ASX 200 Live Today - Thursday, 2nd July

The S&P/ASX 200 is set to fall after US stocks struggled for upside amid a sharp downturn for tech stocks. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, July 2. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

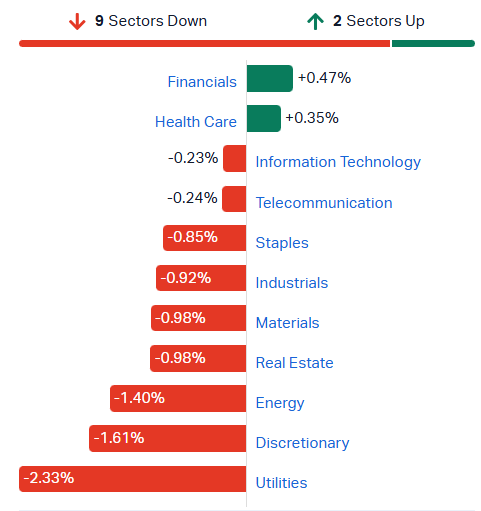

ASX 200 falls on broad weakness

[10:49 am] The S&P/ASX 200 is down for a third straight day, trading 0.41% lower (but already off session lows of -0.76%). Nine out of eleven sectors in red, with 127 constituents (63%) in red.

Discretionary is in the mist of a pullback after a sharp ~22% run between 12 May and 30 June, Energy stocks slip after a four-day win streak and Materials have now dipped to a fresh two-month low.

S&P/ASX 200 sectors (Source: TradingView)

Top ASX 200 gainers and losers

[10:14 am] Gold, defence and tech stocks top the leaderboards, while Megaport tumbles post-retail entitlement offer, Monadelphous was downgraded by Bell Potter this morning (to Hold from Buy; target cut by 14% to $32) and South32 pulls back after yesterday's ~10% rally.

Ticker | Company | % Chg | Price |

|---|---|---|---|

OBM | Ora Banda Mining | 5.88% | $1.08 |

EOS | Electro Optic Systems | 5.63% | $10.32 |

DRO | Droneshield | 4.18% | $2.49 |

360 | Life360 | 3.98% | $27.20 |

NWS | News Corp | 3.63% | $42.07 |

GGP | Greatland Resources | 3.21% | $11.26 |

MI6 | Minerals 260 | 3.19% | $0.71 |

PXA | Pexa Group | 2.91% | $10.96 |

CYL | Catalyst Metals | 2.91% | $4.95 |

RMD | Resmed | 2.78% | $29.20 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

MP1 | Megaport | -9.44% | $18.81 |

MND | Monadelphous Group | -9.14% | $28.33 |

S32 | South32 | -5.84% | $4.03 |

SGM | Sims | -4.65% | $24.79 |

KAR | Karoon Energy | -4.58% | $1.36 |

SLX | Silex Systems | -4.55% | $5.45 |

NWH | NRW | -4.28% | $7.15 |

WES | Wesfarmers | -3.55% | $87.29 |

NXT | NextDC | -3.21% | $14.17 |

SGH | SGH | -3.18% | $44.13 |

Emerald Resources misses FY26 guidance

[9:55 am] The Okvau mine strengthened over the second half after a weaker start to the year weighed on full-year production.

June quarter gold production of about 27koz at Okvau, within ongoing quarterly guidance of 25koz to 30koz

Indicative June quarter AISC anticipated at the lower end of guidance around US$880/oz

FY26 gold production of about 100koz, below full-year guidance of 105koz to 120koz on weaker early-year quarters, with the final two quarters both within guidance

Indicative FY26 AISC in line with guidance at around US$966/oz

Cash, bullion and listed investments of $468m (US$322m) as at 26 June, remaining fully funded, debt free and unhedged

Targeting multi-mine output above 300koz a year via Okvau expansions, the Memot project in Cambodia and the Dingo Range project in Australia

Company page: Emerald Resources (EMR)

Northern Star meets revised FY26 gold sales guidance

[9:54 am] A strong June quarter lifted full-year output above the 1,500koz revised target, with the KCGM mill expansion tracking to schedule.

Total gold sold of 433koz for the June quarter, bringing FY26 gold sold to 1,543koz versus revised group guidance of above 1,500koz

Kalgoorlie Production Centre sold 844koz for the year including 468koz from KCGM, with Yandal at 434koz and Pogo at 265koz, all meeting revised guidance

Unaudited cash and bullion of $1,255m at 30 June, up from $1,183m at 31 March, with no corporate bank debt

Purchased $129m of shares during the quarter under the $500m on-market buy-back program

KCGM Mill Expansion Stage I, lifting throughput from 13Mtpa to 27Mtpa, on track for commissioning in early FY27, with Stage II consolidation of Gidji into the Fimiston mill due by end-2026

AISC to be finalised and reported in the June 2026 Quarterly Activities Report, with quarterly results due 29 July 2026

Company page: Northern Star Resources (NST)

Intelligent Monitoring Group to acquire ADT's UK residential security business for $347m

[9:53 am] The transformational deal more than triples pro forma earnings and adds a large recurring revenue base in one of the world's biggest monitored security markets.

Binding agreement to acquire ADT's UK residential security business for £180m, comprising £155m cash and £25m in IMG shares issued to Johnson Controls International

Adds $12.5m per month in recurring revenue, up 205%, from more than 160,000 direct customers

Expected to lift pro forma annualised EBITDA by around 300% to $130m, against FY26 guidance of $43-$47m

Forecast to be 40% earnings accretive, increasing pro forma EPS to 9.0cps at the current GBP/AUD exchange rate

Company page: Intelligent Monitoring Group (IMB)

Electro Optic Systems secures two Middle East defence orders

[9:52 am] The company landed new naval weapons and counter-drone contracts across the region, spanning both new and existing customers.

Secured a US$16m (around $23m) order for its Naval R400 Remote Weapon System from a new Middle East customer, with delivery expected over the next seven years

MARSS command and control business won an £8m (around $15m) counter-drone defence order from an existing Middle East customer, expected to be substantially delivered across 2026 and 2027

Company page: Electro Optic Systems (EOS)

Kelsian wins Auckland ferry contract

[9:51 am] The Western Package Ferry Contracts secure long-term New Zealand revenue and come alongside a bolt-on acquisition to support delivery.

Awarded the contracts alongside Belaire Ferries for services commencing 1 July 2027, securing total revenue of NZ$101m ($83m) over the initial seven-year term

Entered a binding agreement to acquire Auckland-based Belaire Ferries for NZ$8.9m ($7.3m) cash, comprising NZ$2.8m ($2.3m) upfront and up to NZ$6.1m ($5.0m) in deferred and contingent consideration across FY27-FY29, with completion expected in Q1 FY27

Undertaken to procure five new ferries over the contract term, with the first entering service mid-2028 and the rest between 2029 and 2032

Total estimated capital cost of the five vessels is NZ$38m ($31m), expected to be funded through a limited recourse ringfenced financing vehicle

Company page: Kelsian Group (KLS)

Smart Parking expands US footprint with US$12m acquisition of American Parking

[9:42 am] The deal lifts Smart Parking's US sites under management above 200 across seven states and opens Oklahoma and Arkansas for its SmartCloud technology rollout.

Acquiring American Parking, a Tulsa-based operator of 54 locations across Oklahoma, Texas and Arkansas offering lot management, enforcement, event parking and valet services

Purchase price of US$12m funded from cash reserves, debt facility and scrip, split US$11m cash and US$1m in SPZ shares deferred for six months

American Parking generated 2025 revenue of US$8.0m and EBITDA of US$1.4m, implying an acquisition multiple of about 8.6 times EBITDA

Transaction expected to be EPS accretive pre-synergies

Adds scale in states adjacent to SPZ's existing Texas operations, with room to deploy the proprietary SmartCloud platform across the new sites

CEO Paul Gillespie to relocate to the US in H1 FY27 to drive performance

Company page: Smart Parking (SPZ)

Iluka signs 18-year rare earths concentrate supply deal with VHM for Eneabba feedstock

[9:40 am] The agreement secures all planned rare earth concentrate from VHM's Goschen project as complementary feedstock for Iluka's Eneabba refinery.

VHM to supply 146kt of rare earths concentrate containing 86kt of rare earth oxides over 18 years, averaging about 8,320tpa of concentrate and around 4,900tpa of total rare earth oxides

Iluka granted a right of first refusal over any additional rare earths from Goschen and VHM's earlier stage Cannie and Nowie projects

Iluka to provide a $40m secured convertible note in two tranches, $10m initially and $30m after final investment decision, as part of the construction funding package

Concentrate pricing linked to the price Iluka realises from selling its rare earth products from Eneabba

Eneabba now more than 50% complete with commissioning due mid-2027, producing separated light and heavy rare earth oxides

Company page: Iluka Resources (ILU)

Northern Star names Glencore's Suresh Vadnagra as new CEO

[9:39 am] The incoming chief brings more than 25 years of global mining experience, with a CFO stepping up as interim leader during the handover.

Vadnagra to become Managing Director and CEO effective 5 October 2026, joining from Glencore where he heads its Nickel and Zinc Industrial Assets across more than 25 global operations

Previously Chief Technical and Projects Officer at Newcrest, overseeing major projects including Red Chris, Cadia, Havieron and Wafi-Golpu, with earlier roles at BHP, Iluka, and MMG including Las Bambas in Peru

Stuart Tonkin steps down during the first quarter of FY27 after 13 years, with CFO Ryan Gurner appointed deputy CEO immediately and serving as interim CEO between Tonkin's departure and Vadnagra's start

Company page: Northern Star Resources (NST)

Fortescue's Forrest pitches green mining as a cost advantage, not a cost

[9:20 am] Speaking on the In Good Company podcast, the chairman and CEO argued decarbonisation, electrification and AI will structurally lower costs and widen Fortescue's competitive lead.

On green mining: Forrest expects eliminating roughly one billion litres of diesel a year to deliver around US$1bn in annual savings, framing decarbonisation as a cost advantage rivals will eventually be forced to match

On strategy: Fortescue deliberately stayed focused on iron ore rather than diversifying into copper, nickel or other critical minerals, with that discipline credited for its ability to challenge far larger incumbents

On competitive position: already one of the world's lowest-cost iron ore producers, with electrification and renewables investment expected to widen that gap further

On AI: autonomous equipment, predictive operations and intelligent energy management are already cutting operating costs by hundreds of millions of dollars, and seen as a growing differentiator

On incumbents: rivals have been slow to decarbonise because diesel subsidies dull the incentive to innovate, with broader adoption likely only once Fortescue proves the economics

On China: still viewed as the most important customer base, with Forrest constructive on long-term Chinese steel demand and the country's pragmatic approach to iron ore consumption

This is genuinely a good listen. You can check out the full podcast here.

Alcoa acquires South32's aluminium assets: Q&A highlights

[9:12 am] Management framed the deal as a defining step in building a pure-play upstream aluminium leader, with call commentary focused on pricing, synergies and balance sheet capacity.

Upfront consideration of US$4.1bn split into US$3.1bn cash and 17 million new Alcoa shares (about 6% post-issuance), with implied enterprise value of around US$4.7bn including assumed liabilities, plus a contingent value right of up to US$750m

Acquisition multiple of roughly 5.2 to 6.1x the assets' 2025 EBITDA of about US$900m depending on the CVR outcome, below Alcoa's own five-year average of about 6.3 times

On a 2025 pro forma basis the assets would lift EBITDA by around 45%, revenue by 28%, alumina production by more than 50% and aluminium production by nearly 40%

Around US$900m of net present value synergies identified, including roughly US$50m of run-rate cost savings within the first 12 months, with the largest long-term gains from optimising the co-located Western Australia mine plan

On asset economics, Oplinger said: "We're acquiring smelting capacity at about $1,850 per tonne. We're acquiring refining capacity at $600 per tonne," both below what he cited as Western world new-build costs of US$7,000 to US$8,000 a tonne for smelting and US$1,500 to US$2,000 for refining.

On why add alumina exposure now, Oplinger said the market has been "very rational" over the past 5 to 10 years, with curtailments when prices dip, noting alumina had stabilised and recovered to US$330 a tonne from US$305.

On the balance sheet, CFO Molly Beerman confirmed the US$3.1bn will be funded by a mix of balance sheet cash and long-term unsecured notes rather than new equity beyond the share consideration, with Oplinger pointing to strong second-half cash generation, US$500m to US$1bn of data centre asset sales and monetisation of the first Ma'aden share tranche in mid-2028.

On individual assets, Hillside and the Alumar refinery and smelter are currently EBITDA positive, while Worsley sits around breakeven at roughly US$310 to US$315 a tonne and turns EBITDA positive around US$330.

Perpetual rejects unsolicited $21.64 a share takeover approach from EQT-linked Windflower

[9:11 am] The wealth manager knocked back a non-binding, conditional and indicative scheme proposal it said did not represent fair value.

Windflower, understood to be indirectly controlled by EQT AB, proposed acquiring all shares at $21.64 cash each, reduced by any dividends, capital returns or distributions

Board rejected the approach as highly conditional and not in the best interests of shareholders in a change of control context

Shareholders need take no action, with the company to provide updates in line with continuous disclosure obligations

Company page: Perpetual (PPT)

Goldman flags return to oil surplus as Hormuz flows normalise

[9:06 am] Goldman Sachs expects the market to swing back into oversupply next year as the Iran war premium fades, with strategic reserve rebuilding only partly offsetting the glut.

Surplus expected to average just over 3 million barrels a day next year, or close to 2 million after around 1 million barrels a day of global strategic reserve rebuilding

Hormuz export flows expected to fully normalise by the end of July despite recent vessel attacks

US strategic reserve fell from 415 million barrels at end-February to 331 million by June 19, the lowest since 1983, following an IEA-coordinated record 400 million barrel release

Morgan Stanley echoes the call, cutting price forecasts twice in a fortnight and describing the market as back to surplus

Source: Bloomberg

US lifts export restrictions on Anthropic's Mythos and Fable models

[9:03 am] The Commerce Department has removed a licensing requirement that had forced Anthropic to cut public access to two of its most advanced models.

Anthropic began restoring access on Wednesday July 1, after the models were added to the export-restricted list on June 12

The rule had barred access for foreign nationals without special approval, which proved impractical to comply with at scale

Anthropic agreed to proactively detect security risks, work with the government on release protocols and report malicious activity, much of which it had already pledged voluntarily

Easing came under pressure from Asian rivals such as Fugu and Tulongfeng releasing models approaching Mythos-level capability

Source: TechCrunch

US crude grades shed war premium as Hormuz flows recover and glut looms

[9:03 am] Easing supply fears from the Iran truce and surging Strait of Hormuz shipments have pushed key US oil grades back to steep discounts and multi-year lows.

Medium sour benchmark Mars fell to a $3 discount to Nymex futures, its steepest since January 2023, having peaked at a near US$18 premium in late March at the height of the war

Permian crude in Houston hit its widest discount to futures since 2020 last week, down from an almost US$8 premium at the war's peak

Hormuz oil flows have rebounded to more than 10 million barrels a day with US military support, up toward the pre-war average of about 20 million and easing Iran's ability to choke the corridor

US crude exports fell to just over 4 million barrels a day last week, down from a near 6.5 million peak in late April, as Asian buyers cut US imports on surging freight costs

Cushing stockpiles rose for the first time in 10 weeks but remain below 20 million barrels, with total US commercial petroleum stocks at their lowest since March 2025

US proceeding with release of all 172 million barrels from the strategic reserve despite falling prices, adding further Mars-quality supply to the market

Meta pops 9% on plans to sell excess AI compute through new cloud business

[9:02 am] The Facebook-parent aims to recoup some of its heavy AI infrastructure spend by selling spare computing capacity to outside customers.

Shares closed up nearly 9% on plans to monetise unused compute, easing investor unease over infrastructure spending

Debating whether to offer access to hosted AI models or sell raw computing power, per Bloomberg

Move follows April guidance to spend up to US$145bn on capex this year on data centres and GPUs

Pushes Meta into a competitive cloud market dominated by Amazon, Microsoft, Google and CoreWeave

Neocloud peers CoreWeave and Nebius Group both sank ~12% on the news

Source: CNBC

Warsh says inflation risks have eased but declines to signal rate path

[9:00 am] The Fed chair used a Sintra panel to stress central bank independence, rule out forward guidance and flag a long road to a smaller balance sheet.

Two-year Treasury yields fell to session lows around 4.15% after Warsh said inflation expectations and risks had come down over the past four weeks

Reiterated a 2% inflation target commitment despite the latest core PCE running at 3.4% and headline at 4.1% year-on-year, with recent falls in energy and petrol prices on US-Iran peace talks

Declined to give forward guidance ahead of the July 28-29 meeting, where half of 18 officials projected a rate increase this year and markets are pricing at least one 25bp hike by year-end

On the $6.7tn balance sheet, favoured a smaller portfolio but said any runoff would be FOMC-led and take more than 18 weeks, cementing Wall Street views that shrinkage won't begin until 2027

Named a Bessent aide, Samantha Schwab, among new advisers, with task-force membership including outside experts due next week

On AI, said it was too soon to judge inflation effects but expected a supply-side productivity boom to become clearer within six months

Tesla European registrations climb in June ahead of Q2 delivery report

[8:53 am] Registrations rose across several European markets, extending a sales recovery that analysts expect to underpin second-quarter deliveries.

Registrations rose 39% in Denmark, 56% in Sweden, 43% in Portugal and Italy, and more than doubled in France, with Spain up a softer 5.6%

Norway bucked the trend, with registrations down 43% year-on-year on front-loaded demand ahead of a 2026 cut to tax benefits

France a bright spot, supported by EV subsidies, faster fleet electrification and a recovery from last year's Musk-related controversy

Analysts expect Tesla to report a 5% rise in Q2 deliveries, with much of the gain from Europe

European battery-electric vehicle registrations rose 39.1% in May, helped by higher fuel prices, with Britain and Germany June data due later this week

Source: Reuters

Microsoft plans fresh job cuts as it reins in costs amid AI ramp

[8:52 am] The tech giant is preparing to announce layoffs next week affecting less than 2.5% of its workforce, a smaller round than last year's cuts.

Cuts expected to hit thousands of roles across sales, consulting and the Xbox gaming division, with some affected staff offered new roles immediately

Round projected at under 2.5% of the 220,000-person workforce, versus roughly 15,000 roles (about 4%) cut last year

Earlier voluntary buyout offer to eligible US staff aged and serviced 70-plus years saw about a third take up, allowing a lower headcount reduction this time

Stock down about 19% over the past month, its worst month since the dot-com era, on concerns AI could displace software services

Xbox reductions anticipated since new gaming CEO Asha Sharma called for a business "reset"

Source: Business Insider

Nike slides as cautious outlook offsets a Q4 beat

[8:51 am] Management flagged persistent consumer weakness and a longer turnaround, overshadowing better-than-expected quarterly sales and profit.

Shares surprisingly rallied 4.9% but still down 32% YTD

Next quarter expected to slow versus the current period on North America wholesale shipment timing, with no meaningful improvement seen over the next six months

Greater China down 12% year-on-year and in line with expectations, prompting a "comprehensive reset" toward local product creation and premium positioning

Converse revenue plunged 32% in Q4, with full-year sales the lowest since 2011, raising questions over the brand's future at Nike

Source: Bloomberg

Short sellers ramp up SpaceX bets, already sitting on US$760 million paper loss

[8:45 am] Short interest in SpaceX has jumped to nearly a third of its free float since the June IPO, with bears betting on a resumed decline even as the position has cost them dearly so far.

Short interest stands at 196 million shares, about 31% of the free float, up from 83 million shares or 13% a week earlier, per Ortex data

Shorts are sitting on mark-to-market losses of about US$760 million since the IPO, though that's down from a peak of around US$2.5 billion when the stock bottomed near $153 last week

Every $1 move in SpaceX's share price translates to roughly US$200 million in gains or losses for short sellers, Ortex estimates

Shares fell as much as 23% in the days following the June 12 debut before rebounding

Cost to borrow the stock remains relatively cheap at about 1%

SpaceX's valuation of more than US$2 trillion makes it a target for sceptical shorts, though strong retail and institutional demand pose a risk to that bet

Ortex co-founder Peter Hillerberg said a continued rebound could trigger short covering, with "a lot of potential fuel if it tips into a squeeze"

Source: Reuters

Global M&A tops US$2.6 trillion as first-half deal surge sets records

[8:43 am] Global dealmaking surged in H1 2026, with light-touch regulation and an AI-driven push for scale fuelling the busiest six months for mega-deals on record.

Global transaction values rose around 30% y/y to US$2.6 trillion in the first half, putting 2026 on course to potentially beat the 2021 record

Companies struck 38 deals worth US$10 billion or more, the most ever in a six-month period, surpassing the prior record set in H2 last year

NextEra Energy's US$67 billion bid for Dominion Energy would create a US energy giant

AvalonBay Communities and Equity Residential are pursuing a tie-up with a combined market value of more than US$50 billion

Unilever is selling its food division to McCormick & Co for about US$45 billion

Kone Oyj is paying €29.4 billion for TK Elevator GmbH

Fox Corp is paying about US$22 billion for Roku in a bid to expand its streaming footprint

Dealmakers expect the second half to be as strong or stronger, citing a deep pipeline of carve-outs and portfolio rebalancing, though the US election in November is flagged as a watch point

Source: Bloomberg

Global equity raising hits second-best half on record, tech dominates

[8:38 am] Global equity fundraising topped $729.4 billion in the first half of 2026, the second-best start to a year on record, according to Mergermarket data.

SpaceX's record IPO, which raised US$86.25 billion on 12 June, underpinned the surge

Tech deals accounted for roughly US$302 billion of global issuance, an all-time record for the sector in a first half

Tech companies have raised more than US$100 billion in a first half only twice before, in 2000 and 2021

Neither period preceded strong near-term market performance, the dot-com peak came in March 2000 and the 2021 IPO wave preceded the Nasdaq crash in early 2022

The scale of tech issuance raises questions over investors' capacity to absorb further raises expected in coming months

OpenAI is reportedly considering pushing its planned listing into 2027, according to the New York Times

Anthropic filed confidential IPO paperwork in early June, with a listing possible as soon as this spring

Meta is weighing a stock offering in the second half to fund its AI ambitions

Source: WSJ

Good morning!

[8:36 am] ASX 200 futures are down 23 pts (-0.26%).

The overnight session in a nutshell:

Wall Street began the third quarter mostly lower as a two-day technology rally faded, with the S&P 500 and Nasdaq slipping and the Dow roughly flat

Fed Chair Warsh, in his first international appearance, called inflation too high and stressed independence, hardening bets on a possible September rate hike

Meta soared 8.8% on plans to sell excess AI computing power, Eurozone inflation came in slightly cooler-than-expected, NYSE-listed Alcoa tumbles 8.9% on its South32 aluminium acquisition