Fuel costs, Cochlear and inflation

Hi there,

What a heavy week for markets – the ASX was in a world of its own, weighed by more downbeat bank announcements, healthcare weakness and a pullback for tech stocks.

The S&P/ASX Financials Index managed to snap a nine-day losing streak on Friday – where the sector was hit by a soft trading update from Westpac (last week), unexpectedly weak margins from Bank of Queensland's half-year result and higher provisions for ANZ and Judo – as they set aside more funds to cover potential losses from fuel-sensitive sectors. Not a good look for the market's largest (and quite expensive) sector.

A busy week on the mining and macro front, so let's dive into the highlights.

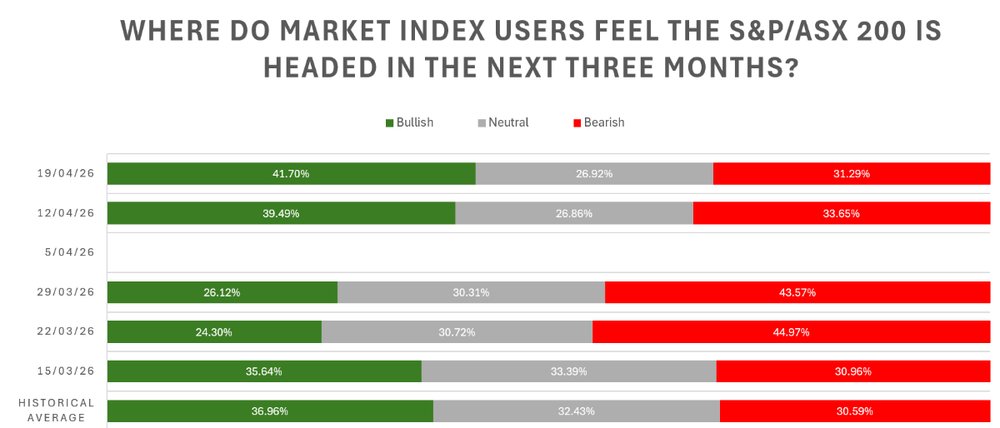

Investor sentiment survey

What miners are saying about the fuel crisis

A lot of mining quarterlies hit the market this week. Besides the usual updates about production, AISC and guidance – every company had their bit to say about the fuel crisis.

PLS Group (24-Apr) – “Diesel is a small component of the operating cost base under normal supply circumstances, representing approximately 4-5% of total production cash costs in the March Quarter. PLS does not foresee any immediate supply constraints for other key inputs, including explosives and processing reagents …”

Black Cat Syndicate (23-Apr) – “Despite unprecedented fuel price increases, fuel costs had a relatively minor impact, increasing from 6% of total costs in January, to 8% in March. A new long-term bulk fuel supply agreement was executed. Together with Lakewood’s grid-connected power, the Group is not experiencing any fuel supply constraints, supporting uninterrupted operations.”

Resolute Mining (23-Apr) – “There is a potential for increased AISC due to rising fuel prices, which could impact our operational costs in the coming quarters. At this stage, we are proactively managing these risks and, where possible, minimising any impacts.”

Perseus (23-Apr) – “There were no operational disruptions to the Group’s activities during Q3 FY26, and fuel supply is expected to be sufficient to support operations.”

Elevra (23-Apr) – "Elevra has only limited exposure to liquid fuel prices and reduced fuel availability, with diesel accounting for only ~5% of site operating costs and renewable hydroelectricity utilised in the process plant.”

Northern Star (22-Apr) – “On 20 January 2026, the Company revised its FY26 Group AISC guidance to A$2,600-2,800/oz, up from A$2,300-2,700/oz and maintains this revised forecast despite lower gold sales and higher diesel prices expected in the June quarter.”

Vault Minerals (22-Apr) – “No disruption to diesel supply to operations, with supply contract in place with a global oil major. Vault continues to monitor the situation with planning in place to leverage high grade underground mines and the large stockpile position across all operations should the situation deteriorate.”

Lynas (21-Apr) – “To date, we have not experienced any material disruptions due to the current global fuel supply situation. However, price increases are expected for a number of materials. It is difficult to forecast the magnitude and duration of these price increases.”

Rio Tinto (21-Apr) - “Other business inputs (such as jet fuel, caustic soda and others): prices rose, however, there was no disruption to our business. On sulphuric acid, we are a net long producer globally via our Kennecott smelter.”

Genesis Minerals (16-Apr) – “Genesis’ diesel is sourced from major importers under long term supply contracts. FY26 cost guidance was based on a diesel price of A$1.10 per litre (net of rebate), representing ~4% of total costs.”

If the commentary above is any guide, diesel concerns look overblown, for now.

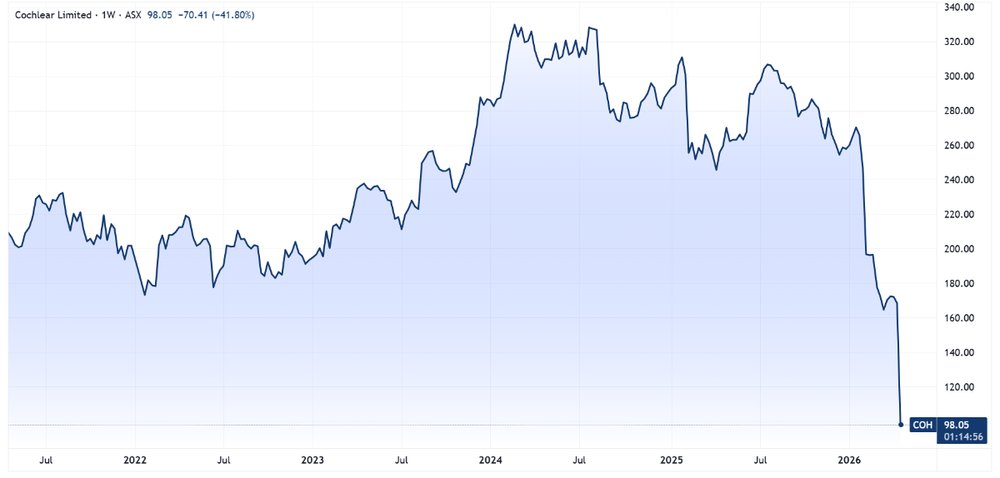

Is that a crypto chart? No it’s Cochlear

Cochlear faced absolute annihilation this week, down 40.7% on Wednesday after the company issued a dire profit downgrade due to deteriorating market conditions in the US and Europe.

The key numbers include:

FY26 underlying net profit guidance now set at $290-330m vs. prior $435-460m (a ~30% downgrade at the midpoint)

UBS FY26 ests were already sitting at US$408m prior to the update (~24% miss)

Cochlear did $195m in underlying net profit in 1H26, so new guidance implies just $95-135m in the second half, suggesting a sharp 41% half-on-half decline and also down 38% compared to 1H25

Cochlear cited an unexpected sharp drop in US sales in mid-February, hospital capacity constraints in the UK and Germany, industrial activity in Italy and Spain

The thing is, Cochlear opened 32.1% lower and spent most of the session grinding lower to a 40.7% decline. Volumes were insane, with 4.7 million shares traded or 820% daily average volumes of just ~511,000. Despite being extremely oversold, the stock dipped another 4.6% the next day.

There’s always a lot to learn about such destabilising downgrades.

When there’s one downgrade, there are usually more

Buying after a downgrade because the stock looks ‘cheap’ or ‘oversold is usually a bad idea

The stabilising and/or bottoming process for the share price can be a long, long process

At the top of my head, there are plenty of relatively large cap names that I swear, have done nothing but trend lower off the back of deteriorating earnings and/or sector-specific challenges in recent years – think Sonic Healthcare, Treasury Wine, Bapcor, Inghams, Endeavour Group, Air New Zealand and more.

I’m worried about inflation

I'm sure we've all started to notice inflation creep into our day-to-day lives, beyond the pump. Some notable ones/headlines would've been Coles raising the price of its private label milk from $1.65 to $1.85 per litre, while in building products, various manufacturers have lifted prices on things like plastic pipes and toilet seats by 30–35%.

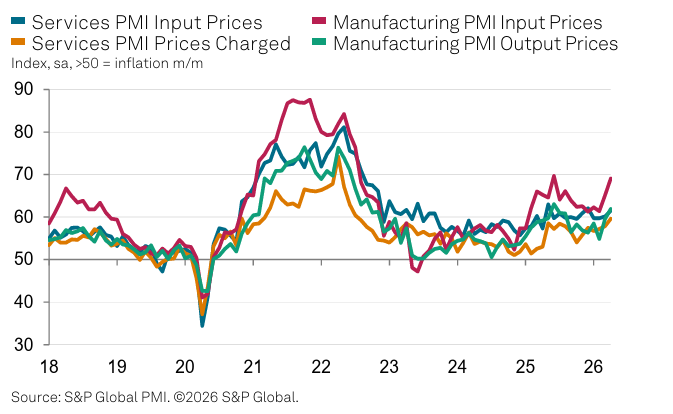

This week's S&P Global PMIs showed resilient activity across manufacturing and services, but the more concerning takeaway was the rather aggressive pickup in cost inflation. Here are some of the cost-related commentary from the reports:

US (chart above): "Average prices charged for goods and services rose in April at the fastest rate since July 2022 ... service sector selling price inflation also accelerated to reach a 45-month high."

UK: "Input cost inflation continued to accelerate sharply and was the highest since November 2022. This was led by a rapid increase in raw material prices in the manufacturing sector. Service providers also experienced a surge in cost pressures, largely due to higher fuel prices."

Eurozone: "Input costs increased at the fastest pace since the end of 2022. Rates of cost inflation quickened across both goods and services, but manufacturers registered the sharper rise. In turn, output price inflation hit a 37-month high. Selling prices increased particularly sharply in Germany, but stronger inflation was also seen in France and across the rest of the single currency bloc as a whole."

Australia: Cost inflation accelerated for a third consecutive month to its highest since August 2022, driven by fuel and shipping costs. Charge inflation hit a 3.5-year high as firms passed costs through

Japan: Input cost inflation hit its sharpest rate since January 2023, driven by staff, raw materials, fuel and energy costs linked to the Middle East and a weak yen. Output charge inflation hit a record high in data going back to late 2007.

This is not a good look for upcoming CPI data.

Last laughs

The S&P 500 held up quite well this week, including a fresh all-time high on Wednesday. What did we get? A four day skid. An absolute timeless classic of US markets up, ASX down.