ASX 200 Live Today - Thursday, 5th March

The S&P/ASX 200 is set for a comeback bounce as markets shrug off geopolitical concerns. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, March 5. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 higher, off best levels

[2:10 pm] That's all for today. The ASX 200 up 0.32%, just ticking over the 50-day moving average. A relatively choppy session, with the index struggling to hold on to session highs of 0.71%. Plenty of things bouncing, with Bitcoin soaring 6.3% overnight, South Korea's KOSPI index up 10.2% today and Aussie Tech up 4.3%. Despite the uptick in volatility, the market remains in a good place, with sectors like Utilities, Staples, Materials, Banks and Energy holding up relatively well. Interesting note from UBS today, where they examined 15 geopolitical shocks over the past 50 years and found the S&P/ASX 200 returned an average of 4%, 5% and 11% over the subsequent 3, 6 and 12 months. The main exception was the first Gulf War, which inflicted lasting damage (and higher for longer oil prices). So it really depends on whether the conflict is contained or continues to escalate.

Energy stocks whipsaw

[1:56 pm] Energy stocks have traded relatively flat over the past couple of days, with most names hovering around Monday's close. Every session has seen relatively wide trading ranges for these stocks as they digest the Middle East conflict. Woodside dipped as much as 4.6% in early trade, now down just 1.9%.

Brent is currently up 1.5% to US$83.8 a barrel. Overnight, Brent finished the session up 0.7% but fluctuated between a high of +3.0% and low of -2.0%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

AGL | AGL Energy | 2.03% | $9.81 |

ORG | Origin Energy | 0.59% | $11.90 |

STO | Santos | -0.21% | $7.24 |

BPT | Beach Energy | -0.87% | $1.14 |

WDS | Woodside Energy | -1.92% | $30.16 |

UBS flags thermal coal upside, met coal near support

[1:32 pm] UBS sees thermal coal prices supported by the Middle East conflict while met coal trades near a floor, with contrasting views on ASX-listed plays CRN and WHC.

Thermal coal could reach US$130-140/t (API2), up 8-17% vs spot, if the TTF gas price surge from the Iran conflict is sustained; thermal prices already up ~9% since conflict began

Met coal at ~US$220/t after a 13% fall on soft Indian buying, but UBS sees demand stepping back in at current levels given Indian end users were waiting for prices to reach ~US$220/t

Australian wet season risk remains live, with a tropical low forming in the Coral Sea carrying a moderate chance of developing into a cyclone and delivering widespread QLD rainfall from Friday

Indonesia policy uncertainty a watchlist item: proposed 2026 production cut to ~600Mt (down ~24% vs 2025) not yet official, coal exports -5% YTD, with quota revisions possible in June/July

Supply set to loosen from mid-2026 with new projects adding over 10Mt to seaborne met coal supply (~3.6% growth), a headwind for prices into the second half

CSL loses market share across key plasma categories in tough 2025

[12:56 pm] UBS analysis shows CSL retained its position as the world's largest plasma-derived therapy supplier but lost ground to Grifols across most product categories, weighed down by US reimbursement cuts and weak commercial execution.

CSL's plasma-derived therapy (PDT) sales fell 4% in 2025, with over $400m in revenue lost to IRA reimbursement cuts and lost tenders, against a tough comparable (PDT sales +12% in 2024)

Global PDT market grew ~4%, below the historical high-single-digit rate

CSL lost share across Ig, subcutaneous Ig, albumin and hereditary angioedema (HAE)

Seqirus was the sole bright spot: seasonal flu sales up 3% against a market that contracted ~4%, lifting estimated share to ~33%

Despite the challenges and CSL's recent disappointing track record, UBS retains a Buy rating with a $235 target price.

Company page: CSL (CSL)

Tech stocks holding up

[12:46 pm] Tech stocks are holding on to gains, with the S&P/ASX 200 Tech Index currently up 4.0%, slight off session highs of 5.1%. The Index is starting to test the 20-day moving average (red), an area where it has failed to break above on numerous occasions. It hasn't traded meaningfully above the 20-day since last September.

S&P/ASX 200 Info Tech Index chart (Source: TradingView)

Australian household spending rebounds in January

[12:40 pm] Household spending rose 0.3% month-on-month in January after a 0.5% fall in December, with services leading the recovery while goods spending slipped.

Spending up 4.6% year-on-year in nominal terms, though real growth remains the key question for the RBA as it weighs further rate cuts

Services spending drove the monthly gain, up 1.0%, led by digital streaming, travel agencies and dental services

Goods spending fell 0.3%, dragged by motor vehicles and recreation/culture, pointing to ongoing caution on big-ticket purchases

Essential spending rose 0.8% (health services, vehicle maintenance) while discretionary edged up just 0.1% (air transport, personal effects, recreational services), suggesting consumers remain selective

Tasmania led state gains (+0.6%), with NSW and Victoria both up 0.5%; the Northern Territory fell 2.3%

Source: ABS

Top ASX 200 gainers

[11:20 am] Tech and growthy stocks have topped the leaderboard in early trade, uranium and defence stocks also trending higher.

Ticker | Company | % Chg | Price |

|---|---|---|---|

TLX | Telix Pharmaceuticals | 6.97% | $10.13 |

IPX | Iperionx | 6.61% | $7.10 |

DRO | Droneshield | 5.95% | $3.56 |

SLX | Silex Systems | 5.88% | $6.40 |

WTC | Wisetech Global | 5.05% | $46.64 |

XYZ | Block | 4.29% | $92.41 |

MSB | Mesoblast | 4.21% | $2.11 |

ZIP | Zip Co | 4.14% | $1.69 |

TNE | Technology One | 3.81% | $26.15 |

PDN | Paladin Energy | 3.50% | $13.02 |

Top ASX 200 losers

[11:20 am] Gold miners, insurers and energy stocks are trading broadly lower this morning.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CMM | Capricorn Metals | -3.88% | $14.12 |

WGX | Westgold Resources | -3.78% | $7.13 |

GMD | Genesis Minerals | -3.76% | $7.29 |

NST | Northern Star Resources | -3.54% | $28.87 |

QBE | QBE Insurance | -3.20% | $20.87 |

BPT | Beach Energy | -3.06% | $1.11 |

WDS | Woodside Energy | -3.02% | $29.82 |

PDI | Predictive Discovery | -2.87% | $0.95 |

AMC | Amcor | -2.87% | $64.65 |

EVN | Evolution Mining | -2.74% | $15.63 |

Analysts take on Endeavour Group

[11:15 am] Endeavour reported its 1H26 result on Wednesday, which was broadly in-line with market expectations. Though its retail division continues to focus on prices and match competitor promotions, at the expense of margins. Early second half trading indicated modest sales growth that slowed into February, offset by continued strength for its Hotels division. Here's what analysts are thinking.

JPMorgan retained Neutral, lowered target from $3.70 to $3.50, citing retail margin pressure from a renewed pricing strategy and uncertainty around the duration of the earnings reset, with Hotels seen as a growing earnings contributor.

UBS retained Neutral, raised target from $3.75 to $4.00, noting Hotels division strength supported earnings but the retail turnaround path remains uncertain amid structural challenges in the liquor market.

RBC Capital Markets retained Sector Perform, raised target from $3.85 to $4.00, with the result toward the upper end of guidance but retail sales momentum softening into early H2 and continued price investment expected at Dan Murphy's.

Banks snap five day losing streak

[10:36 am] The S&P/ASX 200 Financials Index is up 1.35% today, following a five-day losing streak of 4.05%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

BOQ | Bank Of Queensland | 2.27% | $6.98 |

MQG | Macquarie Group | 2.12% | $195.60 |

JDO | Judo Capital | 2.04% | $1.60 |

NAB | National Australia Bank | 1.81% | $47.53 |

CBA | Commonwealth Bank | 1.30% | $174.14 |

WBC | Westpac | 1.19% | $41.62 |

ANZ | Anz Group | 1.08% | $38.35 |

BEN | Bendigo & Adelaide Bank | 0.97% | $10.44 |

By Stephanie Gardner

Tech stocks broadly higher

[10:27 am] The S&P/ASX 200 tech index is up 3.8%, following a strong overnight session for tech stocks. The iShares Expanded Tech-Software Sector ETF closed up 1.82% overnight and is now up 6 of the last 7 sessions.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CAT | Catapult Sports | 6.97% | $3.53 |

NXL | Nuix. | 6.27% | $1.90 |

XRO | Xero | 5.21% | $84.65 |

WBT | Weebit Nano | 5.16% | $4.48 |

BVS | Bravura Solutions | 4.39% | $2.14 |

WTC | Wisetech Global | 4.35% | $46.33 |

TNE | Technology One | 3.99% | $26.20 |

MP1 | Megaport. | 3.84% | $7.98 |

DTL | Data#3. | 3.56% | $6.99 |

NXT | Nextdc | 2.85% | $13.37 |

360 | Life360 | 2.85% | $20.96 |

ELS | Elsight. | 2.40% | $5.12 |

HSN | Hansen Technologies | 2.38% | $5.16 |

SDR | Siteminder | 2.32% | $3.09 |

MAQ | Macquarie Technology Group | 1.93% | $61.67 |

DDR | Dicker Data | 1.88% | $8.69 |

AD8 | Audinate Group | 1.80% | $2.83 |

CDA | Codan | 1.78% | $37.15 |

IRE | Iress | 1.10% | $7.34 |

PPS | Praemium | 0.67% | $0.75 |

OCL | Objective Corporation | 0.00% | $12.75 |

DGT | Digico Infrastructure Reit | -0.51% | $1.97 |

By Stephanie Gardner

Commodities bounce but off best levels

[9:50 am] Commodities finished the overnight session broadly higher, but off best levels.

Commodity | % Chg | Session high |

|---|---|---|

Platinum | +3.16% | +5.28% |

Nickel | +2.48% | +3.91% |

Silver | +1.52% | +5.88% |

Aluminium | +1.83% | +4.57% |

WTI Crude | +1.72% | +3.23% |

Palladium | +1.31% | +4.07% |

Copper | +1.22% | +2.30% |

Gold | +1.03% | +2.31% |

Pioneer Credit lifts FY26 NPAT guidance 28% after MTN repricing

[9:32 am] Pioneer Credit has upgraded FY26 NPAT guidance for the second time, now targeting at least $23 million, after repricing its medium term notes on top of an earlier senior facility reprice.

FY26 NPAT guidance lifted to at least $23m, up 28% from the original guidance and up from the $20m upgrade issued on 18 February

The MTN repricing on the $55.5m facility delivers roughly $1.75m per annum in pre-tax interest savings

Annualised savings from both the senior facility and MTN repricing reach approximately $4.63m from FY27 onwards, materially improving the forward earnings profile.

Underlying operating performance is also contributing, with 1H26 net revenue up 5% on the prior half

Company page: Pioneer Credit (PNC)

Lottery Corp restructures to accelerate digital growth

[9:25 am] The Lottery Corp is overhauling its operating model effective 1 July, splitting the business into dedicated Lotteries, Digital and Keno divisions, each with a new COO.

CEO Wayne Pickup signals the company can "unlock more value" from its existing strategy.

The restructure creates three customer-facing business units, each with a distinct COO: Callum Mulvihill (Lotteries), Loren Somerville (Digital) and Antony Moore (Keno), supported by three enterprise services units covering finance, strategy, and people and brand.

The Digital unit's mandate explicitly includes exploring adjacent lottery entertainment categories, signalling ambitions beyond the core product set.

CFO Adam Newman's role expands to absorb legal, risk, cyber and technology services, consolidating a broader remit under finance.

Two senior executives are departing: Chief Customer and Marketing Officer Andrew Shepherd exits 1 July, while Chief Legal and Risk Officer Nicholas Allton leaves 31 March.

Company page: The Lottery Corporation (TLC)

Citadel's Rubner turns bullish, sees March bounce for US equities

[9:18 am] Scott Rubner reversed his bearish stance, pointing to washed-out sentiment, retail buying strength, and seasonal tailwinds as catalysts for a rebound.

February was the worst month for US equities since March 2025, but defensive positioning now leaves room for upside if geopolitical tensions ease.

Retail traders continue to buy dips consistently, keeping options activity elevated and providing a demand floor for the market.

Large March options expirations could trigger a re-risking rally, particularly in quality tech stocks, with mid-month volatility normalisation expected to drive a durable bounce into April.

Seasonality is supportive: March historically delivers positive S&P 500 returns, aided by mutual fund inflows and above-average tax refunds.

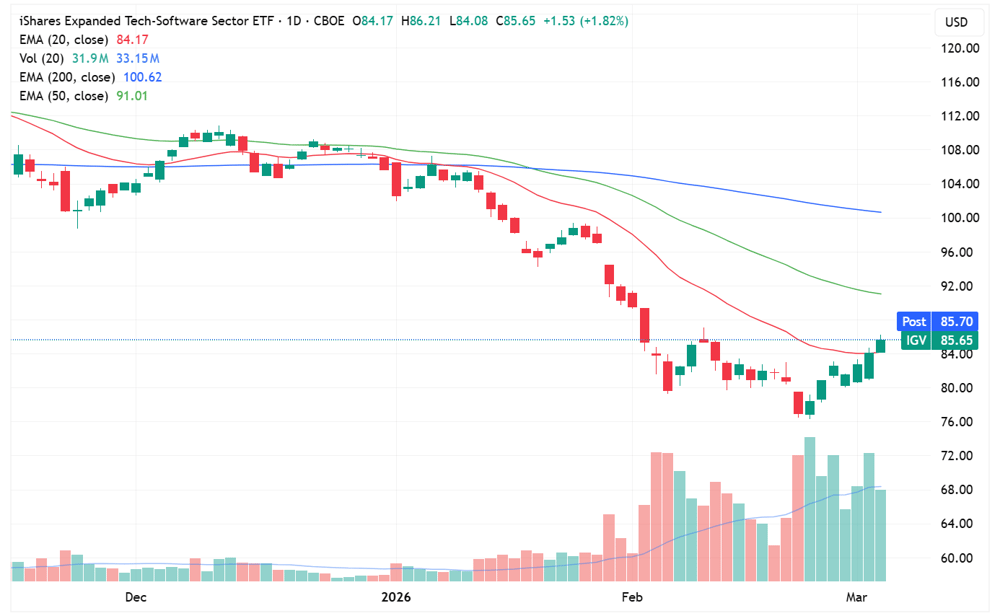

Software stocks find a floor

[9:15 am] Another solid session for the iShares Expanded Tech Software ETF, which is one of the more widely quoted benchmarks for the software sector. It holds plenty of high-profile names like SAP, Salesforce, Uber, Adobe and more.

The ETF gained 1.8% overnight and now up six of the last seven sessions, trading at a fresh one-month high.

iShares Expanded Tech Software ETF daily chart (Source: TradingView)

Can't say the same about local tech, with the S&P/ASX 200 Tech index on a four day losing streak. Though the overnight strength could provide a positive lead in/bounce.

Advanced Innergy to acquire aquaculture tech supplier Imenco Aqua

[9:07 am] AIH is expanding its marine platform with the purchase of a Norwegian aquaculture technology business serving the Atlantic salmon market.

Upfront consideration of $17.7m plus an earn-out of up to $3.0m tied to FY26 EBITDA growth targets, implying a 5.8x FY25 EBITDA multiple pre-synergies.

Imenco Aqua recorded FY25 revenue of $15.0m and underlying EBITDA of $3.0m, with roughly 30% recurring revenue driven by a leasing model for IP-protected products.

AIH's prospectus noted FY26 forecast EBITDA of $62.3 million

Products are proprietary and patented, embedded in regulated fish welfare and environmental compliance frameworks in Norway and Chile, providing strong contract visibility and renewal rates.

Deal is EPS accretive from completion, expected by end of March 2026, funded from existing cash reserves, and incremental to current FY26 guidance.

AIH expects cross-sell opportunities and operating synergies across its global sales footprint, complementing the recent Ovun acquisition.

Company page: Advanced Innergy Holdings (AIH)

Boss Energy flags 3Q26 weather-hit

[9:05 am] Heavy rain at Boss Energy's Honeymoon uranium operation in South Australia has restricted site access and reagent deliveries, cutting Q3 production guidance well below the prior quarter.

Q3 FY26 production now expected at 240-270,000 lbs, down sharply from 456,000 lbs in Q2

Reagent deliveries and production are expected to resume by 14 March, with Boss using the downtime to complete a planned shutdown connecting new plant, wellfield and power infrastructure

Full-year FY26 guidance of 1.6m lbs is maintained, implying a significant ramp into Q4, which management is flagging as a potential record quarter for drummed production

It's worth noting that Boss Energy is the second most shorted stock on the market, with 16.04% short interest.

Company page: Boss Energy (BOE)

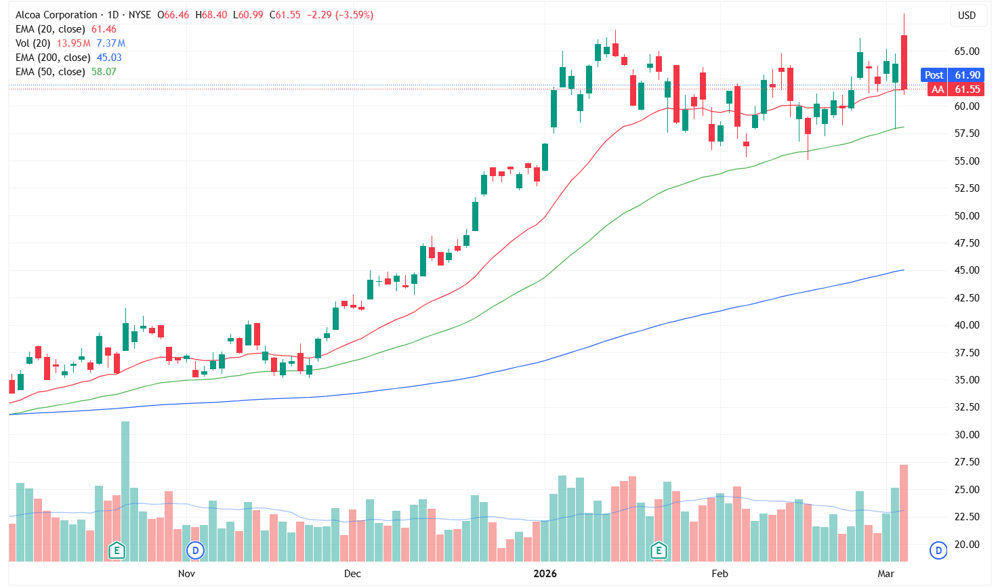

Aluminium prices highest since April 2022

[9:03 am] Aluminium prices rallied as much as 4.5% overnight, but finished the session up just 1.8% to US$3,322 a tonne but still closing at the highest since April 2022. Prices are now up 11.4% year-to-date and up 27.4% in the last twelve months.

Alcoa shares briefly rallied as much as 7.1% overnight, but finished the session down 3.5%.

NYSE-listed Alcoa daily price chart (Source: TradingView)

Aluminium supply crunch deepens as Bahrain halts shipments and Qatari smelter shuts

[8:55 am] Middle East conflict is squeezing global aluminium supply, with two major Gulf producers now offline and prices surging to multi-year highs.

LME aluminium jumped as much as 5.1% to $3,418/t, up 9% on the week, with Goldman Sachs flagging a potential move to $3,600/t if regional production is lost for a month.

Bahrain's Alba, the world's largest smelter outside China with 1.62 million tonnes of annual output, declared force majeure after Strait of Hormuz shipping disruptions halted exports, with the smelter itself undamaged but metal stranded onsite.

Qatar's Qatalum (648,000 t/yr) began shutting down, with shareholder Norsk Hydro issuing its own force majeure and warning a full restart could take six to twelve months.

Around 8% of global aluminium supply is produced in the region, with more than 5 million tonnes per year shipped through the Strait of Hormuz from smelters in Bahrain, Qatar, Saudi Arabia, and the UAE.

Physical premiums are surging, with European premiums hit $436/t for April delivery, a three-and-a-half year high, while US premiums jumped to a record $1.075/lb.

Europe PMIs strengthen, China soft

[8:53 am] Eurozone PMIs strengthened to near 2-3 year highs, while manufacturing and service data from China slumped across the board.

Eurozone Composite PMI rose to a three-month high of 51.9 in February (from 51.3 in January), with growth broadening across manufacturing and services and business optimism hitting its most bullish since May 2024, though input cost inflation accelerated to its sharpest pace since April 2023 and France remained the lone weak spot.

UK Services PMI edged down to 53.9 in February from 54.0 in January, remaining firmly in expansion territory but with persistent job cuts and price pressures complicating the Bank of England's rate decision this month.

China Manufacturing PMI fell to 49.0 in February (vs. 49.2 est, 49.3 prior), contracting more than forecast and matching a four-month low, while the non-manufacturing PMI also missed at 49.5 (vs. 49.7 est), with construction sliding to a six-year low amid Lunar New Year disruptions, weak domestic demand, and mounting tariff uncertainty.

Qatar LNG shutdown sends Asian spot prices to two-year highs

[8:52 am] The US-Israel strike on Iran has forced a halt at Qatar's LNG facilities and closed the Strait of Hormuz, sending Asian spot LNG prices to their highest level since 2023 and sparking a scramble for alternative supply across Europe and Asia.

Asian spot LNG prices hit $25.40/mmbtu, more than double last week's levels, with further upside expected while Qatar's output remains suspended.

Qatar accounts for roughly a fifth of global LNG supply, with the bulk flowing to China, India, South Korea and Taiwan, leaving Asian buyers acutely exposed.

European gas prices have surged 70% since Friday to their highest since 2023, with the disruption threatening the EU's ability to rebuild winter inventories as it phases out Russian gas.

Cargo competition between Europe and Asia is intensifying, with traders watching price spreads to determine where redirected shipments will flow.

China and India face the greatest exposure and may pivot to coal rather than pay spot premiums, while analysts warn the crisis could prompt a broader rethink of LNG portfolio diversification strategies.

Source: Bloomberg

Korean stocks suffer biggest crash since 2008 as Iran war sparks margin unwind

[8:50 am] Panic selling swept South Korean equities as the escalating Middle East conflict collided with a record build-up of leveraged positions, triggering the Kospi's worst single-day loss since the global financial crisis.

The Kospi plunged 12% on Wednesday, following a 7.2% drop the prior session, with a 20-minute trading halt triggered early in the day and only 10 of 800-plus stocks finishing in the green.

The selloff was amplified by record margin debt, with retail investors holding only 30-40% in margin deposits on heavyweight stocks like Samsung Electronics, SK Hynix, and Hyundai Motor, leading to forced liquidations as prices fell.

The government signalled it would deploy its 100 trillion won market stabilisation fund if volatility becomes excessive, with the Kospi still up 21% year-to-date despite the rout.

Source: Bloomberg

Iran war puts "Trump put" in question

[8:44 am] Wall Street strategists are warning that the playbook investors used during Trump's trade war may not apply to the Iran conflict, as oil price risks and geopolitical uncertainty limit the White House's ability to simply reverse course.

Unlike the tariff standoff, where Trump retained direct policy control, the Iran war has its own momentum and involves other powerful parties, making a quick exit harder to engineer.

The S&P 500 has so far held up relatively better than overseas markets, with dip buyers stepping in, but strategists say a 10-15% drawdown would be needed to generate meaningful political pressure on the White House.

Oil price risk is the key transmission channel, with Morgan Stanley's Mike Wilson notes equities have historically held up during Middle East conflicts unless crude surges 75% or more year-on-year.

The conflict threatens to reignite US inflation and delay Fed rate cuts, compounding existing headwinds including AI sector concerns, pockets of credit stress, and softening jobs growth.

Source: Bloomberg

Good morning!

[8:30 am] ASX 200 futures are up 91 pts (+1.02%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks higher in a tech, momentum and growth-led bounce

S&P 500 almost breakeven for the week, Nasdaq has flipped slightly positive

Markets generally resilient, with a focus on how geopolitical shocks have historically not had a lasting impact and tend to present good dip buying opportunities

Commodity prices broadly higher, but off best levels