Why rising bond yields are a tax on every asset you own — and what it means for the ASX right now

Stocks and commodities shrugged off rate risk — until the bond market stopped letting them. Here's why that changes everything.

Source: Shutterstock

KEY POINTS

- Stocks and commodities have rallied hard since the worst Middle East conflict fears receded, but a simmering pot of inflation and slowing growth has been boiling beneath the surface — and last week's bond sell-off has forced investors to confront it.

- Government bond yields have surged in the US, Europe, Asia and here in Australia — the broadest global repricing of risk-free money in years, driven by energy-shock inflation and a Federal Reserve that may now be behind the curve.

- This article explains why rising yields punishes risky assets like shares, drives a stronger US dollar which hammers commodity prices, and why the bond market — not the share market — is the real price-setter for every financial asset you own.

Cast your mind back to the initial shock of the Middle East conflict. Markets lurched, volatility spiked, and investors braced for the worst. Then the immediate fears faded, and equities and commodities staged a sharp recovery. That's what markets do when a threat fails to deliver on its initial shock value. Stocks went back to doing what they were doing before: going up. Particularly for US stocks which have made a series of record highs.

But the conflict didn't disappear. It lit a fire under something that was already simmering — inflation. The rising energy prices caused by the conflict in the Middle East feed inflation, and inflation, left unaddressed, forces central banks to raise interest rates.

Higher interest rates change the price of everything. Stock and commodity markets, it turns out, chose not to think too hard about that chain of events. The bond market did.

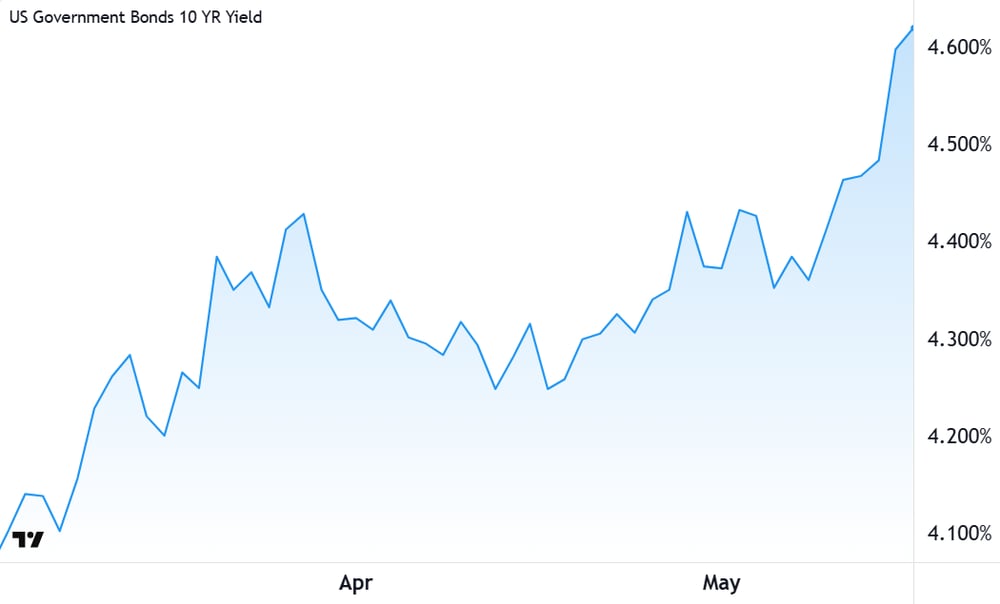

Last week, bond markets around the world sold off sharply — not just in the United States, where the 10-year Treasury yield surged to its highest level since early 2025, and the 30-year broke above 5.1% for the first time since 2007, but across the developed world. Japan's 30-year yield hit 4% for the first time since those bonds were issued in 1999. UK 10-year gilts crossed 5.17%, their highest since 2008. Australian bond yields also pushed sharply higher.

This was a global repricing of the price of risk-free money. And when the price of risk-free money rises, the price of everything else adjusts accordingly.

This article is about why that happens — and why investors who aren't watching the bond market are navigating the ASX with the most important warning signal turned off.

The price of money just went up everywhere ⚠️

It is easy to read last week's bond market sell-off as something that happened in a market where most investors have no direct exposure. It doesn’t matter for the average Aussie investor.

But, as the old saying goes, when the US sneezes, the rest of the world, including Australia, catches the cold. The Federal Reserve is the world's most watched central bank, and the 10-year Treasury yield is the most watched rate in global finance. Last week’s sell off centered on the narrative that US inflation data was running hotter than expected — April's Consumer Price Index came in at 3.8% annually, and the Producer Price Index surged to 6.0% p.a., both driven largely by energy prices.

US 10-year Treasury Bond yield

But it wasn't just America. The 30-year UK gilt hit its highest level since 1998. Japan's yields — anchored near zero for decades — are now at levels not seen since the late 1990s. German bund yields climbed. Australian government bond yields rose in step.

The significance of the global nature of this repricing cannot be overstated. When yields rise everywhere simultaneously, there is no refuge in another currency's bond market. The global price of risk-free money has moved — and every other asset must now reset against a new baseline.

What rising yields actually mean for stock prices

Here is where it helps to understand the mechanics of how all asset prices are set in financial markets.

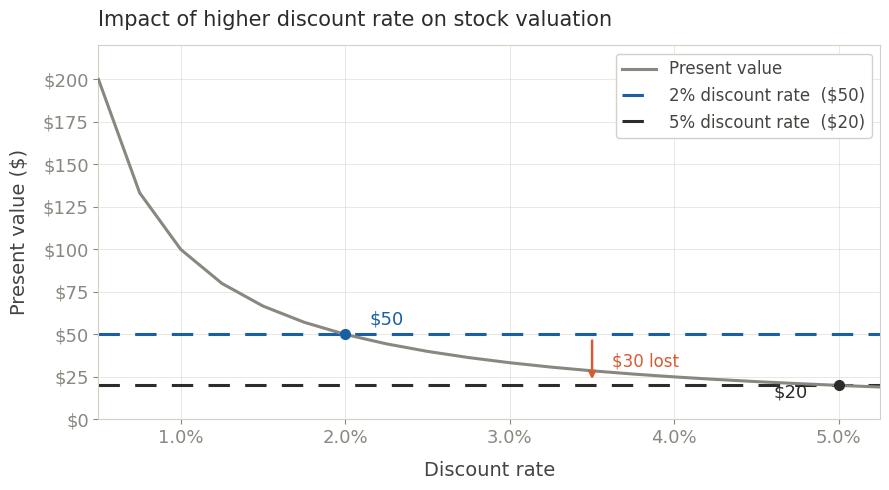

Every asset, including the shares in your portfolio, has a value. But that value is not the price you see on your broking platform today. The fundamental value of a stock is the sum of all the cash flows it is expected to generate in the future, discounted back to what those future dollars are worth in today's terms. This is the discounted cash flow model, and the discount rate at the heart of it is tied directly to risk-free yields on government bonds.

Think of it this way: if a government bond pays you 2%, a risky stock needs to offer you a meaningfully higher return to justify the extra risk of owning it. But if that bond now pays 5%, the hurdle rises. The future cash flows from your stock — ten, fifteen, twenty years out — are now worth less in today's money.

The arithmetic for a stock expected to generate a hypothetical $1 of earnings every year into the future is telling:

At a 2% discount rate — roughly what government bonds were paying not long ago — that stream of future dollars might be worth around $50 in today's money.

At a 5% discount rate — closer to where long dated US Treasuries now sit — the same stream of future earnings is going to be worth closer to $20.

Impact of higher discount rate on stock valuation

Same business. Same earnings. Yet $30 of value — gone. Not because anything changed fundamentally at the company, but because risk-free money got more expensive.

This compression hits hardest for what markets call "long-duration" assets — stocks where the bulk of the value is tied up in earnings expected many years from now. Technology stocks, high-growth small caps, and any business priced on the expectation of future profits rather than today's earnings are acutely exposed.

A 1% rise in the discount rate is far more damaging to a business valued on cash flows in 2040 than one generating strong profits today. Short-duration stocks — those with solid, near-term earnings already being banked — hold up comparatively better. But in a broad yield spike, few sectors escape entirely.

Commodity stocks have borne the brunt — and here's why

Commodity stocks appear to have borne the heaviest selling as last week's bond move worked through markets. Gold fell sharply on Friday, continuing to decline in Asian trade today. On the London Metal Exchange, Aluminium fell 3.5%, Copper fell 3.1%, and Nickel fell 2.8%. The benchmark COMEX Copper futures contract extended those losses by a further 0.9% in Asian trade.

Some of this reflects the same discount rate logic discussed above. But there are two additional mechanisms specific to commodities that amplify the impact of rising US yields.

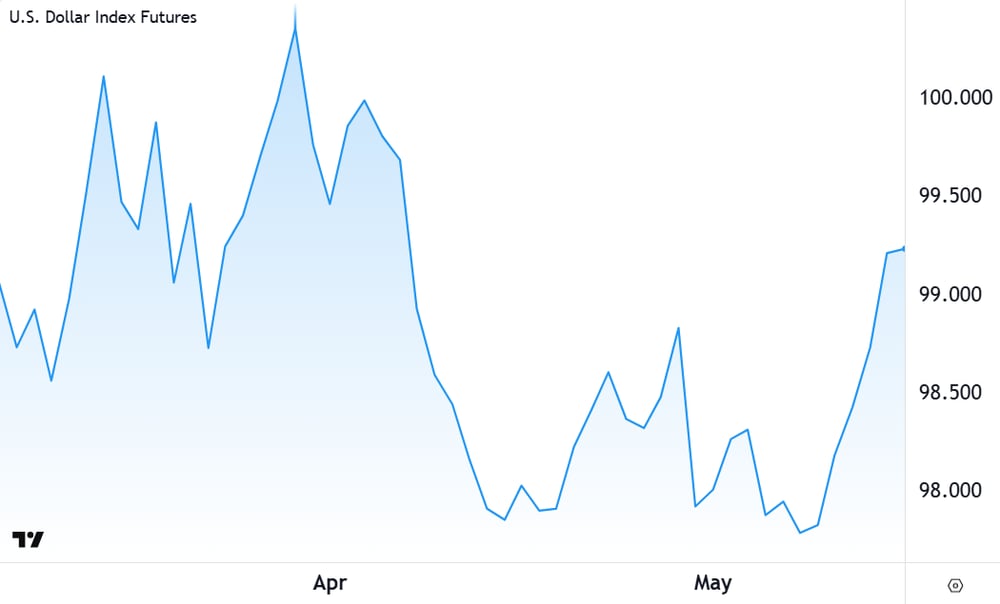

The first is the US dollar. Government bond yields and the currency of that government's country tend to move together — higher US yields attract global capital into US dollar assets, which bids up the greenback. And commodities, almost universally, are priced in US dollars on global exchanges. When the dollar strengthens, the same physical quantity of copper or aluminium costs more in US dollar terms — which means demand from buyers operating in other currencies softens, and prices fall to compensate.

It's not that the world suddenly needs less copper; it's that the world's copper buyers are paying in euros, yen, and Australian dollars that have just become less valuable relative to the US dollar. Copper just became more expensive to them, so they may demand less.

US Dollar Index chart

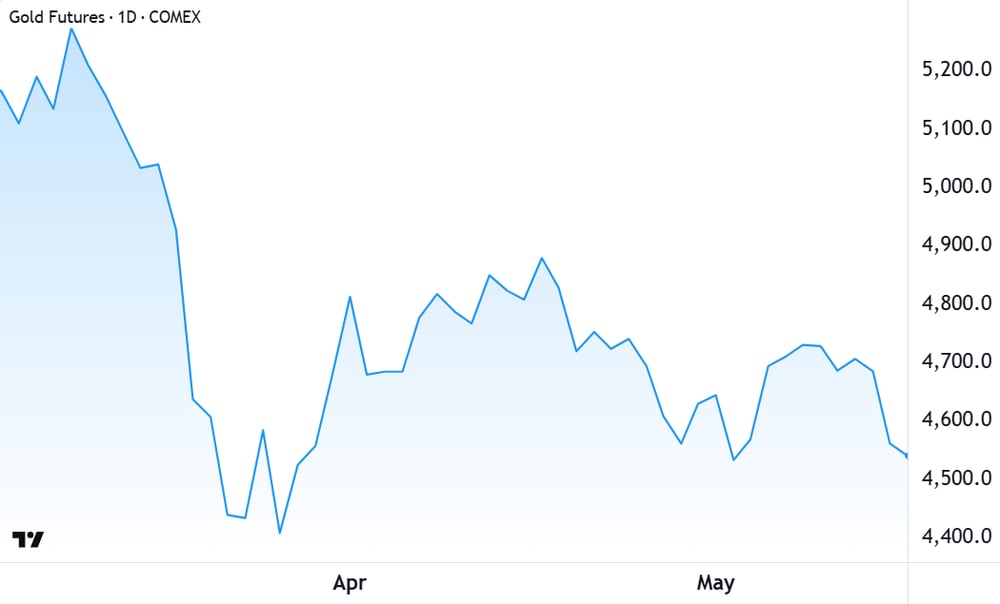

The second mechanism is specific to gold — and it is the opportunity cost trade-off that makes gold particularly vulnerable in a rising rate environment. Gold pays no yield. It produces no earnings, no dividends, no interest. Its entire investment case rests on capital appreciation and its role as a store of value and hedge against currency debasement.

When risk-free government bonds were paying next to nothing, owning gold for nix in yield was no sacrifice at all — you weren't giving up much by forgoing the interest. But when a 30-year US Treasury now pays above 5% annually, the opportunity cost of holding gold becomes very real. Every year you hold gold instead of Treasuries, you are forgoing a 5% yield on a risk-free instrument. That calculus has changed — and gold's price has responded accordingly, pulling back sharply from January's extraordinary highs near US$5,589 per ounce.

Benchmark COMEX gold futures chart

Bond proxy sectors under pressure

Commodity stocks aren't alone in their vulnerability. There are entire sectors of the share market that trade less like growth businesses and more like fixed-income instruments — because their primary investment appeal is the reliable income they generate.

Utilities, real estate investment trusts (REITs), and higher-yielding financial stocks — particularly banks that have been bought for their dividend yields — all sit in this category. When risk-free bonds yield 2%, a utility paying a 5% dividend is genuinely attractive. When risk-free bonds yield 5%, that same utility's income stream offers far less relative compensation for the additional risks of equity ownership: business risk, regulatory risk, weather risk, and all the rest. The relative appeal shrinks — and so does the price investors are willing to pay.

The mechanism is identical to the discount rate compression for growth stocks; it just manifests differently. Where growth stocks lose value because their distant future earnings are worth less today, bond proxy stocks lose value because their present income streams become less compelling against what government bonds now offer for free.

For ASX investors, this has direct implications for a number of the market's most widely held names. Infrastructure stocks, listed property, and the major banks — all pillars of the typical Australian retail investor's portfolio — face headwinds when yields rise meaningfully and stay there.

Why the bond market is the key to every other market

There is a tendency among equity investors — and, frankly, among much of the financial media — to treat the bond market as a separate, technical, and somewhat tedious corner of finance. Something for fund managers and Treasury departments, not something the typical ASX investor needs to follow closely.

That misses the point entirely.

The bond market sets the price of risk-free money. And the price of risk-free money is the foundation on which every other asset price is built — every stock, every property, every commodity, every private business valuation. When that foundation shifts, everything built on top of it moves too. The bond market doesn't comment on what other markets are doing; it determines what other markets can do.

Last week's sell-off is a reminder of that architecture. Stocks and commodities had been rising on the assumption that the inflation and interest rate backdrop would remain manageable — or at least that central banks would continue prioritising growth over price stability. The bond market has shown otherwise. And the bond market is usually right.