Why REA looks cheap after a brutal selloff but AI risk remains

REA delivered a small 1H26 miss, but guidance for a 1% to 3% drop in national Buy listings kept the forward view under the microscope.

Source: iStock

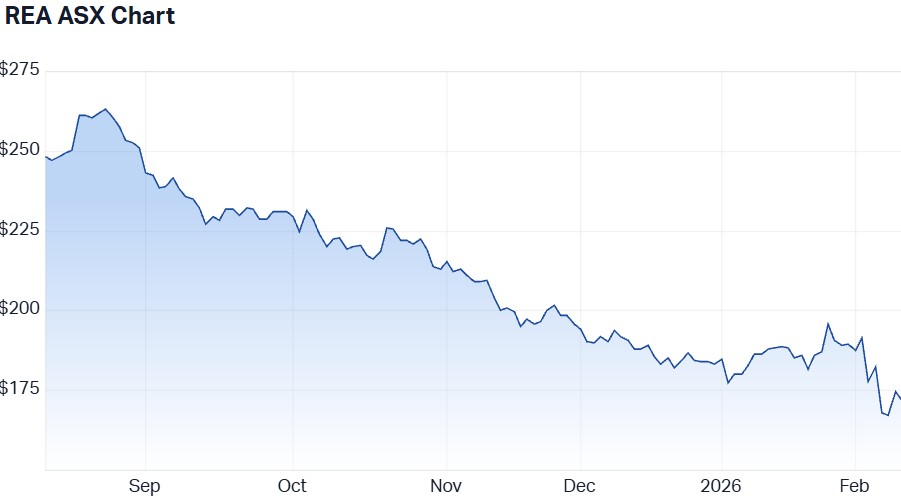

REA suffered a historic selloff last Friday, down as much as -17% after announcing a slightly weaker-than-expected first-half FY26 announcement. Despite opening sharply lower, a flurry of bidding activity helped the decline to -7.8% by market close.

The stock has climbed slightly higher this week, but still down by about -5% since the 1H26 results announcement. Below, we take a look at the key numbers from the result and what will drive the stock moving forward.

Key numbers from 1H FY26:

Revenue up 5% to $916m vs $927m ests (1.2% miss)

EBITDA up 6% to $569m vs $573m ests (0.7% miss)

Net profit from core operations up 9% to $341m vs $345m ests (1.2% miss)

EPS up 9% to $2.58 vs $2.61 ests (1.1% miss)

Interim dividend up 13% to $1.24 per share vs $1.47 ests (15.6% miss)

On market buyback announced of up to $200m

FY26 national new Buy listings now expected to fall 1% to 3% vs prior guidance for flat, with management citing larger than expected declines in Perth and Brisbane and January listings down 8% year on year

FY26 Buy yield growth is guided at 12-14%, in-line with market expectations, with Macquarie citing listing price and higher penetration of Audience Maximiser and Luxe as key supports

What analysts are thinking

Brokers are broadly constructive on medium term earnings, but targets have come down as listing volumes soften and AI uncertainty re-rating catalysts unclear. The miss was marginal, however the listings reset has increased sensitivity to volume trends and any signs of pricing pressure.

Here what analysts had to say after the result:

RBC maintained Sector Perform and cut its target to $200 from $225, leaning into the view the listings backdrop is deteriorating and competitive risks remain live.

JPMorgan maintained Overweight and trimmed its target to $215 from $225, pointing to REA’s AI rollout and the $200m buyback as supports, while keeping the spotlight on yield resilience.

Macquarie maintained Neutral and lowered its target to $200 from $210, saying the medium term earnings profile remains solid but valuation is still in flux.

Macquarie noted REA is trading around 32x, 12 month forward P/E, below the past 12 month average near 44x and closer to pre-COVID levels around 35x, but expects limited near term re-rating catalysts without clearer evidence on AI monetisation and volume stabilisation.

It also cut its FY26 to FY28 EPS forecasts by about 3%, 2% and 1%, on softer listing volume assumptions.

What to watch next

Macquarie added rapid AI developments are driving debate over structural change in online real estate classifieds, keeping it cautious on valuation discovery and near term re-rating catalysts until it is clearer whether AI is a net positive for classifieds monetisation.

That uncertainty is landing amid a broader software selloff, with headlines centred on AI disruption risk and outsized hyperscaler capex expectations.