ASX 200 Live Today - Thursday, 21st May

The S&P/ASX 200 will have another crack at bouncing from recent lows, as Wall Street rallied on US-Iran peace talks.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, May 21. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 higher as Materials and REITs bounce

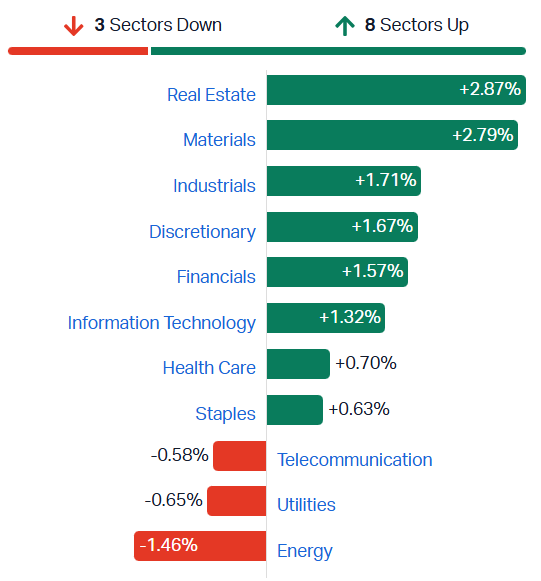

[2:05 pm] ASX 200 currently up 1.54%, slightly off session highs of 1.80%. Overall, a fairly encouraging session, with broad participation (166 or 83% of constituents higher) and sizeable bounces for sectors like Real Estate and Materials.

S&P/ASX 200 sectors (Source: Market Index)

Still, the past couple of days have shown how easily the market can rip back down on another US-Iran escalation, higher oil prices, or further upward pressure on yields.

While oil prices tumbled on Tuesday after Trump said the US is in the "final stages" with Iran, Bloomberg observes a number of key challenges for energy markets:

Rabobank flags physical markets remain "in disarray," with 55-day Persian Gulf-to-destination transit times meaning inventories continue to draw

Adnoc CEO says Middle East oil flows would not fully recover until well into 2027 even if conflict ended immediately, calling Hormuz closure the most severe supply disruption on record

US crude stockpiles drew 7.9m barrels last week as overseas buyers stock up on American oil to offset Middle East disruption

That's all for today. Thanks for tuning in.

Elders Chairman lifts stake by ~96%

[1:25 pm] Elders Chairman Glenn Davis has disclosed an on-market purchase, taking his beneficial holding to ~51,000 shares.

Purchased 25k shares at $5.69, representing ~$142k in proceeds

Holding nearly doubled from 26k to 51k shares post-transaction

Elders tumbled 22.9% on Monday after the company's 1H26 missed market expectations, with elevated corporate services costs weighing on profitability

Company page: Elders (ELD)

Global oil stockpiles draw at record pace in May

[1:24 pm] Goldman Sachs estimates global oil and product inventories are being drawn down at a record pace this month as the Iran war continues to disrupt supply through the Strait of Hormuz, Bloomberg reports.

Visible inventories contracting at a record 8.7m barrels/day so far in May, nearly double the average pace since the conflict began

Estimated oil exports through Hormuz remain at just 5% of normal levels amid the double blockade by Iran and the US

~Two-thirds of May draws driven by a drop in oil on water, with the import slump now spreading from Asia to Europe

Jet-fuel imports into Europe running 60% below 2025 averages

China showing "lack of appetite" for crude with large declines in imports and local fuel sales down 22% last month on weaker activity

IEA warns the market will remain "severely undersupplied" until October even if the conflict ended soon

Source: Bloomberg

Foreign investors return to Chinese equities in April

[1:23 pm] Foreign investors poured back into mainland Chinese equities in April, with estimated net inflows hitting ~200bn yuan ($29bn), the largest monthly amount since January.

Bloomberg estimate based on China's cross-border securities investment balance after stripping out observable flows, serving as a proxy since Beijing stopped publishing northbound flows in mid-2024

Returning appetite came despite earlier selloff driven by the Iran war, with investors looking through Middle East disruption

Inflows coincided with a broader China tech rally driven by AI-related productivity gains

CSI 300 Index up 8% in April and a further 0.9% so far in May

Signals renewed offshore positioning interest at a time when direct flow data visibility is limited

Source: Bloomberg

Gold stocks broadly higher

[12:33 pm] Most gold names are trading 2-3% higher after gold prices bounced 1.3% overnight off a near two-month low to US$4,543/oz. Still, most stocks remain sharply lower over the past week, reflecting ongoing softness in bullion prices.

Ticker | Company | % Chg | Price | 1 Week |

|---|---|---|---|---|

MEK | Meeka Metals | 8.7% | $0.13 | -3.8% |

CYL | Catalyst Metals | 3.9% | $5.40 | -5.2% |

CMM | Capricorn Metals | 3.9% | $12.79 | -9.3% |

RMS | Ramelius Resources | 3.6% | $3.18 | -10.4% |

BGL | Bellevue Gold | 3.3% | $1.49 | -11.2% |

VAU | Vault Minerals | 3.2% | $4.41 | -8.0% |

BC8 | Black Cat Syndicate | 3.1% | $1.06 | -12.6% |

EVN | Evolution Mining | 2.6% | $11.67 | -11.4% |

NEM | Newmont | 2.6% | $150.33 | -8.6% |

RSG | Resolute Mining | 2.5% | $1.22 | -11.6% |

AMI | Aurelia Metals | 2.4% | $0.30 | -16.3% |

ALK | Alkane Resources | 2.2% | $1.49 | -1.5% |

RRL | Regis Resources | 2.2% | $6.32 | -7.4% |

PNR | Pantoro Gold | 2.2% | $3.08 | -5.7% |

PRU | Perseus Mining | 2.1% | $5.26 | -6.9% |

EMR | Emerald Resources | 1.6% | $5.74 | -8.3% |

OBM | Ora Banda Mining | 1.5% | $1.33 | -4.3% |

WGX | Westgold Resources | 1.5% | $5.03 | -9.6% |

GMD | Genesis Minerals | 1.2% | $5.87 | -11.2% |

SBM | St. Barbara | -1.7% | $0.57 | -18.0% |

NST | Northern Star Resources | -2.2% | $18.93 | -12.8% |

Banks bounce from five-month lows

[12:29 pm] Banks are trading broadly higher after the S&P/ASX 200 Financials Index tumbled to a five-month low last Tuesday. The index is now up 4.1% in the last six sessions.

Ticker | Company | % Chg | Price | 1 Year |

|---|---|---|---|---|

JDO | Judo Capital | 5.9% | $1.39 | -2.7% |

NAB | National Australia Bank | 2.7% | $37.79 | 0.9% |

WBC | Westpac | 2.5% | $36.41 | 17.1% |

ANZ | ANZ Group | 1.8% | $35.41 | 21.5% |

BOQ | Bank Of Queensland | 1.7% | $6.38 | -17.1% |

MQG | Macquarie Group | 1.5% | $239.74 | 14.2% |

CBA | Commonwealth Bank | 1.3% | $164.81 | -4.8% |

BEN | Bendigo & Adelaide Bank | 1.1% | $10.53 | -11.0% |

ASX 200 trading near session highs

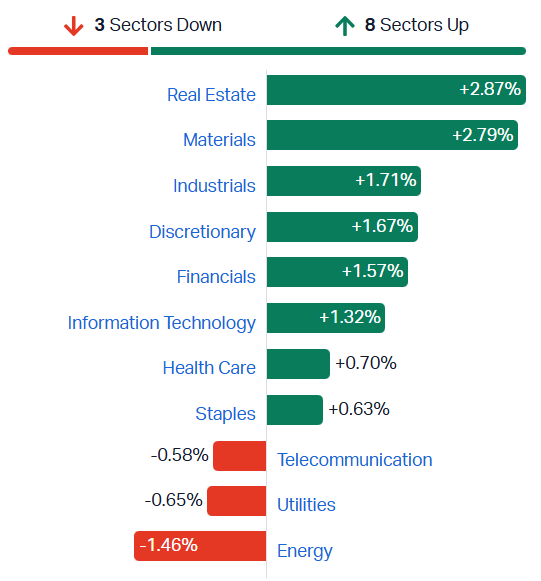

[12:24 pm] The S&P/ASX 200 is currently up 1.69%, now fractionally higher for the week. Bond yields have experienced a notable pullback, with the Aussie 10-year down 6 bps to 4.95% and approaching the lower bond of its recent trading range. The yield-sensitive Real Estate sector is trading sharply higher, while Materials is also experiencing a notable bounce after five straight days of declines.

S&P/ASX 200 sectors (Source: Market Index)

Australia government 10-year bond yield (Source: TradingView)

Analysts' take on Catapult

[12:21 pm] Catapult Sports' FY26 result on Wednesday beat market expectations, with management EBITDA significantly outperforming guidance on accelerating organic growth, successful integration of Perch and Impect, and strong cross-sell momentum across the installed base. The stock closed 17.7% higher on the day.

Bell Potter retained Buy, raised target from $4.50 to $4.65. Management EBITDA significantly beat both broker and consensus expectations, with guidance raised modestly on margin expansion and a strong balance sheet supporting forward cash build.

Morgan Stanley retained Overweight, raised target from $5.00 to $5.20. Revenue and EBITDA beats were driven by strong organic growth and well-performing recent acquisitions, with the outlook supported by continued margin improvement and operating leverage.

Analysts' take on Webjet

[12:19 pm] Webjet's FY26 result on Wednesday was broadly in line with guidance but EBITDA margins compressed from strategic reinvestment, with analysts focused on Virgin Australia's material commission renegotiation, RBA surcharging changes, and weak domestic leisure demand as compounding FY27 headwinds. The stock closed 11.2% on the day.

Jarden retained Overweight, lowered target from $0.90 to $0.80. Valuation-supported call despite execution risks and market share losses, with corporate and international segments seen as key near-term growth catalysts.

RBC Capital Markets retained Outperform, lowered target from $1.00 to $0.80. Acquisition likelihood increases given a deal-making chair and motivated external shareholders, with a strong balance sheet supporting strategic flexibility.

JPMorgan retained Neutral, lowered target from $0.90 to $0.50. Limited forward visibility despite an undemanding valuation, with Virgin commission changes and RBA surcharging regulation presenting difficult-to-offset margin pressure.

Australia unemployment rises to 4.5% in April

[12:14 pm] Australia's seasonally adjusted unemployment rate ticked higher to 4.5% in April, reinforcing signs of a softening labour market.

Unemployment rate up to 4.5% from prior month (vs. 4.3% ests), with unemployed persons up 33,000

Employment down 19,000, with full-time down 11,000 and part-time down 8,000

Female employment drove the decline (full-time -19,000, part-time -13,000), the first fall since August 2025, while male employment rose 13,000

Underemployment rate down 0.1ppt to 5.8%, with hours worked up 0.8% as hours worked per person rose 0.9%

Trend unemployment rate steady at 4.3%, with annual hours worked growth (2.7%) running ahead of employment growth (1.3%)

Source: ABS

Australia May flash PMIs slip into contraction, confidence at record lows

[11:19 am] Australia's private sector returned to contraction in May with new orders falling at the fastest pace since September 2021 and business confidence at joint record lows.

Composite PMI down to 47.8 in May from 50.4 in April, marking second contraction in three months

Services PMI Business Activity at 47.7 (Apr: 50.7)

Manufacturing PMI at 50.2 (Apr: 51.3)

New orders fell at fastest pace since September 2021, with panellists linking softness to Middle East war uncertainty

Employment declined for first time since end of 2024, with the rate of job shedding the joint-fastest in over five-and-a-half years

Business sentiment at joint-lowest on record, matching the start of COVID-19 in March 2020, on cost, rate hike and market concerns

Input price inflation eased but remained second-strongest since August 2022, with manufacturers bearing the brunt of energy and supply chain disruption

Top ASX 200 gainers

[10:26 am] Tuas continues to bounce after its ~62% selloff on Monday, while gold and copper miners are trading broadly higher after a strong overnight session for commodity prices.

Ticker | Company | % Chg | Price |

|---|---|---|---|

TUA | Tuas | 8.56% | $2.41 |

JHX | James Hardie | 7.44% | $28.53 |

VGN | Virgin Australia | 6.67% | $2.40 |

ELV | Elevra Lithium | 5.99% | $11.85 |

DVP | Develop Global | 5.54% | $5.52 |

GGP | Greatland Resources | 5.24% | $12.95 |

LOV | Lovisa | 5.05% | $21.94 |

RMS | Ramelius Resources | 4.40% | $3.21 |

IGO | IGO | 4.38% | $8.81 |

CSC | Capstone Copper | 4.26% | $13.21 |

Top ASX 200 losers

[10:36 am] Oil prices tumbled ~5% overnight amid optimism that the US and Iran were in the "final stages" of a deal. This is driving stocks across the energy complex (coal, refiners, O&G) broadly lower in early trade.

Ticker | Company | % Chg | Price |

|---|---|---|---|

CEN | Contact Energy | -6.10% | $7.70 |

SMR | Stanmore Resources | -4.02% | $2.51 |

PDI | Predictive Discovery | -3.03% | $0.74 |

BPT | Beach Energy | -2.41% | $1.13 |

WDS | Woodside Energy Group | -2.03% | $31.84 |

YAL | Yancoal Australia | -1.87% | $6.83 |

VEA | Viva Energy Group | -1.28% | $2.31 |

CBO | Cobram Estate Olives | -1.24% | $3.98 |

STO | Santos | -1.05% | $8.01 |

ALD | Ampol | -1.02% | $34.84 |

ASX 200 sharply higher

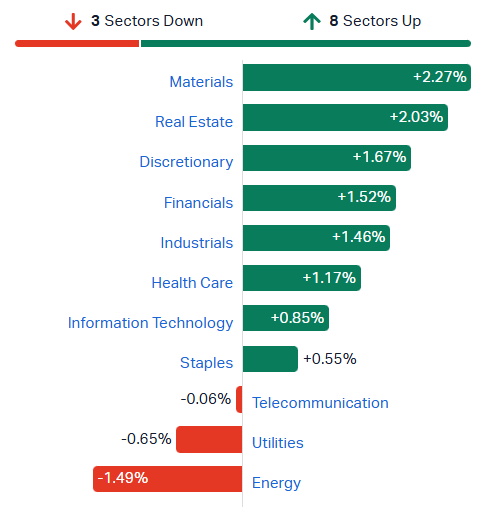

[10:23 am] ASX 200 up 1.51% in early trade, with broad participation outside of Energy and Utilities. A very strong bounce back session for Materials, yield-sensitive Real Estate stocks and Discretionary.

S&P/ASX 200 sectors (Source: Market Index)

It's been a wild ping-pong game these past few days, with the index down 1.45% on Monday, up 1.17% on Tuesday, down 1.26% on Wednesday and now we're back to breakeven for the week!

ASIC flags lifting oversight intensity as new ASX CEO takes helm

[9:55 am] Bloomberg reports that ASIC has signalled increased scrutiny of the ASX, with regulatory pressure unlikely to ease.

ASIC Commissioner Simone Constant flagged the regulator may "lift focus in intensity" on ASX's role as critical national infrastructure

Comments come as incoming CEO Attia prepares to take over from Helen Lofthouse, who departs end of May

ASX agreed to a $150m capital charge by June 2027 to reflect heightened risk profile, plus independent directors on clearing and settlement boards

Follows ASIC probe that identified gaps in risk and compliance practices with potential consequences for Australia's financial markets

ASX shares down ~16% over past 12 months, making it one of the world's worst-performing listed exchange operators

Company page: ASX (ASX)

Energy One trims FY26 ARR growth outlook on project timing

[9:52 am] Energy One has trimmed its FY26 billed ARR growth expectation to ~13% from prior 15-20%, with the shortfall flagged as timing-related rather than demand-driven.

Billed (actual) ARR growth now expected ~13% in constant currency vs prior 15-20% guidance

Shortfall primarily driven by timing of project commencements falling into FY27

Contracted (signed) ARR remains strong, with pipeline described as "extremely strong"

Underlying financial metrics (net of one-offs) expected to remain in line with consensus

Further one-off M&A-related costs likely in FY26

While it may be 'primarily' due to timing, the new ARR guidance still represents a ~26% downgrade in growth rates (compared to prior 15-20% expectations). This is not a good look for a stock that's trade at almost 60x.

Company page: Energy One (EOL)

ASIC sues Equity Trustees over First Guardian Master Fund failures

[9:51 am] ASIC has commenced civil penalty proceedings against Equity Trustees Superannuation Limited (subsidiary of ASX-listed EQT Holdings) over alleged failures in onboarding the First Guardian Master Fund.

~$65m invested in First Guardian between June 2023 and March 2024 by ~2,700 members of NQ Super & Pension

ASIC alleges Equity Trustees did not obtain critical information including constitution, audited financial accounts or compliance plan audit before onboarding

ASIC also alleges Equity Trustees allowed members to invest 100% of funds in First Guardian despite evidence it may have been illiquid

ASIC seeking compensation for member losses plus declarations and civil penalties

Second action against Equity Trustees following ongoing proceedings related to the Shield Master Fund

Fifth action against a super trustee under ASIC's 2026 enforcement priority, with $420m+ already repaid to investors and 26+ matters under investigation

Company page: EQT Holdings (EQT)

Zip settles trade mark dispute with Firstmac, retains brand

[9:47 am] Zip Co has reached a settlement with Firstmac, allowing it to continue using the Zip brand in Australia.

Zip to acquire registered trade mark No. 1021128 for ZIP under the settlement

No further liability for damages or costs in relation to Firstmac's proceedings

Settlement amount confidential but confirmed not material to the Zip Group

FY26 guidance unaffected by the settlement

Company page: Zip Co (ZIP)

AACo posts record operating profit, flags Middle East headwinds for FY27

[9:45 am] Australian Agricultural Company (AACo) delivered its strongest full-year operating profit on record, driven by an 8% lift in average beef prices and disciplined global sales execution.

Revenue up 9% to $422.1m

EBITDA of $208.9m vs $56.3m pcp

Operating profit up 23% to $71.6m, with underlying operating profit of $80.6m adjusting for North Queensland floods

Statutory NPAT of $107.3m vs $1.1m loss pcp, lifted by a $128.6m increase in fair value of the herd

NTA up 15% to $2.92/share, supported by $153.0m uplift in property values

FY27 outlook flags Middle East conflict driving up energy, transport and production costs, though global protein demand remains supportive

Company page: Australian Agricultural Company (AAC)

Arafura takes FID on Nolans Rare Earths Project

[9:40 am] Arafura has announced Final Investment Decision on its Nolans Rare Earths Project in the NT, targeting construction commencement from September 2026.

Nolans set to be Australia's first fully integrated ore-to-oxide rare earths operation, with single-site processing eliminating dependency on concentrated processing infrastructure

Export Finance Australia issued a non-binding Letter of Support for potential Critical Minerals Strategic Reserve support of up to 500tpa NdPr Oxide

EFA Letter combined with four prior binding offtake arrangements (Hyundai, Kia, Siemens Gamesa, Traxys) represents 93% of binding offtake target

Hatch engaged as EPCM contractor, with 20% of targeted nameplate capacity to remain available for spot market sales post-placement of 250tpa into Germany or Europe

What I find striking is that even though the company has signed offtake agreements with various organisations from Asia, Europe, the US and the Australian government - none have featured a floor price.

Company page: Arafura Rare Earths (ARU)

Northern Star MD Stuart Tonkin to step down in FY27

[9:37 am] Northern Star Managing Director and CEO Stuart Tonkin has flagged his intention to step down in the first quarter of FY27, concluding a 13-year tenure.

Tonkin to remain in role until Q1 FY27, aligned with conclusion of current strategic plan and commissioning of the KCGM Fimiston Mill Expansion

Under his leadership, Northern Star grew from a small-cap WA-focused miner into Australia's largest ASX-listed gold producer with three production centres and 10,000+ staff and contractors

Key transactions during tenure include Pogo (Alaska), the Saracen Minerals merger, and the De Grey Mining takeover that added the Hemi development project

Board has commenced a formal search process, with a leading global search firm to be appointed shortly to assess internal and external candidates

Mr Tonkin beneficially owns ~630,000 shares in Northern Star (~0.06% shares on issue).

Company page: Northern Star Resources (NST)

State of play for Webjet

[9:35 am] Webjet has spiraled into a rather interesting spot.

Shares down 50% year-to-date to 43.5 cents

Now trading at a ~52% discount to the offers it received from BGH (91 cents cash per share back in Nov-25) and Helloworld (90 cents cash per share in Nov-25)

Net cash of $93.9 million as at 31 March 2025 (vs. $192m market cap)

No debt and net assets of $138.4 million

There is clearly some 'value' on the table but the FY26 result and outlook commentary is far from bullish.

Webjet daily price chart (Source: TradingView)

Webjet earnings call: FY30 TTV target intact but timing under review

[9:27 am] Webjet flagged ongoing industry headwinds and several FY27 revenue pressures at its FY26 earnings call.

The stock fell 11.2% to a record low of 43.5 cents (now down 50% year-to-date) after its FY26 missed NPAT expectations by ~20%, along with poor year-to-date trading numbers and a significant reduction in Virgin commercial streams.

FY30 TTV doubling target remains in place, though timing is under review given current industry headwinds

Long-term guidance anticipates revenue margin normalising at 8-9% and EBITDA margin stabilising at or above current levels post-investment phase

Virgin Australia commission reduction to hit FY27 underlying revenue and EBITDA by ~$3m, with mitigation strategies being pursued

RBA surcharging changes from October FY27 a headwind for OTA, with ~two-thirds of TTV currently via credit cards

Leisure travel market seeing double-digit declines industry-wide, though Webjet OTA brand relaunch drove record new customer acquisition in Q4

Company page: Webjet (WJL)

Imdex CEO records first sale since 2017

[9:19 am] Imdex CEO Paul House has disclosed his first share sale since joining the company in 2017, primarily to manage personal tax obligations.

Sold 464k shares at an average price of $3.97, traded between 14-20 May 2026

Holding reduced ~20% to 1.8m shares post-transaction

Sale flagged as primarily to cover personal tax obligations, including liabilities from vesting of IMDEX incentive awards

First disposal by House since joining IMDEX in 2017

Imdex shares are up 10.4% year-to-date and up 35% in the last twelve months.

Company page: Imdex (IMD)

Brambles Chairman lifts stake by 17%

[9:16 am] Brambles Chairman John Mullen has disclosed an on-market purchase of ~14,000 shares. lifting his beneficial ownership by 17% to ~96,000 shares.

For context, Brambles has tumbled 25.7% in the last three sessions, after the company downgraded its FY26 guidance on Monday.

Sales revenue growth guidance lowered to 2-3% from 3-4% previously (at constant FX), reflecting volume shortfalls and customer mix impacts in the US where repair capacity constraints have limited ability to fully service higher than expected demand

Underlying profit growth guidance down to 3-5% from 8-11% previously (at constant FX), primarily reflecting an estimated $60m earnings impact from US repair capacity constraints expected to be resolved by end of 1H27

Tightened free cash flow outlook and announced a new $400 million buyback

Company page: Brambles (BXB)

Bond yields take a breather

[9:10 am] Lower oil prices, US-Iran peace talk progress and cooler-than-expected UK inflation were among the catalyst that pushed bond yields lower overnight.

The Aussie 10-year yield fell 8 bps to 5.01%. It's been trading in a relatively rangebound fashion since mid-March.

Australia government 10-year yield daily chart (Source: TradingView)

The US 10-year yield broke out on 12 May and has surged around 20 bps since. It fell 8 bps overnight to 4.58%.

US 10-year yield (Source: TradingView)

Copper prices bounce after five-day pullback

[9:07 am] Copper prices bounced 2.2% overnight to US$6.35/lb after a rather volatile past few weeks.

4-12 May: A massive 13.3% rally to fresh all-time highs of US$6.6/lb. The sessions on 11 May (+3.3%) and 12 May (+2.2%) set two straight days of record highs

12-19 May: Copper prices fell in four of the five sessions, down 6.5%

Copper daily price chart (Source: TradingView)

Oil prices tumble, but still elevated

[9:04 am] Brent tumbled 5.1% overnight to US$105.15 a barrel. While a sizeable decline at face value, prices remain relatively rangebound at the US$100-110 level.

Brent crude price chart (Source: TradingView)

Trump flags Iran deal in "final stages" as oil eases

[8:58 am] Trump said US-Iran talks are nearing resolution after calling off planned strikes, with tentative Hormuz tanker movements adding to downward pressure on oil.

Trump said US is in "final stages" with Iran, with planned military strikes cancelled Tuesday at the request of Gulf state leaders who assured a deal was near

Though Iran's IRGC warned of "crushing blows" extending beyond the Middle East if the US resumes military action

South Korean supertanker carrying Kuwaiti crude appears to have crossed Hormuz alongside two Chinese vessels, potentially marking one of the highest-volume days since war began late February

Tankers are reportedly using a Tehran-controlled lane, with some countries (including China) cutting direct deals with Iran for safe passage

Source: Bloomberg

Supertanker traffic through Hormuz picks up amid war

[8:57 am] A South Korean supertanker is attempting its first ever Hormuz crossing alongside two Chinese vessels, signalling tentative improvement in flows through the strategic waterway.

The Universal Winner, owned by HMM Co. and laden with Kuwaiti crude, is transiting Hormuz via a Tehran-approved route in coordination with the South Korean government

Two Chinese supertankers (Ocean Lily and Yuan Gui Yang) carrying Qatari and Iraqi crude are attempting similar crossings, though one has gone dark and the other is idling

A successful three-VLCC day would be one of the biggest for supertanker traffic through Hormuz since the Middle East war began in late February

Traffic remains well below pre-war levels, with ships facing attacks, U-turns and the need to switch off transponders mid-journey

Source: Bloomberg

Asia equity rally at risk as US yields surge

[8:56 am] Rising US bond yields are threatening Asia's AI-driven equity rally, according to Bloomberg, as historical data shows the region is highly sensitive to sharp moves in Treasury yields.

MSCI Asia Pacific Index has fallen in 16 of 19 weeks over the past five years when US 10-year yields rose 20 bp or more, losing 1.6% on average

Last week broke the recent pattern of equities shrugging off bond market moves on AI optimism, with Gavekal noting "inflation is here to stay" as the new message

Spiking yields reflect bets that war-driven oil gains will force central banks to hike, potentially choking off growth

Sets up a meaningful risk for Asia-exposed portfolios where AI enthusiasm has been the dominant tailwind

Source: Bloomberg

UK inflation eases to 2.8% in April, undershoots expectations

[8:52 am] UK headline inflation came in below market expectations in April thanks to Ofgem's energy price cap, though economists warn the reprieve will be short-lived as Middle East energy costs feed through.

Headline CPI of 2.8% in April vs 3.0% ests, down from 3.3% in March

Fall driven by lower electricity and gas prices following the government's energy bill support package, alongside smaller rises in water, sewage and road tax

Food prices (notably chocolate and meat) and package holidays also pulled inflation lower, partially offset by higher petrol, diesel, clothing and footwear

Market pricing implies a majority expect the BoE to hike 25 bp to 4% at the July meeting, though economists expect a hold at the 18 June meeting

UK unemployment ticked up to 5% in the three months to March from 4.9%, complicating the BoE's balancing act between sticky inflation and a softening labour market

April FOMC minutes lean hawkish, tightening on the table

[8:51 am] April FOMC minutes showed a clear hawkish shift, with a majority of officials open to rate hikes if inflation persists above 2% and many wanting to drop the easing bias entirely.

Most participants said "some policy firming would likely become appropriate" if inflation continues to run persistently above 2%, a notable departure from the easing bias in place earlier in the year

Three dissents emerged at the meeting over retaining easing language in the statement, with many participants preferring to remove it altogether

Vast majority flagged increased risk that inflation takes longer to return to 2% target, with Iran war, blocked Strait of Hormuz and soaring bond yields reinforcing the inflation concern

Nvidia commentary highlights

[8:49 am] Here are a few tidbits of interest from the Nvidia earnings call and results commentary.

“The buildout of AI factories - the largest infrastructure expansion in human history - is accelerating at extraordinary speed.”

"The value of Nvidia AI infrastructure is rising. The price of renting an H100 has risen 20% year to date, while A100 cloud pricing is up nearly 15% benefiting from the versatility of our platform and continuous performance enhancements enhanced by our software stack, customers are generating profitable revenue beyond the depreciable life of their GPUs."

"We should be growing faster than hyperscale capex."

"Vera CPU opens a brand new 200 billion town for Nvidia, a market we have never addressed before, and every major hyperscale and system maker is partnering with us to get it deployed."

"Vera Rubin is going to be even more successful than Grace Blackwell at this point. Every single frontier model company will jump on Vera Rubin from the get-go ... Will be supply constrained throughout the entire life of Vera Rubin.”

Nvidia Q1 smashes ests, Q2 guide well ahead

[8:45 am] Nvidia delivered another blowout quarter with revenue up 85% and Data Center up 92%, while Q2 guidance came in materially ahead of consensus even excluding any China compute revenue.

Revenue up 85% to $81.6bn vs $79.0bn ests (3% beat)

Adjusted EPS up 140% to $1.87 vs $1.77 ests (6% beat)

Data Centre revenue up 92% to $75.2bn vs $73bn ests (3% beat)

Adjusted gross margin of 75.0% vs 74.5% ests (50 bp beat)

Q2 revenue guided to ~$91.0bn vs $87.2bn ests (4% beat), assuming no Data Centre compute revenue from China

$80bn additional buyback authorisation approved and quarterly dividend lifted from $0.01 to $0.25 per share, with ~$20bn returned in Q1

The result was announced after market close, with Nvidia shares down 1.0% in after hours.

Lowe's Q1 beats, reaffirms FY guidance as DIY market stays soft

[8:43 am] Lowe's delivered a top and bottom-line beat with four consecutive quarters of positive comps, though management flagged the toughest housing market since the financial crisis.

Revenue up 10% to $23.08bn vs $22.88bn ests (1% beat)

Adjusted EPS of $3.03 vs $2.97 ests (2% beat)

Comparable sales up 0.6%, supported by spring execution and online sales growth of 15.5%

FY26 sales guided to $92bn-$94bn (up 7-9%) vs $93.07bn ests (in line), with comps flat to up 2%

FY26 adjusted EPS guided to $12.25-$12.75 vs $12.59 ests (in line)

CEO flagged K-shaped consumer dynamic with higher-income spending up and lower-income pulling back, sees sustained sub-6% rates as key to unlocking DIY demand

Lowe shares dipped as much as 4.7% overnight but managed to finish the session up 1.2%.

Target Q1 beats, lifts FY guidance but shares fall ~4%

[8:41 am] NYSE-listed Target delivered its first positive comparable sales in five quarters and raised full-year guidance, though shares slid as investors questioned whether momentum can hold through the year.

Revenue up 6% to $25.44bn vs $24.66bn ests (3% beat)

EPS of $1.71 vs $1.46 ests (17% beat)

Comparable sales up 5.6%, first positive print in five quarters, with traffic up 4.4% and digital comps up 8.9%

Gross margin of 29% vs 28.7% ests

FY26 net sales growth guided to 4% (up 2ppt from prior), with EPS now seen near high end of $7.50-$8.50 range vs $8.14 ests

CapEx lifted by over $1bn to ~$5bn for the year, with CEO flagging more merchandising change in 2026 "than we've seen in a decade"

US equities higher, momentum and AI lead

[8:38 am] US stocks closed near session highs overnight as momentum trades resumed leadership, Treasury yields fell, and oil dropped sharply on US-Iran negotiation chatter.

Momentum and AI-linked names led after recent underperformance, with semis, banks, banks, airlines, homebuilders and precious metals among outperforming

Yields down 7-10 bps across the curve, though the market now pricing ~14 bp of Fed cuts through year-end, down from 19 bp overnight

Brent tumbled 5.1% to US$105 a barrel on chatter around potential US-Iran negotiations, though headline noise remains elevated with nothing concrete confirmed

April FOMC minutes leaned hawkish as expected, showing broader support for patience and majority view that some policy firming may be needed if inflation persists, though many still see cuts as likely appropriate if conflict resolves

Bullish narrative supported by AI demand commentary, impending OpenAI IPO, reasonable valuations and resilient consumer

Bearish risks include stretched positioning, rate/equity disconnect and rising global rate backdrop

Good morning!

[8:28 am] ASX 200 futures are up 104 pts (+1.21%).

The overnight session in a nutshell:

Major US benchmarks higher, with the S&P 500 up 1.1%, Nasdaq up 1.5% and Dow reclaiming 50,000 as oil and yields slid on Iran peace hopes

Trump said US-Iran negotiations are in the "final stages", sending Brent ~5% lower and snapping the bond rout, with US 30-year yields easing from a 19-year high

Nvidia beat with $81.6bn Q1 FY27 revenue (up 85% year-on-year), guided Q2 to $91bn vs $86bn consensus, raised dividend and added $80bn buyback, shares fell ~1.5% after-hours