ASX 200 Live Today - Wednesday, 24th June

The S&P/ASX 200 is set to rise after Wall Street's chip rout dragged the Nasdaq 2.2% lower overnight. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Wednesday, June 24. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

Nickel Industries to invest US$169m for 17.5% of TMI HPAL project

[9:36 am] Nickel Industries will invest US$169 million for a 17.5% stake in the PT Teluk Metal Industry HPAL project in Indonesia, deepening its push into the EV battery supply chain.

TMI is an expansion of the existing ENC project at the Indonesia Morowali Industrial Park, producing mixed hydroxide precipitate, with the acquisition payment due 26 November 2026

The 17.5% stake sits alongside a 72.5% interest held by a Korean-Japanese consortium including LS MnM and Hanwa, and a 10% holding by Sumber International Investment

A construction guarantee caps the total acquisition cost at US$169m and underwrites delivery of nameplate production by September 2027

TMI's nameplate capacity of 38,640 Ni tonnes a year delivers around 6,775 Ni tonnes a year of attributable MHP production to Nickel Industries

The Sampala Project has been named TMI's exclusive ore supplier, aligning the company as both equity investor and upstream supplier

To be funded from cash reserves and existing operations, with largest shareholder Shanghai Decent on hand to provide debt funding if needed

One of the last large-scale HPAL opportunities following the Indonesian government's moratorium on new projects, with the proven HNC HPAL delivering adjusted EBITDA margins of US$9,996/t Ni in Q1 2026

Company page: Nickel Industries (NIC)

Baby Bunting cuts FY26 guidance as fourth-quarter trade softens

[9:26 am] Baby Bunting has downgraded its FY26 profit guidance after softer-than-expected fourth-quarter trading, with prams and car safety dragging on sales.

Pro forma NPAT now seen at $16.0-17.0m, down ~11% on prior guidance of $17.5-19.5m

Below $17m ests (3% miss at the midpoint)

Though still up 32-40% on FY25

Total sales of $553-555m vs. $571.2m ests (~3% miss)

Comparable store sales growth of around 3.5%, roughly half the prior guidance of 5-7%

Gross margin above 41% vs. 40.2% a year ago

Store of the Future sales growth of around 18% for the year, with online up around 16%

CEO Mark Teperson flagged three RBA rate rises in the second half and higher fuel prices as weighing on consumer spending and distribution costs

Net debt expected to finish at around $20m, with FY26 results due 14 August 2026

Company page: Baby Bunting Group (BBN)

Tasmea to acquire energy services group JPS

[9:23 am] Tasmea has agreed to acquire integrated energy services provider JPS Group for total consideration of up to $75 million, diversifying into LNG and gas infrastructure markets.

Upfront consideration of $50m, comprising $24.5m cash and $25.6m in scrip (3,011,750 new shares at $8.50)

Earn-out of up to $25m in cash across FY27 to FY30, tied to JPS hitting a maintainable EBIT target of at least $12m a year

Struck at an upfront EV/EBIT multiple of ~5x JPS FY26e underlying EBIT of about $10m

Forecast to deliver ~5% pro forma EPS accretion in FY26e, incremental to the Maxim Group deal

Settlement targeted around 1 August, subject to ACCC approval, with earnings to contribute from FY27

JPS serves a Tier-1 client base including Chevron, Woodside, Shell and Santos under more than 10 long-term MSAs

On guidance:

FY26 pro forma underlying EBIT of $185m, up from $175m including Maxim

FY26 pro forma underlying NPAT of $113m, up from $107m including Maxim

FY26 standalone underlying EBIT of $117m reconfirmed, up 26% on FY25's $93.2m pro forma

FY26 standalone underlying NPAT of $72.5m reconfirmed, up 16% on FY25's $62.5m pro forma

Company page: Tasmea (TEA)

Atlas Arteria takeover extended after IFM crosses 50%

[9:15 am] IFM's Diamond Infraco has extended its off-market takeover offer for Atlas Arteria after its voting power passed 50% in the final week of the offer period.

Voting power in Atlas Arteria crossed above 50% within the last seven days of the offer period, triggering an automatic extension

The offer is now open for acceptance until 7:00 pm AEST on 7 July 2026, unless withdrawn or further extended

The bid, lodged via IFM Global Infrastructure Fund subsidiary Diamond Infraco, targets all shares it does not already own

Company page: Atlas Arteria (ALX)

3P Learning block trade

[9:15 am] A 16.2m-share block in 3P Learning crossed on Wednesday at 32.97 cents a share, representing 5.9% of the company.

Company page: 3P Learning (3PL)

US growth picks up in June but factory job cuts hit post-2009 high

[9:05 am] US business activity grew at its fastest pace in five months in June, though employment fell and price pressures stayed elevated.

The composite PMI rose to a five-month high of 52.2 from 51.5, pointing to growth of just over a 1% annualised rate in Q2

Manufacturing output hit a 59-month high as new orders surged, though the lift was again driven by precautionary stockpiling amid supply fears

Services activity edged up to a four-month high of 51.3, held back by high prices, elevated rates and weak consumer confidence

Employment fell for a second straight month, with factory job cuts at their fastest since 2009 outside the pandemic

Input cost inflation cooled on lower energy prices but stayed among the highest in four years, keeping selling-price inflation elevated

S&P Global's Chris Williamson said brighter Middle East news has restored some confidence, though growth remains sluggish versus pre-conflict levels

Source: S&P Global

UK output shrinks for second month as services hit 41-month low

[9:04 am] UK private sector activity contracted again in June as a sharp services slowdown outweighed a temporary boost to manufacturing.

The composite PMI eased to 49.4 from 49.7, a 14-month low and a second straight month below 50

Services activity fell to a 41-month low of 48.7, with firms blaming the Middle East war and domestic political uncertainty

Manufacturing output jumped to a 21-month high of 53.6, though the lift is fading as stockpiling-driven demand eases

Input price inflation moderated for a second month on lower energy prices but stayed elevated, allowing a softer rise in selling prices

Firms cut headcounts for a 21st straight month as new business fell at the fastest rate in 14 months

Source: S&P Global

Eurozone downturn eases in June as price pressures soften

[9:02 am] The Eurozone private sector contracted at its slowest pace in three months in June, with inflationary pressures showing early signs of peaking.

The composite PMI rose to 49.5 from 48.5, a three-month high but a third straight month below the 50 mark separating growth from contraction

Services activity improved to 48.9 from 47.7, while manufacturing output eased to a five-month low of 51.2

Germany posted its fastest contraction in 18 months, while France's downturn eased and the rest of the bloc grew modestly

Input cost inflation slowed to its weakest since February, helped by lower energy prices, with output price inflation also easing

Most responses were collected before the 17 June US-Iran cessation of hostilities, with tourism and leisure demand recovering

Source: S&P Global

Hormuz traffic recovers as more tankers signal crossings openly

[8:54 am] Tanker traffic through the Strait of Hormuz is picking up with vessels broadcasting their locations again, signalling growing shipowner confidence after the Iran-US peace deal.

Seven tankers, including two fully-laden non-Iranian supertankers, were in or had crossed the strait on Tuesday, all broadcasting their positions

Iran said the strait is fully open with large volumes transiting, after weekend reports it had been closed

Some ships still go dark mid-crossing, including a Taiwan-bound VLCC carrying Saudi and UAE crude that switched off its transponder before reappearing in the Gulf of Oman

Source: Bloomberg

SpaceX's US$25bn bond debut meets cautious credit investors

[8:52 am] SpaceX's first bond sale drew a more sceptical reception than its record IPO, with investors demanding a premium over comparably rated debt on cash-flow concerns.

The 2036 bonds priced at 1.4 percentage points over Treasuries, around 0.4 point wider than the average BBB-tier spread

Orders peaked near $90bn before falling to $73bn at pricing, leaving the book at under three times the deal size vs. a roughly four-times average for high-grade deals this year

Demand skewed to the shortest-dated, least risky tranche, reflecting concerns over a cash burn S&P expects to persist through 2030 and rise sharply next year

SpaceX held more than $100bn of cash as of 19 June and can cut investment or raise equity to defend its high-grade ratings

Moody's rated the deal Baa1 and S&P one notch lower at BBB, with S&P seeing borrowings climbing to $132bn in 2028 from near zero now

Shares rose 0.9% overnight after a three-day selloff erased more than $600bn in value, leaving them about 15% above the IPO price

Source: Bloomberg

Evercore stays bullish on megacap tech, says earnings will drive recovery

[8:51 am] Evercore ISI's Julian Emanuel expects megacap tech to return to favour after the selloff, arguing earnings will be the catalyst once volatility settles.

Emanuel says strong earnings will be the "proof of the pudding" and drive a rally, as they did during the April and May surge

He expects more churn, volatility and negativity in the near term before a refreshed attitude towards the Mag 7 develops

Alphabet, Amazon and Microsoft have fallen more than 13%, over 15% and almost 20% respectively from recent peaks, with the Nasdaq 100 erasing June gains

Micron is a bright spot ahead of Thursday's results, up more than 300% this year, with Bloomberg Intelligence seeing fiscal Q3 revenue beating guidance by 18% on higher chip prices

Source: Bloomberg

Barclays and Stifel lift S&P 500 target to 7,800 on earnings strength

[8:50 am] Barclays and Stifel raised their year-end S&P 500 targets to 7,800, around 4.4% above the last close, on the back of resilient corporate earnings.

Both cited strong earnings as the primary driver, with Barclays noting the bull case stays intact but earnings and AI capex visibility must do more of the work as Fed support fades

Barclays lifted its 2026 EPS forecast to $337 from $321 and set a 2027 index target of 8,800

Stifel's Thomas Carroll sees stock concentration at 40-year highs signalling a rotation out of megacaps into equal-weight indices

Carroll favours cyclicals such as energy, industrials, materials and select semiconductors with the economy running hot

Source: Reuters

KOSPI crashes 10% as memory rout triggers circuit breaker

[8:46 am] South Korea's KOSPI fell 9.99% on Tuesday as a media report on SK Hynix slowing AI memory expansion sparked a chip selloff that rippled globally.

The KOSPI closed down 9.99%, or 910.71 points, at 8,203.84, its steepest fall since March

Samsung Electronics and SK Hynix each shed more than 12%, triggering an automatic 20-minute market-wide trading halt

The catalyst was a Chosun Biz report that SK Hynix is slowing HBM4 expansion and shifting to higher-margin general-purpose DRAM, with the report citing weaker production forecasts for Nvidia's next-generation Rubin chip

The two chipmakers now make up more than half the index's value, having pushed the KOSPI past 9,100 for the first time on Monday

The index is still up 94.67% year-to-date despite the plunge, with CLSA flagging that record margin debt and newly approved leveraged single-stock ETFs have amplified retail-driven volatility

Fed holds and rate-cut expectations get priced out

[8:45 am] The probability of a Fed rate cut by year-end now sits at zero, with a 25 bp hike now the base case and increasing likelihood of two or more quarter-point hikes.

Source: CME Fedwatch Tool

BofA flips to three rate hikes in 2026, scrapping cut calls

[8:43 am] Bank of America has reversed its easing forecast and now expects the Fed to tighten through year-end as labour and inflation data hold firm.

BofA now sees three quarter-point hikes in 2026, pencilled in for September, October and December, a sharp break from its earlier rate-cut view

The shift follows May payrolls of 172,000, unemployment steady at 4.3% and wage growth still running at 3.4%, undercutting the case for easing

Inflation remains above the Fed's 2% target, with energy risks and firmer demand seen muddying the path lower

The Fed held at 3.5% to 3.75% on 17 June but turned more hawkish, with nearly half of policymakers flagging possible hikes ahead

BofA argues the market may be underpricing the risk that the next Fed surprise is tighter, not easier, policy

Source: Yahoo Finance

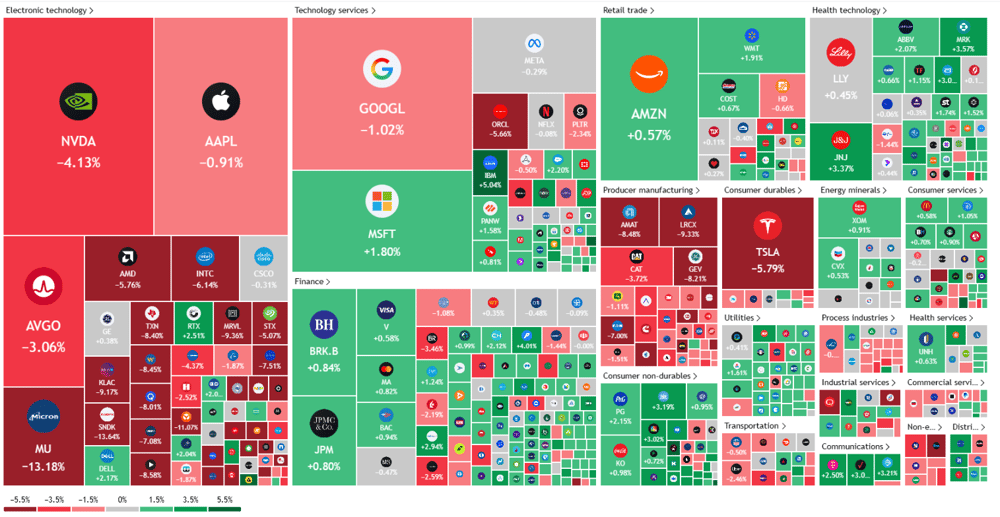

US equities dip as momentum unwind hits memory and semis

[8:38 am] US stocks closed lower on overnight, with a momentum unwind in memory and semiconductors driving the move rather than any shift in fundamentals.

Dow (0.09%), S&P 500 (1.44%), Nasdaq (2.21%) and Russell 2000 (0.96%) all finished lower

Equal-weight S&P 500 (-0.34%) outperformed the cap-weighted index by 110bps, with breadth slightly positive

Memory and semis bore the brunt amid AI scrutiny spanning open-source competition, capex ROI and speculation around 2027 memory price weakness

Nvidia (-4.1%) and Tesla (-5.7%) were the worst of the mostly lower Big Tech names, while quantum computing, airlines and regional banks outperformed

June flash manufacturing PMI beat to hit a 49-month high and services PMI came in slightly ahead, though employment fell for a second straight month

Micron earnings (after tonight's close) and Thursday's PCE inflation print are the next focus

S&P 500 heatmap (Source: TradingView)

Good morning!

[8:29 am] ASX 200 futures are up 21 pts (+0.23%)

The overnight session in a nutshell:

Major US benchmarks lower amid a tech and resources-led selloff, which started in Asian markets (KOSPI tumbled 10%) and flowed through to Europe/Wall Street

A Bank of America note called for three Fed hikes in 2026, with markets now pricing out cuts entirely

Commodity prices were mostly down around 1-2% when the ASX closed on Tuesday, but selling accelerated overnight, with sharp declines for copper (-3.7%), aluminium (-3.0%), gold (-1.9%) and more