ASX 200 Live Today - Tuesday, 24th March

The S&P/ASX 200 is set to bounce after Trump said the US and Iran have had "productive" talks. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, March 24. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 snaps three-day losing streak

[2:00 pm] Not the most encouraging kind of session, with the ASX 200 is up just 0.53% vs. session highs of 1.66%. There's clear skepticism around Trump's "very good and productive conversations" with Iran, particularly after Tehran denied any such talks shortly after. Brent crude is staging a modest bounce, up 3.7% to US$103.70 a barrel, and likely placing downward pressure on equities. The Aussie 10-year is also edging higher to 5.04%.

Oil markets may be drawing additional support from outside the Middle East, with Ukraine launching a drone strike on Russia's largest oil port at Primorsk, while an explosion hit the Valero refinery in Port Arthur, Texas, the world's largest independent petroleum refiner.

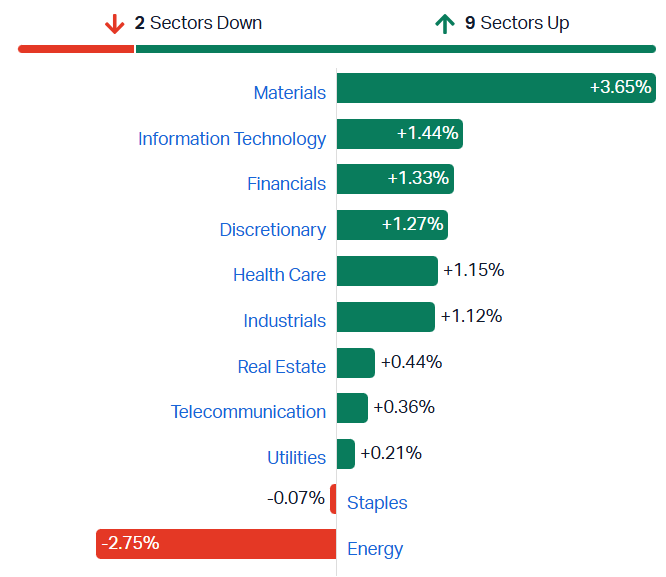

Overall, this bounce offers little comfort amid the recent weakness. Today's gains are largely carried by Materials, up 2.9% after closing below its 200-day moving average yesterday following a 22% selloff from 3 March highs. Early optimism is fading across the board. Tech rallied 1.44% at the open but has since reversed to trade down 0.80%, with Financials and Healthcare following a similar pattern.

That's a wrap. On a side note – I'm on leave for the next ~2 weeks. A few of my colleagues from Livewire will be looking after the blog, though it will likely wrap up a little earlier. As always, thanks for tuning in and hopefully markets don't unravel too much while I'm away.

What's catching a bid?

[1:43 pm] The below table observes the S&P/ASX 200 stocks recording the largest moves from the open.

The S&P/ASX 200 Energy Index dipped as much as 4.1% in early trade after Brent tumbled 8.6% overnight to US$100.05 a barrel. This marked oil's largest one-day selloff since the pandemic. However, prices have already started to bounce on Tuesday, up 3.4% to US$103.5. Likewise, the Energy Index is now approaching breakeven.

Ticker | Company | % Chg from Open | Price |

|---|---|---|---|

BPT | Beach Energy | 7.79% | $1.32 |

NHC | New Hope Corporation | 6.00% | $5.83 |

WDS | Woodside Energy Group | 4.86% | $34.61 |

VEA | Viva Energy Group | 4.49% | $2.45 |

WHC | Whitehaven Coal | 4.20% | $9.43 |

4DX | 4dMedical | 3.87% | $4.56 |

ZIM | Zimplats | 3.69% | $16.59 |

STO | Santos | 3.53% | $7.92 |

ALD | Ampol | 2.99% | $33.73 |

LSF | L1 Long Short Fund | 2.70% | $3.80 |

Santos quietly shuts down flagship Barossa LNG project for several weeks

[1:37 pm] Santos has taken its Darwin LNG plant offline for a multi-week shutdown, according to Boiling Cold.

Santos emailed local stakeholders on 19 March about a "planned shutdown" of its 3.7 million tonne per year Darwin LNG plant, with flaring expected to continue for several weeks until restart

The shutdown prevents Santos from capitalising on sky-high LNG prices for any uncontracted production capacity

The timing raises questions, as BW Offshore told investors just four weeks ago it expected the Barossa production vessel to reach full capacity by end of March, and appeared unaware of a planned shutdown

Darwin Port data shows only one LNG carrier has docked at the facility since 20 February, with a scheduled berthing of the Bishu Maru on 16 March later cancelled. Santos did not respond to questions

Macquarie reviews Iran conflict impact on Aussie discretionary retailers

[12:45 pm] With the conflict entering its fourth week, Macquarie assesses COGS headwinds from higher freight and diesel costs across Wesfarmers, JB Hi-Fi and Harvey Norman, finding limited near-term earnings risk but growing downside if the disruption persists.

At week three, earnings downside from higher freight and diesel costs is estimated at ~2-3% across the group. If the conflict continues for another three weeks, HVN faces the largest downside (~8%) given its exposure to categories such as furniture

WES is Macquarie's top pick in the space, with no clear historic correlation between input costs and share price, sales or margins, consistent with its value focus and Bunnings category diversification

JBH shows positive historic correlations between input costs and share price, sales and margins, reflecting its track record of managing margins, and sits in a net cash position

Macquarie lowers conviction on HVN given its higher housing-related category mix and weaker margin correlation to input costs. A key uncertainty for electronics-exposed names is the volume impact from "hyperinflation" driven by pre-existing memory chip shortages compounding with new conflict-related cost pressures

Balance sheets across all three are solid enough to withstand persistent pressures, though the broader outlook for discretionary has become more challenging given amplifying inflation concerns, softening sentiment and shifting RBA policy expectations

ASX 200 giving back early gains

[12:40 pm] So much for a relief rally, the S&P/ASX 200 is up just 0.35%, having given back most of an early 1.66% bounce. The optimism sparked by Trump's talk of "very good and productive conversations" with Iran is fading fast. Brent crude is 3.4% higher at US$103.45, clawing back some of last night's 8.6% plunge, while S&P 500 and Nasdaq futures have slipped 0.41% and 0.43% respectively.

Lithium futures open 5% higher

[12:10 pm] Lithium stocks are broadly higher, with Chinese lithium carbonate futures up 5.88% to 152,620 yuan a tonne.

Ticker | Company | % Chg | Price |

|---|---|---|---|

AGY | Argosy Minerals | 13.73% | $0.06 |

MIN | Mineral Resources | 5.51% | $53.41 |

PLS | Pls Group | 5.40% | $4.49 |

LTR | Liontown | 5.15% | $1.53 |

INR | Ioneer | 5.00% | $0.11 |

IGO | Igo | 4.78% | $7.24 |

WR1 | Winsome Resources | 4.76% | $0.33 |

LKE | Lake Resources N.L. | 4.62% | $0.07 |

5EA | 5E Advanced Materials | 4.35% | $0.24 |

CXO | Core Lithium | 3.59% | $0.20 |

DLI | Delta Lithium | 2.56% | $0.20 |

VUL | Vulcan Energy Resources | 2.25% | $2.96 |

GL1 | Global Lithium Resources | 1.01% | $0.50 |

By Stephanie Gardner

Gold stocks bounce

[12:02 am] Gold prices reversed a dip of 8.75%, closing the overnight session down 1.88% at US$4,407.35. Despite this, gold stocks are bouncing today breaking a 3-day losing streak of 17.08%.

Ticke | Company | % Chg | Price |

|---|---|---|---|

BMR | Ballymore Resources | 13.33% | $0.17 |

GMD | Genesis Minerals | 5.70% | $5.66 |

NEM | Newmont Corporation | 4.81% | $138.18 |

RMS | Ramelius Resources | 3.78% | $3.44 |

MEK | Meeka Metals | 3.33% | $0.16 |

WGX | Westgold Resources | 3.29% | $5.19 |

RRL | Regis Resources | 2.76% | $5.95 |

CMM | Capricorn Metals | 2.76% | $9.67 |

EMR | Emerald Resources | 2.74% | $4.70 |

NST | Northern Star Resources | 2.73% | $17.68 |

EVN | Evolution Mining | 1.61% | $11.69 |

ALK | Alkane Resources | 1.51% | $1.35 |

PRU | Perseus Mining | 1.43% | $4.63 |

VAU | Vault Minerals | 1.25% | $3.66 |

BGL | Bellevue Gold | 0.80% | $1.27 |

CYL | Catalyst Metals | 0.53% | $5.66 |

OBM | Ora Banda Mining | 0.48% | $1.06 |

BC8 | Black Cat Syndicate | 0.22% | $0.93 |

SBM | St. Barbara | 0.00% | $0.53 |

AMI | Aurelia Metals | 0.00% | $0.22 |

PNR | Pantoro Gold | 0.00% | $3.09 |

RSG | Resolute Mining | -0.41% | $1.22 |

By Stephanie Gardner

Copper stocks bounce higher

[11:38 am] Copper prices bounced 3.45% overnight to US$5.51 after a 3.89% drop in the previous session. Copper stocks are broadly higher with the S&P/ASX 200 Materials Index up 3.12%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

SFR | Sandfire Resources | 7.95% | $15.89 |

CSC | Capstone Copper | 6.98% | $10.27 |

29M | 29Metals | 6.35% | $0.34 |

MC2 | Marimaca Copper | 6.11% | $7.99 |

HGO | Hillgrove Resources | 5.88% | $0.04 |

HCH | Hot Chili | 5.53% | $1.24 |

AR1 | Austral Resources Australia | 4.35% | $0.07 |

FFM | Firefly Metals | 4.20% | $1.49 |

BHP | BHP Group | 3.25% | $48.64 |

AIS | Aeris Resources | 3.12% | $0.40 |

CYM | Cyprium Metals | 3.03% | $0.34 |

TAR | Taruga Minerals | -4.76% | $0.02 |

CPM | Cooper Metals | -6.67% | $0.04 |

By Stephanie Gardner

Uranium stocks broadly higher

[11:30 am] Uranium stocks are broadly higher, although Uranium futures fell to US$85 per pound, the lowest price since mid-January. The S&P/ASX 200 Energy Index is currently down 0.91%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

DEV | Devex Resources | 12.50% | $0.18 |

T92 | Terra Critical Minerals | 9.72% | $0.08 |

EL8 | Elevate Uranium | 4.00% | $0.26 |

PDN | Paladin Energy | 3.26% | $10.45 |

NXG | NexGen Energy | 2.50% | $15.96 |

BOE | Boss Energy | 1.84% | $1.49 |

DYL | Deep Yellow | 1.05% | $1.63 |

AEE | Aura Energy | 0.00% | $0.11 |

AGE | Alligator Energy | 0.00% | $0.03 |

BMN | Bannerman Energy | -0.30% | $3.34 |

PEN | Peninsula Energy | -1.85% | $0.53 |

LOT | Lotus Resources | -1.98% | $1.24 |

By Stephanie Gardner

Top ASX 200 gainers and losers

[11:20 am] Here are today's top gainers and losers on the S&P/ASX 200.

Ticker | Company | % Chg | Price |

|---|---|---|---|

SFR | Sandfire Resources | 9.24% | $16.08 |

CSC | Capstone Copper | 7.19% | $10.29 |

ZIM | Zimplats | 6.51% | $16.35 |

GMD | Genesis Minerals | 6.45% | $5.70 |

MIN | Mineral Resources | 5.91% | $53.61 |

DTR | Dateline Resources | 5.45% | $0.52 |

NEM | Newmont Corporation | 5.38% | $138.93 |

LTR | Liontown | 5.29% | $1.53 |

PLS | PLS Group | 5.28% | $4.49 |

OBM | Ora Banda Mining | 5.24% | $1.11 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

MCY | Mercury NZ | -6.70% | $5.29 |

EOS | Electro Optic Systems | -5.37% | $8.46 |

YAL | Yancoal Australia | -3.71% | $8.31 |

DRO | Droneshield | -3.39% | $3.70 |

SEK | Seek | -2.08% | $14.37 |

COH | Cochlear | -1.81% | $161.26 |

WDS | Woodside Energy Group | -1.70% | $34.20 |

STO | Santos | -1.55% | $7.93 |

SDF | Steadfast Group | -1.53% | $4.18 |

MFG | Magellan Financial Group | -1.52% | $10.06 |

By Stephanie Gardner

ASX 200 bounces, battered miners and tech lead

[10:12 am] ASX 200 up 1.22% in early trade, though already easing off session highs of 1.70%. Pretty much an 'opposite day', where battered miners and tech stocks are bouncing, while sectors that have outperformed (Energy, Staples, Utilities) are flat/lower. Despite the bounce, the index is still trading 2% lower over the last four sessions.

S&P/ASX 200 sectors (Source: Market Index)

Australia leverages LNG exports to secure fuel supplies from Asian partners

[9:54 am] The government is using Australia's position as a major LNG exporter to negotiate continued fuel flows from Asian refiners after six tankers bound for Australian ports were cancelled or deferred.

PM Albanese and Singapore's PM Wong jointly committed to maintaining trade flows of diesel, petroleum and LNG between the two countries, while deepening regional cooperation on energy supply chain resilience

Six fuel tankers from Malaysia, Singapore and South Korea were cancelled or deferred as their refineries grapple with the loss of Middle Eastern oil flows through the Strait of Hormuz

The government is leveraging Australia's status as a major LNG supplier as a bargaining tool, with officials noting South Korea sources almost all of its LNG from Australia, creating a "two-way street" incentive to keep fuel flowing

Energy Minister Bowen said some cancelled shipments have already been replaced by importers and refiners from other sources

Source: News.com

Myer delivers first combined half with Apparel Brands

[9:47 am] Myer reports its first earnings result that incorporates the Apparel Brands acquisition. Here are the key numbers for 1H26 (26 weeks ended 24 January 2026):

Total sales up 24.5% to $2.28bn vs. $2.10bn ests (9% beat)

Though pro forma sales growth was 2.1%

Underlying NPAT up 21.7% to $51.7m vs. $52m ests (1% miss)

Pro forma NPAT was 17.3% lower due to investment in strategic initiatives including store network changes, loyalty relaunch and integration costs

Interim dividend of 1.5 cents per share, at a 50.1% payout ratio

Net cash position of $287m with cash conversion of 134%, providing flexibility for ongoing integration

2H trading update (first seven weeks): group sales up 1.7%, with Myer Retail up 2.2% driven by double-digit growth in Home, Kids and Marketplace. Myer Apparel Brands sales 0.4% lower, though Just Jeans grew 9.8%

Myer shares are down 37% year-to-date and down 59.7% in the last twelve months, trading at the lowest since March 2021.

Company page: Myer (MYR)

Downer wins facilities management contract with Stockland

[9:38 am] The contract is valued at approximately $500 million over an initial five-year term commencing 1 August 2026, with an option to extend for a further five years.

Downer will deliver services across Stockland's operational assets including commercial offices, shopping centres, logistics facilities and land lease communities across NSW, Victoria, Queensland and WA.

Company page: Downer EDI (DOW)

Orica managing dual ammonia supply disruptions

[9:38 am] Orica has flagged an outage at a Western Australian supplier's ammonia plant alongside an unplanned outage at its own Kooragang Island facility in NSW, but does not expect a material financial impact.

Orica working to secure alternative supply from existing inventory and its global manufacturing network, while its own Kooragang facility is expected to be resolved shortly.

Company page: Orica (ORI)

Australian private sector contracts for first time in 18 months

[9:26 am] Flash PMI data for March showed a sharp deterioration in business conditions, with activity falling to its lowest since late 2023 amid surging costs and faltering demand linked to the Middle East conflict.

Composite PMI fell to 47.0 from 52.4 in February, ending a 17-month run of growth and marking the steepest contraction since December 2023.

Services activity dropped to 46.6, its first contraction in over two years

New orders fell for the first time since July 2024 as demand weakened, with the future output index dropping to a 20-month low amid concerns over demand fragility tied to the war

Input cost inflation surged to a three-year high at the composite level, with manufacturing cost pressures at a three-and-a-half year high driven by elevated raw material and fuel costs linked to the conflict and severe supply chain disruption

Firms passed through at least some of the cost burden, with selling price inflation rising to its highest since August 2023

Export sales were a bright spot, rising at the strongest pace in over three-and-a-half years led by manufacturing, while employment continued to expand modestly, hinting at some labour market resilience despite the broader deterioration

Source: S&P Global

Fuel crisis set to hit Australian construction costs

[9:23 am] Soaring petrochemical prices driven by the Middle East conflict are flowing through to critical building materials, with major suppliers already flagging steep increases effective mid-April.

An internal email from major supplier Iplex to Reece Plumbing customers revealed price hikes of:

HDPE Pipe and Fittings "up to 36%"

Twinwall Corrugated Stormwater Pipe and Fittings "up to 31%"

PVC Pipe and Fittings "up to 28.5%"

"Our industry is suffering from a lack of supply of raw material, fuel and freight options, which is driving costs upwards, adding immense pressures across the market."

"The degree of pricing volatility we are currently experiencing in our plastics category is highly unusual, and the trade environment remains very much uncertain"

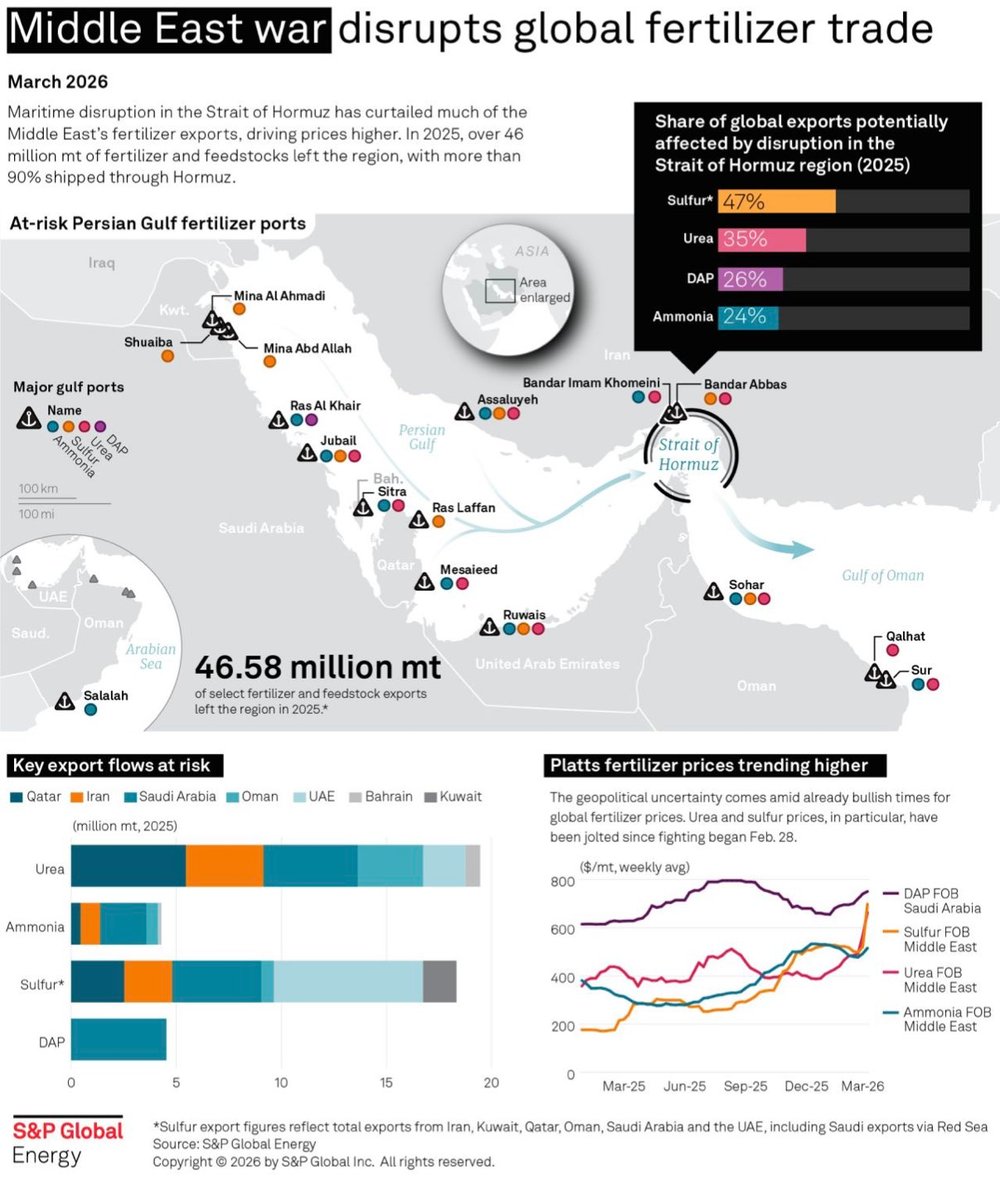

Strait of Hormuz impact on global fertiliser trade

[9:18 am] A slick infographic from S&P Global about how the Iran conflict is disrupting global fertiliser markets.

Source: S&P Global

OpenAI guarantees 17.5% minimum returns to private equity

[9:14 am] OpenAI is offering private equity firms preferred equity stakes with a guaranteed minimum return of 17.5%, along with early access to its newest models, as it courts firms including TPG and Advent for a ~$4bn joint venture at a ~$10bn pre-money valuation

The JV structures allow both companies to absorb high upfront costs of deploying engineers to customise models for clients, easing cost pressures ahead of potential public listings as early as this year.

This is a crazy guarantee given internal documents project OpenAI to lose approximately $14 billion in 2026, with cumulative losses expected to hit US$115 billion through 2029.

Gold trading like a risk asset

[9:08 am] Gold pared sharp losses after Trump postponed military strikes on Iranian energy infrastructure, but the metal's behaviour throughout the conflict has challenged its traditional safe-haven role.

Citi noted gold is "trading like a risk asset" during the current sell-off, with pro-cyclical behaviour "particularly extreme" given the large amount of momentum and retail buying over the past six months

BNP Paribas drew parallels to 2008, 2020 and 2022, noting gold initially fell in all three economic-shock cycles as investors sold assets to hold US dollars, but each period was followed by a sustained rally

Natixis flagged that some central banks are likely selling gold to defend currencies or fund energy purchases

TD Securities noted that USD surpluses previously being recycled into gold have been disrupted by the conflict's impact on Middle Eastern oil producers and consumers alike

The closure of the Strait of Hormuz has crimped Gulf states' dollar flows, while surging energy prices have raised the odds of rate hikes, adding further headwinds for non-yielding bullion

Source: Bloomberg

Global LNG exports hit six-month low as Middle East conflict chokes supply

[9:07 am] The war in Iran has severely disrupted global LNG flows, with Qatari export infrastructure damaged and the Strait of Hormuz effectively closed to shipments.

Global LNG shipments (10-day moving average) have fallen ~20% from the start of March to 1.1m tons, the lowest since September, driven primarily by lost Qatari and UAE volumes that transit the Strait of Hormuz

The Hormuz disruption is offsetting what had been a steady global supply build from new US and Canadian projects, with the strait accounting for roughly a fifth of global LNG supply

European gas storage sits at ~29% full vs. the five-year seasonal average of ~41%, while Europe's LNG imports are running 30% above the five-year average as the bloc scrambles for alternative supply

China's LNG imports are tracking 14% lower year-on-year, while Tehran has threatened to attack key regional infrastructure if the US follows through on threats against Iran's power plants, raising the risk of further escalation

Source: Bloomberg

Record short positions prime US equities for potential sharp rally

[9:05 am] Citadel Securities' Scott Rubner says one of the largest short positions on US stocks ever seen could unwind quickly if geopolitical tensions ease, creating the conditions for a significant bounce.

Hedge funds have aggressively shorted ETFs to reduce exposure, with ETF trading surging to ~35% of total volume (peaking near 47%), creating a large pool of rules-based short bets that could "flip" rapidly on any positive catalyst

Systematic strategies (CTAs, risk-parity, vol-targeting funds) have been heavy sellers since the S&P 500 broke below its 200-day moving average (~5,622), with Citadel's vol-control model cutting equity exposure by more than 20%, meaning the "skew is now back to the buy side"

Dealer positioning has flipped to long gamma following last week's $5tn+ options expiry, removing a key source of mechanical selling pressure that had been amplifying downside moves

Retail investors have remained resilient, recording only three days of net selling since the Iran conflict began, consistently buying dips and taking profits on rallies

Macro sentiment is "extremely bearish" across institutional clients, which Rubner views as a contrarian buy signal, noting the "short base is already at record levels but the right tail is under-owned"

Source: Bloomberg

Suspicious trading activity flagged minutes before Trump's Iran post

[9:03 am] Unusual volume spikes in both equity and oil futures occurred roughly 15 minutes before a market-moving social media post from President Trump, raising questions about potential information leakage.

S&P 500 e-Mini futures saw a sharp, isolated jump in volume at around 6:50am New York time, well outside normal premarket activity and one of the largest volume moments of the session to that point

WTI crude futures showed a similar spike at roughly the same time, with a distinct pickup in trading interrupting otherwise quiet conditions

At 7:05am, Trump posted on Truth Social that the US and Iran had held talks and that he was halting planned strikes on Iranian energy infrastructure, prompting S&P 500 futures to rally over 2.5% and WTI to drop nearly 6%

Source: CNBC

Energy executives flag rising risks from Middle East conflict at CERAWeek

[9:02 am] CERAWeek by S&P Global is the world's premier energy conference, where senior energy leaders are warning that the conflict's impact on global energy markets may be underappreciated, with supply disruption risks mounting.

Chevron CEO warned the Iran conflict has disrupted energy markets more than the Russia-Ukraine war, noting risks from a Strait of Hormuz closure are not fully priced in

TotalEnergies CEO cautioned that disruption to global energy flows lasting beyond 3-4 months could pose a "systemic" economic risk to the global economy

UAE's ADNOC CEO flagged that rising oil prices are already slowing economic growth "everywhere", while US Energy Secretary Wright said prices have not yet risen enough to cause significant demand destruction and urged producers to lift output

Constellation Energy CEO suggested the conflict could accelerate the reshoring of data centre and energy supply chain projects to the US as firms rethink building critical infrastructure in the Middle East

Occidental CEO said US oil production could peak as early as next year, though possibly not until 2031, likely around 15mbpd

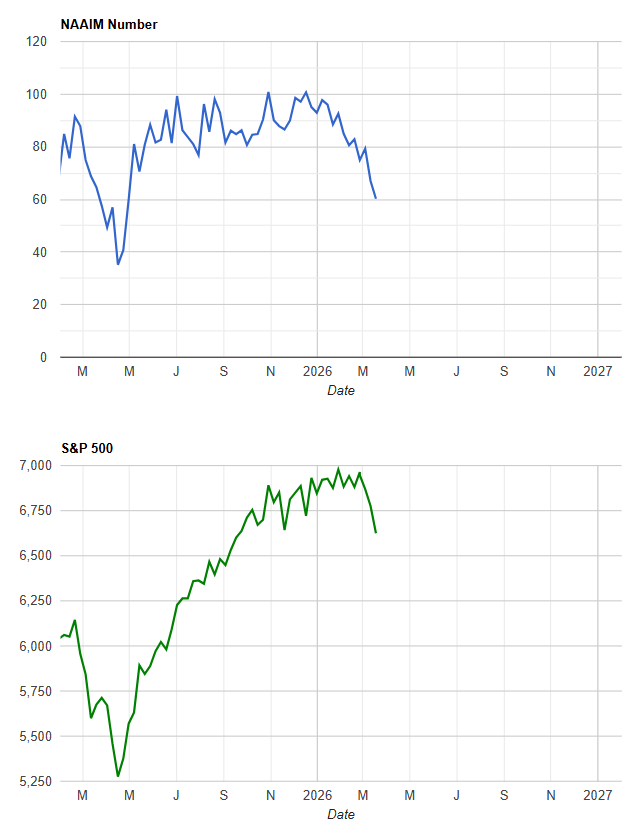

NAAIM Exposure Index tumbles

[8:57 am] The NAAIM Exposure Index represents the average exposure to US Equity markets reported by its members, who are active money managers. Every week, they are asked to provide a number which represents their overall equity exposure, varying from -200% (leveraged short) to 200% (leveraged long). Though you rarely see it go above 100 and below 30.

The NAAIM Exposure Index was sitting at 100.7 on 17 December, 2025 and has since tumbled to 60.2 as of 18 March.

NAAIM Exposure Index (Source: NAAIM)

Positioning and sentiment point to a crowded bearish trade

[8:55 am] Investor positioning and sentiment have deteriorated sharply, setting the stage for potential short squeezes even without full capitulation.

Deutsche Bank's aggregate equity positioning measure fell to its lowest since June 2025 (-0.25 standard deviations, 30th percentile), with discretionary positioning at a nine-month low not seen since the Iran bombing last June

Goldman Sachs flagged US equities were net sold for a fifth straight week, with CTAs selling ~$80bn in one week and ~$150bn over the past month, flipping to net short in the US

CTA short positioning is now around $35bn, approaching the Liberation Day low of ~$50bn (99th percentile short), levels that have historically marked bottoms and fuelled sharp upside squeezes

Sentiment indicators are deeply pessimistic: the AAII bull-bear spread dropped to -21.6% (lowest since May 2025) and the NAAIM Exposure Index fell to 60.24 from 92.58 in late January, the weakest reading since tariff fears last April

The lack of outright capitulation had been a key bearish argument, but the degree of de-risking is now seen as a tactical bounce catalyst, particularly if diplomatic off-ramp hopes gain further traction. The market is not positioned for positive news, exposing right-tail risk that could force institutional buying

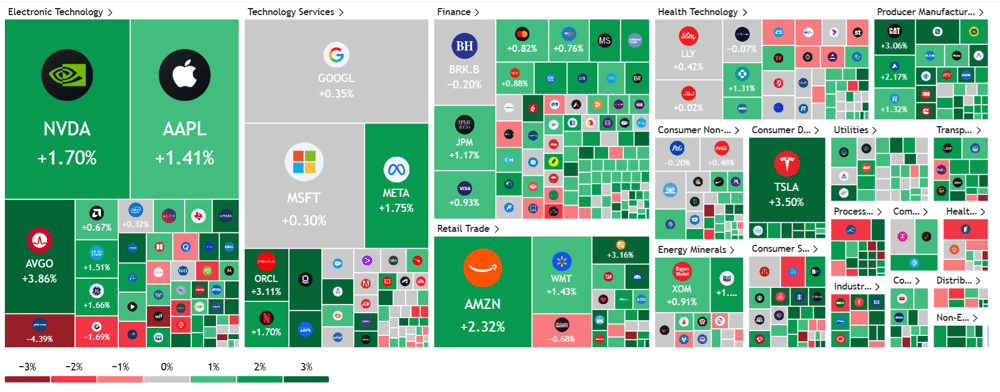

US indices higher, all sectors green

[8:50 am] A relatively encouraging overnight session after Trump posted on Truth Social that the US and Iran have had "very good and productive conversations", ordering a five-day postponement of strikes on Iranian energy infrastructure. Though Iran's Foreign Ministry denied any dialogue with Washington.

The S&P 500 rallied as much as 2.23% in early trade, but faded on the Iran comments, closing the session up 1.15%.

All S&P 500 sectors finished higher, though battered growth and cyclicals led the move, with notable gains from Discretionary (+2.46%), Materials (+1.49%) and Tech (+1.46%).

S&P 500 heatmap (Source: TradingView)

Good morning!

[8:35 am] ASX 200 futures are up 151 pts (+1.79%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks higher but faded early gains after Trump announced a five-day pause on strikes against Iranian infrastructure, citing "very good and productive conversations" with Iranian officials

Iran's Foreign Ministry denied any dialogue, sending stocks lower intraday

Gold experienced a massive reversal, closing the session (-1.8%) lower, off session lows of (-8.7%), which also marked the first touch of the 200-day moving average since Oct-23

Brent tumbled 8% but still holding above US$100 a barrel, marked the largest one-day dip since the pandemic