructure/energy prices remain a key macro focus