ASX 200 Live Today - Thursday, 4th June

The ASX 200 is trading sharply lower as miners tumble and tech stocks take a breather. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, June 4. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

Another dicey day for markets

[2:10 pm] That's a wrap. The ASX 200 is on the backfoot again, down 1.27% as Materials (-3.0%), Tech (-2.3%), Telcos (-1.6%) and Financials (-1.6%) offset modest gains across defensive sectors like Staples and Utilities.

No specific driver behind this defensive tilt, though a few headwinds in focus:

Continued unease in the Middle East and growing doubts about a near-term framework agreement

Brent has slipped 0.5% so far today, but still up 5.5% in the last four sessions to US$96.8 a barrel

Equity supply headlines continue to dominate Wall Street, with the upsized Alphabet raise and upcoming SpaceX, OpenAI and Anthropic IPOs

Trump has proposed broad 10-12.5% tariffs based on forced labour practices (including a 12.5% tariff on Australia)

Likelihood of an RBA rate hike has eased (just ~2% likelihood of a hike in June), with just 24 bps of hikes priced for September 2027. Though the domestic economy is battling a stagflationary mix of higher unemployment (unexpectedly jumped to 4.5% in April), hot CPI (headline at 4.2% in April), soft GDP (Q1 print was up 2.5% year-on-year vs. 2.7% ests) and the latest Fair Work Commission minimum wage increase

Iron ore slides to two-month low

[1:52 pm] Singapore futures fell as much as 1.1% to $102.50 a tonne, the lowest since 14 April, according to Bloomberg.

Rising global iron ore shipments colliding with summer off-season steel demand, with China increasingly oversupplied

Strong coking coal rally squeezing steelmaking margins, with Citic Futures flagging "a downward correction in iron ore is needed to restore a profit balance"

Traders see limited market impact from China Mineral Resources Group's hitches with Fortescue on long-term contracts, with CMRG asking some mills to check the quality of Fortescue's low-grade Fortune Fines product (yet to be shipped)

Source: Bloomberg

New Zealand home-building falls to 10-year low as housing and energy shocks bite

[1:50 pm] Residential construction volumes slumped 5% to NZ$17.6 billion in the year to March, the weakest March-year reading since 2016 and 25% below the 2023 peak, posing downside risk to Q1 GDP.

Building consents up 11% over the past year, with Westpac's Ranchhod expecting activity to turn higher late this year though sustainability into 2027 is unclear given rising rates, higher build costs and soft house prices

House prices have stalled this year as mortgage rates climb and the global energy shock weighs on household incomes

RBNZ last week forecast 1% quarter-on-quarter GDP growth in Q1 and nil growth in Q2, today's data adds downside risk to the Q1 read due 18 June, with the energy shock expected to hit hardest in Q2

Source: Bloomberg

Copper stocks broadly lower

[12:56 pm] Copper prices experienced a sharp pullback from record highs overnight, down 2.9% to US$6.51/lb and continued to drift lower today, currently down 0.3% to US$6.49.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

29M | 29Metals | -7.8% | $0.27 | -48.3% |

AIS | Aeris Resources | -6.5% | $0.43 | -28.3% |

FFM | Firefly Metals | -5.7% | $2.15 | 4.4% |

CYM | Cyprium Metals | -3.8% | $0.39 | -27.3% |

CSC | Capstone Copper | -3.7% | $15.14 | -0.2% |

RIO | Rio Tinto | -3.7% | $187.28 | 27.6% |

BHP | BHP Group | -3.5% | $62.61 | 37.5% |

AR1 | Austral Resources Australia | -3.3% | $0.09 | 52.6% |

SFR | Sandfire Resources | -3.1% | $19.64 | 9.3% |

HCH | Hot Chili | -2.4% | $2.03 | 46.0% |

MC2 | Marimaca Copper | 0.0% | $8.00 | -36.0% |

CPM | Cooper Metals | 0.0% | $0.06 | 0.0% |

HGO | Hillgrove Resources | 4.1% | $0.05 | 6.2% |

Simandou exports surge to 2.2Mt in May, accelerating Pilbara displacement risk

[12:54 pm] Shipments from the Rio Tinto and Baowu Winning-led Simandou project have stepped up sharply in May, with Kpler data showing exports nearly doubling against April's record as port infrastructure matures.

May shipments from Morebaya port hit 2.2Mt, up from 1.3Mt in April

Rio Tinto's official guidance remains for full capacity in 30 months, though some analysts see it taking longer

Ramp-up has involved redeploying assets from Guinea's bauxite industry and Guinean government pressure on BWCS and Simfer to coordinate more efficiently to optimise royalty payments

Comes at a delicate juncture for iron ore with China steel demand under pressure and inventories elevated, raising the question of whether Simandou's high-grade ore displaces Pilbara/Brazilian supply or adds to an already well-supplied market

The news/data appears to be pressuring local iron ore names today, with Fortescue down 3.4%.

Source: Mining.com

Treasury Wine rallies on better-than-expected FY26 guidance

[12:50 pm] TWE is trading 10.5% higher after its Investor Day presentation delivered an FY26 EBIT guidance that was ~2% ahead of consensus. Some of the key numbers from the earlier post include:

FY26 EBITS guided to $480-490m vs $474.2m ests (2% beat at the midpoint)

FY27 EBITS guided to at least equivalent to FY26 vs $487.7m ests (in-line)

Leverage expected to peak at 2.9x in FY26, with management confident of returning below the 2.0x target by end-FY28

Deleveraging driven by free cash flow, divestment proceeds and, from FY28, earnings uplift via completed inventory rebalancing and Ascent transformation benefits

Treasury Wine daily price chart (Source: TradingView)

Macquarie lifts Megaport target to $27.80 on Contracted Compute upside

[11:45 am] Macquarie reiterates Megaport as a high-quality AI play with shorter lead times and lower capex than data centre and neocloud peers.

Megaport shares remain halted amid its $825 million capital raise.

Target price up from $26.30 to $27.80 (vs. $16.61 last close)

Target implies a 12.6x run-rate EBITDA multiple on pro forma EBITDA of $521.5m

EPS revisions: FY26 -52%, FY27 +16%, FY28 +84%, FY29 +53%, reflecting remodelled Contracted Compute economics and conservative timing on capex and D&A

Procurement risk seen as lower than consensus assumes, smaller order sizes than hyperscale-only players, deep relationships across 151 data centre operators, and incremental compute requirement of just circa 7.5-8.0MW (~465-480 B300 servers)

Chip sourcing via direct Nvidia/hardware vendor purchases (not vendor finance), with Cisco relationship and diversification optionality across Lenovo, Dell and WWT

ASX 100 inclusion potentially on the cards within six months on further contract wins, opening passive buying upside

Company page: Megaport (MP1)

House votes 215-208 to halt US war with Iran in rare GOP break from Trump

[11:41 am] Earlier this morning, the Republican-led House passed a War Powers resolution to end US military operations against Iran.

215-208 vote saw four Republicans join all Democrats present. This is the first time Democrats attracted enough GOP support to prevail after three prior attempts this year

Vote doesn't end the war as the Senate has yet to pass its own resolution (advanced past a procedural hurdle last month) and the 1973 War Powers Act provisions invoked are legally contested

Pentagon acting comptroller flagged war costs at circa $29bn to date as of 12 May, with outside experts viewing this as understated given munitions, operations and Middle East deployments

Source: Bloomberg

Analysts' take on Ampol

[11:39 am] The ACCC approved Ampol's acquisition of EG Group on Wednesday, conditional on the divestment of 41 sites to Metro Petroleum. This removed a key regulatory overhang, with ~471 sites set to transfer by 30 June 2026.

Analysts focused on Ampol's decision to cash settle the scrip component rather than issue equity, widely read as a signal of strong near-term earnings momentum driven by elevated refining margins. The stock rallied 3.4% on the day, and currently up a further 2.2%.

Macquarie retained Outperform, raised target from $40.80 to $46.50, viewing the cash settlement as a signal of strong near-term earnings momentum with refining and F&I International tracking well ahead of expectations and gearing trajectory more contained.

JPMorgan retained Overweight, raised target from $38.00 to $39.00, highlighting that the elevated refining environment enabled favourable deal funding while EG operational underperformance offers meaningful upside beyond stated synergies.

Morgan Stanley retained Overweight, target unchanged at $35.00, noting scrip avoidance is contingent on sustained elevated crack spreads with synergy delivery seen as undemanding given site familiarity.

Analysts' take on The Lottery Corp

[11:36 am] The Lottery Corporation's 2026 Investor Day on Wednesday outlined a digitally led strategic evolution centred on a greenfield app launching within 12-18 months, Keno modernisation via a BYOD distribution model, and a restructured three-vertical operating model.

Analysts were broadly constructive on the through-cycle investment case, viewing the digital acceleration as the key re-rating catalyst, though the absence of formal multi-year targets and soft jackpot activity tempered near-term estimate revisions.

The investor day was marked as non-price sensitive, and TLC shares slipped 1.5% on the day.

UBS retained Buy, lowered target from $6.20 to $6.15, viewing the strategy as a formalisation of previously flagged opportunities under the new CEO with the trim reflecting lower H2 turnover assumptions.

Jarden retained Overweight, raised target from $5.60 to $5.65, materially lifting digital penetration assumptions across outer years while noting management still needs to earn credibility without formal multi-year targets.

JPMorgan retained Overweight, target unchanged at $5.70, flagging that negative YTD lotteries turnover and online Keno discontinuation imply meaningful downside to consensus, partially offset by BYOD expansion potential.

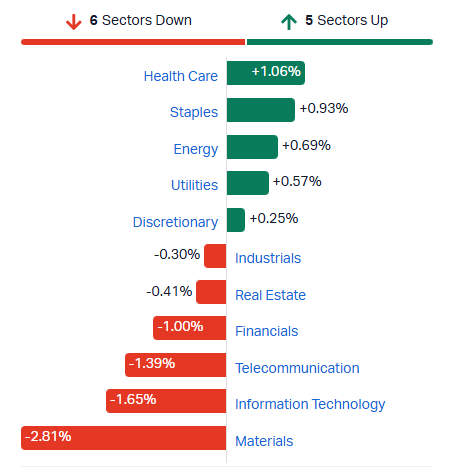

ASX 200 dips, markets on the defensive

[11:33 am] The ASX 200 is down 1.1% in early trade, reflecting a sharp pullback for miners, weakness across most tech names and banks. A very defensive session, where sectors like Healthcare, Staples and Utilities are trading notably higher. Breadth is still fairly weak, with 124 constituents (62%) trading lower.

ASX 200 sectors (Source: Market Index)

Tech stocks take a breather

[10:29 am] The S&P/ASX 200 Tech index is down 2.1% after a ~12% rally between 29 May and 2 June. This follows a relatively weak overnight lead, where the Nasdaq snapped a nine-day winning streak and the iShares Expanded Tech-Software ETF dipped 4.3%.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

360 | Life360 | -5.2% | $21.40 | -33.6% |

CAT | Catapult Sports | -4.3% | $3.53 | -15.1% |

NXL | Nuix | -3.9% | $1.46 | -19.3% |

WTC | Wisetech Global | -3.9% | $39.72 | -42.0% |

PPS | Praemium | -2.8% | $0.69 | -13.2% |

XRO | Xero | -2.8% | $81.57 | -28.4% |

DGT | Digico Infrastructure Reit | -2.7% | $2.51 | -10.0% |

WBT | Weebit Nano | -2.1% | $7.00 | 40.0% |

TNE | Technology One | -1.9% | $32.35 | 17.4% |

BVS | Bravura Solutions | -1.7% | $2.33 | -9.3% |

DDR | Dicker Data | -1.5% | $11.15 | 8.4% |

OCL | Objective Corporation | -1.5% | $10.82 | -34.6% |

DTL | Data#3 | -1.4% | $9.19 | 2.5% |

SDR | Siteminder | -1.3% | $3.70 | -39.6% |

HSN | Hansen Technologies | -1.3% | $4.58 | -13.3% |

CDA | Codan | -1.3% | $42.42 | 49.3% |

AD8 | Audinate Group | -1.0% | $2.04 | -49.8% |

NXT | NextDC | -0.8% | $16.24 | 31.9% |

MAQ | Macquarie Technology Group | 0.0% | $77.58 | 15.8% |

IRE | Iress | 0.0% | $5.96 | -28.9% |

PME | Pro Medicus | 1.4% | $161.84 | -26.7% |

Miners pull back sharply

[10:24 am] The S&P/ASX 200 Materials Index is down 2.9% in early trade, erasing the last two day's worth of gains. Here are the top large cap decliners.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

ILU | Iluka Resources | -6.56% | $7.55 | 30.40% |

LYC | Lynas Rare Earths | -5.23% | $18.47 | 48.83% |

NST | Northern Star Resources | -4.38% | $20.76 | -15.47% |

NIC | Nickel Industries | -4.17% | $1.04 | 17.61% |

FMG | Fortescue | -3.65% | $21.12 | -4.00% |

RIO | Rio Tinto | -3.57% | $187.53 | 27.74% |

LTR | Liontown | -3.51% | $2.34 | 48.73% |

SFR | Sandfire Resources | -3.50% | $19.56 | 8.91% |

CMM | Capricorn Metals | -3.41% | $13.33 | -4.79% |

GMD | Genesis Minerals | -3.39% | $5.70 | -20.39% |

S32 | South32 | -3.26% | $4.75 | 33.80% |

BGL | Bellevue Gold | -2.98% | $1.47 | -13.31% |

EVN | Evolution Mining | -2.88% | $12.12 | -3.58% |

BHP | BHP Group | -2.77% | $63.11 | 38.61% |

Top ASX 200 gainers and losers

[10:20 am] Treasury Wine's is rallying off an above consensus FY26 guidance, coal names catch a bid, while miners and tech stocks experience a sharp pullback.

Ticker | Company | % Chg | Price |

|---|---|---|---|

TWE | Treasury Wine Estates | 7.65% | $4.44 |

EDV | Endeavour Group | 4.53% | $3.00 |

TLX | Telix Pharmaceuticals | 4.02% | $12.69 |

YAL | Yancoal Australia | 3.42% | $7.26 |

WHC | Whitehaven Coal | 3.24% | $9.55 |

FRW | Freightways Group | 2.90% | $11.01 |

ALD | Ampol | 2.52% | $35.84 |

MTS | Metcash | 2.38% | $3.01 |

PME | Pro Medicus | 2.37% | $163.42 |

CBO | Cobram Estate Olives | 2.03% | $4.03 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

PDN | Paladin Energy | -7.09% | $11.01 |

SLX | Silex Systems | -6.96% | $5.88 |

NXG | Nexgen Energy | -6.93% | $15.97 |

IPX | Iperionx | -6.17% | $5.56 |

XYZ | Block | -6.01% | $98.16 |

ILU | Iluka Resources | -5.94% | $7.60 |

360 | Life360 | -5.18% | $21.40 |

LYC | Lynas Rare Earths | -4.82% | $18.55 |

SLC | Superloop | -4.46% | $3.43 |

NST | Northern Star Resources | -4.31% | $20.78 |

Commodities traded broadly lower overnight

[9:53 am] The US-Iran flare up and growing skepticism of a trade deal weighed on commodity prices overnight.

Commodity | % Chg | Last (US$) |

|---|---|---|

Palladium | -5.36% | 1,294.50 |

Platinum | -3.90% | 1,860.10 |

Silver | -3.15% | 72.69 |

Copper | -2.90% | 6.51 |

Nickel | -2.00% | 18,753.03 |

Aluminium | -1.61% | 3,688.80 |

Gold | -1.18% | 4,433.99 |

Brent | 1.49% | 97.38 |

Propel Funeral Partners' FY26 guidance disappoints, bolts on three acquisitions

[9:45 am] PFP has guided FY26 operating EBITDA and revenue below expectations, while announcing three bolt-on funeral services acquisitions for up to $9.1 million.

FY26 revenue guided to $225-230m vs $236.8m ests (4% miss at midpoint)

FY26 operating EBITDA guided to $54.5-56.5m vs $59.7m ests (7% miss at midpoint)

Acquiring three funeral services providers plus related assets, infrastructure (including one cremation facility) and real estate for total consideration of up to $9.1m

Targets generate combined revenue of circa $4.0m, with completion expected in Q4 FY26 or Q1 FY27

Company page: Propel Funeral Partners (PFP)

Racura Oncology raises ~$1m at 23% discount

[9:40 am] Racura Oncology has placed ~526k shares at $1.90 to a specialist institutional healthcare investor establishing an initial equity position.

Placement of ~$1m at $1.90 per share, a 24% discount to the $2.51 last close

Issued to a specialist institutional investor focused on emerging healthcare companies, establishing an initial position on the register

Combined with proceeds from the piggyback options offer and bonus options offers, total funds raised reach $31.2m

Capital earmarked to support clinical development of RC220

RAC shares are down 8% YTD, but up 110% in the last twelve months

Company page: Racura Oncology (RAC)

Treasury Wine Estates' FY26 EBITS guidance beats consensus

[9:38 am] Treasury Wine's Investor Day delivered an FY26 EBITS range ~2% ahead of market expectations, with FY27 guided to at least match and leverage now flagged to peak at 2.9x this year.

FY26 EBITS guided to $480-490m vs $474.2m ests (2% beat at the midpoint)

FY27 EBITS guided to at least equivalent to FY26 vs $487.7m ests (in-line)

Penfolds China customer inventory cover to be reduced by circa 150k cases in FY26, with full rebalancing completed in FY27

Treasury Americas FY26 inventory cover stable with shipments tracking depletions, rebalancing to progress through FY27 and complete in FY28

Leverage expected to peak at 2.9x in FY26, with management confident of returning below the 2.0x target by end-FY28

Deleveraging driven by free cash flow, divestment proceeds and, from FY28, earnings uplift via completed inventory rebalancing and Ascent transformation benefits

Company page: Treasury Wine Estates (TWE)

Chalice upgrades Deep Blue with high-grade Cu-REE rock chips, drilling weeks away

[9:35 am] Rock chip and geophysical results have materially upgraded Chalice's Deep Blue target into a drill-ready, multi-kilometre Copper-Molybdenum-Silver-Rare Earth Element prospect, with first RC drilling planned in coming weeks.

Rock chips returned up to 19.3% TREO and 384-377ppm Cu in isolated outcrop within a circa 2.5km copper-molybdenum-silver soil anomaly

REE assemblage skewed to high-value magnet rare earths (Nd, Pr, Dy, Tb) and defence-critical Sm, Gd and Y, with individual rock chips up to 35,500ppm Nd2O3 and 10,000ppm Pr6O11

Coincident magnetic and gravity anomalies point to a large-scale hydrothermal system with skarn-style affinities extending over 2km+, located circa 15km south-east of the Caravel Copper Project

Target largely concealed beneath agricultural soils with no previous drilling; land access secured for an initial 10-hole RC programme subject to regulatory approvals

Chalice well-funded with circa $63m in cash and listed investments at 31 March 2026

Company page: Chalice Mining (CHN)

Pro Medicus extends Ohio State Wexner deal

[9:30 am] PME's wholly-owned Visage Imaging subsidiary has signed a $16 million, 5-year contract renewal with The Ohio State University Wexner Medical Center, adding Visage 7 Workflow and Visage 7 Cardiology Imaging to the scope.

Transaction-based model with potential upside, negotiated on increased minimums and a higher fee per transaction

OSUWMC is a large academic medical centre with circa 22,000 staff, 2,000 physicians, 1,400+ inpatient beds across six hospitals

Brings total renewals for FY26 to $141m, with management framing the result as evidence of strong client retention

Company page: Pro Medicus (PME)

Magnetic Resources shareholders approve Genesis scheme

[9:28 am] Magnetic Resources scheme holders have voted in favour of the proposed acquisition by Genesis Minerals at an implied $2.00 per share, with implementation tracking to 22 June.

Scheme consideration of $1.40 cash plus 0.0873 Genesis shares per Magnetic share, with all-cash or all-scrip elections available

Supreme Court of WA approval hearing scheduled for 9 June, with ASIC lodgement the following day for the Scheme to become Effective

Magnetic expected to be suspended from ASX trading from close on 10 June, with implementation on 22 June

Magnetic shareholders will own circa 2.4% of the enlarged Genesis pro forma

Company page: Magnetic Resources (MAU)

GDI Property CEO offloads 500k shares

[9:20 am] GDI Property Group CEO Stephen Burns has disclosed the sale of 500,000 shares, primarily to satisfy a personal tax obligation. Burns retains a beneficial interest in 1.6 million shares following the transaction.

Company page: GDI Property Group (GDI)

US services activity beats in May but price pressures intensify on Middle East and tariffs

[9:20 am] The ISM services PMI topped consensus with a strong new orders print, but prices paid hit the highest level since August 2022 and respondent commentary skewed cautious on Middle East tensions and tariffs.

ISM services rose to 54.5 in May vs. 53.8 ests and 53.6 prior, with new orders jumping to 57.3 from 53.5

Prices paid lifted to 71.3 from 70.7, the highest since August 2022, with no commodities reported down in price for a third consecutive month

Employment slipped marginally to 47.9 from 48.0, while inventories surged to 62.5 from 53.1 as respondents flagged confidence activity will hold up amid higher costs

Respondent commentary heavy on price pressures, citing Middle East tensions and tariff policies, alongside mixed signals on supply chains

China-made Tesla deliveries jump 40% in May as broader EV market shows signs of recovery

[9:19 am] Tesla's Shanghai output stepped up in May alongside a 12% lift in the overall China EV market, with BYD snapping an eight-month slide and Leapmotor, Zeekr and Nio all posting strong gains.

Tesla delivered 85,982 NEVs from its Shanghai Gigafactory in May, up 39% year-on-year, with the plant supplying both China and several overseas markets

Total China passenger EV sales hit 1.36m, up 12% y/y and 11% m/m, with the CPCA flagging "an initial recovery" in the market

BYD snapped an eight-month declining streak with 376,990 NEV deliveries, essentially flat y/y at +0.02%

Source: CNBC

Markets split on Fed hike or hold

[9:18 am] The likelihood of a 25 bp hike vs. hold by year end both sit at ~41%, according to CME's Fedwatch Tool.

Source: CME Fedwatch Tool

USTR proposes 10-12.5% tariffs on 60 partners as Trump rebuilds tariff wall

[9:16 am] The forced-labour-linked levies are Trump's biggest protectionist move since the Supreme Court struck down his earlier tariffs, with rates timed to land as the Section 122 stopgap expires in July.

10% rate proposed on imports from Canada, Mexico, EU, Taiwan, UK and others judged to prohibit or commit to prohibiting forced labour imports

12.5% rate on China, India, Japan, South Korea, Brazil and Switzerland for failing to "effectively enforce" such prohibitions

USTR flagged 34 specific goods tied to forced labour inputs, including cotton for garments, critical minerals for solar, fish for fish oil/meal, and palm fruit for palm oil

Apparel/textiles get reduced rates via quotas tied to US export volumes, while beef, tomatoes, bananas, coffee, orange juice, metals, certain fuels/chemicals and USMCA-compliant goods are exempt

Trading partners largely restrained so far, with the EU calling the move unjustified, Beijing denying the allegations, Japan in close contact with Washington, and Australia and India flagging engagement; raises questions over the stability of the May Trump-Xi truce

Source: Bloomberg

Goldman Sachs says markets in "greed" mode as AI funding wave looms

[9:01 am] Goldman's CEO told CNBC there is ample liquidity to absorb the looming wave of trillion-dollar AI listings, pointing to Alphabet's well-received $80bn raise as the first concrete data point that the bid is still there.

Solomon said investors have shifted decisively into "greed" mode, with "plenty of liquidity in the system if the world continues to remain as optimistic"

Comments come ahead of expected mega-IPOs from OpenAI, Anthropic and SpaceX, all potentially at trillion-dollar valuations, alongside other capex-heavy AI raises for data centres, chips and infrastructure

Argued record wealth and liquidity, plus a self-reinforcing cycle of AI profits recycling into taxes and new ventures, support continued issuance

Conceded greed can "turn into fear very quickly" but flagged "a good chance that we're earlier in the cycle than later"

Source: CNBC

Vanguard's VOO becomes first ETF to cross $1 trillion in assets

[9:00 am] A relentless buy-the-dip bid through wars, tariff scares and growth wobbles has propelled Vanguard's S&P 500 tracker past a threshold once thought unimaginable for the ETF industry.

VOO's assets pushed above $1tn after a $1.7bn inflow in the latest session, making it the first and only ETF to cross the milestone and one of just a handful of open-ended funds globally to do so

2026 inflows of ~$69bn make VOO the year's top-gathering ETF, following two consecutive years of $100bn+ annual inflows, with the S&P 500 up 11% year-to-date through multiple all-time highs

Overtook State Street's $787bn SPY as the world's largest ETF in early 2025, with commentary suggesting long-term investors are increasingly defaulting to VOO over SPY as the "easy button"

Sets up a pile of passive cash on standby ahead of expected mega-IPOs this year, including SpaceX

Vanguard is on the cusp of overtaking BlackRock as the world's largest ETF issuer, a notable shift given founder Jack Bogle's well-known scepticism toward the ETF structure

Source: Bloomberg

Americans injured in Iranian missile strike

[8:59 am] A Fateh-110 ballistic missile strike on the Ali Al Salem air base over the past 24 hours injured several Americans and damaged $60 million worth of US Reaper drones.

Kuwaiti air defences intercepted the missile but falling debris hit the base, with one MQ-9 Reaper destroyed and at least one other seriously damaged at ~$30 million each

About five contractors and active duty personnel suffered minor injuries

Trump flagged he was ready to make a "final determination" on a preliminary deal on Friday, but a circa two-hour Situation Room meeting concluded without announcement

Operation Epic Fury casualty count now sits at 14 US dead and 409 injured

Source: Bloomberg

US-Iran clashes flare across the Gulf, putting April truce at risk

[8:54 am] The most serious escalation since the April ceasefire saw Iran target US bases in Bahrain and Kuwait while US forces struck inside Iran, sending oil higher and reigniting Strait of Hormuz supply concerns.

Iran targeted the US' main regional naval base in Bahrain and the Ali Al-Salem airbase in Kuwait, with a separate strike on Kuwait's civilian airport killing at least one person and halting flights

US forces struck a communications tower on Iran's Qeshm Island near the Strait of Hormuz and hit an empty Iran-bound tanker, with Secretary of State Rubio confirming the US is also striking drone launch personnel

Oil extended its rally and bond yields rose on the escalation, with markets pricing in renewed inflation risk

Source: Bloomberg

Broadcom slides ~14% after-hours as AI chip guide undershoots lofty expectations

[8:51 am] Broadcom's Q2 result was largely ahead of market expectations, but guidance fell short of consensus, deflating a stock that had added ~$270 billion in market cap over the prior five sessions.

Q2 results and guidance:

Revenue up 48% to $22.19bn vs $22.13bn ests (in line)

Adj. EPS up 54% to $2.44 vs $2.39 ests (2% beat)

Semiconductor Solutions up 79% to $15.0bn vs $14.65bn ests (2% beat)

AI Semiconductor revenue up 143% to $10.8bn vs $11.3bn buyside ests (4% miss)

Dividend of 65 cps

Q3 AI semiconductor revenue ~$16bn vs $17.2bn ests (7% miss)

Other takeaways:

FY26 AI chip revenue guided to $56bn vs $57.6bn ests, with CEO Hock Tan flagging questions remain over revenue recognition timing across multi-year backlogs

Apollo/Blackstone working on a ~$36bn debt deal for Anthropic to buy Google chips developed with Broadcom

CEO on AI supply: “Getting supply is not just about dropping money... though that does work. We are very comfortable that we have been able to secure supply... for our needs in 2026 and 2027.”

CEO on AI bookings: “Customers have been coming to us incrementally over the last few months. Expect that to continue. Our visibility runs all the way to 2028 right now. Three months ago ... visibility ran pretty much to 2027. Today, it runs to 2028.”

Alphabet upsizes record-breaking raise to $84.7bn as AI capex bill grows

[8:49 am] Alphabet lifted its equity offering by nearly $5 billion just two days after launch, in what is now set to become the largest equity capital markets deal on record.

Raise upsized to $84.75bn from $80bn announced two days earlier, eclipsing Petrobras' circa $70bn 2010 deal as the largest ECM transaction ever

Structure includes a $40bn at-the-market program (selling into the open market from Q3), a $10bn deal with Berkshire Hathaway, $18bn in Class A and Class C stock, and $16.75bn in depository shares

Demand reportedly multiple times oversubscribed

Proceeds earmarked for AI capex, with Google leaning into growing demand for its in-house TPU chips as an alternative to NVDA's processors

US markets snap nine-day rally as Middle East tensions lift oil and yields

[8:46 am] Defensive tilt took hold across US equities overnight, with oil up for a third straight session, firmer higher and renewed equity supply headlines combining to break the S&P 500's nine-session winning streak.

Dow (1.21%), S&P 500 (0.74%), Nasdaq (0.89%), Russell 2000 (1.31%), with stocks ending near session lows

Laggards spanned private equity, software, tech , big banks, precious metals and airlines, while energy, REITs, semis, staples and some retail outperformed

Brent up 1.4% to US$97.3 a barrel as latest Middle East escalation, alongside growing scepticism around a near-term framework agreement

Equity supply pipeline in focus with Alphabet upsizing its raise to nearly $85bn, SpaceX reportedly looking to raise $75bn at a $1.75tn valuation, and USTR floating broad 10-12.5% tariffs tied to forced labour practices

S&P 500 had rallied nearly 20% across the prior nine weeks heading into the session, leaving a higher bar for incremental gains

Good morning!

[8:31 am] ASX 200 futures are down 75 pts (-0.85%)

The overnight session in a nutshell:

US benchmarks snapped a historic run, with the S&P 500 closing its first down day in nine sessions as oil and Treasury yields rose on renewed Iran-US strikes.

Trump flagged a deal could come "fairly quickly" even as the Iran blockade risks dragging past Labor Day, after a sharp escalation in the Gulf, including Iranian missile and drone strikes on Kuwait and Bahrain, US strikes on a ground control station on Qeshm Island and the disabling of an Iran-bound oil tanker

Broadcom delivered a blowout Q3 AI guide ($16bn, over 200% growth) but shares slid ~12% after hours