ASX 200 Live Today - Friday, 10th April

The S&P/ASX 200 is set to slip despite a broadly positive overnight session on Wall Street. Here are today's top stories.

Today’s ASX 200 Updates

Welcome to our live ASX coverage for Friday, April 10. Expect a high volume of posts pre-market and more periodic updates throughout the day. We'll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 slips, off worst levels

[2:21 pm] The ASX 200 currently down 0.30%, but well above session lows of -0.76%, and up 4.2% for the week. It's been an encouraging snap-back rally, with plenty of sectors recovering sharply from year-to-date lows.

In the past week, Financials (+6.4%), Materials (+6.2%), Real Estate (+4.1%) and Discretionary (+3.6%) have all posted solid gains, while initial Iran conflict winners like Staples (-0.5%), Utilities (-1.4%) and Energy (-5.1%) have underperformed.

Pretty insane seeing the Banks (XBK) Index on a seven-day win streak, up 9.0% and within 1.5% of all-time highs. I'm sure it amazes everyone how CBA (also up 9% in the last six sessions) is catching a bid in this climate, while trading at 29x.

That said, volatility is unlikely to subside in the near-term, nor are the headlines. Brent continues to trade around the US$96 per barrel level on Friday, after Israel agreed to direct talks with Lebanon. Still, the cautiously optimistic market will likely want more concrete evidence the Strait is opening, and a more permanent ceasefire. That's a wrap for this week, it's good to be back after a little break. Have a good weekend!

Fed and Treasury summon Wall Street CEOs over Anthropic's Mythos cyber risk

[1:45 pm] US regulators convened an emergency meeting with systemically important bank chiefs to address cybersecurity threats posed by Anthropic's most powerful AI model yet.

Treasury Secretary Bessent and Fed Chair Powell assembled CEOs from Citigroup, Morgan Stanley, Bank of America, Wells Fargo and Goldman Sachs at Treasury headquarters in Washington, with JPMorgan's Jamie Dimon unable to attend

The meeting centred on Anthropic's Mythos model, which the company has said is capable of identifying and exploiting vulnerabilities across every major operating system and web browser when directed to do so

Anthropic has limited Mythos to a small group of major technology and finance firms under "Project Glasswing," which includes Amazon, Apple and JPMorgan, with the aim of securing critical systems before similar models become more widely available

Source: Bloomberg

Energy stocks broadly lower

[1:23 pm] Energy stocks, including coal, refiners and oil, are trading broadly lower despite relatively flattish energy prices overnight, where Brent finished 0.3% lower to US$96.40 a barrel.

Ticker | Company | % Chg | Price |

|---|---|---|---|

WHC | Whitehaven Coal | -5.84% | $7.90 |

NHC | New Hope | -3.48% | $5.14 |

YAL | Yancoal | -3.36% | $7.19 |

BPT | Beach Energy | -2.28% | $1.20 |

STO | Santos | -2.08% | $7.79 |

WDS | Woodside Energy Group | -1.98% | $32.67 |

KAR | Karoon Energy | -1.67% | $1.94 |

ALD | Ampol | -1.56% | $32.71 |

VEA | Viva Energy Group | -0.60% | $2.49 |

China exits factory deflation for the first time since 2022

[12:56 pm] China's producer prices turned positive in March, ending over three years of factory-gate deflation, though the catalyst is an energy shock rather than a genuine demand recovery.

PPI rose 0.5% year-on-year in March (vs. 0.4% ests), swinging sharply from a 0.9% decline in February, marking the first positive reading since late 2022

The rebound is driven by surging commodity costs tied to the Iran war

Input costs are rising faster than selling prices, with raw material purchase prices up 0.8% vs. output prices up just 0.5%, squeezing factory margins as producers struggle to pass on higher costs

Non-ferrous metals are also a key driver, with output prices for non-ferrous metal mining and smelting surging 36% and 22% respectively in March, supported by AI-related demand alongside the commodity rally

CPI cooled to 1.0% in March (vs. 1.3% in February), though consumers are feeling energy pain, with vehicle fuel costs up 3.4% after contracting 9% the prior month, the fastest gain in transportation costs since January 2023

Whitehaven secures US$600m syndicated facility

[12:52 pm] Whitehaven has locked in a new US$600 million syndicated facility, partially refinancing its existing acquisition debt at improved terms with strong lender support.

The facility comprises a US$475m term loan and a US$125m revolving credit facility with a 4.5-year tenor, replacing a portion of the existing US$1.1bn acquisition term loan and the prior US$100m corporate revolving credit facility

Whitehaven has also received credit approvals for an additional US$150m upsizing option, providing further flexibility as part of the broader refinancing process

The deal reduces funding costs, extends the debt maturity profile, and enhances liquidity, with strong lender participation cited as a reflection of confidence in the company's credit profile and strategy

Company page: Whitehaven Coal (WHC)

Tech stocks broadly lower

[11:40 am] The S&P/ASX 200 Tech Index is currently down 2.8%, hovering intraday lows. It's now down 9.1% in the last two sessions. Some pretty heavy selling across key names like Wisetech, Life360 and Xero.

Wisetech opened the session 5.2% lower, rallied back up to a 1.0% decline and currently down 3.7%. The stock is on the verge of breaking below recent lows, which will mark a fresh near-four year low.

Ticker | Company | % Chg | Price |

|---|---|---|---|

NXL | Nuix | -4.24% | $1.13 |

WTC | Wisetech Global | -4.01% | $37.07 |

360 | Life360 | -3.72% | $19.39 |

MP1 | Megaport | -3.36% | $6.62 |

SDR | Siteminder | -3.23% | $2.85 |

XRO | Xero | -2.99% | $71.22 |

CDA | Codan | -2.50% | $33.89 |

DGT | Digico Infrastructure REIT | -2.47% | $1.78 |

NXT | Nextdc | -2.44% | $12.59 |

HSN | Hansen Technologies | -2.03% | $4.59 |

OCL | Objective Corporation | -1.83% | $11.24 |

DTL | Data#3 | -1.78% | $6.64 |

TNE | Technology One | -1.74% | $27.41 |

IRE | Iress | -1.73% | $6.83 |

PME | Pro Medicus | -1.70% | $125.21 |

CAT | Catapult Sports | -1.57% | $3.14 |

PPS | Praemium | -1.45% | $0.68 |

AD8 | Audinate Group | -1.19% | $2.50 |

MAQ | Macquarie Technology Group | -1.02% | $66.04 |

DDR | Dicker Data | -0.11% | $8.69 |

BVS | Bravura Solutions | 0.10% | $1.99 |

Life360 CEO flags AI-driven restructure

[11:36 am] Life360 is cutting staff and reshaping its technology organisation around AI, with CEO Lauren Antonoff framing the move as a strategic necessity rather than a cost-reduction exercise.

The restructure reflects a fundamental shift in how work gets done, with product managers shipping code, designers building end-to-end, and engineers delivering full-stack features, meaning the "roles and ratios" of the pre-AI era no longer apply

The CEO is explicit that this is not about reducing headcount for cost savings, but reallocating investment toward new capabilities, with the company still expecting to hire, though into different roles than before

The longer-term opportunity is framed around expanding Life360's addressable market across all family life stages, from young children and pets through to aging parents, with AI enabling more active and personalised engagement with members

The actual headcount reduction was not specified.

Company page: Life360 (360) | Source: LinkedIn

Top ASX 200 gainers

[10:24 am] Telix is catching a bid after the FDA accepted its re-submission for candidate TLX101-Px, an investigational agent for the imaging of brain cancer. Not many exciting gainers beyond Telix, with most top gainers up just ~1%.

Ticker | Company | % Chg | Price |

|---|---|---|---|

TLX | Telix Pharmaceuticals | 3.23% | $14.08 |

BEN | Bendigo Bank | 2.03% | $11.57 |

SIG | Sigma Healthcare | 1.67% | $2.75 |

BSL | Bluescope Steel | 1.55% | $28.45 |

MFG | Magellan Financial Group | 1.50% | $9.48 |

CEN | Contact Energy | 1.43% | $7.81 |

GYG | Guzman Y Gomez | 1.33% | $20.60 |

AAI | Alcoa Corporation | 1.15% | $103.51 |

4DX | 4DMedical | 1.11% | $6.36 |

VCX | Vicinity Centres | 1.01% | $2.51 |

Top ASX 200 losers

[10:24 am] Gold and coal names dominate today's decliners, while Orora and Transurban continue to slip following weaker-than-expected trading updates on Thursday.

Ticker | Company | % Chg | Price |

|---|---|---|---|

WHC | Whitehaven Coal | -4.17% | $8.04 |

CIA | Champion Iron | -4.04% | $5.22 |

ORA | Orora | -3.89% | $1.56 |

TCL | Transurban Group | -3.66% | $13.42 |

CYL | Catalyst Metals | -3.59% | $6.71 |

PDI | Predictive Discovery | -3.47% | $0.92 |

EVN | Evolution Mining | -3.41% | $13.45 |

SMR | Stanmore Resources | -3.40% | $2.56 |

BGL | Bellevue Gold | -3.37% | $1.81 |

GDG | Generation Development Group | -3.33% | $4.07 |

Analysts' take on Orora

[10:17 am] Orora issued a significant profit warning on Thursday, with management cutting FY26 Saverglass EBIT guidance materially due to weaker volumes, softer premium spirits demand and an adverse mix shift toward lower-margin wine and champagne, with analysts estimating group EBIT of ~$250 million, around 8-10% below prior expectations.

The update also flagged direct disruption at the Ras Al Khaimah facility and a pause to the on-market buyback. Shares fell as much as 7.9% intraday before closing down 4.7%.

Jarden downgraded to Neutral, lowered target from $2.60 to $1.80. Management's limited visibility on Saverglass demand was a key concern, with indirect conflict impacts difficult to separate from what may be broader structural softness, driving material cuts to FY26-28 earnings forecasts.

JPMorgan retained Underweight, lowered target from $1.95 to $1.55. The sharpness of the sales correction and ongoing mix headwinds were the primary concerns, with the buyback pause read as a signal of continued weakness ahead, and Amcor preferred over Orora for better end-market exposure.

UBS retained Neutral, lowered target from $2.40 to $1.70. Persistent premium spirits weakness and downtrading trends are expected to extend into FY27, with the risk of Saverglass impairments increasing despite conservative leverage.

Orora shares have continued to tank on Friday, currently down 3.7% to $1.56.

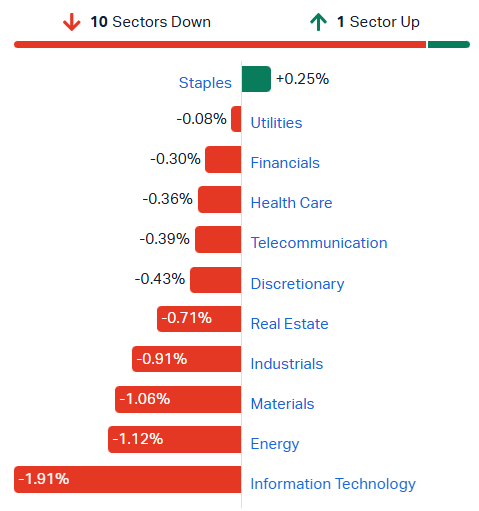

ASX 200 lower, Tech stocks tumble

[10:12 am] A classic risk-off session where Staples and Utilities are outperforming, while Tech and Resources struggle. The S&P/ASX 200 is currently down 0.76% and still trying to find a session low, though today's session follows a 6.0% rally since 30 March.

The Tech Index has gone from rallying ~14% between 30 March to 8 April to unraveling ~8.5% in the last two sessions, largely driven by the latest updates from Anthropic.

S&P/ASX 200 sectors (Source: Market Index)

Analysts' take on Transurban

[9:47 am] Transurban's March quarter traffic update on Thursday came in softer than expected, with headline growth flattered by West Gate Tunnel's contribution, easier Brisbane comparisons and North American strength, while underlying Australian traffic weakened through March. The key concern was that fuel costs, macro uncertainty and geopolitical pressures appeared to be weighing on driving behaviour, particularly in Melbourne, with Sydney also subdued due to construction disruption.

Jarden retained Neutral, lowered target from $13.50 to $12.90. Near-term traffic risk is elevated, though inflation-linked tolls provide some earnings protection and West Gate's vehicle mix was better than volumes implied.

UBS retained Neutral, lowered target from $14.65 to $14.40. Melbourne softened notably through March and the West Gate ramp-up remains uncertain, though longer-term growth options were seen as still credible.

E&P retained Neutral, lowered target from $13.85 to $12.95. Melbourne's weakness was sharper than expected and Sydney remains weighed by construction, though distribution guidance still looks adequately supported and cost control provides some downside buffer.

Rising petrol prices are rapidly improving EV economics

[9:45 am] UBS analysis finds that the surge in Australian petrol prices since the onset of the Middle East conflict has materially shifted the total cost of ownership equation in favour of EVs, particularly for small and medium segments with home charging.

Australian retail petrol prices are up ~30% since the conflict began

This has driven a near-3x surge in Google searches for "electric vehicles" and a jump in BEV market share from 7% in January to 14.6% in March

Small and medium EVs carry an ~18% upfront purchase price premium over comparable ICE vehicles

However, operating cost savings increasingly offset this as petrol prices rise

Under elevated fuel prices and low-cost home charging, EVs are cost-competitive or cheaper on a discounted total cost of ownership (TCO) basis

The "allowable" upfront EV price premium for medium segment buyers to still break even on TCO rises from ~20% at pre-disruption petrol prices (~$1.60/L) to ~29% at peak disruption pricing (~$2.65/L), meaning higher fuel costs effectively expand consumers' willingness to pay for an EV

Large SUV EVs carry a ~26% upfront premium and remain more expensive than ICE on a 10-year discounted TCO basis across all scenarios, though the gap narrows materially at higher petrol prices (EV plan charging: ~7% more expensive at $2.60/L vs. ~13% at $1.60/L)

Aurum Resources lifts Napié gold resource by 34%

[9:31 am] Aurum Resources has upgraded its mineral resource estimate for the Napié Gold Project in Côte d'Ivoire, lifting the company's total gold resource to 4.2Moz.

Napié MRE increases 34% (+290koz) to 1.16Moz at 1.2 g/t Au, with maiden Indicated Resources of 0.35Moz at 1.2 g/t Au representing a step-up in resource confidence

Group resource base now totals 4.2Moz Au across two Côte d'Ivoire projects, comprising the 3.03Moz Boundiali and 1.16Moz Napié projects

Both Tchaga and Gogbala deposits within Napié remain open along strike and at depth, supporting further resource growth potential

Company page: Aurum Resources (AUE)

Bravura Solutions chairman lifts stake by 62.5%

[9:28 am] Baskerville acquired 25,000 shares at $1.99, increasing his holding by 62.5% from 40,000 to 65,000 shares.

Bravura experienced a 29.4% rally on 9 February, when the company upgraded its FY26 guidance, including:

Revenue guidance upgraded to $280–285m vs. prior $265–275m and $269.7m ests (4.6% upgrade vs. prior, 4% beat vs. ests at the midpoint)

Cash EBITDA guidance lifted to $69–73m vs. prior $55–65m, $67.7m ests (18.3% upgrade vs. prior and 8% beat vs. ests)

The stock is now up 10.5% since the guidance upgrade, but outperformed most tech peers by trading relatively sideways since March.

Company page: Bravura Solutions (BVS)

Monadelphous secures ~$145m in new contracts and extensions

[9:22 am] Monadelphous has announced a bundle of new contracts and extensions across iron ore, copper, aluminium and gold. MND has held up relatively well in recent weeks, down 8.6% since March and still up 12% year-to-date.

Rio Tinto contract for fabrication, supply, installation and commissioning of a dust collector and ventilation system at the Paraburdoo iron ore mine in the Pilbara, with work expected to complete in 1Q27

Two-year extension to its maintenance services contract at BHP's Olympic Dam operations in South Australia, covering mechanical and electrical maintenance, shutdown and project services

Two-year extension at Queensland Alumina Limited's Gladstone operations, where Monadelphous has worked for over 30 years, with scope expanded to include demolition and power generation work

New contract with Harmony Gold for construction of a Cyclone Dewatering Plant and associated pipeline at Hidden Valley Gold Mine in Papua New Guinea

Total contract value across all awards is approximately $145m

Company page: Monadelphous Group (MND)

Capstone Copper looking to sell Mexican Cozamin mine

[9:16 am] Capstone Copper has hired Scotiabank to run a sale process for its Cozamin underground copper-silver mine in Mexico, as the company sharpens its focus on growth assets in Chile.

Cozamin produces around 20-25,000 tpa of copper and has been owned by Capstone since 2006, but is considered a smaller, non-core asset relative to the company's Chilean operations

The mine is valued at approximately $400m, with Scotiabank mandated to run the sale process

Capstone's strategic focus is on Chile, where it is expanding the Mantoverde mine and advancing the Santo Domingo project toward a final investment decision

The potential divestment adds to a broader wave of copper M&A, with First Quantum recently agreeing to sell its Çayeli mine in Turkey, Hudbay agreeing to acquire Arizona Sonoran Copper, and Anglo American having bid for Teck Resources last year

Company page: Capstone Copper (CSC) | Source: Bloomberg

SaaSpocalypse continues

[9:15 am] This is like the ... third episode of SaaSpocalypse? Software names traded broadly lower overnight, with the iShares Expanded Tech-Software ETF down 3.9%, breaking below recent lows to trade at the lowest since November 2023. Plenty of high-profile names faced far greater carnage, including Shopify (-6.4%), Intuit (-7.1%), ServiceNow (-7.8%), Snowflake (-11.8%) and more.

Earlier this week, Anthropic announced its Claude Mythos Preview, a model described as "a step change" in AI performance and "the most capable we've built to date".

Overnight, Anthropic also announced that Claude Cowork for macOS and Windows is now generally available for all paid subscribers, adding six enterprise features: Role-based access controls, group spend limits, usage analytics, expanded OpenTelemetry support, a Zoom MCP connector, and per-tool connector controls.

iShares Expanded Tech-Software ETF daily chart (Source: TradingView)

The local tech sector has already started to respond to the news, with the S&P/ASX 200 Tech Index down 6.4% on Thursday, but still ~6% away from its 30 March low.

Private markets face a $330bn debt reckoning as AI disrupts software

[9:05 am] A looming wall of software debt maturities is colliding with AI-driven disruption and tighter credit conditions, putting private equity and private credit under significant stress.

Over $330bn in high yield, leveraged loan and BDC-linked software and technology debt matures through 2028, with more than $140bn due in 2028 alone and $31bn in BDC-linked software debt coming due this year

Software and tech services have accounted for roughly half of all private equity deals in recent years, meaning the sector's deterioration has outsized implications for private market portfolios

The technology loan premium in the leveraged loan market has completely broken down this year, and falling loan prices are historically a leading indicator of rising private credit stress, with up to 15% of software direct lending potentially defaulting in coming years according to Marathon Asset Management

Source: Bloomberg

Retail investors have flipped from dip-buyers to defensive sellers

[9:01 am] Both JPMorgan and Citadel flag a meaningful regime change in retail behaviour, with the cohort now selling into strength rather than chasing rebounds.

JPMorgan notes retail has shifted from "buying the dip" to "skipping the dips, selling into rallies, and positioning more defensively," with overall activity remaining extremely subdued this week despite oil posting its largest single-day decline since 2020 and the VIX breaking below 20

Citadel Securities reports retail put activity has surged to the 99th percentile over the past two weeks relative to all 10-day periods since 2020, while call activity has fallen to the 70th percentile, and just the 13th percentile versus the past year

This divergence culminated on 2 April, when retail traded more puts than calls at Citadel Securities, only the sixth such occurrence in the platform's history, suggesting the defensive shift is structural rather than a short-term reaction

Nomura's McElligott: Ceasefire rally is a mechanical squeeze

[8:59 am] Charlie McElligott argues the equity surge is driven by positioning dynamics rather than genuine confidence in the ceasefire, with the underlying geopolitical situation far from resolved.

On the ceasefire itself, McElligott says Trump was forced "to take a knee" to "kick the can" and maintain future optionality, with "99% certainty that the vast majority of 10-point Iranian demands are untenable to both GCC and Israel on the long-horizon"

He argues the "energy and petrochem supply shock 'damage is done'" regardless of the ceasefire outcome, and that China played a key role, having "threatened Iran into last-minute pressuring to accept that Pakistani-mediated ceasefire"

On markets, he is clear that there is "99% certainty that mechanical forces in the equities vol market can't have a view on ceasefire winners/losers," framing the rally as a positioning unwind rather than a fundamental re-rating

The spike higher is described as "punitive right now for macro doomers, overhedgers bleeding YTD PNL they don't have," with vol-scaled funds forced to de-gross into what became a "face-ripper up"

The market "overhedged for chaos" and unable to crash, it was simultaneously "underpositioned for right tail rally," hence the market "crashing up" today

McElligott cautions the relief may be short-lived, warning "that doesn't mean we aren't here again and stressing in two weeks' time"

Constellation Brands beats Q4 but pulls long-term guidance amid consumer uncertainty

[8:57 am] Constellation Brands, the US maker of Modelo and Corona, delivered a solid Q4 beat but withdrew its outlook as a cautious consumer and macro uncertainty cloud the path ahead.

EPS of $1.90 vs. $1.72 ests (10% beat) and revenue of $1.92bn vs. $1.88bn ests (2% beat)

FY27 EPS guidance of $11.20-$11.90 (midpoint $11.55) vs. $12.36 ests (7% miss), with FY28 guidance withdrawn entirely citing limited near-term visibility

Overall net sales fell 3% in FY26, with consumer spending on alcohol described as increasingly "deliberate," though the CFO characterised current headwinds as cyclical rather than structural

Beer remains the core growth engine, though broader demand stayed subdued for most of the year across both beer and wine and spirits categories

IMF to cut global growth forecasts as Iran war triggers supply shock

[8:55 am] IMF Chief Kristalina Georgieva warns the world economy is ill-equipped to absorb the fallout from the US-Israeli war on Iran, with growth downgrades imminent and inflation risks mounting.

The IMF was on track to upgrade 2026 growth projections before the conflict, but will now downgrade them, with new forecasts due next week at the IMF and World Bank spring meetings in Washington

The war is delivering a "negative supply shock" by choking Gulf energy shipments, pushing prices up and forcing central banks to balance inflation control against the risk of strangling growth

Georgieva flagged that the world is responding to this shock with "depleted policy space" after Covid and the Ukraine war, with few governments having meaningfully reduced post-Covid debt

Beyond energy, fertiliser markets have been hit and the UN World Food Programme warns nearly 45 million more people could fall into acute food insecurity if the conflict does not end by mid-year

US PCE runs hot as consumer spending stalls

[8:54 am] February PCE data revealed sticky inflation and a faltering consumer, with the Iran war poised to make both dynamics worse in the months ahead.

Headline PCE rose 0.38% month-on-month vs. 0.32% ests and 2.8% year-on-year vs. 2.6% ests

Core PCE rose 0.37% month-on-month and 3.0% year-on-year, both in-line with consensus expectations

Real consumer spending rose just 0.1% in February after stagnating in January, with real disposable income falling 0.5%, the steepest decline in nearly a year

Goods prices drove the inflation beat, with recreational goods, clothing and energy all picking up, though services inflation excluding energy and housing rose just 0.2%, its smallest advance since September

Companies are beginning to pass on higher costs, with Delta Air Lines flagging further fare increases and the US Postal Service planning to lift prices by 8% on some packages, adding to the squeeze on household budgets

Fourth quarter GDP was revised down to 0.5% annualised growth, though pre-tax corporate profits rose 6%, the strongest quarterly gain in over three years

Iran ceasefire hangs by a thread as talks shift to Islamabad

[8:47 am] The US-Iran ceasefire is under serious strain, with disputes over its scope threatening to unravel the deal before formal peace negotiations have even begun.

Iran is accusing Israel of violating the ceasefire by continuing strikes on Hezbollah in Lebanon, though the US and Israel maintain Lebanon was never included in the deal's scope

Iranian media reported Tehran was suspending tanker traffic through the Strait of Hormuz and considering pulling out of the deal entirely, though the White House denied the strait had been closed

Peace talks brokered by Pakistan are scheduled for this weekend in Islamabad, with US VP Vance leading the American delegation, though uncertainty remains after Iran's ambassador deleted a post confirming the delegation's arrival schedule

Netanyahu has instructed his cabinet to begin direct negotiations with Lebanon, but notes there is "no ceasefire" in Lebanon and they will "continue to strike Hezbollah with force"

Source: BBC

Hormuz shipping traffic remains frozen despite US-Iran ceasefire

[8:44 am] Shipping through the Strait of Hormuz has barely recovered following a US-Iran ceasefire deal, with traffic still at near-standstill levels. Only one oil products tanker and five dry bulk carriers transited the strait in the past 24 hours, despite a two-week ceasefire between Iran and the US being in place.

BlackRock warns earnings forecasts face downside risk

[8:42 am] BlackRock's Helen Jewell cautions that elevated earnings expectations leave significant room for disappointment, particularly as Middle East tensions fuel inflation and reset rate cut hopes.

Consensus expects S&P 500 EPS to rise 16% in 2026, the strongest since 2021, but Jewell argues there is "a lot of headroom for earnings to come down"

Citigroup's US earnings momentum index turned negative last Friday, with downgrades outpacing upgrades by the most in nearly a year, an early signal of fading bullish sentiment

Consumer sector earnings forecasts are seen as difficult to justify given persistent inflation and elevated interest rates

Energy gains are likely to be offset by pressure on sectors like airlines, pointing to broadly flat aggregate earnings outcomes

Oil prices expected to remain sticky, with Jewell arguing markets are underestimating the inflationary impact, even if Middle East conflict were to de-escalate today

Source: Bloomberg

Good morning!

[8:34 am] ASX 200 futures are down 8 pts (-0.08%) as of 8:30 am AEST.

The overnight session in a nutshell:

US indices broadly higher, with the S&P 500 recording its seventh straight day of gains and the Dow returning to positive YTD territory

Every S&P 500 sector except for Energy and Healthcare finished higher

Software was a key underperformer, with the iShares Expanded Tech-Software ETF down 3.9% and broke below recent lows to trade at the lowest since Nov-23

Recent Anthropic updates around Claude Cowork and its new Mythos model are the likely suspects behind renewed pressure for software names

Only one oil products tanker has crossed the Strait of Hormuz since the ceasefire announcement, while Israel continues to "strike Hezbollah with force"