ASX 200 Live Today - Friday, 12th June

The S&P/ASX 200 is set to rally after commodity prices bounced sharply higher overnight and Wall Street rallied on renewed Iran deal talks.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Friday, June 12. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 sharply higher, positive for the week

[2:15 pm] The S&P/ASX 200 is currently up 1.93%, trading around session highs and on track to finish the week 2.0% higher. Is it wrong to feel cautiously optimistic after this bounce (very strong breadth, resources bounce, yield-sensitive/consumer-facing sectors soared this week, yields breaking down etc.)

Miners bounced back, with the Materials index up 3.7% (but still down 4.9% in the last six sessions). Staples, Discretionary, Healthcare and Real Estate have all had an incredible week, up 9.2%, 8.7%, 7.5% and 5.0% respectively. While Aussie inflation continues to run hot (latest headline CPI was 4.2% in April, but below 4.6% in March and 4.4% ests), yields are starting to move in the opposite direction. The Australian 10-year yield is down 15 bps in the last four sessions to 4.82%, the lowest since 6 March, while the policy-sensitive 2-year is down 19 bps to 4.48%, the lowest since 11 March.

Of course, there's the highly anticipated SpaceX IPO tonight, which could drive plenty of broader market volatility. The valuation chatter has been relentless, and there's plenty of coverage out there about that.

What I'll leave you with is this: Remember when Guzman Y Gomez debuted and copped all that criticism for trading on (off the top of my head) ~42x FY25e EBITDA? The stock still rallied ~30% on debut, and was up a little over 100% from its IPO price just eight months later. And the highly anticipated Figma? It rallied 250% on debut back in July 2025. (Just don't look at where these stocks are at now)

Best and worst performing stocks of the week

[1:33 pm] Here are the best and worst performing S&P/ASX 200 stocks week-to-date. Steadfast has surged off the back of a takeover offer, building-related names like Reece and Reliance rallied off solid US home sales data and consumer-facing names like Coles and Premier Investments caught a bid. Meanwhile, a broad list of gold, uranium and aluminum stocks struggled.

Ticker | Company | 1 Week % | Price |

|---|---|---|---|

SDF | Steadfast Group | 30.22% | $5.24 |

CSL | CSL | 15.72% | $108.10 |

LLC | Lendlease Group | 14.92% | $2.85 |

REH | Reece | 14.39% | $15.78 |

RWC | Reliance Worldwide | 13.05% | $3.60 |

PMV | Premier Investments | 11.57% | $14.27 |

COL | Coles Group | 11.48% | $24.13 |

BXB | Brambles | 11.45% | $18.94 |

CHC | Charter Hall Group | 11.40% | $22.73 |

SGP | Stockland | 11.10% | $4.26 |

Ticker | Company | 1 Week % | Price |

|---|---|---|---|

OBM | Ora Banda Mining. | -18.65% | $1.08 |

EOS | Electro Optic Systems | -16.28% | $9.34 |

NXG | Nexgen Energy | -14.00% | $13.80 |

PDN | Paladin Energy | -12.55% | $9.62 |

CMM | Capricorn Metals | -11.41% | $11.72 |

AAI | Alcoa Corporation | -11.08% | $97.54 |

NXT | NextDC | -10.91% | $14.61 |

REA | REA Group | -10.46% | $141.80 |

BGL | Bellevue Gold | -9.73% | $1.33 |

SIG | Sigma Healthcare | -9.69% | $2.66 |

Top ASX 200 gainers and losers

[1:30 pm] Lithium and copper stocks have managed to trend slightly higher, while a few gold stocks slipped out of the leaderboards. While REA Group, refiners, oil and gas plays, and healthcare stocks lag.

Ticker | Company | % Chg | Price |

|---|---|---|---|

DVP | Develop Global | 8.93% | $6.83 |

GMD | Genesis Minerals | 8.65% | $5.22 |

A2M | A2 Milk Company | 8.45% | $5.97 |

ELV | Elevra Lithium | 8.26% | $11.53 |

IMD | Imdex | 8.13% | $3.99 |

SFR | Sandfire Resources | 7.98% | $19.82 |

BGL | Bellevue Gold | 7.89% | $1.33 |

EMR | Emerald Resources | 7.10% | $5.28 |

JHX | James Hardie | 6.79% | $33.80 |

PLS | PLS Group | 6.73% | $6.34 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

REA | REA Group | -3.68% | $141.71 |

VEA | Viva Energy Group | -3.43% | $2.25 |

CBO | Cobram Estate Olives | -2.01% | $3.90 |

BPT | Beach Energy | -1.83% | $1.07 |

ASK | Abacus Storage King | -1.64% | $1.38 |

WDS | Woodside Energy Group | -1.40% | $31.08 |

CNU | Chorus | -1.39% | $8.14 |

GNE | Genesis Energy | -1.38% | $2.14 |

SIG | Sigma Healthcare | -1.30% | $2.66 |

RMD | Resmed | -1.29% | $27.61 |

Monash IVF claws its way back to breakeven

[1:17 pm] Shares in Monash IVF opened 5.9% lower this morning, but currently up 0.7% despite the company announcing its second downgrade of the year.

The key numbers from this morning's post:

FY26 underlying NPAT guided to $17-18m vs prior $20m and ests of $20.3m (14% miss at midpoint)

Australian market stimulated cycle volumes down 4.7% on a rolling three-month basis to end-April, with weakness continuing through May and June

National market share lifted 1.0ppt to 20.1% on a rolling three-month basis, with notable gains in some states

Cost and operational efficiency initiatives flagged at the half to contribute more meaningfully in FY27 given timing of implementation

What's interesting here is that the company has managed to win market share, despite the two embryo incidents last year.

Korean stocks surge

[12:08 pm] The Kospi soared as much as 8.5% on Friday, led by Samsung Electronics (+11.0%) and SK Hynix (+7.7%), as easing Middle East tensions drove foreigners back into the world's best-performing equity market.

Kospi now up 97% year-to-date as the world's top-performing stock market

Foreigners turned net buyers on Friday after offloading $83bn of Kospi names year-to-date through Thursday

Korea Exchange briefly halted program buying as futures surged, with circuit breakers triggered repeatedly this week including a 20-minute halt on Monday

Samsung and SK Hynix make up more than half of Kospi market cap, leaving the index unusually exposed to the AI chip cycle and amplified further by leveraged ETF flows

Analysts' take on Super Retail

[11:32 am] Super Retail Group hosted an investor day on Thursday, where new management outlined a 5-year strategy centred on network expansion, category growth, and a cost transformation program across its four retail brands, with an ambitious store rollout plan targeting over 900 stores that surprised brokers and exceeded consensus by a meaningful margin.

RBC Capital Markets maintained Outperform, raised target from $15.50 to $15.70, calling the store growth plans the largest surprise of the day with regional Rebel expansion targeting higher contribution margin stores, despite a material FY27 group EBIT cut on Ignite costs.

Goldman Sachs maintained Buy, raised target from $15.20 to $15.40, viewing management's multi-year growth roadmap as credible with favourable FX and stock loss improvements supporting FY27 margins and ERP investment a necessary step for long-term operating leverage.

Analysts' take on Steadfast Group

[11:30 am] Steadfast Group received a non-binding indicative proposal from a consortium of Amwins Group and Dragoneer Investment Group on Wednesday, to acquire all outstanding shares at $6.00 cash per share (~52% premium) via a scheme of arrangement, with Dragoneer taking the retail brokerage franchise and Amwins acquiring the underwriting agency business. The stock rallied 36.2% on the day.

The board granted 8 weeks of exclusive due diligence and signalled intent to unanimously recommend the deal absent a superior proposal.

Jarden maintained Overweight, raised target from $5.65 to $5.90, flagging Amwins as a strategic trade buyer with Kelly's continued tenure a strong completion signal and AUB as a credible read-across for sector consolidation.

UBS maintained Buy, target unchanged at $6.00, noting private market valuations are compressing less than listed peers and that further bidder interest remains possible given no broader process was run.

Macquarie maintained Outperform, expecting elevated short interest to unwind near term while flagging nuanced leverage dynamics under the split ownership structure and uncertainty around retail brokerage roll-up assumptions, with ACCC and FIRB approval not viewed as an impediment.

Gold stocks sharply higher

[10:45 am] Gold prices bounced 3.5% overnight (after falling 10.3% in the previous seven sessions) to US$4,212/oz, bringing much needed life back into battered gold miners. Most names are up 3-7% in early trade but still down an average 19.9% year-to-date.

Ticker | Company | % Chg | Price | YTD % |

|---|---|---|---|---|

BC8 | Black Cat Syndicate | 10.9% | $0.97 | -20.6% |

BGL | Bellevue Gold | 7.9% | $1.33 | -21.5% |

GMD | Genesis Minerals | 7.7% | $5.17 | -27.8% |

AMI | Aurelia Metals | 7.5% | $0.29 | 16.3% |

MEK | Meeka Metals | 6.4% | $0.12 | -56.7% |

EMR | Emerald Resources | 6.3% | $5.24 | -16.6% |

EVN | Evolution Mining | 6.1% | $11.62 | -7.6% |

PNR | Pantoro Gold | 6.1% | $2.44 | -50.2% |

VAU | Vault Minerals | 6.0% | $4.07 | -25.2% |

WGX | Westgold Resources | 5.3% | $4.73 | -24.9% |

RRL | Regis Resources | 5.0% | $5.86 | -22.1% |

CYL | Catalyst Metals | 5.0% | $5.03 | -31.8% |

NEM | Newmont | 4.9% | $139.05 | -7.4% |

OBM | Ora Banda Mining | 4.9% | $1.07 | -30.1% |

SBM | St. Barbara | 4.9% | $0.54 | -7.0% |

NST | Northern Star Resources | 4.8% | $19.20 | -21.8% |

RMS | Ramelius Resources | 4.2% | $2.99 | -26.9% |

RSG | Resolute Mining | 4.0% | $1.04 | -15.5% |

ALK | Alkane Resources | 3.8% | $1.43 | 7.3% |

CMM | Capricorn Metals | 3.8% | $11.71 | -16.4% |

PRU | Perseus Mining | 3.3% | $4.82 | -12.6% |

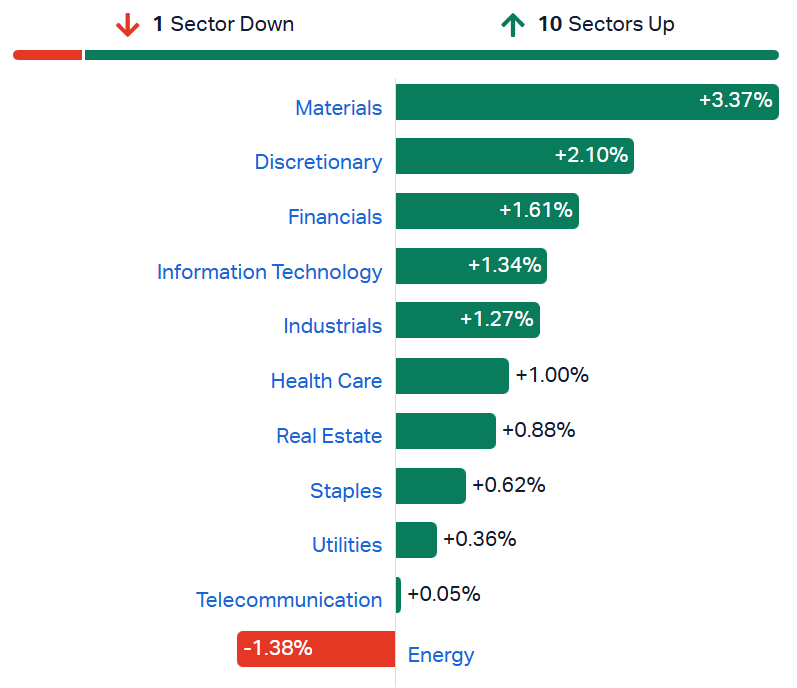

ASX 200 rallies to a near-six week high

[10:40 am] ASX 200 up 1.75% in early trade, just ~0.1% away from a fresh six-week high. Only Energy is trading lower after Brent suffered a 6.1% dip overnight to US$89.14 a barrel. Very strong breadth, with 169 constituents (85%) trading higher. Materials (+3.4%) bouncing after suffering an 8.6% pullback between 4-10 June, Discretionary now up 8.5% in the last five sessions and All Ords Gold Index (+5.1%) set to snap a five-day losing streak, where it dipped 14%.

S&P/ASX 200 sectors (Source: Market Index)

Top All Ords gainers and losers

[10:30 am] Here are the top S&P/All Ords movers in early trade.

Ticker | Company | % Chg | Price |

|---|---|---|---|

BC8 | Black Cat Syndicate | 11.72% | $0.97 |

BMC | Bmc Minerals | 10.27% | $2.90 |

MEI | Meteoric Resources | 9.37% | $0.18 |

CTM | Centaurus Metals | 8.82% | $0.56 |

BGL | Bellevue Gold | 8.54% | $1.34 |

DVP | Develop Global | 8.45% | $6.80 |

ASM | Australian Strategic Materials | 8.29% | $1.27 |

SFR | Sandfire Resources | 8.07% | $19.83 |

EQR | EQ Resources | 7.91% | $0.23 |

PDI | Predictive Discovery | 7.76% | $0.79 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

DTR | Dateline Resources | -7.69% | $0.12 |

VEA | Viva Energy Group | -4.29% | $2.23 |

MAU | Magnetic Resources | -3.65% | $1.85 |

KAR | Karoon Energy | -3.41% | $1.98 |

OCA | Oceania Healthcare | -3.36% | $0.58 |

REA | REA Group | -3.25% | $142.35 |

VGL | Vista Group International | -3.17% | $1.83 |

NWS | News Corp | -3.10% | $42.81 |

WTN | Winton Land | -3.08% | $2.20 |

CEN | Contact Energy | -2.46% | $7.94 |

Top ASX 200 gainers and losers

[10:28 am] Gold and copper stocks open sharply higher, while energy-related stocks (oil and gas, refiners and coal) dip on US-Iran deal progress.

Ticker | Company | % Chg | Price |

|---|---|---|---|

BGL | Bellevue Gold | 8.54% | $1.34 |

PDI | Predictive Discovery | 8.44% | $0.80 |

SFR | Sandfire Resources | 8.04% | $19.83 |

DVP | Develop Global | 7.66% | $6.75 |

GMD | Genesis Minerals | 7.50% | $5.16 |

GGP | Greatland Resources | 7.27% | $12.39 |

JHX | James Hardie | 7.14% | $33.91 |

IMD | Imdex | 6.64% | $3.94 |

EVN | Evolution Mining | 6.30% | $11.64 |

EMR | Emerald Resources | 6.29% | $5.24 |

Ticker | Company | % Chg | Price |

|---|---|---|---|

VEA | Viva Energy Group | -4.29% | $2.23 |

REA | REA Group | -3.00% | $142.72 |

CEN | Contact Energy | -2.46% | $7.94 |

WDS | Woodside Energy Group | -2.40% | $30.77 |

SLC | Superloop | -2.08% | $3.53 |

BPT | Beach Energy | -1.83% | $1.07 |

STO | Santos | -1.36% | $7.96 |

RMD | Resmed | -1.04% | $27.68 |

SMR | Stanmore Resources | -0.93% | $2.68 |

YAL | Yancoal Australia | -0.91% | $6.52 |

Magellan to rebrand as Barrenjoey Group after ACCC clears merger

[10:08 am] Magellan Financial Group has secured unconditional ACCC clearance for its merger with Barrenjoey Capital Partners and intends to rebrand the combined entity.

ACCC determination unconditional, subject to expiry of the statutory 14-day review period

Merger completion expected in early July

Shareholder approval to be sought at the 22 October 2026 AGM to change the company name to Barrenjoey Group Limited and ticker from MFG to BJY

Magellan Investment Partners will be rebranded as Barrenjoey Investment Partners

Company page: Magellan Financial Group (MFG)

DigiCo to divest LAX data centre sites, reaffirms FY26 EBITDA guidance

[9:58 am] DigiCo Infrastructure REIT has entered a conditional agreement to sell its LAX1 and LAX2 data centre sites in Los Angeles at broadly the acquisition price, freeing up capital for its SYD1 development.

Proceeds, alongside the Chicago sale, will lift available liquidity to ~$1.0bn to fund the SYD1 development

On 6 May, DGT sold its Chicago (CHI1) facility for US$750m, a 5% premium to its November 2024 purchase price and a passing yield of 5.8%

Completion subject to customary conditions and expected in 1H FY27

FY26 underlying EBITDA guidance reaffirmed at $125m

Company page: DigiCo Infrastructure REIT (DGT)

Hedgeye flags ResMed as new short with 30% downside on GLP-1 risk

[9:43 am] Hedgeye analyst Tom Tobin has added ResMed as a short idea, arguing GLP-1s will erode the sleep apnea TAM and pressure consensus estimates.

Hedgeye sees at least another 30% downside on top of the ~30% fall from the 2025 peak

Thesis hinges on cheaper, oral and multi-condition GLP-1s shrinking the sleep apnea TAM at the margin

Tobin argues ResMed's growth algorithm leans heavily on a new-patient funnel that is already narrowing

Overweight and obese cohorts, identified as ResMed's real incremental TAM, are the same population GLP-1s are now shrinking

Consensus estimates have largely held, leaving room for downgrades and a lower multiple regime

Company page: ResMed (RMD)

ANZ NZ CEO Antonia Watson to retire

[9:42 am] ANZ Bank New Zealand CEO Antonia Watson will retire at the end of FY26, with current Chief Risk Officer Ben Kelleher to step into the role.

Watson finishes on 30 September 2026 after 17 years at ANZ NZ, including six as CEO and Group Executive

Kelleher has been ANZ NZ Chief Risk Officer for more than two years, previously serving as Managing Director, Personal Banking for five years

Company page: ANZ Group (ANZ)

Brazilian Rare Earths defines +9km rare earth corridor at Velhinhas

[9:36 am] Brazilian Rare Earths has unveiled a district-scale exploration corridor south of its Monte Alto deposit in Bahia, supported by airborne geophysics and early diamond drilling results.

Airborne survey defines more than 9km of cumulative rare earth exploration trends across four parallel north-northeast zones, beginning ~5km south of Monte Alto

Ultra-high-grade surface samples returned grades of 39.6%, 20.9% and 13.5% TREO

Reconnaissance diamond drilling returned 19.6% TREO, 33,607ppm NdPr, 1,463ppm Dy₂O₃, 248ppm Tb₄O₇, 7,431ppm Y₂O₃ and 1,087ppm U₃O₈

Mineralisation includes a suite of critical minerals spanning NdPr, DyTb, yttrium, niobium, scandium, tantalum and uranium

Additional diamond rig mobilised, with a +5,000m drilling campaign now underway to test priority geophysical anomalies and extend bedrock mineralisation

Company page: Brazilian Rare Earths (BRE)

Monash IVF cuts FY26 guidance on weaker Australian ART market

[9:19 am] Monash IVF has downgraded FY26 underlying NPAT guidance to $17-18 million, well below consensus, citing softer Australian fertility market activity.

FY26 underlying NPAT guided to $17-18m vs prior $20m and ests of $20.3m (14% miss at midpoint)

Australian ART market stimulated cycle volumes down 4.7% on a rolling three-month basis to end-April, with weakness continuing through May and June

ART = Assisted Reproductive Technology.

National market share lifted 1.0ppt to 20.1% on a rolling three-month basis, with notable gains in some states

International operations volumes expected to be materially higher year-on-year in H2

Cost and operational efficiency initiatives flagged at the half to contribute more meaningfully in FY27 given timing of implementation

The company guided to FY26 NPAT of $20 million just four months ago, so new guidance reflects a 12.5% downgrade (at the midpoint) after a relatively short span of time. The stock is down 8% year-to-date and flat in the last twelve months (though ~55% off May 2024 record highs).

Company page: Monash IVF Group (MVF)

Commodities broadly higher

[9:08 am] Commodities traded sharply higher overnight, bouncing from sharp declines over the past 5-6 sessions.

Commodity | Change % | Last (US$) |

|---|---|---|

Silver | 6.3% | $67.35 |

Palladium | 4.5% | $1,268 |

Gold | 3.5% | $4,213 |

Platinum | 3.3% | $1,717 |

Copper | 3.1% | $6.43 |

Zinc | 1.7% | $3,497 |

Aluminum | 1.0% | $3,520 |

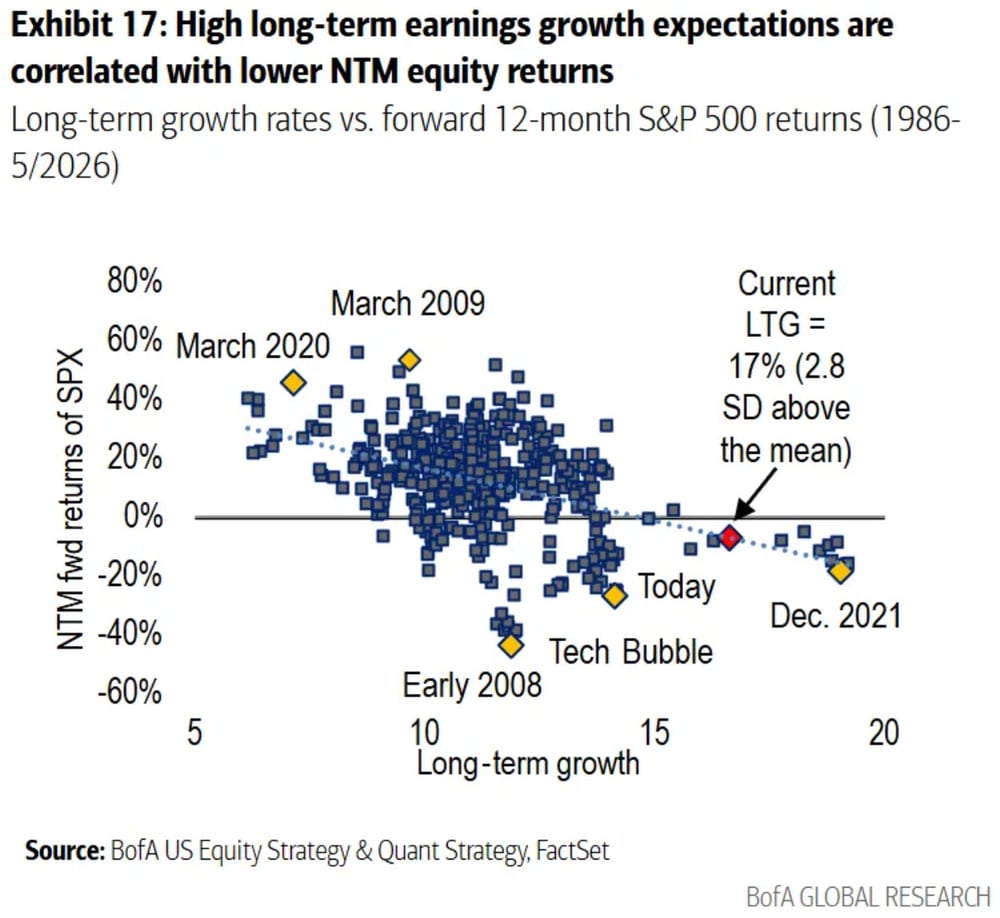

BofA warns elevated growth expectations point to weaker forward returns

[9:00 am] Bank of America research flags that today's exceptionally optimistic long-term earnings growth forecasts have historically preceded weaker equity returns, raising the risk of disappointment from current levels.

Fertiliser prices unwind Iran war spike

[8:58 am] Urea prices have retraced sharply toward pre-war levels as supply chains adjust to the Strait of Hormuz disruption, according to Bloomberg.

New Orleans granular urea spot fell to US$453.50 per short ton, the lowest since early February

India's latest tenders saw offers at US$530 per tonne, down 44% from April highs

Relief driven by seasonal demand dips, China restarting exports, and faster-than-expected supply chain rerouting

Risks remain from damaged infrastructure and uncertainty heading into future planting cycles

OpenAI weighs token price cuts ahead of Anthropic IPO

[8:53 am] OpenAI is considering significant cost reductions for its services in anticipation of similar moves from Anthropic, hinting at a pricing war between the two as both head toward IPOs.

Deliberations remain early with nothing decided, but cuts under consideration include lowering per-token pricing if Anthropic moves first

OpenAI filed confidentially for its IPO this week and was last valued at $852bn in March, with Anthropic having lined up Morgan Stanley and Goldman Sachs after raising at a $965bn valuation last month

Corporate AI budgets under pressure, with Uber capping internal use of tools like Claude Code after blowing through its annual AI spend and Walmart restricting employee access to its in-house agent

Both companies also face mounting competition from Microsoft and Alphabet, raising the stakes of any sustained pricing battle

Source: Bloomberg

Oil's puzzle: Why the Iran shock hasn't broken the market

[8:51 am] Bloomberg's Javier Blas argues 10 structural and circumstantial factors have kept Brent below US$100 despite the largest supply shock on record, with China the single biggest swing factor.

China imported 6.7m b/d of crude by tanker in May, down nearly 40% on the 2025 average, with the 4m b/d drop equivalent to combined German and French consumption and possibly reflecting strategic reserve draws

Demand destruction running at 3-4m b/d mostly in petrochemicals, with Asian consumers switching to coal and firewood and Indian cooking fuel supplies running dry

Around 7m b/d still leaves the Persian Gulf, with bypass pipelines through Saudi Arabia and the UAE moving 5m b/d and another 2m b/d shuttled by tanker around the Strait with beacons off

IEA's record 400m barrel release is flowing at 2.5m b/d but US reserves sit at 40-year lows, with commercial stockpiles potentially hitting critical levels by August

Market was already oversupplied by 3-4m b/d before the war thanks to US shale and OPEC+ hikes, while American continent production is up 2m b/d y/y with Brazil up 20% to a record and Guyana, US and China also at all-time highs

Trump's near-40 deal-is-close social media posts have repeatedly knocked prices up to 10%, while deeper options market liquidity (call volumes up 8x since 2016) has reduced reliance on outright futures buying as a hedge

Source: Bloomberg

World Bank cuts global growth to weakest since pandemic

[8:45 am] The World Bank cut its 2026 global growth forecast to 2.5% citing the Iran war's energy shock, warning growth could slow to as little as 1.3% under a severe scenario.

2026 global growth lowered to 2.5% from 2.9% in 2025, the weakest since the pandemic, with two-thirds of economies seeing downward revisions and headline inflation forecast at 4%

Baseline assumes Brent averages US$94/bbl in 2026 (up 36% on 2025) with worst energy disruptions abating by end-July, growth slips to 2.1% at US$115/bbl and as low as 1.3% if financial market stress compounds the shock

Middle East, North Africa, Afghanistan and Pakistan growth slashed 2.7ppt to 1.6%, with UAE cut to 2.4% from a prior 5% forecast and Turkey trimmed to 2.8%

Developing economy growth seen at a post-pandemic low of 3.6%, down from 4.4% in 2025, with the 2020s described as a "lost decade" for dozens of poorer nations

Eurozone pegged at 0.8% in 2026 (from 1.4%), Japan 0.7% (from 1.1%), China 4.2% (down 0.2ppt), US held at 2.2%, India remains the fastest-growing major economy at 6.6%

ECB delivers first hike since 2023 as Iran war stokes inflation

[8:44 am] The ECB hiked rates by 25 bps to 2.25% in response to energy-driven inflation pressures from the US-Iran conflict, lifting its inflation forecasts and trimming growth.

Headline inflation now expected to average 3% in 2026, cooling to 2.3% in 2027 and 2% in 2028, with the revision driven by higher energy prices feeding into food, goods and services

Growth forecasts cut to 0.8% in 2026, 1.2% in 2027 and 1.5% in 2028, reflecting a more pronounced commodity, real income and confidence hit from the war

Lagarde flagged upside risks to inflation and downside risks to growth, with the Governing Council not pre-committing to a particular rate path

Eurozone inflation rose to 3.2% in May with Q1 GDP growth at just 0.1%

Trump flip-flops on Iran strikes as deal talks intensify

[8:42 am] Markets looked through another volatile day of Mideast brinkmanship, with Trump first threatening fresh strikes before cancelling them and flagging an imminent agreement.

Trump initially said Iran would be hit "very hard tonight" and floated US control of Iranian oil infrastructure including the Kharg Island export terminal, before backtracking in the early afternoon and saying main points have been "approved by all parties"

Equities rallied and crude eased on the reversal, consistent with the market's pattern of treating ceasefire threats as noise and pricing any MOU as a wait-and-see outcome

Key sticking points remain unresolved including sanctions relief, Strait of Hormuz navigation oversight, and the fate of Iran's highly enriched uranium, with Israel's Hezbollah operations in Lebanon a further wild card

Reuters reports MOU-related messages continue to be exchanged with possible release of Iran's frozen funds in focus, while a deal anchored on a no-nuclear-weapons pledge and lengthy enrichment pause is seen as attainable

US stocks rally as Trump pulls Iran strikes

[8:39 am] Wall Street surged on signs of an Iran ceasefire deal, with risk-on positioning across equities, bonds, and small-caps.

S&P 500 up 1.7% and Nasdaq up 2.5%, the S&P's best session since 8 April, after Trump cancelled tonight's planned bombing of Iran and Tehran approved a draft ceasefire extension

Russell 2000 led gains up 3.02% with VIX down around 12%, semis, memory, networking, tech hardware, industrials and materials all outperforming

Yields down 8-10 bps as Fed tightening expectations eased, dollar index down 0.3%, Brent settled 6.1% lower to US$89.14 a barrel

Oracle Q4 beat and guided ahead but flagged $70bn capex for FY27 and plans to raise $40bn in additional capital, with reports OpenAI is weighing steep token price cuts to win customers back from Anthropic

May headline PPI up 1.1% m/m vs 0.7% ests, but core PPI rose just 0.4% m/m vs 0.5% ests

Markets cautious on follow-through given prior failed deals, with the naval blockade staying in place until signing and Israel-Lebanon dynamics still unresolved ahead of tomorrow's $75bn SpaceX IPO

Good morning!

[8:32 am] ASX 200 futures are up 146 pts (+1.68%)

The overnight session in a nutshell:

S&P 500 jumped 1.7% and the Nasdaq 2.5% after Trump called off Iran strikes and signalled a deal is close, sparking a broad risk-on bounce

VIX fell 12% as the Russell 2000 led gains up 3.02%, with tech, industrials and materials driving the turnaround

Most commodities bounced more than 3%, the ECB delivered its first rate hike since 2023, and SpaceX prices its $1.75tn Nasdaq mega-IPO