Why UBS says it's too early to buy the ASX 200 dip

UBS warns the ASX 200's seven-day slide isn't the bottom, with broad earnings downgrades set to dominate headlines in the weeks ahead.

Source: Shutterstock

KEY POINTS

- UBS believes the ASX 200's earnings upgrade cycle has peaked and is set to turn negative, driven by weaker GDP, higher oil prices and stickier inflation

- History shows share prices typically bottom roughly halfway through an earnings downgrade cycle, suggesting it's too early to buy the recent weakness

- UBS has flagged 25 stocks including Temple & Webster, Harvey Norman, Flight Centre and Brambles where prices have fallen more than 10% but earnings forecasts have barely moved

It's been a very rough week for Australian equities. The S&P/ASX 200 is on a seven-day losing streak, down 3.0% and now slightly down for the year.

While the weakness might tempt bargain hunters, UBS reckons investors are looking through macro, inflation and earnings risks too early.

UBS economists have cut GDP forecasts and lifted inflation expectations across the board since the Middle East conflict began in late February, a stagflationary mix that's already feeding into earnings revisions. The ASX 200's 12-month forward earnings estimates have flipped from clearly positive territory into negative, and now heading lower, with energy the only sector still contributing meaningful upgrades.

The analysts believe a combination of weaker GDP, elevated oil prices and stickier inflation could deliver "broad-based earnings downgrades that will dominate headlines over coming weeks."

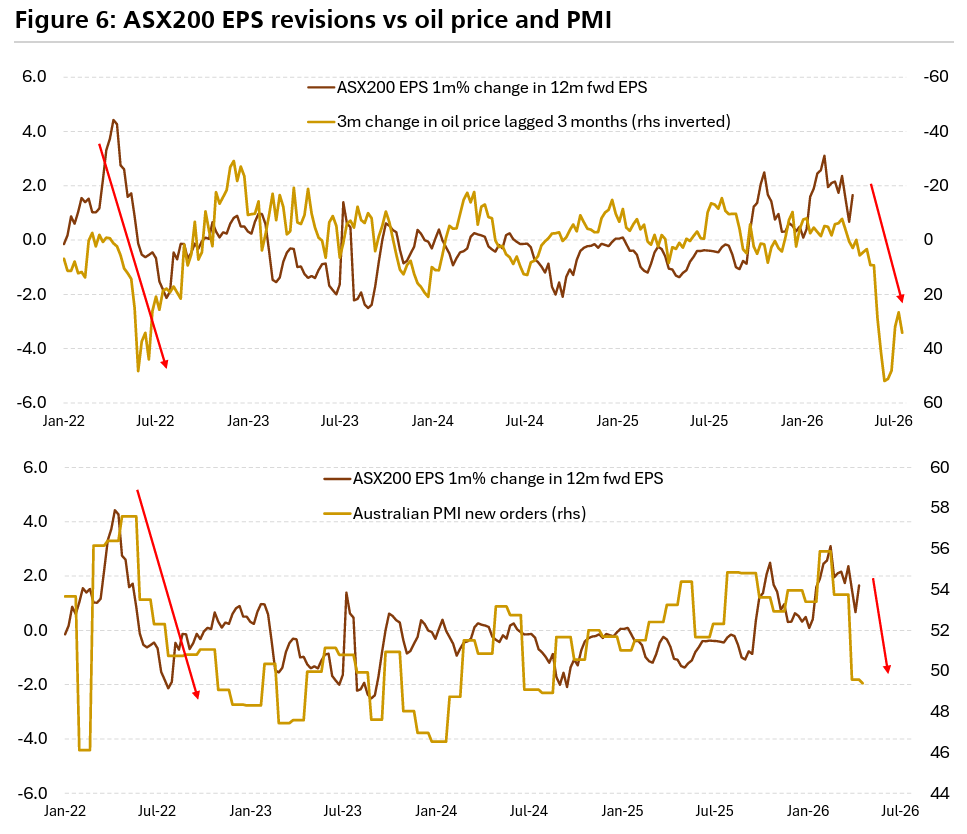

Earnings upgrade cycle set to swing to downgrades

Higher oil prices and softening PMIs have historically driven downward revisions for ASX 200 earnings, and UBS sees both conditions in play now.

Source: UBS

Recent downgrade cycles have played out over very different timeframes:

GFC cycle (2008-09): downgrades lasted around 18 months for most sectors, with EPS falls of 17% to 63% and share price falls of 28% to 78%

COVID cycle (early 2020): just 5 to 9 months, with EPS down 20% to 54% and prices down 25% to 49%

In both cycles, share prices bottomed roughly halfway through the EPS downgrade period. The takeaway is that share prices tend to bottom well before earnings, hence the often-quoted line that the stock market tends to bottom two to three quarters before the economy.

The 'no news is bad news' screen

UBS has screened for stocks where the share price has dropped more than 10% since the conflict began but earnings expectations have barely budged.

Names on the screen include: Temple & Webster, ARB Corp, Fletcher Building, Super Retail, Harvey Norman, Nick Scali, Amcor, Stockland, Flight Centre, PEXA, Ansell, ALS, Mirvac, Orica, SGH, Brambles, Reece, Downer, Auckland International Airport, Seek, Domino's, Endeavour, Ingenia, Monadelphous and Light & Wonder.

Whether that's an opportunity list or a warning depends on your view of the cycle, but UBS sits firmly in the warning camp.

Announcements have hurt, even after prices had already fallen

The analysts tracked 21 announcements referencing the conflict between 10 March and 24 April. On average, those stocks had already fallen roughly 8% heading into the update, then dropped another 4% on the day.

Here's the full list of updates:

Air NZ (10-Mar): Suspended guidance, shares down 1.1%

Orica (10-Mar): Trading update noted no immediate constraints related to Middle East conflict, shares down 3.4%

Ridley Corp (10-Mar): Investor day noted earnings not expected to be materially impacted by Middle East developments, shares up 0.7%

Orora (9-Apr): Trading update with lower EBIT guidance, shares down 18.0%

Transurban (9-Apr): Q3 traffic update flagged fuel costs, macro uncertainty and geopolitical concerns, shares up 0.2%

a2 Milk (13-Apr): FY26 NPAT guide lowered to "similar to down" with margins impacted by higher air freight costs, shares down 13.0%

Cleanaway (14-Apr): Lowered guidance, shares down 2.6%

Qantas (14-Apr): Update on FY26 outlook amid Middle East conflict, shares down 0.3%

Westpac (14-Apr): Q2 trading update mentioned geopolitical uncertainty, shares down 2.6%

Nufarm (15-Apr): H1 trading update noted supply chains are currently operating largely normally, shares up 11.3%

Virgin Australia (15-Apr): Flagged increase in fuel costs for 2H26 of ~A$30-40m vs prior expectations, shares up 7.2%

Fletcher Build (16-Apr): Q3 sales update noted Middle East impact can't yet be ascertained, shares down 2.4%

NAB (20-Apr): Increased impairment charges for sectors most exposed to geopolitical risks, shares down 3.6%

Qube (20-Apr): Trading update lowered guidance, shares flat

Worley (20-Apr): Update on Middle East impacts, shares down 5.8%

Atlas Arteria (21-Apr): Q1 trading update noted no major effect of rising fuel prices on traffic, shares down 0.9%

Cochlear (22-Apr): Trading update with FY guidance downgrade, shares down 40.7%

EBOS (22-Apr): Lowered guidance, shares down 3.4%

Iress (23-Apr): AGM flagged geopolitics and macro risks, guiding FY26 revenues towards bottom of range, shares down 1.1%

EVT Limited (24-Apr): FY26 update warned of emerging demand weakness, shares down 7.3%

Judo Capital (24-Apr): Q3 update reaffirmed guidance at low end with top-up provision in response to economic conditions, shares up 1.4%

UBS equity strategist Richard Schellbach concludes that "not all the bad news was in the price," supporting the view that it's too early to confidently buy into earnings weakness.

Valuations still leave little margin for error

The ASX 200 is trading around 19x FY26 earnings estimates, with EPS growth of 12.8% largely driven by the resource sector.

Beneath the index level, sector valuations differ significantly:

Energy: 19.1x FY26 EPS, but earnings forecast to fall 15% before rebounding 49.6% in FY27

Materials: 16.4x, with EPS growth of 32% expected in FY26

Health Care: 18.4x after a ~20% tumble in the last three months

Technology: 79.2x, the most expensive sector by a wide margin

Discretionary: 23x, after falling ~13% in the last three months

The bottom line

UBS' cautious view is based on three key assumptions and takeaways.

The earnings cycle has peaked and is starting to turn negative

History shows share prices typically bottom halfway through these cycles rather than at the start

Announcements over the past six weeks suggest the market is still actively repricing risk rather than having already priced it in

That doesn't mean every fallen stock is a value trap, but the path of least resistance for earnings is towards the downside amid weakening macro signals.