ASX 200 Live Today - Tuesday, 16th December

The S&P/ASX 200 is set to open flat as markets digest recent gains. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Tuesday, December 16. Expect a high volume of posts pre-market and more periodic updates throughout the day. It'll wrap up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

ASX 200 fades early gains

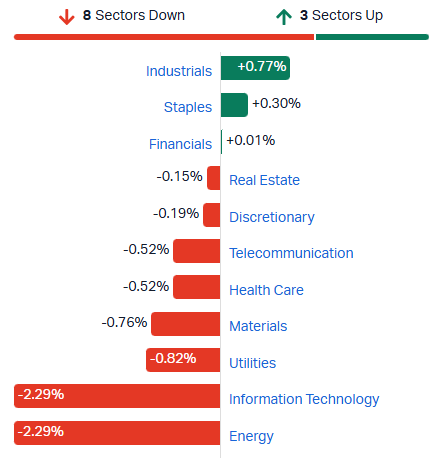

[2:15 pm] A pretty ugly session, with most sectors trading lower (except for Industrials and Staples). Tech is looking very ugly, down 2.2%, on a six-day losing streak and down almost 30% since mid-September. Materials opened ~0.4% higher, now down 0.7%. Energy also tumbled intraday, now down 2.2%. ASX 200 has now flopped back to the 200-day moving average, the mood has gone from "maybe we've set a low" to "we need to show some strength here to avoid rolling over."

S&P/ASX 200 sectors (Source: Market Index)

Miners pull back sharply

[1:35 pm] S&P/ASX 200 Materials Index currently down 0.53% and down 2.7% in the last two sessions, likely weighed by downbeat Chinese economic data on Monday.

China's retail sales rose 1.3% in November from a year ago vs. expectations of a 2.9% increase and the slowest figures on record outside the pandemic.

Fixed-asset investment down 2.6% in the first 11 months of the year vs. expectations of a 2.3% fall and keeping it on track to post the first annual drop in data going back to 1998.

Industrial output grew 4.8% from a year ago, slightly below market expectations of 5.0%

New home prices in 70 Chinese cities fell 0.39% month-on-month in October. Prices have now been falling month-on-month for more than two years, with analysts expecting another 11% decline in 2026

AMP's take on Aussie consumer confidence

[1:25 pm] A few interesting comments from AMP economist My Bui:

"With the RBA expected to remain on hold for now (with a bias towards rate hikes), and the labour market likely soften a bit next year, we don’t anticipate further recovery in consumer confidence."

"This means that we’ll continue to see household consumption growth positive but not picking up pace from here."

"The overall willingness to purchase remains contained and the majority of the inflation rises have been concentrated in the administered/index categories as seen in the chart below."

Australian consumer sentiment falls sharply amid rate worries

[12:30 pm] The Westpac–Melbourne Institute Consumer Sentiment Index dropped 9% to 94.5 in December, reversing most of November’s bounce and returning to ‘cautiously pessimistic’ territory. While household confidence has improved from the deep pessimism of 2024, the survey highlighted rising concerns over inflation, interest rates, and the economic outlook.

Mortgage rate expectations surged 22.2% in December, part of a 65.4% rise over three months, reflecting fewer consumers expecting cuts and more anticipating rate rises, with mortgage holders most affected.

Economic outlook and family finances deteriorated, with the ‘economic outlook next 12 months’ sub-index falling 9.7% to 94.6 and ‘family finances vs a year ago’ down 5% to 80.9, while labour market expectations remained broadly stable.

Homebuyer sentiment weakened, with the ‘time to buy a dwelling’ index falling 10.6% to 86.2, and house price expectations eased slightly to 169.9, though most consumers still expect prices to rise over the next 12 months.

Consumers showed increased caution in financial risk-taking, favouring safe options such as bank deposits and debt repayment over shares or property, reflecting ongoing cost-of-living concerns and rate anxieties.

Resolute rallies on Doropo study

[12:03 pm] Resolute Mining has emerged as the best performing large cap gold stock this morning. The company released the DFS for its Doropo Project in Côte d'Ivoire on Monday, which highlighted:

Average life of mine production of 170koz over 13 years

Life of mine AISC of US$1,406/oz vs. prior US$1,047/oz est

Capital cost of $516m

In first five years average annual post-tax FCF and EBITDA of $268m and $364m respectively, with payback period of 1.7 years

Macquarie reiterated an Outperform rating this morning and raised its target price by 7% to $1.45.

"Doropo will become RSG's third operational asset and provides important geographical diversification outside Mali (Syama) and Senegal (Mako), opening up a third production asset in Côte d'Ivoire," noted the analysts.

Top ASX 200 gainers and losers

[11:10 am] Droneshield is catching a bid after announcing a ~$50 million contract this morning, a few IPO names (GYG, GLF and VGN) also catching a bid. Meanwhile, uranium and richly valued tech names (360, PME, REA) continue to unravel.

Ticker | Company | % Chg | Price |

|---|---|---|---|

DRO | Droneshield | 15.43% | $2.66 |

RSG | Resolute Mining | 7.49% | $1.18 |

TUA | Tuas | 3.06% | $7.25 |

MEZ | Meridian Energy | 2.54% | $4.84 |

SIG | Sigma Healthcare | 2.41% | $2.98 |

GYG | Guzman Y Gomez | 2.22% | $21.61 |

QAN | Qantas Airways | 1.99% | $10.01 |

DMP | Domino's | 1.96% | $22.86 |

GLF | Gemlife Communities | 1.93% | $5.29 |

VGN | Virgin Australia | 1.72% | $3.26 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

360 | Life360 | -6.28% | $32.52 |

SLX | Silex Systems | -4.92% | $7.44 |

NXG | Nexgen Energy | -4.54% | $12.95 |

PME | Pro Medicus | -4.12% | $224.07 |

REA | REA Group | -4.09% | $181.34 |

PDN | Paladin Energy | -3.41% | $8.65 |

MND | Monadelphous Group | -2.85% | $26.22 |

CPU | Computershare | -2.65% | $33.22 |

TNE | Technology One | -2.48% | $26.72 |

GDG | Generation Development Group | -2.38% | $5.54 |

ASX 200 flat as tech stocks tumble

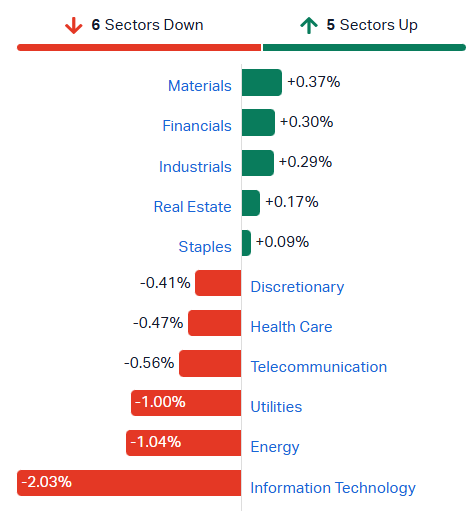

[10:58 am] ASX 200 currently trading around breakeven, down from early highs of 0.43%.

Very heavy session for tech stocks, with most large cap names down 1-2%. This is a sector that's been under heavy distribution for quite some time, with no meaningful bounce in sight.

Energy stocks also under pressure as Brent prices fell 1.3% overnight to US$60.4 a barrel. This marks the lowest close since 5 May. Woodside and Santos both down around 0.7%, coal stocks slightly lower and most uranium names down 3-4%

Materials bouncing after a volatile last two sessions (up 2.0% last Friday to record highs, down 2.2% on Monday)

S&P/ASX 200 sectors (Source: Market Index)

Australian business activity expands, growth slows slightly

[10:45 am] S&P Global’s December flash PMI showed continued expansion in the private sector, driven by new orders and rising employment, though growth softened compared with November.

The Composite Output Index eased to 51.1 from 52.6, marking the slowest pace of growth in seven months as manufacturing and services activity moderated.

New orders remained solid, with goods exports offsetting softer services export growth, supporting higher staffing levels to manage workloads and anticipate future demand.

Future Output Index hit its highest since June, reflecting optimism around expansion plans, new product launches and improved economic conditions in 2026.

Cost pressures intensified, pushing input costs and output prices higher, with manufacturers reporting the fastest rise in goods input costs in eight months and output price inflation reaching a three-month high.

The last point on costs is not a good look for the current inflation and interest rate outlook.

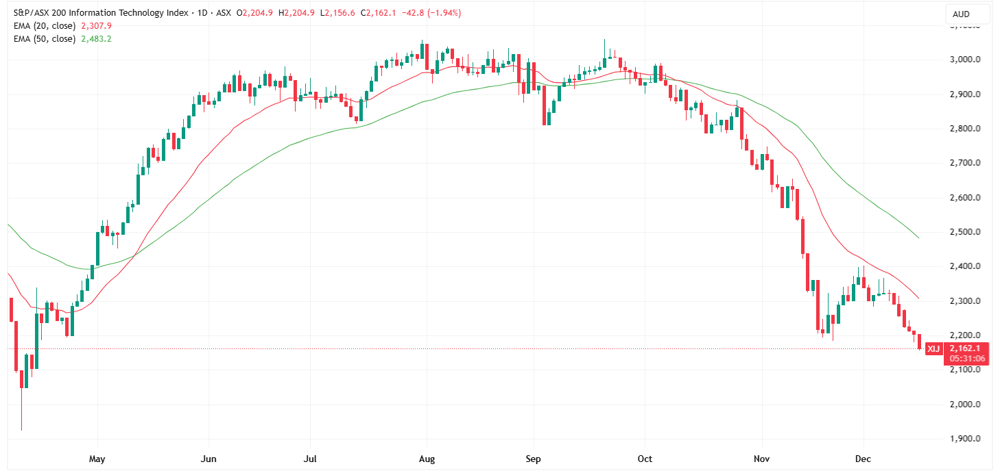

Tech stocks continue to unravel

[10:30 am] Very ugly price action for local tech stocks, with the S&P/ASX 200 Tech index trading at a fresh 8-month low this morning. The index dipped 1.95% in early trade and currently on a six-day losing streak. Large cap names like Wisetech, Xero, TechnologyOne and NextDC are all down 1-2%, while Life360 has slumped 6% to a fresh five-month low.

S&P/ASX 200 Tech index daily chart (Source: TradingView)

Star Entertainment CEO Steve McCann to depart

[10:03 am] Star Entertainment confirmed Steve McCann will step down as CEO effective 16 December, with Bruce Mathieson Jnr assuming additional responsibilities as Executive Chair while a search for a permanent replacement is underway.

McCann has only served as CEO since June last year, where his remuneration package featured:

$2.5 million per year fixed salary

$2.5 million cash sign-on bonus

$2.5 million per year short-term incentives for FY25 and FY26

$2.5 million retention bonus for FY26

A one-off grant of $5 million in performance rights, vesting in 2027

Analysts' take on ASX

[9:37 am] Shares in the exchange operator tumbled 5.7% on Monday (fresh two-year low) after ASIC's interim report triggered a significant reset in governance, capital management and strategic priorities. Key downward drivers include a $150 million capital charge, a lower dividend payout guidance and revised ROE targets.

Jarden retained Neutral, lowered target from $66.70 to $57.45. The broker flags elevated risk of further investment surprises, with capital constraints likely to pressure profitability and valuation offering limited upside amid muted growth.

UBS retained Sell, lowered target from $62.15 to $53.00. A reset expense base is expected to weigh through FY27, with DRP-driven dividend dilution adding a near-term headwind and consensus forecasts seen as too optimistic.

JPMorgan retained Neutral, lowered target from $65.00 to $61.00. The outcome was worse than expected, with the Accelerate reset proving materially more costly, although management stability remains intact and DRP funding is expected to cover a significant share of capital needs.

ASIC escalates warning on ASX governance and market infrastructure

[9:27 am] ASIC chair Joe Longo told stockbrokers the ASX will face serious consequences if it fails to meet commitments agreed with regulators, including potential loss of its clearing and settlement functions, the AFR reported.

Longo flagged regulatory escalation through tougher licence conditions, enforceable rules and, if necessary, advice to government on structural separation.

The comments follow a scathing AFR-reported review by an ASIC appointed panel, which found excessive influence by ASX directors over clearing and settlement subsidiaries. The panel said ASX governance has placed too much emphasis on shareholder returns at the expense of investment in critical market infrastructure, leaving subsidiary boards without sufficient independence or authority.

While the panel stopped short of recommending forced separation, it called for independent non-executive chairs, fully independent subsidiary boards and greater control over budgets and financial accounts.

For what it's worth, a mate of mine (full-time trader) emailed the ASX explaining why removing the staggered close would only increase volatility and worsen liquidity (which it has). Their reply was basically 'no you're wrong'.

Company page: ASX Limited (ASX)

DroneShield lands large European military order

[9:21 am] DroneShield says the sizable defence contract boosts revenue visibility into early 2026, with limited execution risk.

DroneShield secured a $49.6m contract via a European reseller supplying a European military end customer.

The order covers handheld counter drone systems, accessories and software updates, with a significant portion already held as finished stock.

Deliveries and full cash receipts expected to be completed in Q1 2026, with no additional material conditions attached.

The reseller relationship is well established, with 15 contracts over the past three years totalling more than $86.5m.

I wonder how the market will respond to this news, given the recent sequence of events (withdrawal/human error re 10 November announcement, which coincided with largest director selldowns).

Company page: DroneShield (DRO)

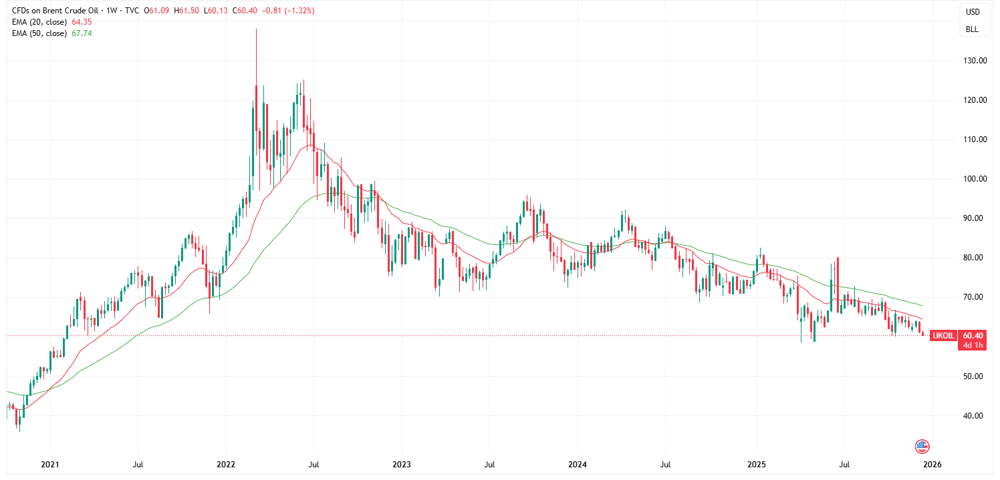

Gulf Coast crude market flashes oversupply warning

[9:09 am] A key physical pricing signal in the US is diverging from futures markets, pointing to a growing regional and potentially global oil glut, Bloomberg reported.

WTI at Magellan East Houston is trading in contango, around 12 cents a barrel below later dated prices, a bearish structure that has persisted almost daily since October despite inventory draw efforts. This contrasts with backwardated WTI and Brent futures, suggesting paper markets still price tightness while physical barrels are showing oversupply.

Traders view the Gulf Coast as the new stress point for the oil market, given its role as the largest US tank farm, refining centre and export hub, with inventories shifting away from Cushing.

Floating storage near US shores is close to pandemic era highs, reinforcing signs of excess supply, according to Vortexa data cited by Bloomberg.

The IEA forecasts a record global oil surplus of 3.8 million barrels per day next year, with traders expecting Gulf Coast tanks to refill after year end tax pressures ease.

Brent prices fell 1.3% overnight to US$60.4 a barrel. This marks the lowest close since 5 May and on the cusp of falling to the lowest level since February 2021.

Brent crude weekly price chart (Source: TradingView)

US homebuilder confidence lifts but cost pressures remain

[8:57 am] US homebuilder sentiment improved to an eight month high in December, but tariffs, affordability constraints and weak demand continue to weigh on activity.

NAHB housing market index rose to 39 in December from 38, the highest since April but still below the 50 breakeven level for a 20th straight month.

Two thirds of builders are offering incentives, with tariffs pushing up material costs and immigration policy tightening labour supply.

Weak demand is driving inventory build up, with 40% of builders cutting prices for a second straight month and the average discount easing to 5%.

Current sales conditions and future sales expectations edged higher, but buyer traffic remained flat at deeply subdued levels.

Is the sector in the process of making a bottom (and an opportunity to look at names like James Hardie?).

Fed speakers lean dovish as markets price gradual easing

[8:50 am] Post December FOMC commentary reinforces a softer policy bias, though rate cut expectations remain restrained.

Miran argued policy is too restrictive with inflation near target, downplayed tariffs as an inflation driver, called for avoiding unnecessary tightening to limit job losses and said rates should decline further as the Fed should be setting policy with 2027 in mind.

Williams said the economy could regain momentum in 2026 after a uncertain 2025, sees tariff impacts as muted and gradual, and stressed inflation expectations remain well anchored with policy guided by the full balance of risks.

Collins said last week's rate cut was a "close call" and seeks greater clarity before further easing

Markets are now pricing ~55 bp of cuts through end 2026, up from 48 bp post December FOMC but well below the near 80 bp priced in late November.

Bond market backlash clouds Hassett’s Fed Chair prospects

[8:48 am] Concerns about Fed independence and inflation credibility are shifting momentum in the race to succeed Powell.

Push back from Trump allies centres on fears markets would view Hassett as too politically aligned, risking a bond sell off and higher long term yields.

Investors worry Hassett may favour rate cuts even with inflation above the 2% target, undermining confidence in the Fed’s inflation fighting mandate.

FT previously reported bond investors raised these concerns directly with the US Treasury, including doubts over Hassett’s ability to build consensus on a divided Fed board.

Trump said Hassett and Warsh are his top picks and expects the next Fed Chair to consult with him on rates, heightening independence concerns.

Prediction markets now show Warsh overtaking Hassett as the leading nominee

Wall Street awaits US jobs data

[8:45 am] November nonfarm payrolls will be released on Wednesday and expected to show modest growth, though distortions, revisions and data gaps mean the signal for the Fed will be noisy.

Consensus is for just ~40,0000 jobs added, with analysts flagging downside risk from federal job cuts and potential downward revisions to September’s 119k print.

Unemployment rate flat at 4.4%, with upside risk given September’s unrounded 4.44% and reliance on incomplete survey coverage.

October payroll data will include establishment survey results but exclude the household survey, limiting clarity around true labour market slack.

Rotations in focus

[8:43 am] Another session where Tech underperformed by a wide margin while value oriented pockets of the market like Healthcare and Utilities underperform.

S&P 500 sector performance (Source: Bloomberg)

Good morning!

[8:31 am] ASX 200 futures are down 5pts (-0.05%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks modestly lower and closed near worst levels

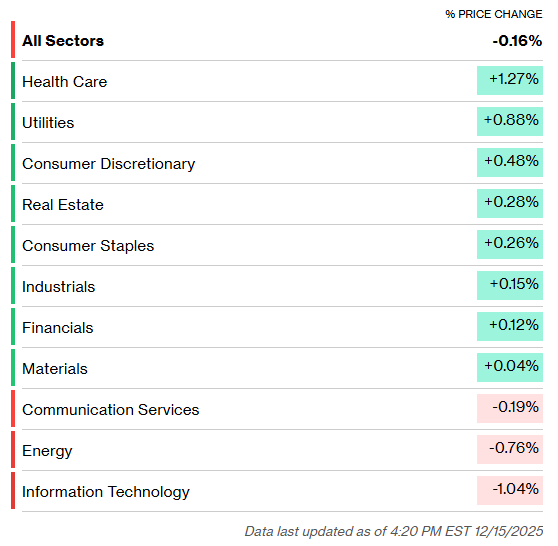

Equal-weight S&P 500 (+0.12%) outperformed the official benchmark by 28 bps as sectors like Healthcare (+1.27%), Utilities (+0.88%), Discretionary (+0.48%) and more finished higher

Rotation dynamics continued to play out amid persistent AI bubble/financing/ROI concerns