ASX 200 Live Today - Wednesday, 17th December

The S&P/ASX 200 is set to open slightly higher despite a weak lead from Wall Street. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Wednesday, December 17. Expect a high volume of posts pre-market and more periodic updates throughout the day. It'll wrap up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

ASX 200 on track to finish lower

[2:15 pm] Not bad but not great. The S&P/ASX 200 is currently down 0.23%, off session lows of -0.60% but still on track to record a three-day losing streak and close slightly below the 200-day moving average. A relatively even split of constituents trading higher and lower, though large cap weakness is dragging most sectors into negative territory (only Materials and Real Estate positive at the moment). Broad range of headwinds for markets at the moment, including weak consumer confidence, economists (CBA, Citi and NAB) now forecasting 25-50 bps of rate hikes in the first half of 2026, disappointing Chinese economic data (and Vanke default jitters), AI momentum taking a breather and more. Materials is the only bright spot in the past week (up 2.4%) and enough to prop up the rest of the market. Let's see if the market can muster up some strength around these key levels.

Gold stocks back at record highs

[1:55 pm] The All Ords Gold index is up 3.7%, trading fractionally above last Friday's record high. Gold is trading slightly higher today, up 0.24% to US$4,312/oz. The past four sessions have been volatile, with prices swinging to and from positive/negative territory (but overall still up 0.76%).

Ticker | Company | % Chg | Price |

|---|---|---|---|

OBM | Ora Banda Mining | 6.59% | $1.38 |

PNR | Pantoro Gold | 6.20% | $4.89 |

GMD | Genesis Minerals | 5.89% | $6.83 |

WGX | Westgold Resources | 5.82% | $6.18 |

RRL | Regis Resources | 5.09% | $7.64 |

EVN | Evolution Mining | 4.42% | $12.65 |

RSG | Resolute Mining | 4.23% | $1.16 |

BGL | Bellevue Gold | 3.99% | $1.62 |

RMS | Ramelius Resources | 3.97% | $3.80 |

EMR | Emerald Resources | 3.95% | $6.19 |

CMM | Capricorn Metals | 3.73% | $14.32 |

PRU | Perseus Mining | 3.62% | $5.59 |

VAU | Vault Minerals | 3.52% | $5.44 |

NST | Northern Star Resources | 3.40% | $27.03 |

NEM | Newmont | 1.09% | $149.49 |

Austal dips on White House comments

[12:58 pm] The White House is reportedly preparing an executive order that could restrict capital returns and executive pay at military contractors, signalling tougher oversight amid delivery shortfalls.

Proposed measures may limit share buybacks, dividends and executive compensation for defence contractors, according to sources cited by Punchbowl.

Policy intent is tied to improving delivery performance rather than shareholder returns, according to US Treasury Secretary Scott Bessent

Boeing was touted as an example where excessive buybacks have come at the expense of R&D and operational execution.

A large cap defence name like Austal is down 11% at noon.

ASX 200 off lows as miners bounce

[12:51 pm] The ASX 200 is currently down 0.20%, well-off session lows of -0.60%. The intraday bounce is largely thanks to a sizeable swing from the Materials sector, which opened 0.21% lower but currently up 1.15%. Surprisingly, most other sectors have continued to grind lower and trading around intraday lows.

Best and worst performing stocks of the year

[12:46 pm] Here are the best and worst performing S&P/ASX 200 stocks of the year. Interesting to see that eight of the ten top runners are all ... gold miners. Meanwhile, the losers are mostly tech, building materials and high PE names.

Ticker | Company | % Chg | Price |

|---|---|---|---|

DRO | Droneshield | 223.38% | $2.49 |

PNR | Pantoro Gold | 217.32% | $4.86 |

RRL | Regis Resources | 193.39% | $7.54 |

RSG | Resolute Mining | 186.75% | $1.15 |

LTR | Liontown | 182.45% | $1.50 |

GMD | Genesis Minerals | 171.05% | $6.70 |

EVN | Evolution Mining | 158.07% | $12.47 |

VAU | Vault Minerals | 152.21% | $5.41 |

NEM | Newmont | 148.90% | $149.59 |

CMM | Capricorn Metals | 125.55% | $14.26names. |

Ticker | Company | % Chg | Price |

|---|---|---|---|

PMV | Premier Investments | -56.79% | $14.01 |

TWE | Treasury Wine Estates | -55.51% | $5.01 |

TLX | Telix Pharmaceuticals | -51.00% | $11.75 |

GYG | Guzman Y Gomez | -46.97% | $21.52 |

REH | Reece | -44.27% | $12.60 |

WTC | Wisetech Global | -43.05% | $68.51 |

JHX | James Hardie | -38.95% | $30.41 |

CSL | CSL | -37.25% | $176.05 |

XRO | Xero | -32.53% | $112.04 |

XYZ | Block | -29.34% | $97.86 |

Treasury Wine conference call highlights

[11:45 am] TWE just hosted a business update call to address this morning's earnings downgrade. The key highlights include:

1H26 EBIT forecast at $225–235m, with 2H26 expected to exceed 1H26.

Distributor inventories to be reduced: ~400,000 cases in China over two years from Q4 2025 and 300,000 cases in Americas (outside California) over two years from 2H26.

Leverage expected at 2.5x in 1H26, remaining above the 1.5–2x target range for roughly two years.

TWE Ascent transformation program targets $100m annual cost improvement over 2–3 years, with initial benefits from FY27, DAOU synergy benefit revised to $20m in FY26 ($10m this year).

On-market share buyback cancelled as US tariffs to increase Treasury Collective COGS by ~$10m, with minimal pricing impact.

Top ASX 200 gainers and losers

[10:38 am] Lithium and gold stocks are trading higher, while company specific announcements drive Treasury Wine, Austal and South32 sharply lower.

Ticker | Company | % Chg | Price |

|---|---|---|---|

IGO | IGO | 7.31% | $7.34 |

LTR | Liontown | 5.54% | $1.43 |

ZIP | Zip Co | 4.42% | $3.07 |

PNR | Pantoro Gold | 2.93% | $4.74 |

PLS | PLS Group | 2.84% | $3.99 |

L1G | L1 Group | 2.83% | $1.09 |

AAI | Alcoa Corporation | 2.77% | $70.39 |

XYZ | Block | 2.69% | $97.90 |

NEU | Neuren Pharmaceuticals | 2.36% | $19.96 |

OBM | Ora Banda Mining | 2.33% | $1.32 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

TWE | Treasury Wine Estates | -11.93% | $4.84 |

ASB | Austal | -11.62% | $5.93 |

DRO | Droneshield | -7.47% | $2.60 |

TLX | Telix Pharmaceuticals | -3.82% | $12.08 |

VEA | Viva Energy Group | -3.02% | $2.09 |

S32 | South32 | -2.62% | $3.35 |

360 | Life360 | -2.12% | $32.02 |

RMD | Resmed | -1.96% | $37.43 |

ALD | Ampol | -1.84% | $31.97 |

WDS | Woodside | -1.67% | $23.59 |

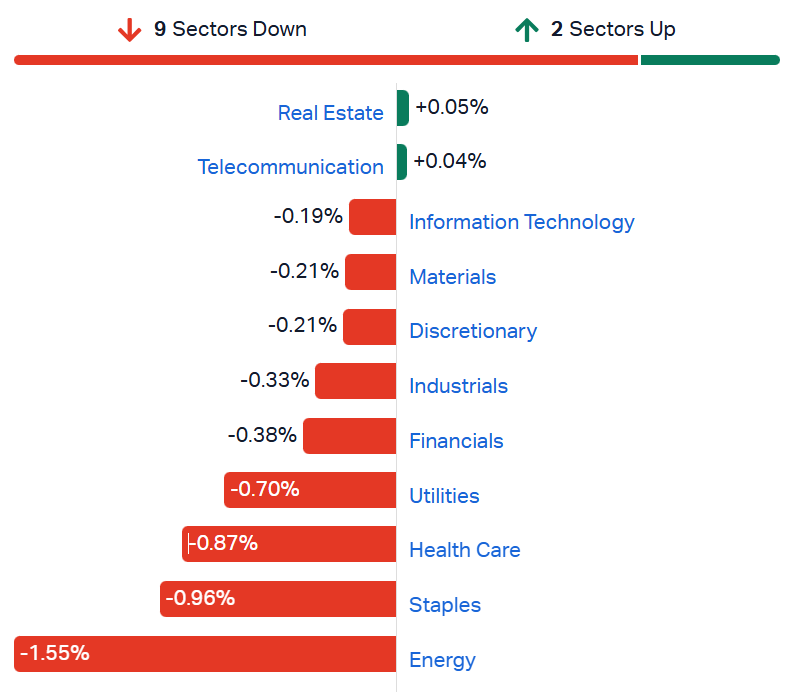

ASX 200 lower, not a good look

[10:31 am] ASX 200 trading 0.40% lower, now down for a third straight session and below the 200-day moving average. Energy stocks continue to trend lower against the backdrop of lower oil prices, while defensive sectors like Staples, Healthcare and Utilities also struggling.

ASX 200 sectors (Source: TradingView)

Graincorp dives 18% in early trade

[10:06 am] Graincorp opened 10.2% lower, currently down 18% to a fresh seven month low. I think the main driver of this gap down was its total receival volume guidance for FY26 (11.0-12.0m tonnes), which represents a sizeable miss vs. Macquarie estimates (Aug-25) of 12.2 million tonnes (approx 5.7% miss).

The guidance miss also follows a sizeable run up, with the stock rallying ~24% since mid-May.

Treasury Wines opens 15% lower

[10:00 am] Treasury Wine has opened 15% lower to $4.65, the lowest since September 2015. The stock is now down around 56% year-to-date.

Extremely oversold, with short interest sitting at 7.8%. However, the 1H26 guidance was a significant ~30% miss vs. consensus along with elevated leverage (3.0x vs. 1.5-2.0x target). Expect some wild swings today.

Boss Energy trading halted ahead of Honeymoon review

[9:55 am] Trading in Boss Energy has been paused pending the release of an announcement related to its Honeymoon uranium project.

This is going to be a big deal since the announcement will likely relate to the production downgrade announced back in July.

The announcement cut production and hiked cash costs, AISC and capex (23%, 41% and 64% above Macquarie estimates, respectively), resulting in a ~43% one-day selloff.

A key line from the announcement was: "Boss has identified potential challenges that may arise in achieving nameplate capacity ... largely due to the potential for less continuity of mineralisation and leachability."

Company page: Boss Energy (BOE)

Metal Powder Works inks partnership with Austal USA

[9:48 am] MPW and Austal USA will co-develop specialised metal powders for additive manufacturing, including projects at the US Navy’s Additive Manufacturing Center of Excellence. The partnership could lead to a commercial offtake agreement with agreed volumes, pricing and supply terms.

Company page: Metal Powder Works (MPW)

GrainCorp to exit Canadian JV, flags softer FY26 volumes

[9:41 am] GrainCorp will sell its GrainsConnect Canada joint venture and provides an update on a lower East Coast Australia winter harvest, highlighting margin pressure from high global supply.

GrainsConnect Canada sold to Parrish & Heimbecker for C$150m (A$164.5m), with completion expected 1H26, GrainCorp expects a A$5-10m loss on sale.

FY26 winter crop receivals in Queensland and northern NSW largely complete, but southern NSW and Victoria affected by weather

Total receival volumes for FY26 estimated at 11.0-12.0m tonnes, down from 13.3M tonnes in FY25.

Soft domestic demand and near-record international grain and oilseed production are expected to continue weighing on margins for grain handlers.

Macquarie (Aug-25) had forecast FY26 receivals of 12.2m tonnes, so the guidance today represents a modest miss vs estimates.

Company page: GrainCorp (GNC)

Treasury Wine Estates set to tumble

[9:32 am] It's about to get even uglier for Treasury Wine Estates. The company has guided to 1H26 EBIT of $225-235 million, well below consensus of $328 million amid distribution and pricing challenges for Penfolds and ongoing transformation costs.

1H26 EBIT guidance of $225-235m represents a 31-32% miss vs. consensus expectations

Penfolds expected to contribute ~$200m EBIT in the first half, with second half anticipated to be stronger following California distribution transition.

Elevated customer inventories in China and the US, alongside parallel import activity, are causing pricing pressure and operational disruption.

TWE is implementing the Ascent transformation program targeting $100m per annum in cost savings to support long-term competitiveness.

Leverage expected at 2.5x at 1H26, above the 1.5-2.0x target range, with multiple strategic and operational initiatives planned to maintain capital structure flexibility.

The stock might be down 51% year-to-date and trading at decade lows, but it doesn't get any uglier than this, with new 1H26 guidance that's 31-32% below consensus, 'anticipating' stronger 2H25 earnings and much higher-than-expected leverage.

Company page: Treasury Wine Estates (TWE)

Macmahon awarded $51m wind farm contract

[9:21 am] Macmahon subsidiary Decmil will deliver $51 million of works on the 18-turbine Waddi Windfarm, covering turbine bases, access tracks, cabling and a switch room, with work starting early 2026 and completing by early 2027.

That's already two contract announcements this morning!

Company page: Macmahon Holdings (MAH)

Cedar Woods lifts FY profit guidance (again)

[9:14 am] Cedar Woods Properties now expects FY NPAT to rise at least 20% vs. its prior guidance of at least 15%. The company says this has been supported by strong first-half sales price growth and historically high enquiry and sales volumes.

CWP shares are up 45% year-to-date following a series of earnings upgrades, including:

30-Apr: Upgraded FY25 NPAT growth guidance to 15%

26-Aug: Reported FY25 NPAT growth of 19%, guided to FY26 NPAT growth of 10%

29-Oct: Upgraded FY26 NPAT guidance to 15%

Company page: Cedar Woods Properties (CWP)

Macmahon secures major Byerwen contract extension

[9:09 am] Macmahon Holdings has been awarded a new three-year contract at the Byerwen coking coal mine worth $792 million, with an option to extend a further two years taking total value to $1.32 billion.

The contract award does read rather material for the $1.27 billion market cap Macmahon, though the company left its FY26 guidance unchanged.

Company page: Macmahon Holdings (MAH)

RBNZ eases bank capital rules to support competition

[9:06 am] The Reserve Bank of New Zealand has announced revised capital settings that materially lower equity requirements to reduce funding costs and favour smaller deposit takers.

Common equity requirements across the system will be eased by around NZ$5bn vs. current levels, reflecting the introduction of the Depositor Compensation Scheme and stronger supervision since 2019.

Capital reforms include lower common equity requirements, more granular risk weights, simpler capital instruments and closer alignment of big four bank settings with Australia.

Funding costs are expected to fall, with small and mid-sized deposit takers seeing proportionately larger benefits than major banks, supporting faster balance sheet growth and competition.

US PMIs cool as growth momentum fades and cost pressures re-emerge

[9:01 am] December flash PMI data show slowing activity across manufacturing and services, alongside renewed inflation pressure driven by services.

Both manufacturing and services PMIs missed expectations, with manufacturing at 51.8 (vs. 52 ests) and services at 52.9 (vs. 54 ests), marking five to six month lows and signalling softer end-year momentum.

Forward indicators weakened, with manufacturing new orders falling for the first time in a year and services new business sliding to a 20-month low.

Output growth moderated, as the manufacturing output index fell to a three-month low, reinforcing signs of cooling demand.

Labour signals were mixed, with manufacturing employment improving modestly but services hiring flat, delivering the weakest net jobs gain since April.

Inflation pressures picked up, particularly in services, where input costs and selling prices accelerated to multi-year highs, partly attributed to tariffs and rising labour costs.

US consumer resilient but uneven under the surface

[8:59 am] October US retail sales point to firmer underlying demand, led by core categories, despite a flat headline and pockets of weakness tied to housing and discretionary spend.

Headline retail sales rose a marginal 0.03% month-on-month, in line with expectations, while annual growth slowed to 3.5% vs. 4.2% in the previous month.

Underlying momentum was stronger, with sales excluding autos up 0.4% and ex-autos and fuel up 0.5%, both ahead of consensus and improving on September.

Core control group sales jumped 0.9%% month-on-month, the strongest result since June and a clear positive for near-term GDP tracking.

Strength was evident in categories previously affected by tariffs, including furniture, electronics and clothing, suggesting some release of pent-up demand.

Weakness persisted in autos, food services and building materials, reinforcing concerns around discretionary spending and ongoing softness in residential investment.

US nonfarm payrolls beat, unemployment jumps

[8:57 am] The November US jobs report delivered a modest payrolls beat, but revisions, rising unemployment and soft wages point to accelerating labour market softness.

Nonfarm payrolls rose 64k versus 50k expected, but prior months were heavily revised down, with August now negative and October showing a 105k decline, reinforcing a weaker underlying trend.

The unemployment rate climbed to 4.6%, the highest since September 2021, and has risen for four consecutive readings for the first time since the GFC era, alongside a participation rate of 62.5%.

Wage pressures eased further, with average hourly earnings up just 0.1% month-on-month and annual growth slowing to 3.5%.

Job gains were concentrated in defensive sectors such as health care, construction and social assistance, while cyclicals and government saw losses, including a further drop in federal employment following October’s sharp fall.

Markets interpreted the data is incrementally dovish, with the odds of a rate cut in January rising to 28% vs. 22% before the data release.

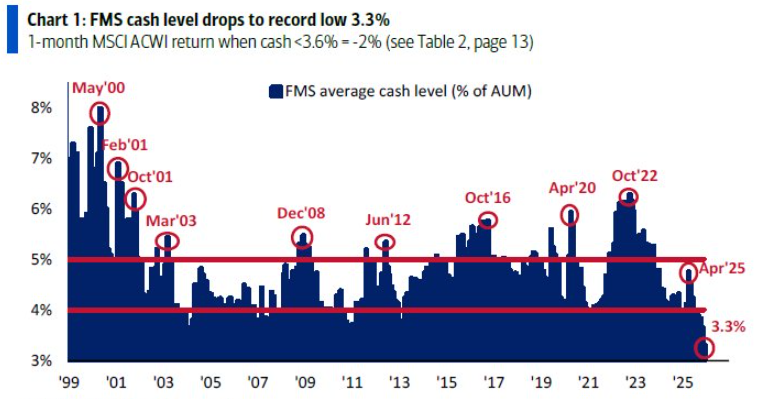

Fund managers lean bullish as risk appetite stretches

[8:55 am] BofA’s December Global Fund Manager Survey shows optimism on growth and profits at multi-year highs, with positioning increasingly stretched across equities and cyclicals. Key takeaways include:

Sentiment index rose to 7.4, the highest since July 2021, while global growth expectations and profit expectations hit their most optimistic levels since August 2021.

Bull and Bear Indicator climbed to 7.9, close to a sell signal, as cash allocations fell to a record-low 3.3 percent, signalling limited dry powder.

Allocations to cyclical risk assets surged to the highest since February 2022, with equities at a net 42 percent overweight, the strongest in a year, and commodities also seeing increased exposure.

Technology exposure rose to a net 21 percent overweight, the highest since July 2024, with Long Magnificent Seven the most crowded trade at 54 percent.

AI remains the top tail risk at 38 percent, while private credit is now viewed as the most likely source of a credit event at 40 percent, alongside expectations for higher long-term rates and a steeper yield curve.

FMS cash allocations hit a record low of 3.3%, at a time where sentiment is the highest in ~4 years and allocations to stocks/commodities is at the highest since Feb-22. It's clear that fund managers are fully loaded on equities and positioning is stretched. Not that a turn is imminent but it does pose a risk to markets moving forward.

Source: BofA Global Fund Manager Survey

SPIE buys Worley's Power Services

[8:47 am] SPIE Global Services Energy has agreed to acquire Worley Power Services, adding established power generation operations and maintenance capability and deepening its exposure to Australia’s energy transition.

Acquisition expands SPIE’s technical maintenance offering into power generation assets, strengthening its Australian platform where it has operated since 2012.

Worley Power Services brings scale and track record, with contracts across 27 power generation assets totalling more than 2,700MW and over 1,100km of gas pipelines.

Business has pivoted toward low-carbon assets over the past five years, aligning with coal retirements and driving demand from governments, utilities and infrastructure investors.

Power Services generated approximately €70m of revenue in FY25 with a workforce of 320 specialised technicians and engineers.

Company page: Worley (WOR)

South32 mothballs Mozal smelter

[8:45 am] South32 will place its Mozal Aluminium smelter into care and maintenance from March 2026, with manageable one-off costs and no change to FY26 production guidance.

Mozal to enter care and maintenance around 15 March 2026, while FY26 production guidance remains unchanged at 240kt on a South32 share basis.

One-off costs of around $60m (100% basis) reflect employee separation and contract terminations.

Ongoing care and maintenance costs ~$5m per annum.

Alumina previously supplied from Worsley to Mozal will be redirected to third-party customers, preserving volumes through the system.

Sales will be made under index-linked pricing options, reducing pricing risk and improving earnings visibility.

Overall, no big surprises here. Mozal is South32's lowest asset by NPV. Macquarie forecasts (Aug-25) had Mozal producing 240kt in FY26, followed by zero output thereafter.

Company page: South32 (S32)

Good morning!

[8:31 am] ASX 200 futures are up 10pts (+0.11%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks mostly lower but off worst levels

Nasdaq snapped a four-day losing streak amid a small bounce for Big Tech, though S&P 500 posted a third-straight decline

Brent crude down 2.5% to US$58.8, closing at the lowest since Feb 2021 following Russia-Ukraine peace headlines

US November nonfarm payrolls better-than-expected, unemployment rate jumps to 4.6% (vs. 4.4% ests), with markets pricing in slightly more rate cuts