ASX 200 Live Today - Thursday, 18th December

The S&P/ASX 200 is set to open flat despite broad-based weakness overnight. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Thursday, December 18th. Expect a high volume of posts pre-market and more periodic updates throughout the day. It'll wrap up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

ASX 200 to slip for a fourth straight session

[2:00 pm] ASX 200 currently down 0.15% and on track to fall for a fourth straight session. There's been a small bounce off intraday lows of -0.38% but still a relatively discouraging session, with the market closing below the 200-day moving average.

No major change in market narratives. It still feels heavy and selective out there. Hard to deny the recent bearishness amid hawkish RBA rate repricing, continued AI/tech weakness and elevated positioning (BofA survey noted fund managers at the most bullish level in more than three years). On the plus side, volatility remains somewhat low and we're heading into the seasonally most bullish part of the year.

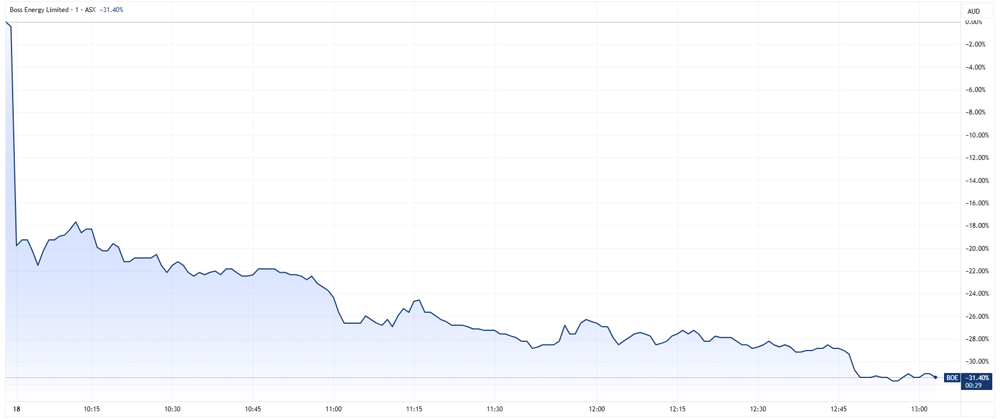

Boss Energy oblierated

[1:00 pm] Boss Energy opened 19% lower this morning but now it's down 30.9% to a mere dollar.

This price action stresses how no one is buying the dip against a backdrop of higher costs for FY27 and the unknowns associated with the new economic study for its Honeymoon Project.

Boss Energy intraday chart (Source: TradingView)

Tech stocks start to bounce

[12:20 pm] S&P/ASX 200 Tech Index currently down 0.94%, rallying off intraday lows of -2.7%. Most names are off session lows, with a handful starting to tick into positive territory.

All things considered, a very weak bounce given how badly these stocks have sold off in recent weeks.

Ticker | Company | % Chg | Price |

|---|---|---|---|

WBT | Weebit Nano | -6.24% | $3.91 |

AD8 | Audinate Group | -5.63% | $4.28 |

CAT | Catapult Sports | -3.30% | $4.10 |

NXT | NextDC | -3.11% | $12.31 |

MP1 | Megaport | -2.11% | $12.09 |

360 | Life360 | -1.95% | $31.74 |

NXL | Nuix | -1.54% | $1.79 |

TNE | Technology One | -0.31% | $27.23 |

XRO | Xero | -0.06% | $110.20 |

IRE | Iress | -0.06% | $8.56 |

DDR | Dicker Data | 0.15% | $10.03 |

DTL | Data#3 | 0.33% | $9.04 |

WTC | Wisetech Global | 0.66% | $67.44 |

SDR | Siteminder | 0.95% | $5.82 |

PPS | Praemium | 2.24% | $0.78 |

Analysts' take on Graincorp

[12:17 pm] Graincorp suffered a 15.3% selloff on Wednesday after flagging FY26 receival volumes of 11-12Mt vs. market expectations of just over 12Mt. Analysts viewed this as inconsistent with prior ABARES forecasts.

RBC Capital Markets lowered target to $9.50 from $10.75, maintains outperform. Expects FY26 margins under pressure, receival guidance below consensus, and sees GCC exit loss as final clean-up.

Macquarie lowered target to $8.30 from $8.80, maintains outperform. Highlights global oversupply risk, on-farm storage limiting throughput, and sees GCC sale removing an earnings drag.

Bell Potter lowered target to $7.60 from $8.50, maintains hold. Early FY26 receival trends weak, southern competition diluting share, and GCC sale not valuation accretive.

Top ASX 200 gainers and losers

[11:03 am] A handful of gold miners, REITs and healthcare stocks are trading modestly higher. Meanwhile, lithium, uranium and tech stocks are posting sizeable declines in early trade.

Ticker | Company | % Chg | Price |

|---|---|---|---|

OBM | Ora Banda Mining | 2.86% | $1.44 |

EBO | Ebos Group | 2.70% | $23.95 |

RYM | Ryman Healthcare | 2.38% | $2.58 |

APA | Apa Group | 2.30% | $9.35 |

LNW | Light & Wonder | 1.95% | $147.77 |

RSG | Resolute Mining | 1.89% | $1.19 |

SDF | Steadfast Group | 1.87% | $5.17 |

CQR | Charter Hall Retail Reit | 1.86% | $4.11 |

MGR | Mirvac Group | 1.71% | $2.09 |

DXS | Dexus | 1.63% | $7.19 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

CDA | Codan | -5.74% | $27.43 |

PDN | Paladin Energy | -5.55% | $8.26 |

TWE | Treasury Wine Estates | -5.42% | $4.71 |

LTR | Liontown | -4.49% | $1.45 |

NXG | Nexgen Energy | -4.47% | $12.40 |

NXT | NextDC | -4.37% | $12.15 |

RRL | Regis Resources | -4.16% | $7.38 |

NEU | Neuren Pharmaceuticals | -3.84% | $19.14 |

NWH | NRW Holdings | -3.65% | $4.89 |

360 | Life360 | -3.40% | $31.27 |

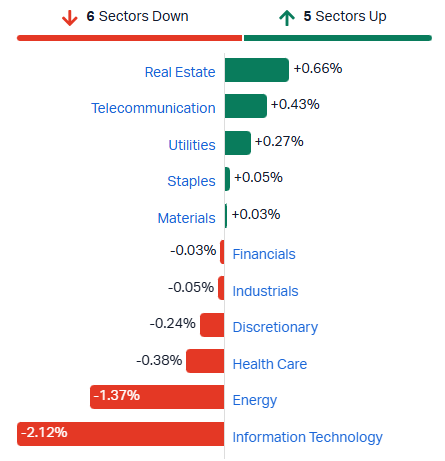

ASX 200 edges lower, tech obliteration continues

[10:21 am] ASX 200 down 0.16% in early trade, with relatively flattish opens for heavyweight sectors like banks and miners.

Tech sector down for an eighth straight session and trading at Liberation Day lows. Notable decliners include NextDC (-4.5%), Life360 (-3.6%), Megaport (-2.5%) and Technology One (-2.0%).

Food for thought: What's the difference between a stock trading at 200x from one at 100x? A deeper pool of willing buyers and committed holders. But when these buyers and holders begin to fade and pivot elsewhere, the result is a painful unwind.

ASX 200 sectors (Source: Market Index)

Taking a closer look at Boss Energy

[10:15 am] Boss Energy has nosedived 20% in early trade after releasing the outcomes of its Honeymoon project review. The key highlights include:

The review has "indicated an expected material and significant deviation from the assumptions underpinning the company's 2021 Enhanced Feasibility Study"

"This in turn would be expected to impact life of mine production and cost from FY27 onwards primarily due to less continuity of higher-grade mineralisation, mineralisation not overlapping, less leachability and smaller wellfields."

In layman's terms: we rushed the initial study and now the project's economics are way worse, with higher costs.

Boss reaffirmed its FY26 production and cost guidance, but now expects FY27 production to be similar to FY26 but AISC would be ~15% higher year-on-year.

To add some perspective, Macquarie (Oct-25) was expecting production to grow 12.5% year-on-year to 1.8Mlb in FY26, with AISC to fall 5% to US$35.86/lb.

Taking a more medium-term view, withdrawing your EFS guidance is not a good look (imagine explaining to financiers that your project economics assumptions are no longer valid). This withdrawal creates substantial overhang, as new economic assumptions could vary dramatically from the original projections.

Boss Energy starts new Honeymoon study, FY26 guidance unchanged

[9:59 am] Boss Energy is set to tumble this morning after withdrawing its 2021 Enhanced Feasibility Study.

A review indicated material deviations from the 2021 study, with the company launching a New Feasibility Study exploring a wide-spaced wellfield design.

The concept-stage design could lower costs and improve grades, with initial updates expected in the first quarter of 2026 and completion by the 3Q26.

Will take a look at the FY26-27 guidance in a moment.

Company page: Boss Energy (BOE)

Woodside CEO Meg O'Neill to lead BP

[9:53 am] Woodside Energy CEO Meg O’Neill will resign to become BP’s CEO, effective 1 April 2026.

Liz Westcott, Woodside’s EVP and COO Australia, has been appointed acting CEO from 18 December.

At BP, Carol Howle will serve as interim CEO until O’Neill joins, while outgoing CEO Murray Auchincloss will remain as an advisor until December 2026.

Company page: Woodside Energy Group (WDS)

Gemlife expands Townsville development pipeline

[9:51 am] GemLife Communities is acquiring a 32.5ha greenfield site in Townsville for $21 million, aiming to develop over 500 manufactured home sites and associated facilities.

Increases GemLife’s portfolio to 33 communities with an expected 10,413 homes on completion.

The site consists of two lots, each valued at $10.5m, settling in March 2026 and February 2027.

Purchase will be funded through cash and existing debt, consistent with the group’s disciplined capital management approach.

Gemlife made its ASX debut on 3 July after raisin $750 million at $4.16 per share. The chart looks very clean (low vol, shallow pullbacks) and currently trying to break out to all-time highs.

Company page: GemLife Communities (GLF)

Bendigo Bank faces regulatory risk capital and oversight

[9:44 am] APRA and AUSTRAC are imposing measures on Bendigo Bank following an independent review that highlighted weaknesses in money laundering controls, non-financial risk management, and risk culture.

APRA requires a further $50m risk capital add-on and a root cause analysis to assess broader non-financial risk management issues.

AUSTRAC has launched an enforcement investigation into the bank’s compliance with the AML/CTF Act.

Measures follow Deloitte’s review of suspected money laundering at a Bendigo Bank branch reported to AUSTRAC.

BEN has wound up as one of the worst performing banks, with the stock down 18% year-to-date. Most of the decline has occurred in recent weeks following a weaker-than-expected quarterly result on 11 November and ongoing AML/CTF compliance issues.

Company page: Bendigo & Adelaide Bank (BEN)

Bapcor CEO resigns

[9:30 am] Bapcor CEO Angus McKay has resigned, with Chris Wilesmith appointed as his replacement starting 14 January.

Wilesmith was the former CEO and MD of Jaycar Electronics, and CEO of Mitre 10 New Zealand.

Interestingly, McKay announced his plans to step down from the Board but continue his role as CEO just two months ago (24-Nov).

The resignation is taking place as the stock is down 61% year-to-date and trading at levels not seen since 2015.

Company page: Bapcor (BAP)

APA exits minor gas distribution stake

[9:27 am] APA is divesting a non-core equity interest, simplifying its portfolio with minimal earnings impact.

APA will sell its 20% stake in GDI to Stonepeak affiliates as part of a transaction that transfers 100% ownership of GDI to Stonepeak.

GDI owns the Allgas gas distribution network, covering South East Queensland and Northern New South Wales.

The divested assets contributed less than 1% of APA’s FY25 underlying EBITDA, indicating immaterial earnings exposure.

APA expects to generate $64 million from the sale. It's not overly material vs. the company's debt position of $12.6 billion in FY25.

Company page: APA Group (APA)

Reminder: It's options expiry day

[9:25 am] Pre-market prices are a bit volatile today due to options expiry (e.g. CBA’s indicative open is down 5%). Prices usually stabilise after the open because the auction clears expiry-related imbalances in a single print, options settle, and dealer hedging pressure eases.

First Guardian claims to hit Netwealth earnings

[9:17 am] Netwealth flagged a material one-off earnings impact from compensation claims, while maintaining underlying growth and dividend settings.

First Guardian compensation is expected to reduce 1H26 NPAT by around $71m and will be treated as an extraordinary item.

Funded through a mix of cash and debt, limiting near-term balance sheet strain but lifting leverage temporarily.

FY26 dividends will be based on underlying earnings (ex-one off)

Netwealth reaffirmed previous FY26 guidance, with FUA net flows expected to be broadly in line with FY25 and related compliance costs not material.

Netwealth will hold an investor call today at 9:00 am.

Company page: Netwealth Group (NWL)

Gold and silver prices continue to trend higher

[9:11 am] Another strong overnight session for the two safe havens.

Gold up 0.82% to US$4,337/oz

Silver up 3.89% to US$66.20/oz

Gold is now trading within 1.0% of its 17 October record of US$4,381, with prices up six of the last seven trading sessions.

Silver's price action has been a little volatile in recent days, as prices have now doubled since late May. Though the overnight session was a relatively clean upside move to yet another fresh all-time high.

The challenge here is that the broader market remains relatively weak and the risk-off vibe may weigh on miner upside.

The VanEck Gold Miners ETF finished 1.18% higher overnight, while the Global X Silver Miners ETF rose 0.99%. Both ETFs closed within 2% of recent all-time highs.

Treasury Wine could become a buyout candidate

[9:04 am] An article by The Australian says Treasury Wine could become a private equity target as its share price falls to multi-year lows.

The article notes that the company was approached by KKR back in 2014, with TWE rejecting a bid of $5.20 per share.

TWE shares dipped 9.2% on Wednesday after issuing a 1H26 EBIT guidance of $225-235 million, which was 31-32% below consensus expectations. The trading update also flagged elevated customer inventories in China and the US, as well as expectations of leverage soaring to 2.5x in the first half of FY26 vs. the target range of 1.5-2.0x.

Source: The Australian

Oracle CDS surge to 2009 highs

[8:59 am] Credit default swap spreads on Oracle's debt have surged to 150 bps from just ~40 bps in August. Lenders are becoming increasingly nervous about whether the company can meet its debt obligations.

Oracle's debut has soared to $108 billion, with recently issued investment-grade notes trading more like junk bonds.

The CDS spike suggests the market is now pricing in the likelihood of default at greater than 12%.

AI capex scrutiny collides with renewed optimism

[8:57 am] Concerns around hyperscaler balance sheets persist, but investor anxiety appears to be easing as long-term AI upside remains central to equity bull cases.

Oracle’s proposed US$10bn Michigan data centre is in limbo after a financing deal with Blue Owl collapsed, reflecting lender concerns over AI infrastructure strategy, rising debt and tighter leasing and funding terms.

The setback adds to pressure on Oracle, following scrutiny over data centre delays and profit risks from AI investment, with its CDS now at the highest level since the GFC.

Amazon is reportedly in talks to invest US$10bn in OpenAI, potentially lifting its valuation above US$500bn, on top of a prior commitment by OpenAI to spend US$38bn on Amazon servers over seven years.

Yesterday's BofA’s Global Fund Manager Survey shows AI hyperscaler capex remains a key credit risk, cited by 29% of investors, but concern over excessive capex has eased to 14% from 20% in November.

Citi sees AI upside as a major pillar of its 2026 S&P 500 target of 7,770, though expects returns to increasingly diverge between perceived AI winners and losers.

Waller leans dovish as Fed chair odds rise

[8:54 am] Fed Governor Waller signalled comfort with further rate cuts, framing policy as clearly restrictive even as growth holds up.

Waller said rates are 50 to 100 bps above neutral, with inflation likely to move closer to the 2% target in the first half of 2026.

His policy focus remains on continued labour market softening, though he stressed the pace does not warrant aggressive or abrupt easing, supporting a gradual path. He argued that solid economic growth and potentially stimulative factors next year are not a justification for keeping rates elevated.

Remarks came across as slightly more dovish than markets expected, with prediction markets lifting Waller to second favourite for Fed chair at around 26%, behind Hassett and ahead of Warsh.

Oil bounces off multi-year lows

[8:52 am] Brent staged a 3.0% bounce overnight, now back above US$60 a barrel as fresh geopolitical risks surfaced, though structural oversupply concerns continue to cap the medium-term outlook.

Brent rebounded sharply after its lowest close since early 2021, driven by renewed geopolitical headlines rather than demand fundamentals.

Trump’s proposed blockade of sanctioned Venezuelan tankers would likely cripple Venezuela’s exports, but global impact is limited as the country accounts for less than 1% of world oil supply.

The US is also flagging potential new sanctions on Russia’s energy sector if peace talks on Ukraine fail, undermining recent optimism that had pressured oil prices.

Oil remains on track to finish the year down 25%, reflecting persistent concerns around a 2026 supply glut.

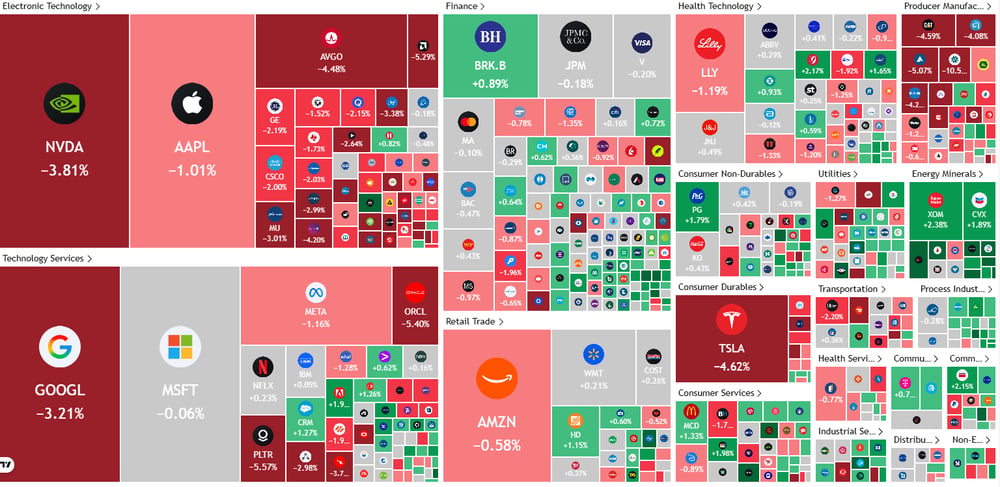

Tech stocks tumble as AI hype fizzles

[8:48 am] Very heavy overnight session for tech and AI-related stocks. Key names like Nvidia, Alphabet, Tesla, Palantir and Broadcom all down more than 3%.

S&P 500 heatmap (Source: TradingView)

Good morning!

[8:31 am] ASX 200 futures are up 7pts (+0.08%) as of 8:30 am AEDT.

The overnight session in a nutshell:

Major US benchmarks broadly lower and finished at worst levels

S&P 500 and Russell 2000 down for a fourth straight session, Nasdaq gave back yesterday's small bounce and now down 3.8% in the last four sessions

Overall, US market feels rather heavy, with very selective upside and continued weakness among AI and tech-related sectors

Strong session for commodities, with silver (+4.0%) and gold (+0.9%) continuing to trend higher, copper (+1.2%) back within 2% of recent all-time highs, oil bouncing off multi-year lows and more

What happened overnight? Catch up quick via today's Morning Wrap.