ASX 200 Live Today - Monday, 19th January

The S&P/ASX 200 is set to open flat after major US benchmarks finished little changed on Friday. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Monday, January 19. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Be sure to refresh manually for the latest updates — and let us know how we can make it even better.

ASX 200 lower as breadth weakens

[2:05 pm] Fairly heavy session, with most sectors and stocks trending lower towards intraday lows. ASX 200 currently down 0.44% despite a flattish start, on track to close near intraday lows and snap a five day win streak.

Tech sector now trading smack bank on 7-Apr-25 lows, very oversold but no bounce in sight. Life360 (-7.3%) obliterated today, Qoria (-5.7%) now down 27% in the last eight sessions, Xero (-4.0%) trading in a straight line down since Jun-25 and now at the lowest since Nov-23, and so forth. Despite how much they've fallen, most are still trading at fairly frothy valuations (e.g. TNE still at 65x vs. earnings growth rates of ~20%).

Materials Index briefly dipped as much as 0.4% after China's data dump. Though its now recovered to a 0.22% gain. Most other sectors have been trending lower today, though not a terrible outcome considering last week's win streak. That's all for today, thanks for tuning in and I'll catch you all tomorrow.

Uranium stocks trend higher

[1:55 pm] Another very strong session for uranium equities, off the back of stronger spot pricing.

A bellwether name like Paladin Energy opened 2.2% higher, now up 6.8% to the highest since October 2024. The stock is now up 23.3% year-to-date.

Ticker | Company | % Chg | Price |

|---|---|---|---|

BOE | Boss Energy | 12.47% | $1.78 |

LOT | Lotus Resources | 9.76% | $0.23 |

BMN | Bannerman Energy | 8.09% | $4.08 |

T92 | Terra Critical Minerals | 7.14% | $0.06 |

PDN | Paladin Energy | 6.80% | $11.87 |

EL8 | Elevate Uranium | 5.71% | $0.37 |

PEN | Peninsula Energy | 3.47% | $0.90 |

DYL | Deep Yellow | 3.02% | $2.22 |

AGE | Alligator Energy | 2.70% | $0.04 |

AEE | Aura Energy | 2.63% | $0.20 |

NXG | Nexgen Energy | 1.21% | $17.57 |

A2 Milk abruptly dips 10pc

[1:47 pm] A2 Milk was trading around breakeven, now down 10.9% ($8.39). The catalyst remains unclear, but the selloff occurred right as the Chinese economic data was released at 1:00 pm AEDT. This may coincide with the relatively soft economic data and birth/population trends, including:

Lowest birth rate since 1949, at just 5.6 births per 1,000 people

Population fell by 3.4 million last year, the largest drop in decades

Age group 16-59 shrank, account for 60.6% of the total population vs. 60.9% a year ago

Those age either 60 or above made up 23% of the total population vs. 22% a year ago

China growth meets deep structural headwinds

[1:43 pm] Fresh data highlight a widening gap between headline GDP growth and underlying economic momentum, with demographics, deflation and investment weakness weighing on the outlook.

Births fell to a record low of 5.6 per 1,000 people, with just 7.9 million babies born, underscoring a worsening demographic drag despite government incentives.

Deflationary pressures persist, with economy-wide prices falling for an 11th straight quarter, the longest streak since the mid-1990s, even as nominal GDP growth lags real growth.

Fixed-asset investment contracted 3.8% in 2025, the first annual decline in nearly three decades, driven by a 17.2% collapse in property investment and tighter controls on local government debt.

Infrastructure investment fell 2.2% and manufacturing investment growth slowed sharply, reflecting policy caution around inefficient spending and capacity expansion.

Activity data remain mixed, with 2025 GDP growth meeting the 5% target, industrial output slightly beating expectations, but retail sales undershooting and steel output falling to its lowest level since 2018.

Australian inflation gauge picks up in December

[12:13 pm] Australia’s Monthly Inflation Gauge, compiled by the Melbourne Institute, jumped 1.0% month-on-month in December, the fastest monthly rise since 2023.

This is despite the RBA holding the cash rate at 3.6% at its December meeting. The latest official headline CPI print for November was 3.4% year-on-year, above the 2–3% target, with trimmed mean at 3.2%.

Gold surges to another all-time high

[12:08 pm] Gold continues its formidable rally, up 1.72% to US$4,674/oz. Prices are now up 3.0% and up 72% in the last twelve months.

The All Ords Gold Index is up 2.7% today, also trading at fresh all-time highs.

Ticker | Company | % Chg | Price |

|---|---|---|---|

MEK | Meeka Metals | 6.54% | $0.28 |

CYL | Catalyst Metals | 6.22% | $9.56 |

BC8 | Black Cat Syndicate | 4.91% | $1.54 |

SBM | St. Barbara | 4.86% | $0.58 |

BGL | Bellevue Gold | 4.63% | $1.70 |

GMD | Genesis Minerals | 4.32% | $7.62 |

WGX | Westgold Resources | 4.06% | $6.92 |

RSG | Resolute Mining | 4.05% | $1.34 |

CMM | Capricorn Metals | 3.76% | $15.32 |

PRU | Perseus Mining | 3.43% | $6.03 |

OBM | Ora Banda Mining | 3.40% | $1.68 |

NST | Northern Star Resources | 3.30% | $27.72 |

EVN | Evolution Mining | 2.32% | $13.43 |

PNR | Pantoro Gold | 2.01% | $5.33 |

RMS | Ramelius Resources | 1.87% | $4.63 |

RRL | Regis Resources | 1.29% | $7.84 |

NEM | Newmont | 1.27% | $171.40 |

VAU | Vault Minerals | 1.27% | $5.99 |

ALK | Alkane Resources | 0.97% | $1.56 |

EMR | Emerald Resources | 0.73% | $6.89 |

Top ASX 200 gainers and losers

[11:30 am] Uranium and gold stocks are trading broadly higher, while major tech and lithium names are down 3-6%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

PDN | Paladin Energy | 6.35% | $11.82 |

SLX | Silex Systems | 6.00% | $6.89 |

GYG | Guzman Y Gomez | 4.70% | $22.74 |

CYL | Catalyst Metals | 4.33% | $9.39 |

WGX | Westgold Resources | 4.21% | $6.93 |

BGL | Bellevue Gold | 4.14% | $1.69 |

L1G | L1 Group | 3.67% | $1.13 |

CMM | Capricorn Metals | 3.52% | $15.28 |

RSG | Resolute Mining | 3.50% | $1.33 |

PRU | Perseus Mining | 3.43% | $6.03 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

360 | Life360, Inc | -6.09% | $27.45 |

AAI | Alcoa Corporation | -6.03% | $89.53 |

LTR | Liontown | -5.58% | $2.03 |

CIA | Champion Iron | -4.98% | $6.29 |

RWC | Reliance Worldwide | -4.20% | $3.88 |

4DX | 4DMedical | -4.13% | $4.87 |

ILU | Iluka Resources | -3.49% | $6.79 |

JHX | James Hardie | -3.39% | $34.49 |

PLS | PLS Group | -3.31% | $4.53 |

PME | Pro Medicus | -3.00% | $196.81 |

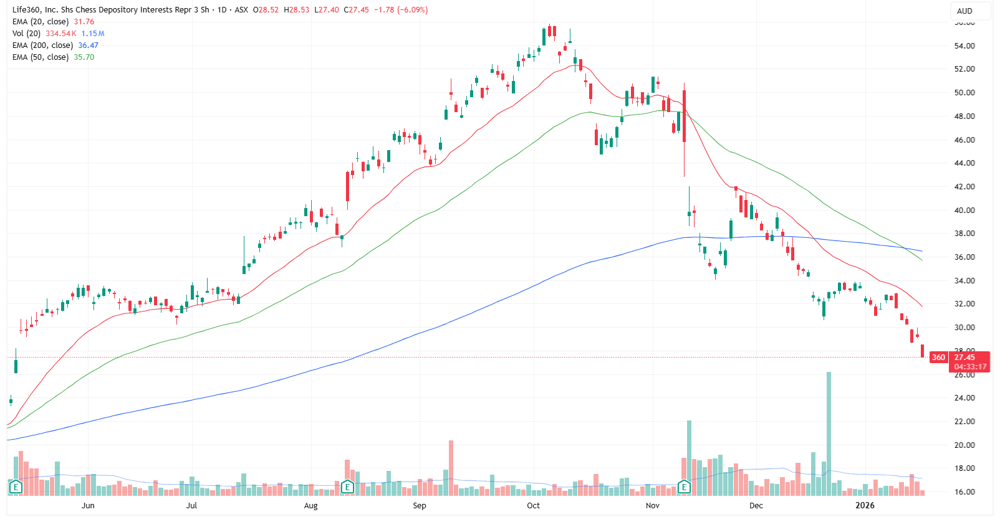

Life360 nears one-year low

[11:29 am] Just when you thought a beaten-up tech name like Life360 couldn't get any more oversold – it's down another 6% in early trade.

The stock has now halved since October and trading back at May-25 levels. Despite the selloff, the stock is still trading at a trailing price-to-earnings of ~150x.

Life360 daily price chart (Source: TradingView)

American Rare Earths sells non-core stake to fund Halleck Creek

[11:12 am] American Rare Earths says it has sold its entire shareholding in Godolphin Resources as part of a non-core asset review.

Shares sold 84,922,311 GRL shares

Average buy price 2.12c vs average sale price 3.4c

Gross proceeds $2.89m and gross profit $1.10m

Fees and brokerage $29,117

ARR said the cash will go toward Halleck Creek development activities, working capital and maintaining balance sheet strength, with chairman Richard Hudson saying the deal “enhances financial flexibility” while keeping Halleck Creek the “clear strategic priority.”

ARR has a market cap of $246 million, with $21.2 million cash as at 30 September 2025.

Company page: American Rare Earths (ARR) | By Warren Masilamony

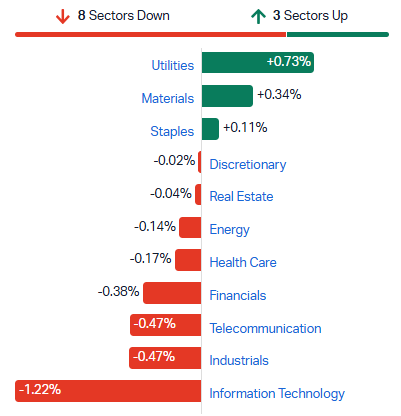

ASX 200 slips as tech stocks tumble

[10:27 am] Fairly flat open, ASX 200 currently down just 0.05% following a five-day win streak last week. Sector performance is relatively tame, with notable moves from:

Materials sector continues to grind higher, currently up 0.34% to record levels

Tech index down 1.2%, not far from recent lows (~0.3% away from 6-Jan-26 low)

Notable tech decliners include Life360 (-5.0%), Bravura (-1.8%), Wisetech (-1.6%), Technology One (-1.4%) and Xero (-1.1%)

S&P/ASX 200 sectors (Source: Market Index)

Nickel Industries sees strong start to 2026 despite December setback

[9:57 am] Nickel Industries expects December 2025 quarter Adjusted EBITDA of US$35m-US$40m, impacted by delayed RKAB approval at Hengjaya Mine which cut ore sales to 945,631 wmt. Operations resumed in December and 2026 has started strongly with 735,000 wmt sold by 17 January.

Company page: Nickel Industries (NIC)

NRW wins $750m Meandu Mine contract

[9:55 am] NRW Holdings’ subsidiary Golding Contractors has secured a 5.5-year Mining Services Agreement at Stanwell Meandu Mine, covering full mine operations and employing around 400 local staff. The capital-light contract supports NRW’s strategy of low-capital intensity while leveraging Golding’s reputation for safe and efficient mining services.

Company page: NRW Holdings (NWH)

Resources riding a strong, broad-based upswing

[9:43 am] The ASX resources sector has surged since July, with multiple commodities driving a sustained rotation that may be more durable than many investors expect, according to Morgan Stanley.

Resources have outperformed the broader market by more than 30 percentage points since early July, marking the strongest relative gain since 2009.

The rally has been commodity-specific and gradual, led by gold, copper, bulks, lithium, and uranium, each with distinct drivers and market pushback.

Supply dynamics are supportive while demand indicators are positive, creating momentum in both price and earnings for the sector.

Potential upside remains if spot commodity prices translate into longer-term averages, with M&A activity providing an additional catalyst for valuations.

Historical periods of similar outperformance suggest the rotation could be sustained, encouraging a sector-level investment approach.

Polynovo preliminary 1H26 results

[9:38 am] "We are pleased to see strong growth across key markets, supported by a broader adoption across multiple indications, new products, and expanded geographies—giving us confidence in continued momentum through 2026," says CEO Bruce Peatey.

The key numbers from this morning's indicative 1H26 result include:

Group sales up 26% to $68.2m

U.S. sales up 25% to $51.7m

NovoSorb MTX sales up 195% to $6.2m

Rest of World sales up 28% to $16.5m

BARDA revenue down 62.5% to $2.0m

Total group revenue including BARDA up 17.6% to $70.4m vs. Macquarie ests of $72.9m (3.4% miss)

Company page: Polynovo (PNV)

Gold miners set for growth despite Q2 cash tax pressures

[9:21 am] RBC Capital Markets analyst Alex Barkley says strong gold prices (+13% in Q2 FY26) have boosted equities by ~25%, with miners well-positioned for near-term production growth and balance sheets remaining in net cash. His key takeaways for the upcoming quarterly reporting season include:

Q2 production expected to track guidance after a maintenance-heavy Q1, though cash tax outflows will impact NST, EVN, RMS, and WGX as loss credits expire, according to RBC Capital Markets

High earnings growth is led by WGX, BGL, VAU, and RRL, with latent in-ground gold value unlocking potential project opportunities.

Companies with growth-focused strategies are favoured over operational/valuation safety as overall balance sheets remain strong enough to self-fund expansion.

Rising gold prices and capex demands may increase competition for mining services, though owner-operator models offer relative insulation.

Australia’s land lease sector set for consolidation

[9:19 am] GemLife CEO Adrian Puljich told the AFR that over the next decade, mergers in the seniors housing sector are likely to leave just three large listed operators, amid strong multi-generational demand.

Consolidation is underway, with major players like Stockland, Mirvac, Ingenia and GemLife expanding portfolios and attracting institutional capital.

Land lease communities offer downsizers a home without owning the land, benefiting from low market penetration and strong demand in Queensland and WA.

GemLife recently listed at a $1.58 billion valuation, has acquired its 33rd site in Townsville and aims to become an ASX 300 company while pursuing aggressive growth.

Source: AFR

Macmahon subsidiary wins Rio Tinto Pilbara contract

[9:16 am] Macmahon subsidiary Decmil has secured a $120 million contract from Rio Tinto to build a heavy haulage road, light vehicle access roads and associated drainage works at Western Hill in the Pilbara. Work starts in January 2026 and is expected to finish in 2027, with FY26 guidance unchanged under a new earthworks framework with Rio Tinto. Macmahon shares have rallied 116% in the past twelve months.

Company page: Macmahon (MAH)

JPMorgan resource ratings roundup

[9:15 am] JPMorgan has released a broad set of resource updates this morning. At a glance, most appear driven by changes to commodity price assumptions and are unlikely to have a significant impact on today’s price action.

BHP Group retained Overweight; target up to $56.50 from $48.00

Boss Energy upgraded to Overweight from Underweight; target up to $2.05 from $1.85

Deterra Royalties upgraded to Overweight from Equal-weight; target up to $4.75 from $4.40

Fortescue downgraded to Underweight from Overweight; target down to $19.75 from $21.20

IGO Limited retained Underweight; target up to $8.40 from $4.50

Iluka Resources retained Overweight; target down to $7.30 from $8.60

Lynas Rare Earths upgraded to Overweight from Equal-weight; target down to $17.55 from $19.45

Paladin Energy retained Overweight; target up to $12.05 from $10.40

PLS Group retained Overweight; target up to $5.25 from $2.85

Rio Tinto retained Equal-weight; target up to $138.00 from $129.50

Sandfire Resources retained Underweight; target up to $16.15 from $11.45

South32 retained Overweight; target up to $4.70 from $3.45

Whitehaven Coal downgraded to Equal-weight from Overweight; target up to $8.75 from $8.00

Macquarie seeks GIC support for $11.6bn Qube takeover

[9:09 am] Macquarie Asset Management is looking for a co-investor as several large infrastructure funds decline to join its high-priced bid for logistics giant Qube, according to the AFR.

Singapore’s GIC is in talks to take a stake in Qube, but no commitment has been made yet.

Major potential partners, including Australian Retirement Trust, Aware Super, PSP Investments and IFM Investor, have declined, citing deal complexity, exit risks and return expectations.

UniSuper has been increasing its stake in Qube, now holding 15.1%, and could play a key role if external co-investors remain scarce.

MAM’s $5.20 per share bid represents a 27.8% premium and 14.4x 2025 EBITDA, with shareholders largely supportive of the offer.

The deal is the largest announced in Australia for 2025, and Macquarie has until February 1 to finalise due diligence and firm up the scheme bid.

Source: AFR

China to end 2025 on weak note

[9:01 am] China's reporting Q4 GDP growth along with industrial production, retail sales and fixed asset investment around noon, with the economic growth likely falling to a three-year low, reflecting weak consumption and investment.

Q4 GDP forecast to grow 4.5% year-on-year, the slowest since post-Covid reopening, while full-year growth is projected to hit 5%, meeting Beijing’s official target.

Domestic demand remained weak, with retail sales and fixed-asset investment slowing sharply and property investment declining 16.5% in 2025.

Industrial output and exports provided support, with output growth accelerating to near September levels, highlighting China’s lopsided reliance on external demand.

Policy stimulus is expected to remain modest, focused on targeted lending and efficiency measures, as authorities avoid large-scale monetary easing or fiscal expansion.

Structural challenges including a weak job market, falling home prices, local government debt and legacy industries mean China’s shift toward consumption and services will be gradual, likely taking years to fully materialise.

Trump threatens Greenland tariffs, sparking transatlantic tensions

[8:57 am] The US president announced plans to impose up to 25% tariffs on eight European countries to pressure Denmark into selling Greenland, drawing sharp pushback from allies.

Trump proposes a 10% tariff on Denmark, Norway, Sweden, France, Germany, the UK, the Netherlands and Finland, rising to 25% if a deal for Greenland is not reached by June 1.

European leaders condemned the move as undermining NATO and sovereignty, with Germany, France, the UK, Sweden and Denmark pledging coordinated responses.

The tariffs risk raising prices on imports to the US, including pharmaceuticals and industrial goods, while further straining transatlantic relations.

S&P 500 Q4 earnings slightly beat expectations

[8:52 am] Early Q4 results show solid profit growth, though revenue beats are weaker than historical norms.

7% of S&P 500 companies have reported so far

Blended EPS growth for Q4 stands at 8.2%, slightly below the 8.3% consensus

Of companies reporting so far, 79% have beaten EPS forecasts, in-line with the one-year average and above the five-year average.

Revenue surprises are weaker, with 67% of firms beating sales expectations, below the one-year (71%) and five-year (70%) averages.

Overall, earnings are 5.8% above expectations, and sales are only 0.3% above forecasts, both below recent historical averages, suggesting profit growth is outpacing top-line performance.

Wall Street banks see momentum rolling into 2026

[8:49 am] After a record year for trading and a sharp rebound in dealmaking, major US banks say market conditions remain supportive, though risks around valuations and policy loom.

Trading revenue jumped 15% in 2025 to a record US$134bn across Wall Street’s biggest banks, with executives arguing the cycle is still mid stream rather than peaking.

Market volatility tied to Trump’s policy agenda has driven client repositioning, while rate cuts and deregulation are rebuilding pipelines for M&A and capital markets activity.

Goldman flagged one of its strongest ever backlogs across advisory, debt and equity underwriting, reinforcing expectations of a strong 2026 for investment banking fees.

Share prices of Morgan Stanley and Goldman rose sharply on results, while the six largest US banks posted their biggest combined profit since 2021 and returned over US$140bn via dividends and buybacks.

Executives cautioned that elevated asset prices and geopolitical or policy shocks could quickly derail activity, even as banks continue to cut costs after eliminating more than 10,600 jobs last year.

Source: Bloomberg

Trump flags credit card rate cap as banks push back

[8:48 am] The White House is considering executive action to cap US credit card interest rates, signalling a more interventionist approach to affordability that is already unsettling banks and payments firms.

The administration is weighing a one year 10% cap on credit card rates, with Trump setting a January 20 deadline and publicly demanding companies lower rates despite limited detail on implementation.

Lenders are pushing back, with JPMorgan, Citi and Bank of America warning the cap could restrict access to credit, slow the economy and disproportionately impact lower income borrowers.

The proposal sits alongside broader affordability measures, including banning institutional buyers from single family homes, restricting buybacks at listed homebuilders and allowing 401(k) withdrawals for housing deposits.

Markets remain focused on execution risk, with industry lobbyists scrambling for clarity and the possibility that banks either pull back lending or introduce capped rate products on limited terms.

Global equity inflows surge as rate cut bets build

[8:46 am] Investors piled back into risk assets last week, pushing global equities to fresh highs as softer US inflation reinforced expectations of rate cuts later this year.

Global equity funds saw US$45.6bn of net inflows, the largest weekly buying in 15 weeks, signalling strong risk appetite despite macro and geopolitical concerns.

US equity funds led with US$28.2bn of inflows, the biggest in two and a half months, while Europe and Asia also recorded solid net buying.

The MSCI World index hit new records, building on a 20.6% gain last year and rising about 2.4% year to date, underscoring momentum-driven flows.

Sector positioning favoured cyclicals and growth, with tech, industrials and metals and mining attracting a combined US$7.2bn in weekly inflows.

Investors rotated out of cash, with money market funds seeing US$67.2bn of outflows, while bond funds continued to attract steady inflows and emerging markets saw their strongest equity inflows since October 2024.

Source: Reuters

Good morning!

[8:34 am] ASX 200 futures are down 1pts (-0.01%) as of 8:30 am AEDT.

Major US benchmarks pretty much flat overnight, only the Russell 2000 finished higher

Russell 2000 outperformed the S&P 500 for an eleventh straight session, marking the longest beat streak since 2008

Trump threatened tariffs on EU countries that don't support the Greenland takeover

To catch up on all overnight developments, check out today's Morning Wrap.