Hi there!

The ASX 200 traded slightly lower this week, but miners faced a bloodbath on Friday ... there's always gotta be some turmoil under the hood, eh?

The Materials sector fell almost 3% for the week to close smack bang on the key 200-day moving average. A strange sequence of events too, given the macro backdrop mostly worked in the resource sector's favour. Both US CPI and PPI came in cooler than expected, and oil prices flat-lined after a two-day spike to start the week.

Elsewhere, markets are starting to look rather shaky, with the Nasdaq starting to roll over and KOSPI down ~25% from all-time highs. Perhaps reporting season can sprinkle in some much needed optimism for stocks.

Let's dive in.

Investor sentiment survey

.png)

A mildly positive result for the week ended 12 July, with bearishness dropping below 30% for the first time since 21 June. The move was all on the bearish side, with 4.3 pp of bears shifting into neutral. This marks the third straight week of bears falling, the most sustained move since September last year.

Over the next three months, do you expect the Australian stock market to be:

Cashed up and cheap but a microcap

Experience Co announced on Wednesday a deal to sell its skydiving business for $65 million, comprising $41 million cash, a $5 million vendor note (repaid after five years) and a 32.5% stake in a new joint-venture company (valued at ~$19m).

The stock rallied 25% on the day to 10 cents, giving it a market cap of roughly $75 million, or an enterprise value of $88 million once you add in the $13 million net debt. On a pro-forma basis, that deal drops EV to $47 million (ex-note and NewCo equity).

Here's the kicker. The skydiving business contributed ~45% of group revenues and 40% of EBITDA at the 1H26 result, so they've effectively sold less than half the overall business for ¾ of today's EV.

What you're left with is a business that's now net cash, simpler (just Adventure Experiences, comprised of reef and treetops) and trading at a much cheaper multiple. With a cash balance like that, buybacks and special dividends should come into question too.

But then again, these are microcaps we're talking about, and value on the table doesn't always translate into investment returns.

Coles, you've made the right decision

When Coles confirmed its discussions with TPG over a potential acquisition of pet care company Greencross on 1 July, the stock tumbled ~4% in a "please, please don't do this" moment.

Coles is already operating in an oligopoly, and now looking to acquire a pet business for ~$4 billion, a company TPG picked up for just under $1 billion seven years ago, and a sizeable deal relative to Coles' $30 billion market cap. Those M&A fears drove a fairly wide and otherwise unwarranted underperformance against Woolworths, around 5pp.

Then on Friday, Coles said it had ceased discussions with TPG, sending the shares up as much as 5% and narrowing what's supposed to be a narrow performance gap.

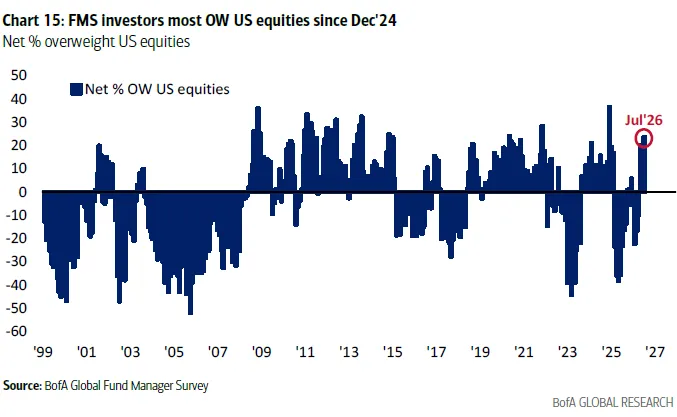

BofA’s monthly survey

Never a dull moment in Bank of America's monthly global fund manager survey.

FMS sentiment most bullish since February on optimism around a macro boom, AI capex and a dovish Fed, with the US equity overweight the largest since December 2024

Cash levels fell 0.5 percentage points to 3.6%, the lowest since February 2026, and the Bull and Bear Indicator hit 9.4, an extreme bull reading

BofA recommended reducing equity and high-beta exposure, warning summer upside for risk assets is stymied by bull positioning

A record 54% saw "no landing" as the most likely outcome, while a net 4% now expect lower global inflation, down from net 45% expecting higher inflation last month

An AI bubble overtook a second inflation wave as the biggest tail risk, and 82% called long global semiconductors the most crowded trade, though a net 48% said AI stocks are not in a bubble

Can China pop the AI bubble?

Every industry China has entered has seen profit margins collapse. Think EVs, solar panels, steel, consumer electronics ... the list goes on. Yet somehow people believe AI will be the exception.

Here's the current state of play:

Market share: Chinese AI models have accounted for more than 30% of US-originating token traffic on OpenRouter every day since Feb 8, peaking at 46%, up from 4.5% in the first half of 2025.

Price: DeepSeek V4 Flash costs $0.09 per million input tokens vs ~$5 for GPT-5.5 and Claude Opus 4.8. That's ~55× cheaper.

Performance: Zhipu's open-weight GLM 5.2 finished within 1ppt of Opus 4.8 on the FrontierSWE benchmark, at ~20% lower cost.

Adoption: Programming workloads rose from 11% of OpenRouter usage in early 2025 to more than 50% by mid-2026.

Chinese models now offer comparable performance at a fraction of the cost while rapidly gaining market share, despite the US spending hundreds of billions on AI infrastructure. Let's see how this plays out ...

Last laughs

Koreans are built different – they received the largest ever wealth boom from Samsung and SK Hynix … and immediately rolled that into 3x leveraged positions and got wiped out.

Goldman Sachs notes: “As of July 13, a total of over 1.2 million leveraged retail accounts across the Korean market triggered margin calls. Approximately 320,000–360,000 accounts were fully liquidated by brokers. South Korea has an adult population (aged 15–64) of 35.7 million people… i.e. 1 in 30 (3.4%) adults got margin called."

It really is Squid Game out there.