Judo Capital, El Nino's and US valuations

Hi there!

Another downbeat week for Aussie markets. The ASX 200 finished lower on four of five days, while miners finally snapped a six-day losing streak. Offsetting some of that weakness were gains of 3-5% across consumer-facing and defensive sectors like Healthcare, Staples and Discretionary.

Probably the most interesting story to cross the desk this week was Apple and Microsoft handing down price increases, both blaming AI data centre demand for driving memory and storage chip costs sharply higher. In the US, various Xbox, MacBook and iPad models are now up 16-25%, stoking concerns of a third wave of inflation. C'mon AI, you were supposed to destroy inflation, not cause it.

This week, we take a closer look at Judo's massive one-day decline and what the upcoming El Niño means for the economy (gosh it sucks to be a consumer).

Let’s dive in.

Investor sentiment survey

.png)

Judo in freefall

Judo faced absolute annihilation on Thursday after downgrading both FY26 and FY27 earnings expectations. The stock fell 40.3% in a single session, and at some point, was down as much as 46.5%.

At face value, it was a sizable cut to FY26 profit before tax expectations, and a very material downgrade for FY27.

FY26 PBT guided to $163-169m, down from prior lower-end guidance of $180-190m and below ests of $180.7m (8% miss at midpoint)

Cost of risk now expected at $116-122m, driven by specific provision increases across three exposures in different sectors

Second half NIM lifted to over 3.2% vs. prior 3.15% guidance

CET1 of 12.4% and second half cost-to-income on track to come in below first half of 48.5%

FY27 PBT guided to $210-220m, well short of ests of $255.1m (16% miss at midpoint)

What made the selloff worse was a couple of things:

Analysts loved the stock. 12 of 13 sell-side ratings were Buy rated, with an average target price of $2.14. With optimism and expectations so high, the stock cannot afford to announce a downgrade that hit both FY26 and FY27.

No issues at the recent Q3 update. Judo's Q3 update in late April reaffirmed the prior $180-190m guidance, so the market was completely blind-sided by this.

Management held a Q&A on Thursday afternoon and some of the key takeaways include:

CEO Chris Bayliss framed the downgrade as isolated, telling analysts the three exposures are "borrower-specific issues for three different reasons"

On exposure size, Bayliss said the exposure at default across the three is "around about somewhere between sort of 70 million and 80 million", not evenly spread, with one relatively large and well-secured loan

On the loans not surfacing in the Q3 review, Bayliss said they had no line of sight, adding they "deteriorated very rapidly" and one borrower went into voluntary administration without being significantly in arrears

The three are a mix of financial planning, a window manufacturer (working capital) and one property-backed loan

Here comes El Niño

With the US-Iran conflict and energy crisis now in the rear-view mirror, we've got another inflationary problem on our hands: El Niño.

The US National Oceanic and Atmospheric Administration sharply raised its June forecast for a strong or record El Niño, expecting Pacific sea surface temperatures to climb more than 2 degrees in coming months.

Citi sees agriculture price risks heavily skewed to the upside over the next 6 to 12 months, with the main uncertainty being the severity of the weather hit to global food production.

Prior very strong events in 1997-98 and 2015-16 caused large drops in global agricultural yields

Cocoa flagged as the key El Niño play given its production is concentrated in the most weather-exposed regions

Sugar yields at risk from drought across India, Thailand, Australia and elsewhere, with a weaker Indian monsoon set to cut cane yields

Citi notes the link to food inflation is weak immediately but strengthens at a 4 to 5 month lag (0.65 correlation), with import-reliant countries most exposed to pass-through

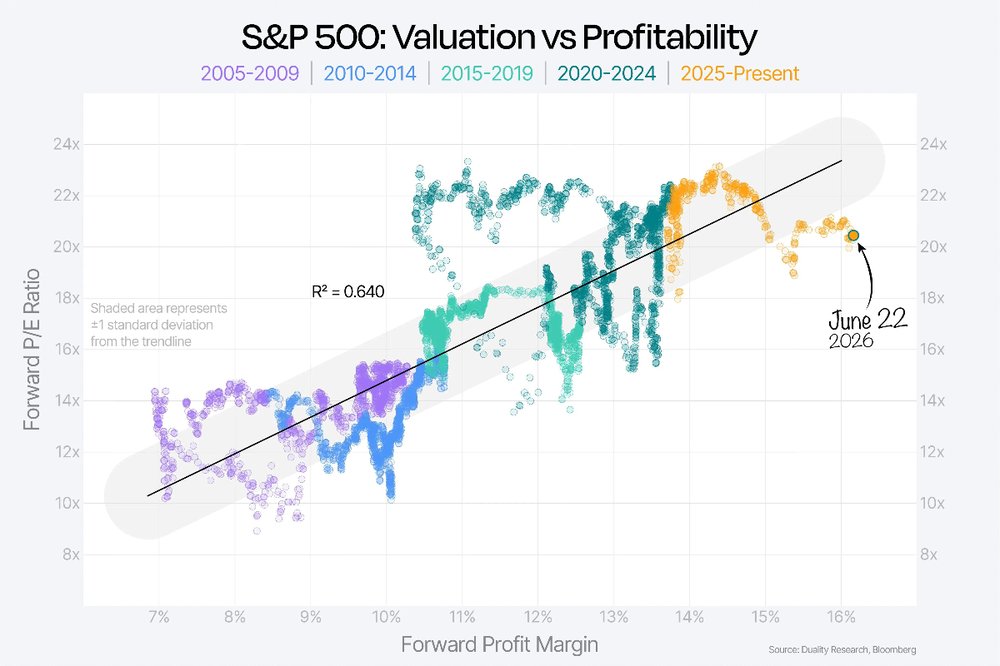

S&P 500 valuations vs. profitability

A short post, but a very cool chart from Duality Research, which noted that at today's record margin levels, the model would typically point to a valuation closer to 23x earnings. Instead, the market is trading about 1.5 standard deviations below its long-term regression trend.

In plain terms: When companies are this profitable, the premium investors pay for shares should be much higher. Yet, investors are pricing stocks as if they're worried.