Here come's a commodity bull market

Hi there!

I’m back after a two week break – funny how the ASX 200 got nuked 1.6% the day after I left (Fri, 21 Nov). It’s managed to bounce and is currently loitering around the 200-day moving average, not really bullish or bearish, just trading sideways before its next directional move.

Despite broader market weakness, I've observed many data points and commentary suggesting a solid outlook for commodities heading into 2026. I've outlined a few key talking points below that could serve as useful starting points for further research.

Let’s dive in.

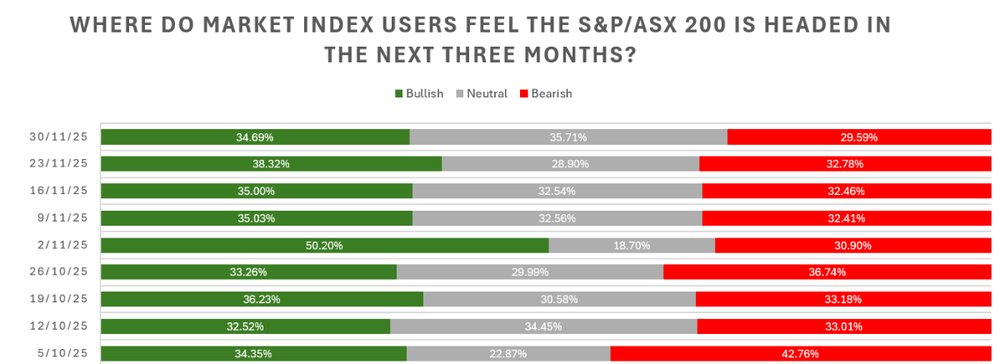

Investor sentiment survey

Bullish resources

The resource complex is looking very bullish heading into 2026.

ASX 200 Materials Index up 26% YTD, trading at all-time highs after ~4 years of sideways movement

Bloomberg Commodity Index trading at the highest since January 2023 after almost three years of consolidation

There are a lot of moving parts, but I’ll try to give a succinct summary of the bull case for major commodities.

Iron ore: Despite widespread bearish sentiment, iron ore has traded around US$105 per tonne for most of this year, defying analyst expectations. While there's no strong fundamental bull case beyond contrarian positioning, the key upside driver is that consensus forecasts remain in the low-to-mid US$90s, suggesting material upside potential from current spot pricing (e.g. FMG's FY26e free cash flow soars from 5.0% (consensus pricing) to 8.6% (spot pricing), according to Morgan Stanley).

Copper: Global supply has been reduced by 5-6% in recent months through major disruptions including QB2 (~100kt), Grasberg (~500kt), Kamoa-Kakula (~200kt), and Cobre Panama (~330kt lost in 2023). The recent approval of Harmony's Eva Copper Project, requiring ~$3 billion capex for low-teens IRR, shows just how valuable it is to get supply online.

Gold: Bullion continues its strong momentum supported by multiple tailwinds including the debasement trade, ETF inflows, and sustained central bank buying.

Aluminium: (more details in the section below)

Lithium: After a significant rally that saw some producers like Pilbara Minerals rise nearly 4x in five months, prices are starting to pull back. However, recent positive catalysts include China's lithium royalty reform, which raises the sector's cost floor, and MinRes' 30% lithium asset sale to POSCO at A$3.9 billion or a 45% above consensus valuations of A$2.7 billion.

Uranium: The sector, in theory, should offer relatively asymmetric upside given AI's growing electricity demands. Recent commentary from Nvidia's CEO predicting widespread adoption of small nuclear reactors for AI systems adds to the bullish case, though investors should note uranium's historical volatility (it's really good at doubling, then halving).

The bottom line: The sector's moving out after a prolonged consolidation. Watch this space.

AI's stain on commodities

Here’s a closer look at how AI and data centres are squeezing the aluminium industry.

AI data centres are outbidding US aluminium smelters for electricity, paying over US$100 per MWh vs. the US$30-40 per MWh smelters need to operate profitably.

US aluminium production is tiny, with only four commercial smelters producing under 1% of global supply and at full capacity covering just a third of domestic demand.

Aluminium prices are forecast to fall 15% by Q4 2026 as international supply rises, squeezing margins for domestic producers.

High electricity costs make new investment unattractive, potentially forcing producers like Alcoa to sell assets to companies that can use the power more efficiently.

Despite market expectations of falling aluminium prices, they're actually up 13% YTD and trading at levels not seen since June 2022!

What in the capital raise

Vulcan Energy completed a wild capital raise – the numbers will shock you. No seriously.

Raised A$1.08 billion (vs. its market cap of $1.4 billion) at A$4.00 per new share or a 34.7% discount to its last closing price

Will issue 269 million new shares, more than double its current 234 million existing shares

Post-dilution, Vulcan shareholders will own approximately 70% of its forecast Lionheart project NPV (since kfW and industrial investors have taken ~14% and ~15% respectively)

Not only are they raising a bucketload of cash but project economics have been revised sharply lower, including:

Post-tax NPV from €2.17 billion to €1.15 billion and unlevered IRR from 20.7% to 13.7%

These project economics still assume lithium hydroxide prices of ~ US$24,000 a tonne, which is almost double spot prices (and well-below long-term price forecasts that typically sit around US$15-20,000)

First production was delayed from 2H27 to 2H28, while the project’s power source is now internalised, raising further capex and opex concerns

Lionheart forecast to have the “lowest-quartile” C1 costs, but may be optimistic given the project’s $4 billion capex and capex intensity relative to established peers

I think another way to look at this is that a) Europe is desperately trying to establish a domestic lithium supply chain and b) lithium prices likely need to move higher for projects like this to make economic sense. Nevertheless, Vulcan faces a high-stakes, high-risk path forward.

JPMorgan’s oil prediction

Shortly after Russia invaded Ukraine in 2022, JPMorgan warned oil prices could reach a "stratospheric" US$380 per barrel if Western sanctions prompted retaliatory Russian output cuts.

Fast forward to today, and the same investment bank is forecasting oil could fall to US$30 per barrel by 2027 amid a growing surplus.

When a forecast sounds too outrageous, it probably is (much like backing a 10-leg multi).

Interestingly, I'm quietly bullish on oil from 2027 onwards. Goldman Sachs expects the oil market to face a surplus in 2026 as OPEC's final major supply wave hits the market. However, this all-too-familiar structural setup could lead to higher prices in the medium-term, driven by years of underinvestment in long-cycle projects, declining Russian supply, ongoing demand growth, and the absence of another major US shale boom.

The other compelling factor is sentiment, as everyone is overwhelmingly bearish. Much like iron ore, being contrarian may well pay off.

Last laughs

Apparently OpenAI is ready to roll out ads in ChatGPT responses. We’re so screwed.