ASX 200 Live Today - Tuesday, 17th February

The S&P/ASX 200 is set to open higher after a relatively quiet overnight session, where the US market was closed for President's Day.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, February 17. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 higher, off best levels

[2:20 pm] That's all for today. ASX 200 up 0.36%, off session highs of 0.66%. Another results driven session, with BHP (+5.6%) strength offset by weakness from Real Estate (-0.8%), Tech (-0.8%), Energy (-0.5%) and Utilities (-0.5%). Not the most encouraging session as benchmarks like the Small Ords (-0.34%) and Emerging Companies (-0.50%) trading lower. I think the index is pretty lucky to have CBA rip ~12% in the last five sessions and BHP rally to fresh all-time highs today. VanEck have an Australian Equal-weight ETF (MVW) that's currently down 1.0% year-to-date vs. the official benchmark that's up 3.0%. Overall, the index does feel a little bearish in the absence of banks and miners. Wednesday is a relatively tame day for big hitting reporters, with notable results due from names like The Lottery Corp, Santos and Suncorp.

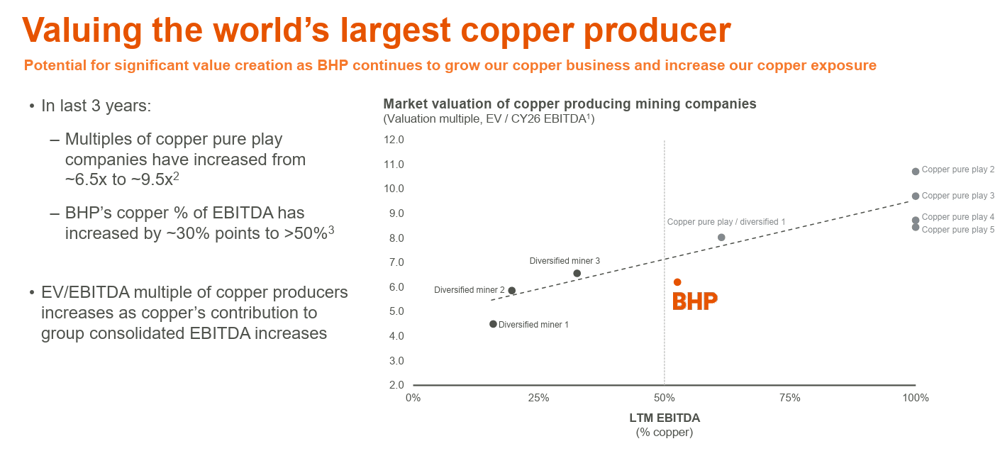

Interesting slides from BHP's 1H26 results presentation

[1:30 pm] A few interesting slides from the BHP result. The below highlights how BHP's valuation is caught in the middle, either a very expensive diversified miner or a cheap copper play.

Source: BHP 1H26 results presentation

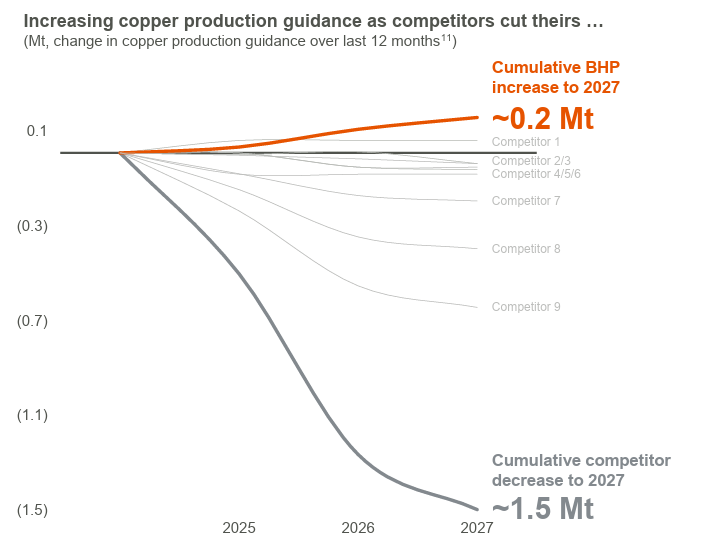

A great chart about the state of play for copper, where most large producers are struggling to grow output.

Source: BHP 1H26 results presentation

Gold stocks broadly lower

[12:11 pm] Gold stocks are mostly down 1-2% after gold prices eased around 1.0% to US$4,990/oz overnight. The S&P/ASX All Ords Gold Index is down 1.2% and trading 9% away from its 29 Jan all-time high.

Ticker | Company | % Chg | Price |

|---|---|---|---|

WGX | Westgold Resources | -2.48% | $7.08 |

GMD | Genesis Minerals | -2.37% | $7.21 |

OBM | Ora Banda Mining | -2.29% | $1.28 |

PRU | Perseus Mining | -2.01% | $5.61 |

RMS | Ramelius Resources | -1.74% | $4.51 |

EVN | Evolution Mining | -1.65% | $14.94 |

VAU | Vault Minerals | -1.63% | $5.44 |

CYL | Catalyst Metals | -1.46% | $7.44 |

NST | Northern Star Resources | -1.25% | $28.11 |

BGL | Bellevue Gold | -1.13% | $1.76 |

CMM | Capricorn Metals | -0.86% | $13.33 |

NEM | Newmont | -0.60% | $172.56 |

RRL | Regis Resources | -0.60% | $8.23 |

RSG | Resolute Mining | -0.56% | $1.43 |

EMR | Emerald Resources | -0.54% | $6.41 |

ALK | Alkane Resources | 0.00% | $1.76 |

Reliance Worldwide 1H26 earnings call highlights

[12:06 pm] Reliance shares dipped as much as 9.8% in early trade, currently down 5.4% after reporting a slightly weaker-than-expected first half result, where most key metrics missed market expectations by 3-7%. Some of the key highlights from the earnings call include:

Copper exposure is the critical near-term risk with ~$900,000 EBITDA impact per $100/t LME movement, but management has a clear multi-year mitigation plan involving material substitution projects (polymers, stainless steel) aim to structurally eliminate copper as a material P&L item by FY29

Americas growth guidance is price-driven, not volume recovery, suggesting underlying demand remains weak despite freeze events providing temporary tailwinds, while tariff headwinds of $5-7M will persist through FY27 until Mexico facility is operational

Cost-out program is delivering $8-10M in FY26 with further savings expected beyond current Poland and Mexico projects, but management acknowledges elevated cost base is structural rather than temporary, requiring ongoing discipline

APAC region is underperforming at mid-single digit EBITDA margins and "requires a couple of years" to hit targets, representing an execution risk alongside the copper transition and tariff mitigation timeline all converging in FY27-29

Baby Bunting 1H26 earnings call highlights

[12:03 pm] Baby Bunting shares are up 9.5% ($2.41) after reporting a solid first half result and slight upgrade to its FY26 earnings guidance. Here are some of the key takeaways from the earnings call:

Store refurbishment strategy is working with 15-25% sales uplifts in year one, but small format stores are underperforming due to poor foot traffic conversion rather than competition, raising questions about location strategy and format viability

Capital expenditure is accelerating in the near term (upper end of guidance for FY26) but management expects per-store costs to decline as the rollout matures, with operating leverage delivering ~200bps margin improvement from FY24 base

Medium-term financial targets are ambitious: EBITDA margin above 10%, gross margin reaching 42% by FY27, supported by 10-15 refurbishments annually and potential network expansion of ~80 stores (44 large format, up to 37 small format pending pilot results)

Bendigo’s small beat fails to shift consensus

[11:29 am] Bendigo and Adelaide Bank's H1 result on Monday came in modestly ahead of expectations, supported by improved NIM and healthy credit, but lending volumes contracted and the bank flagged higher compliance and investment spend. BEN rallied modestly in early trade but reversed to close down 3.0% at $11.20 on the day of the result.

JPMorgan retained Neutral, raised target from $10.30 to $10.50 (up 1.9%). It said the earnings beat was helped by a provision benefit and sees capital build leaning on the underwritten Dividend Reinvestment Plan.

UBS retained Neutral, target unchanged at $10.95. It noted core margin improvement despite weaker lending, but expects compliance spend and the push to rebuild growth to keep pricing pressure elevated.

Shares are up 0.8% at $11.29 this morning.

By Warren Masilamony | Company page: (BEN)

Analysts split on Ansell, despite H1 earnings beat

[11:04 am] Ansell delivered a H1 earnings beat on Monday, despite softer revenue, with margin expansion offsetting subdued demand. FY26 guidance was reaffirmed, with brokers flagging margin expansion from Kimberly-Clark synergies, plus pricing actions now activated to offset an estimated $80m annualised US tariff cost. Shares jumped 3.8% on the results announcement at $32.4.

Morgan Stanley retained Equal Weight, lowered target from $36.70 to $34.40 (down 6.3%). It argued the beat was driven mainly by pricing and warned volume risk skews to the downside, awaiting clearer H2 volume exit trends.

RBC Capital Markets retained Outperform, target unchanged at $41.00. It said efficiency gains underpinned guidance retention and expects positive organic growth to return in H2.

UBS retained Neutral, lowered target from $36.00 to $35.60 (down 1.1%). It noted margin uplift offset weak sales but said most restructuring benefits are now captured, with CEO transition adding uncertainty and organic growth needed to sustain earnings. By Warren Masilamony | Company page: (ANN)

Analysts upgrade JB Hi-Fi

[10:44 am] JB Hi Fi delivered a solid H1 result that was broadly in line with expectations, with earnings slightly ahead of some forecasts and margins holding up despite heavy promotional activity. Shares initially opened 10.5% lower but rallied through the day to close up +7.5%.

Morgans upgraded to Hold from Trim, lowered target from $95.00 to $87.00 (down 8.4%). It noted the 1.1% NPAT beat and margin control despite promotions and upgraded mainly because valuation now looks more reasonable.

UBS upgraded to Buy from Neutral, target unchanged at $94.00. It framed the 1.1% NPAT beat as modest but highlighted upside in The Good Guys margins, with valuation de-rating improving risk reward.

JBH is up 7.4% at $82.4 in morning trade.

By Warren Masilamony | Company page: (JBH)

Top ASX 200 gainers and losers

[10:13 am] Judo, BHP and Deterra trading sharply higher after reporting results this morning, JB Hi-Fi also continuing to trend higher after a solid 1H26 on Monday. Meanwhile, tech stocks are giving back some of yesterday's bounce.

Ticker | Company | % Chg | Price |

|---|---|---|---|

JDO | Judo Capital | 10.00% | $2.04 |

JBH | JB Hi-Fi | 7.00% | $88.17 |

BHP | BHP Group | 6.04% | $53.40 |

PXA | Pexa Group | 4.15% | $14.45 |

DRR | Deterra Royalties | 3.86% | $4.31 |

S32 | South32 | 2.95% | $4.54 |

ANN | Ansell | 2.22% | $33.20 |

GNE | Genesis Energy | 1.94% | $2.10 |

NCK | Nick Scali | 1.79% | $18.76 |

ALK | Alkane Resources | 1.42% | $1.78 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

RWC | Reliance Worldwide Corp | -7.53% | $3.56 |

SNZ | Summerset Group | -6.11% | $8.92 |

CEN | Contact Energy | -5.29% | $7.87 |

WTC | Wisetech | -5.01% | $45.70 |

SGM | Sims | -4.65% | $20.29 |

NHC | New Hope Corporation | -3.98% | $4.58 |

TLX | Telix Pharmaceuticals | -3.48% | $8.33 |

PNI | Pinnacle Investment Management | -3.32% | $15.42 |

XRO | Xero | -2.92% | $76.75 |

CPU | Computershare | -2.49% | $30.90 |

BHP opens at all-time highs

[10:00 am] The market is loving the result, with BHP shares opening 5.5% higher to a record high of $53.

A very tame day for results, with most reporters higher at the open, including Baby Bunting (+4.0%), Judo (+6.4%), Qualitas (+1.9%), Seek (+4.5%) and Sims (+0.7%).

BHP beats on strong margins and copper dominance

[9:55 am] BHP delivered a solid first half with underlying earnings and revenue exceeding expectations, driven by record copper performance and disciplined cost control that offset currency and inflation headwinds.

Revenue up 11% to $27.9bn vs $27.34bn ests (2% beat)

Underlying EBITDA up 25% to $15.5bn vs $15.11bn ests (3% beat)

Profit from operations up 34% to $12.3bn vs $11.93bn ests (3% beat)

Underlying EPS of $1.22 vs $1.21 ests (1% beat)

Interim dividend of $0.73 per share with dividend payout ratio of 60% vs. Macquarie ests of 69 cps (5.7% beat)

Adjusted effective tax rate of 36.6% (43.0% including royalties)

Divisional metrics of interest:

Copper contributed record 51% of group underlying EBITDA at $8.0bn (prior 39%), first time copper generated majority of group EBITDA with 66% margin (up 12 percentage points)

Escondida and Copper South America unit costs down 16% and 53% respectively, supported by increased gold and silver byproduct credits

WAIO strengthened position as lowest cost major iron ore producer globally

At a glance, a very solid 1H26 result that eked out a small beat across most key metrics. A fair bit to unpack, including closely watched factors like CMRG negotiation, commentary on Jansen's capex blowout and dividend/gearing guidance. Will take a closer look after market open.

Company page: BHP Group (BHP)

SEEK tightens guidance after strong AI-driven growth

[9:45 am] SEEK delivered a strong first half with double-digit revenue growth and margin expansion driven by AI-enabled pricing and ad tiers, though offset by a significant Zhaopin impairment.

Net revenue up 12% to $600.9m vs $600.4m ests (in-line)

EBITDA up 19% to $267.1m vs $267.4m ests (in-line)

Adjusted NPAT up 35% to $104.1m vs $103.6m ests (in-line)

Interim dividend up 13% to 27 cps vs. Morgans ests of 26 cps (3.8% beat)

Reported loss of $178m for continuing operations and $250m total operations due to $356m Zhaopin impairment, reducing investment value to $182m from $529m

Divisional metrics of interest:

ANZ revenue up 14% with yield up 17% driven by AI-enabled ad tiers and outcome-based pricing, however job ad volumes down 2%

Asia revenue up 4% (up 1% constant currency) with yield up 17%, paid job ad volumes down 14% impacted by freemium launches and weaker markets

Placement leadership in Australia increased to 4.9 times nearest competitor

Guidance:

FY26 adjusted profit guidance tightened to $195-215m from prior $190-220m (unchanged at the midpoint)

FY26 net revenue guidance tightened to $1.19-1.23bn from prior $1.15-1.25bn (up 0.8% at the midpoint)

FY26 EBITDA guidance lifted to $530-550m from prior $510-550m (up 1.9% at the midpoint)

SEEK shares have tumbled 41% amid the ongoing software selloff, trading at levels not seen since June 2020. A bit oversold heading into the result, though the stock did bounce 7.9% on Monday.

Company page: SEEK (SEK)

Baby Bunting lifts guidance on store refurb success

[9:38 am] Baby Bunting delivered a strong first half with sales and margins exceeding expectations, driving an upgrade to full year guidance as store refurbishments deliver top-end uplifts.

Revenue up 7% to $271.4m vs $266.1m ests (2% beat)

Pro forma NPAT up 4% to $5.0m vs guidance of $4.5-5.5m

Underlying NPAT up 44% to $7.2m

Comparable store sales up 4.7% vs pcp, exceeding 1H guidance of 2% to 3%

Gross margin up 124 basis points to 41.0%, in line with FY26 target

Store of the Future refurbishments delivered 25% sales uplift, top end of 15% to 25% guidance range, with nine stores refurbished

Trading update and guidance commentary:

First seven weeks of 2H saw comparable sales up 6.7%, with Australia up 6.4% and New Zealand up 17.8%

FY26 pro forma NPAT guidance narrowed to $17.5-19.5m from prior $17.0-20m vs $18.1m ests (midpoint unchanged, 2.2% beat vs. ests)

FY26 comparable store sales growth guidance lifted to 5-7% from prior 4-6%

Capex guidance lifted to $41-43m vs $26.8m ests (56% above)

2H26 pro forma NPAT guidance maintained at $12.5-14.5m

A few moving parts to this result, with BBN shares down around 31% since early October. 1H26 numbers either in-line or above company guidance, with gross margins (41.0%) tracking ahead of some analyst estimates (Morgans ests at 40.7%). Encouraging same store sales guidance increase (most analysts in-line with the prior 4-6% guidance), though capex stands as a big surprise.

Company page: Baby Bunting Group (BBN)

Sims beats on strong lifecycle services and cost control

[9:29 am] Sims delivered a solid first half result with underlying earnings well ahead of expectations, driven by strong performances in lifecycle services and disciplined cost management despite difficult ferrous markets.

Revenue up 4% to $3.78bn vs $3.84bn ests (2% miss)

Underlying EBIT up 66% to $121.1m vs $104.0m ests (16% beat)

Underlying EBITDA up 7% to $249.8m vs $234.1m ests (7% beat)

Underlying NPAT up 71% to $60.0m vs $59.7m ests (in-line)

Interim dividend of 14 cps vs 13 cps ests (7.6% beat)

Lifecycle services delivered at top end of guidance range, benefiting from extraordinary demand for AI chips driving prices for high-quality used DDR4 chips and hardware

North America metals achieved margin expansion through disciplined execution despite softer ferrous conditions, SAR JV benefited from higher non-ferrous retail exposure

ANZ performance above guidance range despite difficult ferrous conditions from elevated Chinese steel exports, aided by strong non-ferrous market

However, outlook commentary was a little mixed:

"AI-driven migration to DDR5 chips is constraining DDR4 chip supply, while legacy demand remains resilient across hyperscaler, automotive and consumer applications. This structural imbalance is expected to continue supporting secondary-market pricing."

"Tariffs are expected to continue to support US ferrous and non-ferrous demand, as domestic steel and aluminium industries remain protected and local demand for ferrous scrap is sustained."

"Chinese exports remain the strongest headwind, with record-high Chinese steel exports likely to keep ferrous prices muted in markets outside the USA. This will continue to challenge NAM, ANZ, and SAR ferrous exports, as well as ANZ’s domestic market."

Company page: Sims (SGM)

Judo Bank beats on earnings, upbeat on NIM guidance

[9:25 am] Judo Bank delivered a strong first half with profit growth accelerating and greater confidence in topping its NIM guidance on improved deposit costs and lending momentum.

PBT up 53% to $86.5m vs $84.8m ests (2% beat)

NPAT up 46% to $59.9m vs $59.7m ests (in line)

Net interest margin of 3.03% vs 3.02% ests (1 bp beat)

Gross loans and advances up 7% over half and 15% year on year to $13.4bn driven by differentiated customer proposition and improved productivity

FY26 GLA guidance lifted to $14.4-14.7bn from prior $14.2-14.7bn (0.7% upgrade)

2H26 NIM guidance upgraded to around 3.15% vs. prior ~3.1%, reflecting improved cost of new term deposits

FY26 PBT guidance reaffirmed at $180m to $190m vs $187.9m ests

Analysts have been rather upbeat heading into the result, with Citi noting: "While we expect that management will reiterate guidance at this result, we note recent movement in TD pricing vs swaps could drive a better-than-expected exit NIM and outlook commentary."

Company page: Judo Capital Holdings (JDO)

SRG Global upgrades guidance despite earnings miss

[9:20 am] SRG Global delivered strong revenue growth and upgraded full year guidance after TAMS acquisition performed to plan, though first half earnings came in below expectations. It's worth noting that the stock does not receive much institutional coverage, so estimates may be outdated/volatile.

Revenue up 20% to $743.9m

Adjusted EBITDA up 20% to $71.0m vs $74.3m ests (4% miss)

NPATA of $33.7m vs $37.9m ests (11% miss)

Interim dividend up 20% to 3.0 cps

Strong cash conversion of 97% with net debt reduced to $21.2m from proforma $52.5m post TAMS acquisition in October

TAMS delivered to business case in first two months and now fully integrated

Record work in hand of $4.2bn and opportunity pipeline of $11.5bn across diverse sectors

FY26 EBITDA guidance upgraded to $164-168m vs. prior $163m and $164.1m ests (up 1.8% vs. prior and 1.2% beat)

FY26 EBITA guidance upgraded to $126-130m vs. prior $125m and $125.9m ests (up 2.4% vs. prior and 1.7% beat)

Company page: SRG Global (SRG)

Bellevue Gold approves paste plant, lifts capex guidance

[9:17 am] Bellevue Gold has approved construction of a new paste plant to support high-grade mining areas, lifting FY26 growth capex by around 30%.

FY26 growth capital guidance lifted to $105-115m vs. prior $80-90m

New 120m3/hr wet paste plant approved for Deacon and Deacon North high-grade mining areas at estimated cost of $35-40m (including 10% contingency)

Construction commencing FY26 with completion mid FY27, paste filling to start immediately after

Capital spend during CY26 to be funded from operational cash flows

FY26 production and AISC guidance unchanged despite paste plant construction

Company page: Bellevue Gold (BGL)

Macmahon beats on revenue but earnings miss slightly

[9:14 am] Macmahon delivered strong revenue and earnings growth in the first half with civil infrastructure and underground mining driving performance, though earnings came in slightly below expectations.

Revenue up 11% to $1.31bn vs $1.30bn ests (1% beat)

Underlying NPATA up 17% to $54.9m vs $58.9m ests (7% miss)

EBITA up 17% to $91.0m vs $92.4m ests (2% miss)

Interim dividend up 73% to 0.95 cps

Order book of $5.1bn with $2.5bn secured for FY26

Free cash flow of $39.3m impacted by $20m tax payment as group becomes taxpayer for first time

FY26 guidance reaffirmed: Revenue of $2.6-2.8bn and EBITA of $180-195m vs $196.3m ests (4.4% miss)

Macmahon is an interesting one, given the industrial stock has run ~128% in the past twelve months. Though its trailing price-to-earnings remains a modest ~18x.

Company page: Macmahon Holdings (MAH)

Challenger misses on earnings despite record annuity sales

[9:05 am] Challenger delivered a modest earnings increase in the first half but fell short of expectations, though record annuity sales and strategic partnerships signal growth momentum.

Normalised NPAT up 2% to $229m vs $235.5m ests (3% miss)

Normalised NPBT of $327m vs $341.5m ests (4% miss)

Normalised EPS up 2% to 33.3 cents vs 32.0 cents ests (4% beat)

Interim dividend up 7% to 15.5 cps vs. 14.6 cents ests (6.1% beat)

Record annuity sales of $3.8bn, up 32%, with annuity book growing 7.4%

Normalised ROE of 11.4% above target but below 11.9% ests (50 bp miss)

Intends to buy back up to $150m of shares on market subject to conditions and regulatory approval

FY26 normalised EPS guidance reaffirmed at 66 to 72 cents

Company page: Challenger (CGF)

Reliance Worldwide hit by US tariffs and weak demand

[9:04 am] Reliance Worldwide posted a challenging first half with earnings missing estimates as US tariffs and subdued residential markets weighed on performance.

Revenue down 5% to US$645.4m vs US$665.6m ests (3% miss)

Underlying NPAT down 31% to US$52.2m vs US$56.4m ests (7% miss)

Adjusted EBITDA down 23% to US$111.4m vs US$118.4m ests (6% miss)

Interim dividend of 2.0 US cents per share (in-line) plus on-market buyback of US$15.3m

US tariffs expected to impact full year earnings by US$25-30m with impact weighted to first half, mitigation actions including product sourcing shifts and pricing adjustments to flow through in second half

Strong cash generation with net debt reduced by US$21.2m despite earnings pressure

Second half external sales expected up mid-single digits on pcp (adjusting for exit from low-margin Canadian products and Spanish manufacturing sale), full year FY26 sales broadly flat

Company page: Reliance Worldwide (RWC)

Qualitas beats on credit fund strength

[9:00 am] Qualitas delivered a solid first half result with earnings beating across the board as credit fund deployment accelerates.

Revenue up 54% to $62.4m vs $54.9m ests (14% beat)

Normalised NPAT up 6% to $21.1m vs $19.9m ests (6% beat)

Normalised PBT of $30.2m vs $28.5m ests (6% beat)

Interim dividend of 3.5 cents per share

Credit fund performance fees rising as funds mature with recognition and cash receipts becoming more consistent

Multi-dwelling residential market momentum has accelerated meaningfully over the past six months, expected to continue as demand shifts to affordable housing segments

FY26 NPBT guidance reaffirmed at $60m to $66m, representing 13% to 25% growth on FY25

Company page: Qualitas (QAL)

Praemium restructures technology division

[8:51 am] Praemium is cutting approximately 15% of its Australia-based workforce and closing Armenian software development operations by end of FY26, targeting $9 million in annual technology salary savings.

Overall annual technology salary budget (ex-incentives) expected to reduce by ~A$9m

Armenia closure to cut further ~13% of headcount, reducing direct staff salaries by ~$3.5m

FY26 savings offset by redundancy costs of ~$3.3m

Company page: Praemium (PPS)

Ray Dalio: Post-1945 world order officially dead as leaders declare era of "great power politics"

[8:50 am] In an X post, Ray Dalio wrote how global leaders at Munich Security Conference unanimously confirmed the breakdown of the post-war order. Dalio warned that we've entered Stage 6 of the Big Cycle where "there are no rules, might is right, and there is a clash of great powers."

German Chancellor Friedrich Merz: "The world order as it has stood for decades no longer exists", freedom "is no longer a given" in this new era of great power politics

French President Emmanuel Macron said Europe's old security structures tied to previous world order don't exist and Europe must prepare for war, US Secretary of State Marco Rubio confirmed we're in a "new geopolitics era"

Dalio's Stage 6 framework explains how international relations revert to "law of the jungle" when no governing body (UN, League of Nations) has more power than individual countries, conflicts escalate through five war types: trade/economic, technology, capital, geopolitical, and military

Greatest military war risk exists when both parties have comparable military power and irreconcilable existential differences, currently most explosive conflict is US-China over Taiwan

Historical parallel to 1930s: economic depression led to populist/autocratic leaders, tariff wars, and decade of economic/technological/geopolitical conflict before hot wars began—Germany and Japan used military expansion to seize resources when economic conditions became desperate

Source: X

Fund manager who beat 99% of peers says most software stocks face existential AI threat

[8:47 am] A Bloomberg article highlights how Nick Evans of Polar Capital dumped nearly all software holdings and warns most firms won't survive the AI disruption, comparing the looming shakeout to newspapers in the 2000s.

Evans' $12bn global technology fund beat 99% of peers over one year and 97% over five years after selling software stocks early

Sold all application software holdings except small Microsoft position and call options, exiting SAP, ServiceNow, Adobe and HubSpot: "We won't go back to these companies"

AI coding tools now advanced enough to replicate and modify existing software, meaning established firms face competition from their own clients building internal tools plus AI startups

Increased holdings in infrastructure software (Cloudflare, Snowflake) which saw soaring demand, while maintaining neutral view on cybersecurity as no immediate AI threat

Warns current software prices don't reflect "terminal value uncertainty or pressure on free cash flow" as companies may need to pay more cash compensation to offset falling equity value for employees

Source: Bloomberg

Extreme bullish gold bets pile up despite historic volatility

[8:43 am] Traders are building deep out-of-the-money call spreads on gold at unprecedented levels, betting on a near-tripling of prices by December despite recent sharp corrections.

December $15,000/$20,000 call spreads have grown to ~11,000 contracts even with gold consolidating near US$5,000, following late January's brief peak above US$5,600 and subsequent largest one-day drop in decades

State Street's Aakash Doshi calls the trade's size "striking" given distance from current prices, describing it as a "cheap lottery ticket" that limits upside but reduces cost

Gold has doubled since early 2024 driven by speculative flows, geopolitical tensions, Fed independence concerns, and diversification away from currencies and sovereign bonds

For spreads to expire in-the-money, prices would need to nearly triple to above $15,000 by December. This structure allows traders to exit on sharp rallies or hold through expiry

Dollar shorts hit 14-year extreme as tech short interest surges

[8:40 am] Investor positioning has swung to extreme bearish bets across multiple markets, with dollar shorts at their most negative since 2012 and tech stocks seeing record short exposure.

Dollar net short positioning reached highest level since January 2012 (earliest available data), with fund manager exposure now below April 2025 lows despite easing Fed independence concerns following Kevin Warsh's nomination as Chair

Further US labour market deterioration cited as key downside risk for the dollar by survey respondents

Tech sector short interest hitting multi-year highs, with XLK ETF at 1.8% (6-year high, doubled in recent weeks), Microsoft shorts at 0.8% of free float (near 5-year high of 58m shares), Salesforce at 1.9% (100th percentile vs. recent years)

US Software ETF short interest spiked to ~19% last week, near record levels, raising short-squeeze risk as crowded positioning builds

WTI crude net short positions jumped to 202,928 contracts (week of 10 Feb) from 196,804 at start of 2026, approaching October 2025's 8-year high of 232,877 contracts

European markets higher, US futures flat

[8:38 am] Not the most action packed overnight session. European stocks slightly higher as investors digested takeaways from the Munich Security Conference. Pan-European Stoxx 600 (+0.13%) within 0.5% of last Wednesday’s record close, other notable indices include IBEX (+0.99%), FTSE 100 (+0.26%), CAC 40 (+0.06%) and DAX -0.46%.

S&P 500 futures (+0.05%) flat, while Russell 2000 and Nasdaq futures both down 0.2-0.3%.

European earnings beat estimates but investors demand more amid sky-high valuations

[8:36 am] European company earnings are recovering with Q4 growth of 3.9%, but elevated valuations are making investors pickier about rewarding even strong results.

60% of European companies beat earnings expectations this season vs. typical 54%, yet positive share price reactions have been muted

Companies beating estimates saw flat returns on earnings day while misses saw small declines

STOXX 600 trading at 15.3x forward earnings, highest since January 2022, with strategists noting investors are more nervous at these elevated multiples despite solid fundamentals

Euro strength above $1.20 (first time in four years) has been a headwind but largely priced in, with companies already factoring currency impacts into guidance

Financials lead for the 12th consecutive quarter of net earnings beats, with banks seeing most guidance upgrades and tipped as "net winners" from AI despite minimal near-term impact on estimates

Tech dispersion widening sharply, ASML raised sales outlook on AI chip demand while SAP tumbled 16% on earnings day amid AI disruption concerns, pushing software valuations below hardware for first time

Source: Reuters

Good morning!

[8:28 am] ASX 200 futures are up 15 pts (+0.16%) as of 8:30 am AEDT.

The overnight session in a nutshell:

US market closed for Presidents Day

S&P 500 futures (+0.05%) relatively flat, Nasdaq and Russell futures (both down 0.2-0.3%) slightly lower

European markets finished mostly higher, with the Stoxx 600 up 0.13%, closing within 0.5% of last Wednesday's record close

Munich Security Conference saw several European leaders stress the need for greater defence spending

To catch up on all overnight developments, check out today's Morning Wrap.