2025 will be a stinker for dividends, but these ASX companies could pay big fully franked specials

The dividend yield of the Australian share market is at lows not seen in a generation after accounting for the post-COVID dip.

Source: Shutterstock, Market Index

Mentioned

KEY POINTS

- The dividend yield of the S&P/ASX 200 is likely to be its lowest in 2025 when compared to typical dividend paying years since 2025 (i.e., accounting for the post COVID-19 dip)

- Many Australian companies have chosen to undertake share buybacks rather than distribute surplus cash directly back to shareholders as dividends

- Should investors who rely on dividend income be concerned by recent trends? The tide may be turning back towards higher dividend payments, suggests a major broker

3.6%. That’s Morgan Stanley’s forecast for the combined dividend yield of the S&P/ASX 200 in FY25. If that doesn’t sound like a great deal (you may wish to consider that current term deposit rates are topping 5%), you’re correct. The “12mf Dividend Yield” as Morgan Stanley calls it, is currently 2 standard deviations below its mean since 2000.

If you’re like me, and high school statistics was also about 2 standard deviations ago, this means that Aussie dividend yields have only been this low roughly 5% of the time over the last 25 years. This statistic would be even worse if not for the post-COVID period where many Australian companies understandably suspended their dividends for one or two halves.

Take that period out, and arguably the ASX 200 dividend yield is likely to be its lowest over the coming 12 months than at any other time in over a generation.

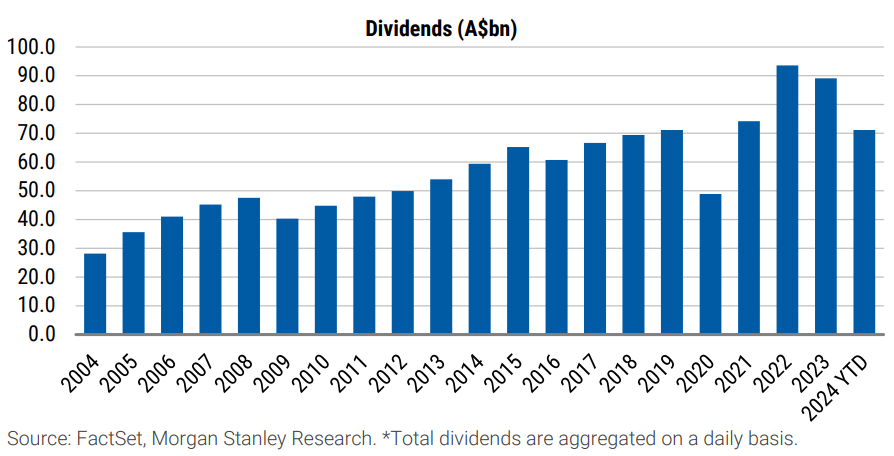

Exhibit 4: Dividends paid by constituents of the ASX 200 by calendar year*. Source: FactSet, Morgan Stanley Research. *Total dividends are aggregated on a daily basis. (Available from: “Frankly Speaking...Who Has The Most Credits?”, Morgan Stanley Research, 29 September 2024) (click here for full size image)

{kind=link}

Exhibit 9: ASX 200 Dividend Yield is at 2std below historical average 4.5%. Source: RIMES, IBES, Morgan Stanley Research. (Available from: “Frankly Speaking...Who Has The Most Credits?”, Morgan Stanley Research, 29 September 2024) (click here for full size image)

{kind=link}

The charts above tell the ASX 200 dividend story in pictures. Exhibit 4 shows ASX 200 companies have paid a lower value of dividends for a second year in a row this year, and Exhibit 6 shows how those dividends have translated into dividend yield.

It’s interesting to see how the two don’t always move in the same direction – which makes sense when you consider a dividend yield is a function of dividend and share price. A low dividend yield can be just as much a result of a higher share price as a lower dividend payout.

One thing is clear from Exhibit 9 – there is a steady downtrend in the 12mf Dividend Yield since 2022 (at least partly due to lower dividend payments), but adjusting for the COVID-19 blip, there’s arguably also a pervasive downtrend in place since 2012.

Special dividends: “the poor cousin”

Morgan Stanley suggests one reason for the general decline in the ASX 200 dividend yield is the growing preference of cashed up companies to use share buybacks, and not special dividends, to translate surplus cash to increased shareholder returns. “Special dividends in the past have been a poor cousin to buybacks as a preferred capital management tool”, the broker notes.

A share buyback occurs when a company uses its own cash to buy its own shares on the ASX. There are two main benefits of a share buyback for shareholders. The first stems from buyback shares being removed from circulation – resulting in the same dollar of future profit being spread across fewer remaining shares. This means a company's return per share typically increases after it conducts a buyback, and investors generally pay more in terms of share price for the higher return per share.

The second benefit comes down to basic demand and supply. Share buybacks create greater demand for the company’s shares, and all things being equal, greater demand should translate into a higher share price. Indeed, companies often cite the view that their shares are undervalued as a reason for conducting a buyback.

So it's clear that both buyback benefits translate into a higher share price. Also, because companies are generally choosing a buyback over either a higher regular dividend or the paying of a special dividend – they also translate into a lower dividend yield. This may not matter to some investors, because overall returns are usually roughly the same, but it might be critical to others who have a preference for fully franked dividends.

It's also worth pointing out at this stage that a major drawback of both share buybacks and dividends, is that each reduces the amount of cash available within a business to reinvest in future earnings growth. High dividend yields and/or buybacks can be a signal a company has few viable growth opportunities, management is effectively saying: "Here’s the cash – you go and find something better to do with it!"

Despite that last point, each of the Big 4 banks, Macquarie Group, AMP, Brambles, Cochlear, Computershare, Corporate Travel Management, Incitec Pivot, and Qantas, are just a few of the major ASX-listed companies currently conducting share buybacks.

The tide might be turning

The Australian share market has averaged a 4.4% p.a. dividend yield since 2000, and its probably fair to say that many Aussie investors have come to rely on this solid and reliable return. When you add in franking credits, the deal has been even sweeter. But, if you’re the type of investor who relies on dividends for your income stream, then the data in this article is likely to be very concerning.

Morgan Stanley notes that one upshot of all of the recent buybacks is that Aussie blue-chips are stacking up unused franking credits. These cannot be distributed via on-market share buybacks, and as Morgan Stanley points out, recent regulatory changes have excluded the distribution of franking credits via off market buybacks as well. The result is that these potentially lucrative benefits to many Aussie shareholders are effectively going begging.

Morgan Stanley notes that as a growing proportion of Australians move into retirement via demographic changes, “there is a growing shareholder base that looks at after tax returns and will value franking balances incrementally higher as a result”.

So the tide is shifting. What investors should be watching for now is how the capital management narrative will be crafted going forward. A well intended (but often less active) on market buy back commitment combined with highlighted capacity to pay out above ordinary dividend parameters (fully franked) for an extended period of time could become a more powerful signal of business model confidence and shareholder focus.

––Morgan Stanley

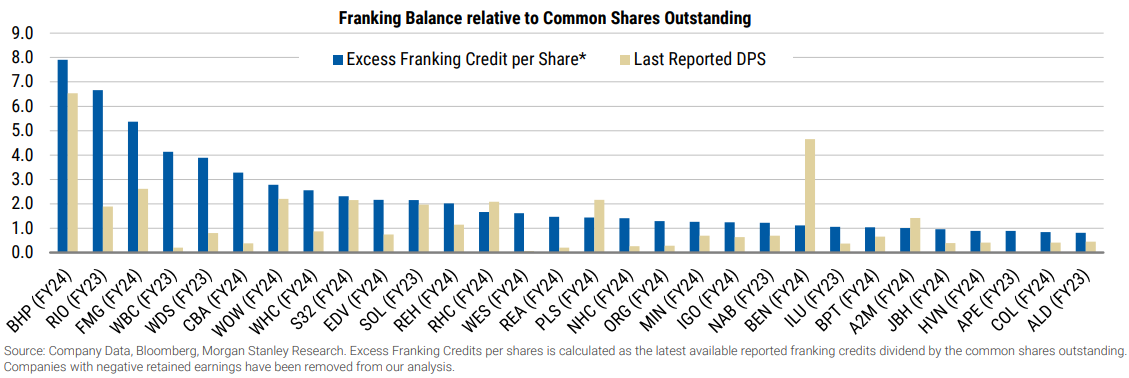

The companies Morgan Stanley thinks investors should watch closely for franking credit friendly capital management initiatives like special dividends are shown in the table below.

Exhibit 3: Who has the ability to distribute excess franking credits to shareholders? Our chart identifies companies that have excess franking credits (per share) available relative to last paid dividends. Source: Company Data, Bloomberg, Morgan Stanley Research. Excess Franking Credits per shares is calculated as the latest available reported franking credits dividend by the common shares outstanding. Companies with negative retained earnings have been removed from our analysis. (Available from: “Frankly Speaking...Who Has The Most Credits?”, Morgan Stanley Research, 29 September 2024) (click here for full size image)

{kind=link}

There are plenty of usual suspects here with respect to ASX dividend paying royalty. The major iron ore miners BHP Group (ASX: BHP), Rio Tinto (ASX: RIO), and Fortescue (ASX: FMG) top the list, and they’re followed by Westpac (ASX: WBC), Woodside Energy (ASX: WDS), Commonwealth Bank (ASX: CBA), Woolworths (ASX: WOW), New Hope Corporation (ASX: NHC), South32 (ASX: S32), Washington H Soul Pattinson & Company (ASX: SOL) to make up the top 10.

Sector by sector back up plan

Even if the companies in the above table don’t end up paying out big fully franked special dividends, there remain a few sectors where investors may still find dividend yields in excess of 4%.

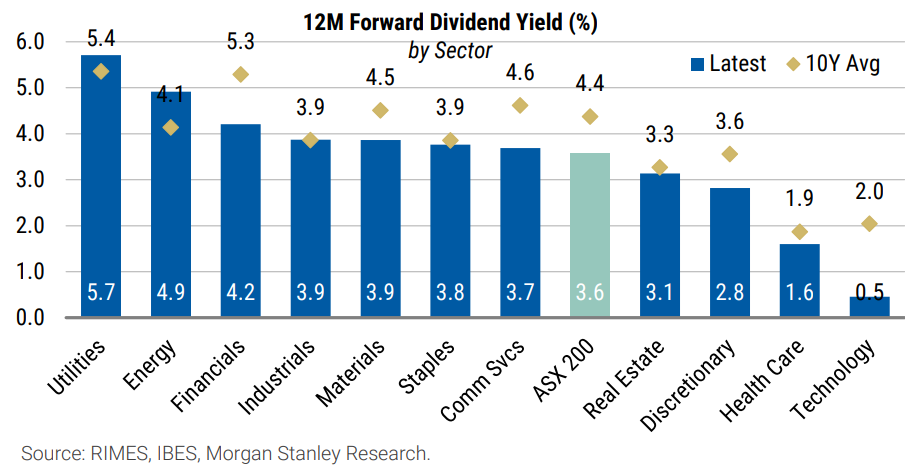

Exhibit 8: Historical Yield Comparison - Sectors relative to 10Y averages. Source: RIMES, IBES, Morgan Stanley Research. (Available from: “Frankly Speaking...Who Has The Most Credits?”, Morgan Stanley Research, 29 September 2024) (click here for full size image)

{kind=link}

According to Morgan Stanley forecasts, Utilities (XUJ) are your best bet. This sector is likely to deliver an average 5.7% dividend yield over the next 12 months, slightly better than its 5.4% 10-year average. Next is Energy (XEJ) with a forecast 4.9% yield, and then comes Financials (XFJ) with a forecast 4.2% yield.

On Financials, it’s interesting to note with this sector the impact of recent large buybacks. At 4.9%, the XFJ’s next 12 months dividend yield is substantially below its 10-year average of 5.3%.

Industrials (XNJ) (3.9%), Materials (XMJ) (3.9%), Consumer Staples (XSJ) (3.8%), and Communication Services (XTJ) (3.7%) are each likely to deliver better than benchmark yields over the next 12 months.

The above table doesn’t imply that sectors like Information Technology (XIJ) with a relatively low 0.5% next 12 month dividend yield represent a bad investment, simply that companies in that sector are less likely to pay out big dividends. Technology companies are traditionally higher growth businesses that prefer to reinvest surplus cash back into their businesses to drive increased earnings growth. This generally translates into a higher share price.

It's horses for courses, and some investors prefer growth while others prefer fully franked dividends. You can, of course, go for a mix – that’s up to you – but hopefully this article has helped highlight some of the challenges that potentially lie ahead for Aussie dividend investors. At the very least, I trust it's also highlighted which stocks and sectors are likely to continue to deliver the best fully franked dividend yields over the next 12 months.