What the hell just happened to CBA?

CBA crashed 10.4% in its worst session since listing in 1992, as a soft Q3 result collided with sweeping Budget tax reforms.

Mentioned

KEY POINTS

- CBA closed down 10.4% at $153.67, marking its worst single-day decline since listing in 1991 and surpassing routs seen during the GFC, dot-com bust, and pandemic.

- Q3 cash NPAT came in ~$2.7 billion, 2% below Citi's forecast, with personal loan arrears over 90 days hitting 1.71%, the highest reading since the pandemic.

- Budget reforms scrapping negative gearing on established property and the 50% CGT discount from 1 July 2027 hit CBA hardest, as it holds Australia's largest investor loan book.

It doesn't seem possible for the words Commonwealth Bank (ASX: CBA) and "down 10%" to fit in one sentence, but they just did.

CBA recorded its worst session in the 34 years that it's been listed, narrowly eclipsing the one-day routs of the pandemic, GFC and dot-com bust. The stock opened 5.0% lower on Wednesday and spent the whole day trending lower, closing the session down 10.4% to $153.67.

Q3 earnings soft

CBA reported its Q3 result this morning, where cash NPAT was 2% below Citi's forecast, largely on a provisioning top-up to reflect heightened macro risks. Personal loan 90-day arrears also hit 1.71%, the highest reading since before the pandemic.

The key numbers from the Q3 result include:

Unaudited cash NPAT of ~$2.7bn, down 1% on 1H26 quarterly average and up 4% on the prior comparative quarter

Operating income flat in the quarter, with lending and deposit volume growth offsetting two fewer days

Underlying NIM broadly stable excluding non-recurring tailwinds

Loan impairment expense of $316m, including a $200m top-up to forward-looking collective provisions reflecting heightened uncertainty

Home loan and credit card arrears "increased modestly" (6bps and 2bps respectively) on seasonality

Budget reforms

Tuesday night's 2026-27 Budget contained the most significant tax overhaul in 26 years, and CBA is the most structurally exposed name to it. These are the two that matter most:

Negative gearing on established residential property will be scrapped from 1 July 2027 for properties purchased after 12 May 2026. Existing investors are grandfathered, but anyone affected can no longer offset rental losses against salary or other personal income. Losses can only be used against residential rental income or future capital gains.

The 50% CGT discount will also be replaced from 1 July 2027 with cost base indexation plus a 30% minimum tax rate on capital gains for individuals, trusts and partnerships.

So why does this hit CBA harder than its peers?

Capital Brief cited Jarden's Matthew Wilson, who expects the changes to cut housing credit growth by 25% as the core investor incentive disappears. CBA carries the country's largest investor loan book, leaving it the most exposed.

Wilson says investors have been a lucrative slice of home loan growth, with interest-only loans carrying wider spreads, typically better asset quality, and therefore higher return on equity.

CBA's own economics team flags a subtle "lock-in effect" from the grandfathering. Existing investors now have a stronger reason to hold rather than sell, which translates to lower turnover, less refinancing flow and weaker new lending volumes.

Put it all together

CBA was trading at a price-to-earnings ratio of 28x despite lacklustre growth, a dividend yield of just ~3% and a valuation well above peers sitting in the high teens.

A softer-than-expected quarter, rising arrears and a structural hit to a high-margin slice of the most-exposed bank's business proved quite overbearing for what is the world's most expensive banking stock.

Today's price action showed how badly things compounded. The market's second largest company opened 5% lower and finished the session down 10%, with no bounce in sight.

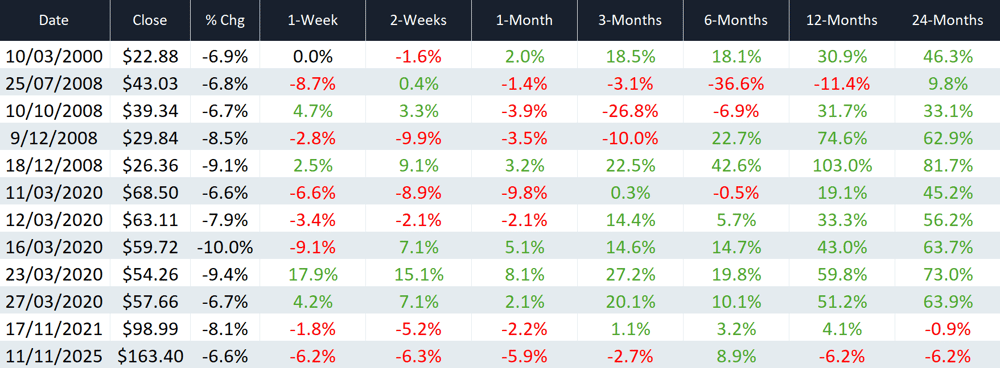

The worst session on record

Here's a look at CBA's worst one-day sessions since 1992.

Date | Close | % Chg |

|---|---|---|

13/05/2026 | $153.19 | -10.71% |

16/03/2020 | $59.72 | -10.01% |

23/03/2020 | $54.26 | -9.43% |

18/12/2008 | $26.36 | -9.09% |

9/12/2008 | $29.84 | -8.54% |

17/11/2021 | $98.99 | -8.07% |

12/03/2020 | $63.11 | -7.87% |

10/03/2000 | $22.88 | -6.88% |

25/07/2008 | $43.03 | -6.77% |

10/10/2008 | $39.34 | -6.72% |

Source: Market Index

Food for thought

This is a fairly unprecedented selloff as the vast majority of historical moves all come off the back of a major shock to the global economy, namely the dotcom bubble, GFC and pandemic. Most of those large one-day declines turned out to be reasonably attractive medium-term entry points.

How CBA performed after a major one-day selloff | Source: Author's own calculations

Only one entry on the list sits outside of an economic implosion, 17 November 2021. That day, CBA reported its 1Q22 trading update and flagged "considerably lower" net interest margins as customers shifted into lower margin fixed-rate loans.

The backdrop was the tail end of the COVID ultra-low rate era, when borrowers piled into sub-2% fixed-rate mortgages. By late 2021, fixed-rate loans had ballooned from a historical share of around 15% of new flow to roughly 40-45% of CBA's new originations. At the time, CBA was trading on 18x versus the low-teens multiples of the other Big Four. Forward returns from that point were dicey at best, and the global rate hike cycle kicked in shortly after.

The bottom line

CBA has suffered a rare one-day selloff and it's difficult to tell how much of it was the Q3 result and how much was the budget reforms.

The recent updates from ANZ (3 May), NAB (4 May) and Westpac (6 May) were all relatively soft – ANZ flagged underwhelming revenue trends, Westpac reported strong loan volume growth offset by margin compression and NAB's revenues missed on lower deposit balances. CBA's soft Q3 shouldn't have come as a big surprise, given this read through.

What's different this time is the budget overlay, where negative gearing and CGT changes are structural, not cyclical. At the same time, mining heavyweights like BHP and Rio Tinto have soared to fresh all-time highs, potentially driving a rotation from banks into miners.

That doesn't mean the stock can't recover from here, but it's fair to say that the odds are stacked against CBA.